Understanding the “Future Value” (FV) of money is one of the most transformative concepts in personal and business finance. At its core, it answers a fundamental question: “How much will the money I have today be worth at a specific point in the future?” Whether you are an individual planning for retirement, an entrepreneur weighing a new business venture, or an investor comparing different asset classes, mastering the calculation of future value allows you to make decisions based on mathematical reality rather than guesswork.

This article delves into the mechanics of future value, the importance of the Time Value of Money (TVM), and how you can apply these calculations to build a more secure financial future.

The Fundamentals of Future Value and the Time Value of Money

Before diving into the formulas, it is essential to understand the underlying philosophy: The Time Value of Money. This principle states that a dollar today is worth more than a dollar tomorrow. Why? Because a dollar today can be invested to earn interest or capital gains. If you hide $1,000 under a mattress for ten years, its nominal value remains $1,000, but its purchasing power will likely have decreased due to inflation, and you will have missed out on ten years of potential growth.

Defining Future Value

Future Value is the value of a current asset at a specified date in the future based on an assumed rate of growth. It is a projection used to estimate the magnitude of an investment’s increase over time. By calculating FV, investors can determine if the eventual payout of an investment justifies the current expenditure and the risks involved.

Simple vs. Compound Interest

There are two primary ways interest can accrue, and they drastically change the future value of your money.

- Simple Interest: This is calculated only on the initial principal. If you invest $100 at a 10% simple interest rate, you earn $10 every year.

- Compound Interest: This is often called “the eighth wonder of the world.” Interest is calculated on the initial principal and also on the accumulated interest of previous periods. In the same $100 example, in year two, you earn 10% on $110, not just the original $100. Over long periods, compounding creates exponential growth that simple interest cannot match.

The Role of the Discount Rate

In future value calculations, the interest rate is often referred to as the “discount rate” or the “opportunity cost.” It represents the rate of return you could earn on an alternative investment of similar risk. Choosing the right rate is crucial; a slight variation in the assumed interest rate can lead to vastly different future value projections over twenty or thirty years.

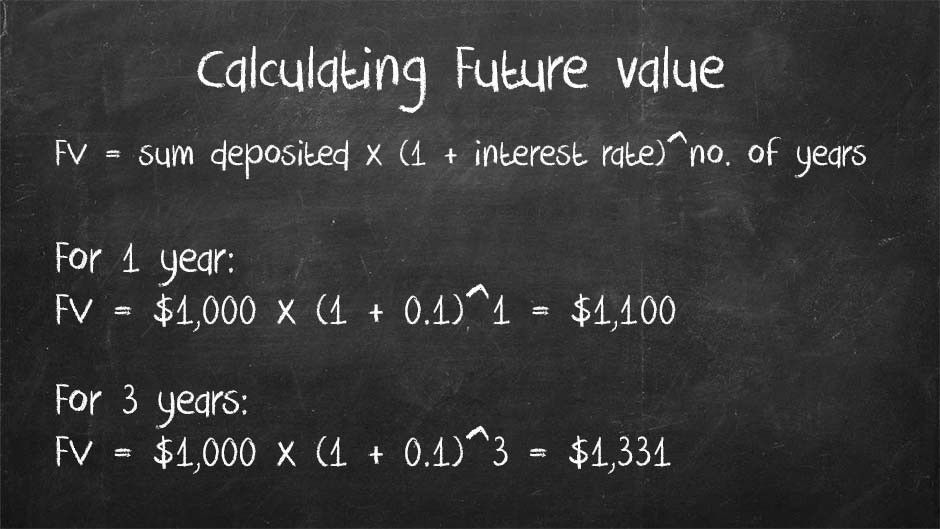

The Mathematics: How to Calculate Future Value

Calculating future value can be done through a standard mathematical formula. While modern software handles much of this, understanding the manual calculation provides a deeper intuition for how your wealth grows.

The Standard Future Value Formula

The basic formula for Future Value is:

FV = PV × (1 + r)^n

Where:

- FV: Future Value

- PV: Present Value (the amount of money you have now)

- r: Periodic interest rate (expressed as a decimal, so 5% becomes 0.05)

- n: Number of compounding periods (years, months, etc.)

Understanding the Variables

Each variable in this equation acts as a lever.

- Present Value (PV): The more you start with, the higher the FV. This is the “seed” of your financial garden.

- Interest Rate (r): This is the “growth hormone.” Even a 1% or 2% difference in annual returns can result in hundreds of thousands of dollars in difference over a 40-year career.

