Securing a business loan is often a pivotal moment for entrepreneurs, marking either the start of a new venture, an opportunity for significant growth, or a means to navigate challenging financial waters. While the prospect can seem daunting, understanding the process, requirements, and available options can transform a complex challenge into a strategic financial move. This comprehensive guide will demystify how to take out a business loan, providing insights and actionable steps to help you navigate the landscape of business finance effectively.

Understanding Business Loans: Types and Purposes

Before embarking on the application journey, it’s crucial to grasp the fundamental reasons businesses seek financing and the diverse array of loan products available. Not all loans are created equal, and choosing the right type can significantly impact your business’s financial health and trajectory.

Why Businesses Seek Loans

Businesses pursue loans for a multitude of reasons, each critical to their operational continuity and expansion:

- Startup Capital: New businesses often require substantial upfront investment for inventory, equipment, marketing, and operational expenses before generating revenue.

- Expansion and Growth: Existing businesses might seek funds to open new locations, launch new product lines, enter new markets, or scale up production.

- Working Capital: To cover day-to-day operational costs, manage cash flow fluctuations, or bridge gaps between invoicing and payment collection.

- Equipment Financing: Purchasing essential machinery, vehicles, or technology without depleting cash reserves.

- Inventory Purchases: Stocking up on goods to meet seasonal demands or capitalize on bulk discounts.

- Debt Refinancing: Consolidating existing high-interest debts into a single, more manageable loan with better terms.

- Emergency Funds: Addressing unforeseen expenses or navigating temporary revenue downturns.

Common Types of Business Loans

The financial market offers a variety of loan products, each tailored to different business needs and risk profiles:

- Term Loans: These are perhaps the most traditional form of business financing. A lump sum is provided upfront, which the borrower repays over a set period (term) with fixed interest rates. They are suitable for significant, one-time investments like equipment purchases or expansion projects.

- SBA Loans (Small Business Administration Loans): Government-backed loans offered through a network of lenders. The SBA guarantees a portion of the loan, reducing the risk for lenders and making it easier for small businesses to qualify for favorable terms, lower interest rates, and longer repayment periods. Popular programs include 7(a), CDC/504, and Microloans.

- Business Lines of Credit: Similar to a credit card, a line of credit provides access to a revolving pool of funds up to a certain limit. Businesses can draw upon these funds as needed, repaying what they borrow and then borrowing again. Ideal for managing short-term cash flow needs or unexpected expenses.

- Equipment Financing: A specialized loan used specifically for purchasing new or used business equipment. The equipment itself often serves as collateral, making it easier to secure for businesses with limited other assets.

- Invoice Factoring/Financing: Businesses sell their unpaid invoices to a third-party factor at a discount to get immediate cash. Alternatively, invoice financing uses outstanding invoices as collateral for a short-term loan. Both are excellent for improving cash flow, especially for businesses with long payment terms.

- Commercial Real Estate Loans: Used to purchase, refinance, or renovate commercial properties. These are typically long-term loans with the property serving as collateral.

- Merchant Cash Advances (MCAs): A lump sum payment given in exchange for a percentage of future credit card sales. While quick and accessible, MCAs often come with higher effective interest rates compared to traditional loans.

