Understanding how to calculate monthly interest is a cornerstone of sound personal and business finance. Whether you’re assessing the cost of a loan, projecting the growth of your savings, or dissecting a credit card statement, the ability to accurately determine monthly interest empowers you to make informed financial decisions. This article delves into the intricacies of monthly interest, providing practical methods, formulas, and insights to demystify this critical financial concept.

The Fundamentals of Interest: Annual vs. Monthly Rates

Before diving into calculations, it’s essential to grasp the basic concepts of interest and how annual rates translate into monthly figures. Interest is fundamentally the cost of borrowing money or the return on lending/investing money.

Annual Percentage Rate (APR) and Annual Equivalent Rate (AER)

Most financial products, especially loans and credit cards, quote an Annual Percentage Rate (APR). The APR represents the annual cost of borrowing, including any additional fees, expressed as a yearly percentage. For savings and investments, you might encounter the Annual Equivalent Rate (AER), which accounts for compounding interest over a year, giving you a truer picture of the annual return.

While APR and AER are annual figures, our financial lives often unfold on a monthly basis – monthly payments, monthly statements, monthly contributions. Therefore, converting these annual rates into their monthly equivalents is the first crucial step in understanding monthly interest.

Simple vs. Compound Interest

The nature of interest also significantly impacts its monthly calculation.

- Simple Interest: Calculated only on the principal amount (the initial sum borrowed or invested). The interest earned or owed does not become part of the principal for subsequent interest calculations. It’s often used for short-term loans or basic savings accounts.

- Compound Interest: Calculated on the principal amount and on the accumulated interest from previous periods. This “interest on interest” effect means your money grows (or your debt increases) at an accelerating rate. Most savings accounts, investments, and long-term loans (like mortgages) use compound interest. The frequency of compounding (daily, monthly, quarterly, annually) plays a significant role in the total interest accrued.

Understanding these distinctions is vital, as the method for working out monthly interest will vary depending on whether the interest is simple or compounded, and what the compounding frequency is.

Core Methods for Calculating Monthly Interest

Calculating monthly interest involves a few standard formulas, each tailored to different financial scenarios. The key is to correctly identify your annual interest rate, the principal amount, and the compounding frequency.

Method 1: Simple Monthly Interest Calculation

Simple interest is the most straightforward to calculate. It’s often used for short-term loans, basic savings accounts, or when you need to quickly estimate interest without considering compounding.

Formula:

Monthly Simple Interest = (Principal Amount × Annual Interest Rate) / 12

Explanation:

- Principal Amount (P): The initial sum of money borrowed or invested.

- Annual Interest Rate (R): The yearly interest rate, expressed as a decimal (e.g., 5% becomes 0.05).

- Divide by 12: To convert the annual interest into a monthly figure.

Example:

Imagine you take out a simple, short-term personal loan of $5,000 at an annual simple interest rate of 8%.

Monthly Simple Interest = ($5,000 × 0.08) / 12

Monthly Simple Interest = $400 / 12

Monthly Simple Interest = $33.33

This means you would owe $33.33 in interest each month, in addition to any principal repayment.