- Time (n): This is perhaps the most powerful variable. Because n is an exponent, time has a disproportionate impact on the final result. This is why financial advisors stress starting to save as early as possible.

Practical Examples

Imagine you have $10,000 to invest for 10 years at an annual interest rate of 7%.

Using the formula:

FV = 10,000 × (1 + 0.07)^10

FV = 10,000 × (1.967)

FV = $19,671.51

In ten years, your money has nearly doubled. If you were to extend that time frame to 20 years, the value wouldn’t just double again; it would grow to approximately $38,696.84, thanks to the compounding effect.

Advanced Considerations: Inflation and Taxes

A common mistake in financial planning is looking at the nominal future value—the raw number—without considering what that money will actually buy. To get a realistic picture of your future wealth, you must adjust for external economic factors.

The Impact of Purchasing Power

Inflation is the steady increase in prices and the subsequent fall in the purchasing value of money. If your investment returns 5% annually, but inflation is 3%, your “real” rate of return is only about 2%. When working out future value for long-term goals like retirement, failing to account for inflation can lead to a significant shortfall in your standard of living.

Nominal vs. Real Future Value

To calculate the “Real Future Value,” you should subtract the expected inflation rate from your nominal interest rate.

- Nominal FV: The dollar amount you will see in your bank account.

- Real FV: The value of that future money in today’s purchasing power.

Professionals often use a “Real” rate of 4–5% for stock market projections (assuming a 7–8% historical return minus 2–3% inflation) to keep their expectations grounded.

Tax Implications on Gains

Unless your money is in a tax-advantaged account like a Roth IRA or a 401(k), the government will take a portion of your earnings. Capital gains taxes and income taxes can eat into your compounding. When calculating future value for investments in taxable brokerage accounts, it is wise to use an “after-tax” interest rate to ensure your projections are accurate.

Tools and Methods for Financial Projection

While the manual formula is vital for understanding the concept, various tools can help you perform these calculations quickly and incorporate more complex variables, such as monthly contributions.

Using Excel and Financial Calculators

Microsoft Excel and Google Sheets have a built-in function for this: =FV(rate, nper, pmt, [pv], [type]).

- Rate: Interest rate per period.

- Nper: Total number of payment periods.

- Pmt: The payment made each period (if you are adding money regularly).

- PV: The present value.

This tool is particularly useful for calculating the future value of an annuity—a series of equal payments made at regular intervals.

The Rule of 72

For quick mental math, investors use the “Rule of 72.” By dividing 72 by your annual interest rate, you can estimate how many years it will take for your initial investment to double.

- At 6% interest, your money doubles in 12 years (72/6).

- At 10% interest, your money doubles in 7.2 years (72/10).

This is a helpful shorthand for comparing different investment opportunities on the fly.

Scenario Planning for Retirement

Future value isn’t just a single number; it’s a range of possibilities. Professional financial planners use “Monte Carlo Simulations,” which run thousands of FV calculations using different randomized interest rates to determine the probability of reaching a financial goal. When working out your own future value, it is smart to run “Best Case,” “Worst Case,” and “Most Likely” scenarios.

Strategic Application in Personal Finance

Knowing how to calculate future value is only useful if you apply it to your financial strategy. It serves as a compass for your long-term economic journey.

Evaluating Investment Opportunities

Should you pay off a 4% mortgage early or invest that money in the stock market with an expected 7% return? By calculating the future value of both paths, the math usually favors the higher interest rate. However, future value also helps you quantify the “cost” of safety. It allows you to see exactly how much potential wealth you are sacrificing when you choose a low-risk savings account over a higher-risk equity fund.

Planning for Long-term Goals

Whether it’s a child’s college fund or a down payment on a house, future value calculations help you work backward. If you know you need $100,000 in 15 years, you can use the FV concepts to determine exactly how much you need to invest today or contribute monthly to reach that target. This transforms vague “saving” into “targeted investing.”

Risks and Limitations of FV Models

It is important to remember that future value calculations are projections, not guarantees. The primary risks include:

- Sequence of Returns Risk: The order in which you receive your returns matters, especially if you are withdrawing money.

- Variable Rates: Real-world interest rates fluctuate; they are rarely a flat 7% every single year.

- Life Volatility: Unexpected expenses can interrupt the compounding process.

To mitigate these risks, always use conservative estimates for your interest rates and ensure you have an emergency fund so that you never have to “interrupt” your future value compounding during a market downturn.

Mastering the calculation of future value shifts your mindset from short-term spending to long-term wealth creation. By understanding how time, interest, and principal interact, you gain the clarity needed to navigate the complex world of personal finance with confidence.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.