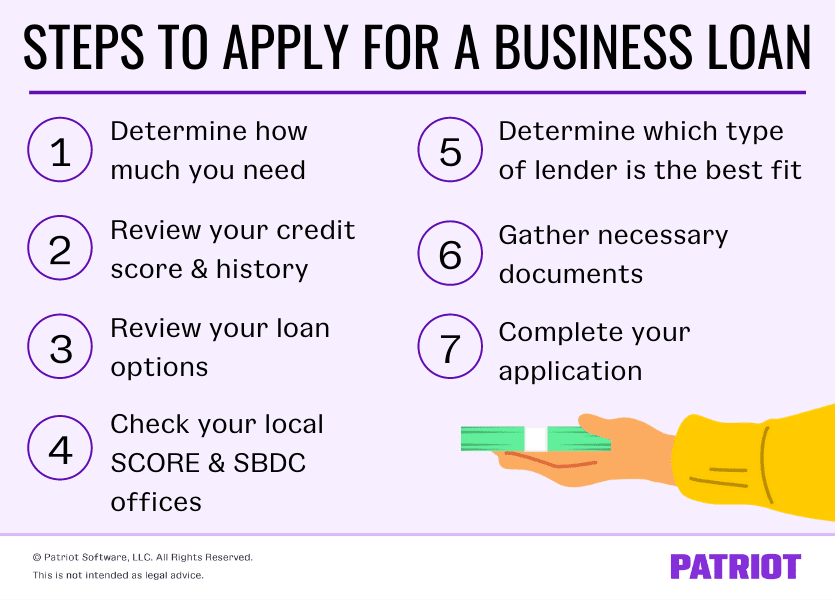

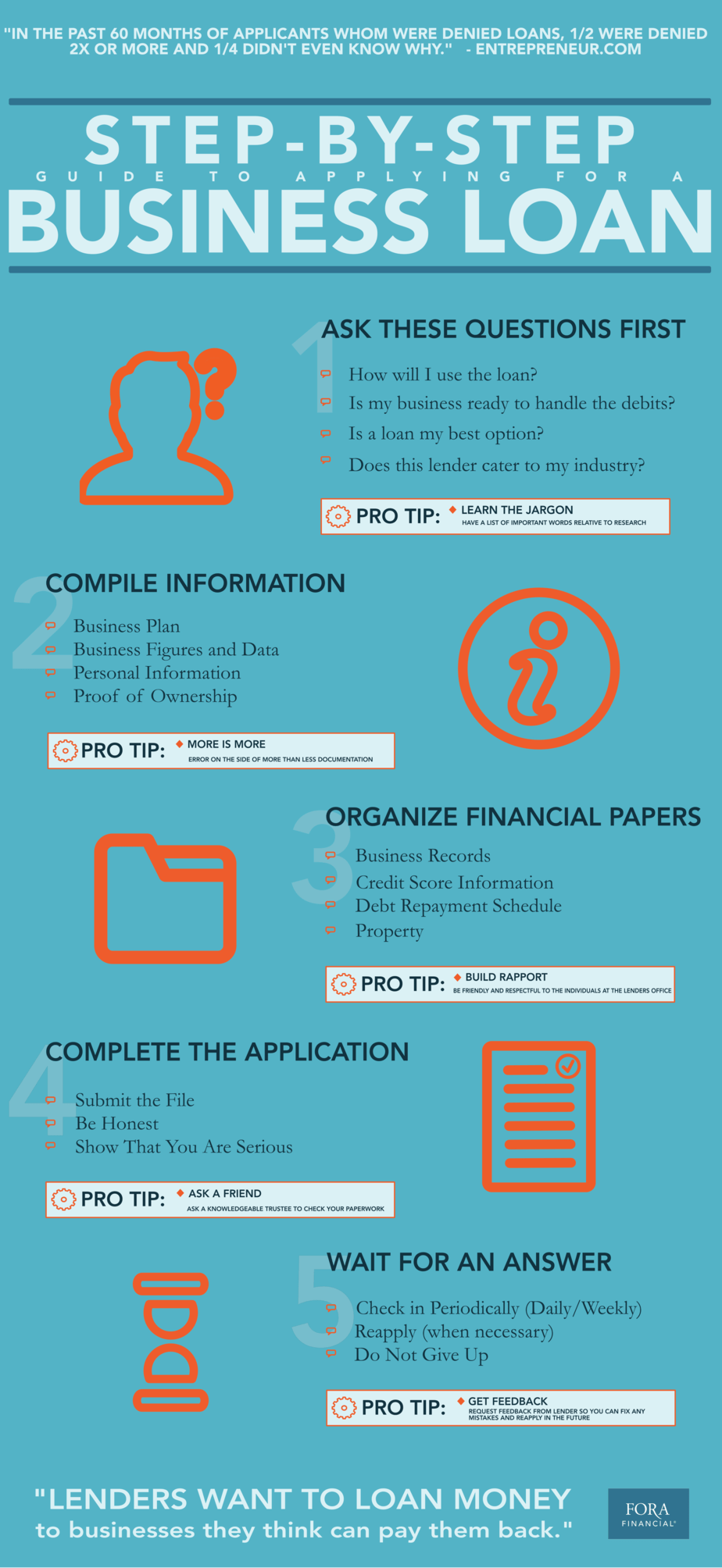

Preparing for Your Loan Application: Key Steps and Requirements

Successfully securing a business loan hinges significantly on thorough preparation. Lenders scrutinize various aspects of your business to assess risk and repayment capacity. Proactive organization and a clear understanding of what’s expected can streamline the process.

Assessing Your Business’s Financial Health

Before approaching any lender, objectively evaluate your business’s financial standing and creditworthiness.