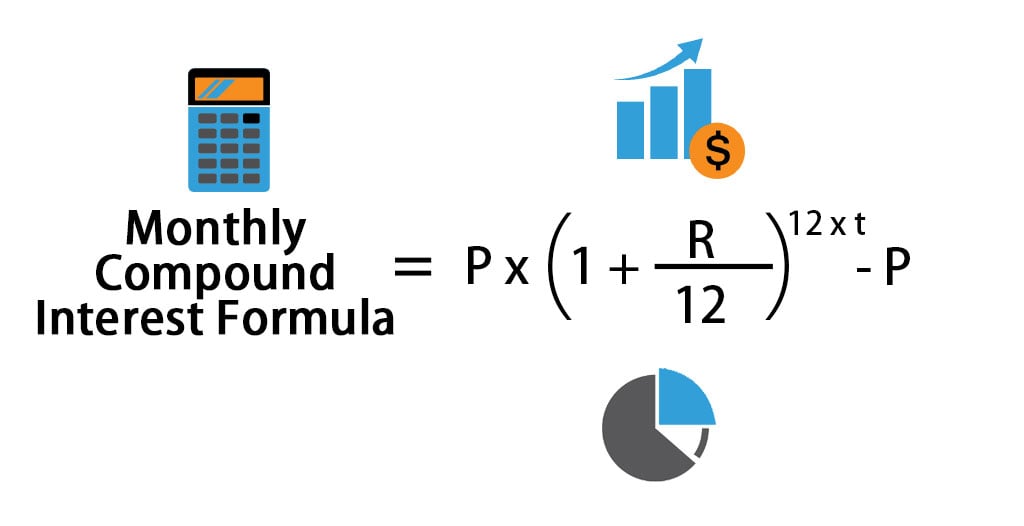

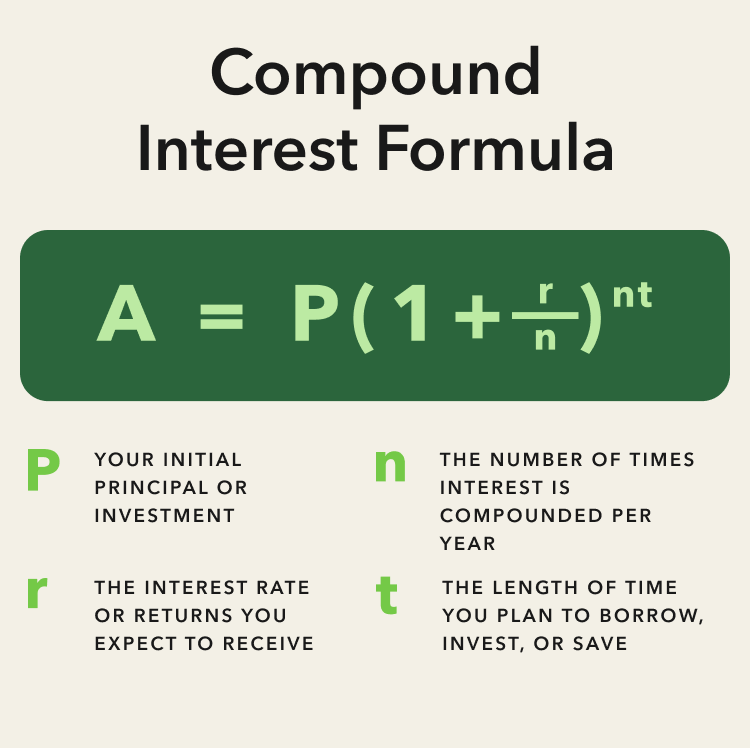

Method 2: Compound Monthly Interest Calculation

Most real-world financial products, from savings accounts to mortgages and credit cards, involve compound interest. The “interest on interest” effect can significantly alter the total amount of interest over time. When interest is compounded monthly, it means that the interest earned (or charged) in one month is added to the principal, and the next month’s interest is calculated on this new, larger principal.

Formula:

Monthly Interest Rate (as a decimal) = Annual Interest Rate (as a decimal) / 12

Once you have the monthly interest rate, you can calculate the interest for a given month or project future balances.

For a single month’s interest (when compounding monthly):

Monthly Interest = (Previous Month’s Balance × Monthly Interest Rate)

Example (Savings Account):

Let’s say you have a savings account with a starting balance of $10,000 and an Annual Percentage Yield (APY) or AER of 3%, compounded monthly.

-

Calculate the monthly interest rate:

Monthly Interest Rate = 0.03 / 12 = 0.0025 -

Interest for the first month:

Interest = $10,000 × 0.0025 = $25.00

New Balance after 1st month = $10,000 + $25.00 = $10,025.00

- Interest for the second month (compounding effect):

Interest = $10,025.00 × 0.0025 = $25.06

New Balance after 2nd month = $10,025.00 + $25.06 = $10,050.06

Notice how the interest earned slightly increased in the second month due to compounding. This effect accelerates over time, demonstrating the power of compound interest for investments and the increasing cost for debts.

Method 3: Calculating Credit Card Interest

Credit card interest calculation can be a bit more complex due to varying balances throughout the billing cycle and grace periods. Most credit card companies use the “Average Daily Balance” method.

Steps:

- Find your Annual Percentage Rate (APR).

- Convert APR to a daily periodic rate: Daily Rate = APR / 365.

- Calculate your Average Daily Balance (ADB): This involves summing the balance for each day in the billing cycle and dividing by the number of days in the cycle. Any payments or new purchases will affect the daily balance.

- Calculate Monthly Interest: Monthly Interest = Average Daily Balance × Daily Rate × Number of days in the billing cycle.

Example (Simplified Credit Card):

Assume your credit card has an APR of 20% and a 30-day billing cycle. Your Average Daily Balance for the cycle was $1,500.

- Daily Rate: 0.20 / 365 = 0.0005479 (approximately)

- Monthly Interest: $1,500 × 0.0005479 × 30 = $24.66

Important Considerations for Credit Cards:

- Grace Period: If you pay your statement balance in full by the due date, most credit cards offer a “grace period” during which no interest is charged on new purchases. However, if you carry a balance, you lose this grace period, and interest is often charged from the date of purchase.