- Personal and Business Credit Scores: Lenders will almost always check both your personal credit score (FICO) and your business credit score (e.g., from Dun & Bradstreet, Experian Business, Equifax Business). A strong credit history demonstrates responsible financial management. Aim for scores of 680+ for personal credit and establish a separate business credit profile as early as possible.

- Financial Statements: Prepare up-to-date and accurate financial documents, typically covering the last 2-3 years. This includes:

- Profit & Loss (P&L) Statements: Show your revenue, costs, and profit over a period.

- Balance Sheets: Snapshot of your assets, liabilities, and owner’s equity at a specific point in time.

- Cash Flow Statements: Detail the cash inflows and outflows, indicating your liquidity.

- Business Plan: A well-articulated business plan is critical, especially for startups or businesses seeking substantial growth funding. It should outline your business model, market analysis, management team, marketing strategy, and detailed financial projections (revenue, expenses, and cash flow for the next 3-5 years). This demonstrates foresight and a clear path to profitability.

Identifying the Right Lender

Choosing the correct lender is as important as choosing the right loan type. Different lenders specialize in different types of businesses and loan products.

- Traditional Banks: Often offer the lowest interest rates and most favorable terms for established businesses with strong credit and collateral. However, they typically have stricter eligibility requirements and longer application processes.

- Online Lenders: Known for their speed and convenience, online lenders often have more flexible eligibility criteria, making them a good option for businesses that don’t qualify for traditional bank loans or need funds quickly. Interest rates can be higher, though.

- Credit Unions: Member-owned financial institutions that may offer more personalized service and potentially lower rates than large banks, especially for their members.

- Alternative Lenders: This broad category includes invoice financiers, merchant cash advance providers, and peer-to-peer lending platforms. They cater to specific niches or businesses with unconventional needs but might come with higher costs.

Gathering Essential Documentation

Once you’ve assessed your financial health and identified potential lenders, start compiling the necessary paperwork. While requirements vary, common documents include:

- Business Legal Documents: Business registration, articles of incorporation, business licenses, and any permits.

- Tax Returns: Personal and business tax returns for the past 2-3 years.

- Bank Statements: Business bank statements for the past 6-12 months.

- Loan Application Form: The lender’s specific application.

- Collateral Information: Details of any assets you’re offering as security (e.g., property deeds, equipment lists).

- Personal Guarantees: Many small business loans require a personal guarantee from the owner, making them personally liable if the business defaults.

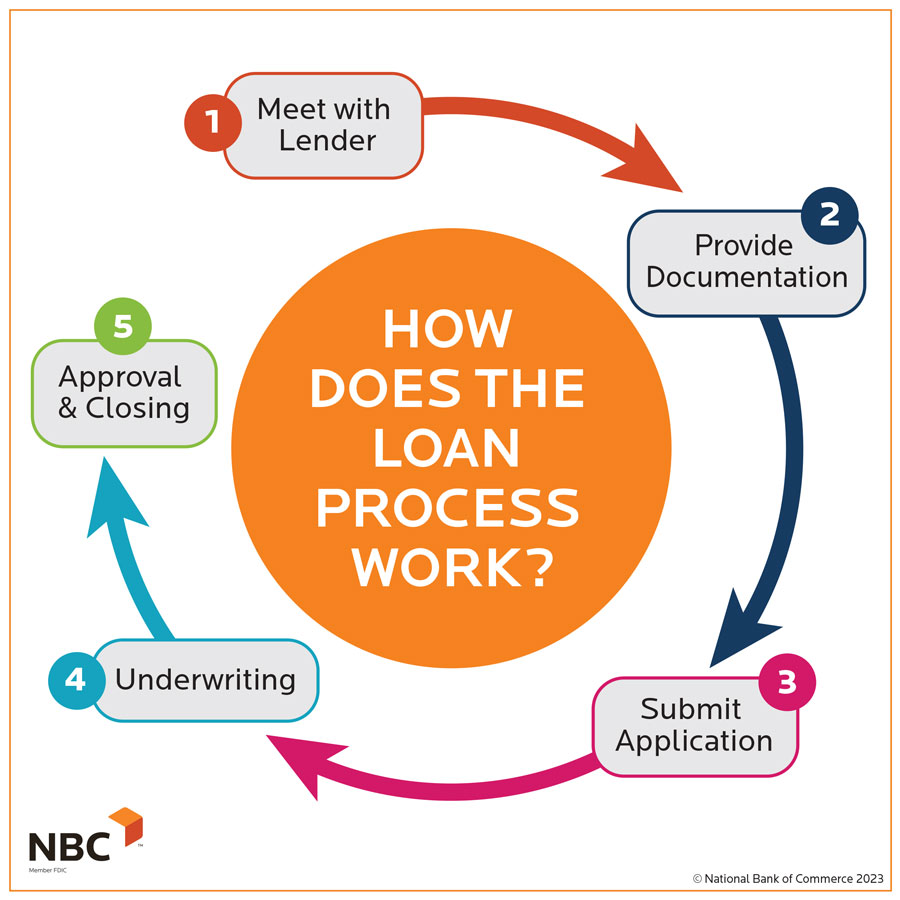

Navigating the Application and Approval Process

With your preparations complete, the next phase involves submitting your application and working with the lender through their evaluation process.

Submitting Your Application

Carefully complete the loan application, ensuring all information is accurate and consistent with your supporting documents. Any discrepancies can raise red flags and delay approval. Be prepared to provide additional information or clarification if requested.

Underwriting and Due Diligence

After submission, the lender’s underwriting team will conduct a thorough review. They will verify your financial information, assess your creditworthiness, analyze your business plan, and evaluate the risk associated with lending to your business. This phase can involve interviews, site visits, and further requests for documentation. Transparency and responsiveness during this stage are crucial.

Understanding Loan Offers and Terms

If your application is successful, you will receive a loan offer detailing the terms and conditions. It is imperative to review this document meticulously before signing. Key elements to scrutinize include:

- Interest Rates: Whether fixed or variable, and the Annual Percentage Rate (APR), which includes all associated fees.

- Repayment Schedule: The frequency (monthly, weekly) and amount of payments, including the loan term.

- Fees: Origination fees, closing costs, administrative fees, and prepayment penalties.

- Collateral Requirements: What assets, if any, are pledged as security for the loan.

- Covenants: Specific conditions or restrictions placed on your business by the lender, such as maintaining certain financial ratios or not incurring additional debt without approval.

- Personal Guarantee: Understand the full implications if you are personally guaranteeing the loan.

Don’t hesitate to ask questions or negotiate terms if you feel they are not suitable for your business.

Post-Approval: Managing Your Business Loan Wisely

Securing the loan is a significant achievement, but responsible management post-approval is equally critical to leverage the financing for sustained growth and maintain a strong financial reputation.

Strategic Use of Funds

Ensure the loan funds are used strictly for the purposes outlined in your business plan and agreed upon with the lender. Misusing funds can lead to financial strain and even breach of loan covenants. Create a detailed budget for how the funds will be allocated and track their usage diligently.

Adhering to Repayment Schedules

Timely loan repayments are paramount. Late payments can incur penalties, damage your credit score, and strain your relationship with the lender. Set up automated payments or establish a clear system to ensure payments are never missed. Proactive communication with your lender is advisable if you anticipate any difficulties in meeting a payment.

Maintaining a Strong Financial Standing

Continuously monitor your business’s financial performance. Keep accurate records, update your financial statements regularly, and strive to improve your creditworthiness. A strong financial standing not only ensures compliance with existing loan terms but also positions your business favorably for future financing needs.

Maximizing Your Chances of Loan Approval

While the process can be involved, several strategies can significantly bolster your chances of securing a business loan.

Building Strong Business Credit

Start building a separate business credit profile early by registering your business, obtaining an EIN, opening a dedicated business bank account, and applying for business credit cards. Ensure timely payments on all business obligations, including vendor invoices.

Crafting a Compelling Business Plan

Beyond mere compliance, view your business plan as a persuasive argument for your business’s viability and potential. Highlight your unique selling propositions, demonstrate a clear understanding of your market, and present realistic yet ambitious financial projections supported by sound assumptions.

Seeking Professional Guidance

Consider consulting with a financial advisor, small business consultant, or accountant. These professionals can help you prepare your financial documents, refine your business plan, identify suitable lenders, and navigate the complexities of loan applications. Their expertise can be invaluable in presenting your business in the best possible light.

Taking out a business loan is a strategic decision that can fuel significant growth and stability for your enterprise. By thoroughly understanding the types of loans available, meticulously preparing your application, diligently reviewing the terms, and responsibly managing the funds, you can successfully navigate the process and secure the financial resources needed to achieve your business objectives. Remember, a well-managed loan is not just debt; it’s an investment in your business’s future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.