- Promotional Rates: Be aware of introductory rates and when they expire, as your interest rate can jump significantly.

- Cash Advances: Cash advances typically do not have a grace period and start accruing interest immediately, often at a higher rate than purchases.

The Impact of Understanding Monthly Interest

Beyond the raw calculations, grasping how monthly interest works has profound implications for your financial well-being. It transforms abstract percentages into tangible costs or gains, enabling smarter decision-making.

Informing Borrowing Decisions

When taking out a loan, understanding monthly interest allows you to:

- Compare Loan Offers: You can accurately compare the true monthly cost of different loans, not just their advertised APR, especially when factoring in compounding.

- Evaluate Affordability: Knowing the monthly interest component helps you determine if the total monthly payment (principal + interest) fits within your budget.

- Minimize Debt Costs: By recognizing how compounding interest on debt can snowball, you’re motivated to pay down high-interest loans (like credit cards) more aggressively.

Maximizing Savings and Investments

For savers and investors, monthly interest calculations are equally crucial:

- Projecting Growth: You can accurately forecast how your savings or investments will grow over time, especially with monthly compounding. This helps in setting realistic financial goals.

- Understanding APY/AER: A higher compounding frequency (e.g., monthly vs. annually) will result in a higher Annual Equivalent Rate (AER) even if the nominal annual rate is the same. Understanding this helps you choose the best savings products.

- Appreciating Time Value of Money: The “interest on interest” effect highlights the power of starting early with investments and letting compound interest work its magic over decades.

Budgeting and Financial Planning

Monthly interest directly impacts your cash flow.

- Accurate Budgeting: Incorporating exact monthly interest payments for loans and credit cards into your budget ensures you have a realistic picture of your expenses.

- Debt Repayment Strategies: Understanding how much of your monthly payment goes towards interest versus principal allows you to devise effective strategies for accelerating debt repayment. Paying even a little extra each month can significantly reduce the total interest paid over the life of a loan.

- Retirement Planning: When planning for retirement, projecting the growth of your investments based on monthly compounding helps in determining how much you need to save and for how long.

Practical Tools and Strategies for Managing Interest

While manual calculations are valuable for understanding, various tools can simplify the process and aid in effective interest management.

Utilizing Online Calculators and Spreadsheets

- Online Loan/Savings Calculators: Numerous free online calculators can instantly compute monthly payments, total interest paid, or future savings balances. These are invaluable for quick estimates and comparisons.

- Spreadsheets (Excel/Google Sheets): For more detailed analysis, spreadsheets offer immense flexibility. You can set up amortization schedules for loans, track investment growth, and model different interest rate scenarios. Functions like

PMT(for loan payments) andFV(for future value of investments) are particularly useful.

Strategies for Minimizing Interest Paid (Debt)

- Pay More Than the Minimum: Even a small extra payment each month can dramatically reduce the total interest paid and shorten the loan term, especially for high-interest debts.

- Consolidate High-Interest Debt: If you have multiple high-interest debts, consider consolidating them into a single loan with a lower interest rate.

- Refinance Loans: If interest rates have dropped or your credit score has improved, refinancing a mortgage or personal loan can secure a lower monthly interest payment.

- Understand Your Billing Cycles: Pay attention to credit card billing cycles and due dates to avoid interest charges by paying your full statement balance.

Strategies for Maximizing Interest Earned (Savings/Investments)

- Shop for High-Yield Accounts: Look for savings accounts, CDs, or money market accounts that offer competitive Annual Percentage Yields (APYs) and compound interest frequently.

- Automate Savings: Set up automatic transfers to your savings or investment accounts. Consistent contributions, combined with compound interest, lead to significant growth over time.

- Invest Early and Consistently: The longer your money is invested, the more time compound interest has to work its magic. Regular contributions further accelerate this growth.

- Understand Investment Fees: Be aware of any fees associated with your investments, as these can eat into your monthly and annual returns.

Conclusion

Mastering the art of working out monthly interest is not just an academic exercise; it’s a fundamental financial literacy skill that directly impacts your wealth and financial freedom. By understanding the distinction between simple and compound interest, converting annual rates to monthly equivalents, and applying the correct formulas for various scenarios, you gain invaluable insight into your financial landscape.

From making astute borrowing decisions and diligently paying down debt to intelligently growing your savings and investments, a solid grasp of monthly interest empowers you to take control of your financial destiny. Armed with this knowledge and the right tools, you can navigate the complexities of personal finance with confidence, clarity, and control.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.