Auto insurance is often viewed as a static monthly bill—a necessary evil that keeps a driver legal on the road. However, from a personal finance perspective, an auto insurance policy is a dynamic financial instrument designed to protect your net worth. For the savvy individual, knowing how and when to switch auto insurance is not just about administrative maintenance; it is a tactical move to reduce fixed expenses and enhance risk management.

In an era of fluctuating inflation and evolving actuarial models, staying loyal to a single insurance provider for decades can often lead to a “loyalty tax,” where long-term customers pay more than new acquisitions. By mastering the process of switching providers, you can reclaim hundreds, if not thousands, of dollars annually, which can then be redirected toward investments or high-yield savings.

1. Evaluating Your Current Financial Exposure and Coverage Needs

Before looking at the marketplace, you must conduct a thorough audit of your current policy. This isn’t merely about looking at the premium; it’s about understanding the underlying value of the protection you are purchasing.

Analyzing Your Existing Policy Limits

The first step is to pull your “Declarations Page.” This document summarizes your current coverage limits, deductibles, and premiums. From a wealth management standpoint, you need to ensure your liability limits are high enough to protect your total assets. If your net worth has increased since you first signed your policy, your current coverage might be dangerously low. Conversely, if you are driving an older vehicle with a market value lower than your annual premium plus deductible, you might be over-insuring the car by maintaining comprehensive and collision coverage.

Identifying Potential Savings Windows

Timing is a critical element of financial planning. While you can switch auto insurance at any time, certain milestones offer the best opportunities for lower rates. These include reaching the age of 25, improving your credit score, or passing the three-to-five-year mark after a minor traffic violation or accident. Additionally, if you have recently transitioned to a remote-work model, your annual mileage has likely decreased significantly. This shift in usage can drastically lower your risk profile and, consequently, your premium.

2. Navigating the Marketplace: Comparing Quotes and Risk Profiles

Once you have a baseline of your current coverage, the next phase is market research. In the world of personal finance, comparison shopping is the most effective way to ensure you are receiving the best price for the risk the insurer is assuming.

Understanding the Impact of Deductibles on Cash Flow

One of the most direct ways to manipulate your premium is through the adjustment of your deductible. A deductible is the amount you pay out-of-pocket before insurance kicks in. Increasing your deductible from $500 to $1,000 can result in a premium reduction of 15% to 30%. However, this must be a calculated decision. You should only opt for a higher deductible if your emergency fund is sufficiently liquid to cover that expense without causing financial strain.

The Role of Credit Scores in Insurance Pricing

In many jurisdictions, insurance companies use a “credit-based insurance score” to determine your premium. They have found a high correlation between credit responsibility and driving safety. If you have spent the last year improving your debt-to-income ratio or paying down credit cards, you likely qualify for a much lower rate than you did a year ago. When switching, ensure your credit report is accurate, as this financial metric can be just as influential as your driving record.

Comparing “Apple-to-Apples” Coverage

The biggest mistake people make when switching is comparing a high-quality policy from their current insurer with a “bare-bones” policy from a competitor. To make an informed financial decision, you must ensure that the limits for Bodily Injury Liability, Property Damage, and Uninsured Motorist coverage are identical across all quotes. Only then can you accurately assess which company offers the best return on investment.

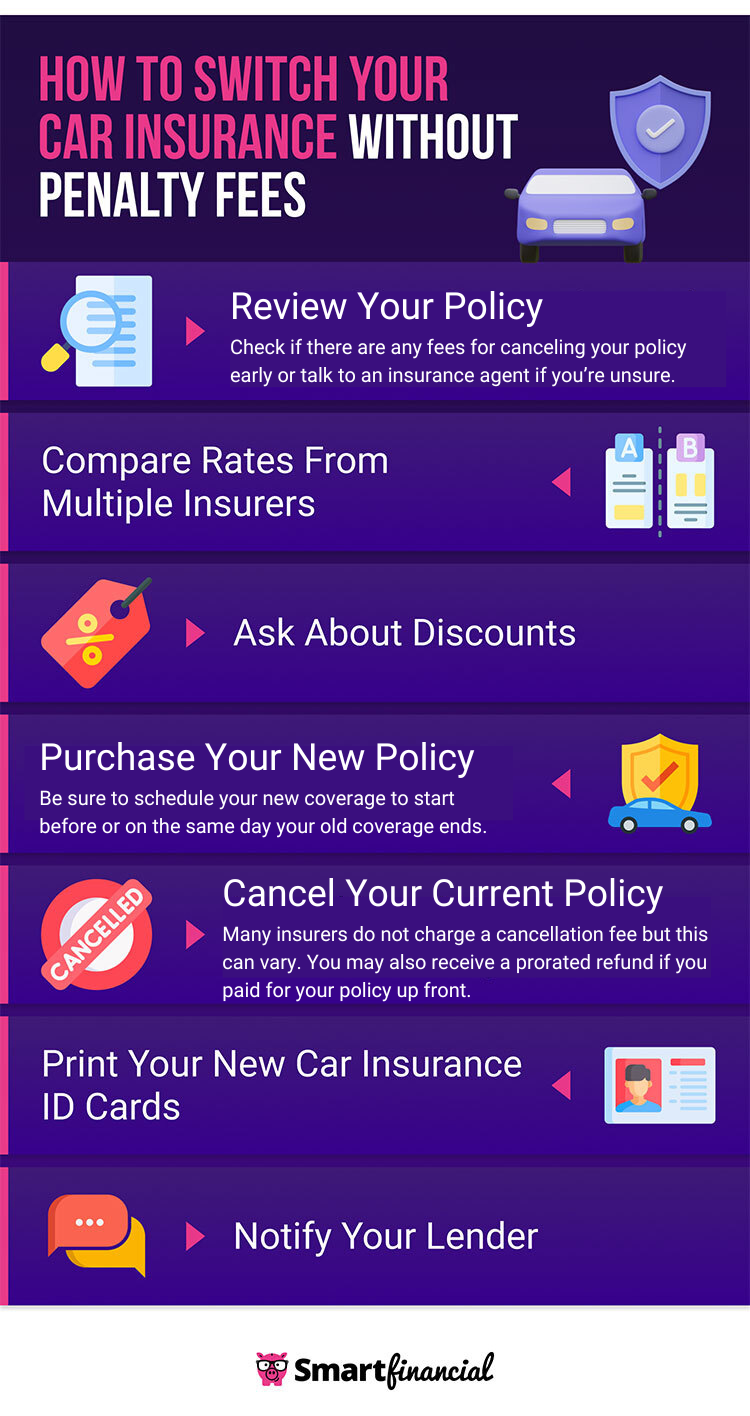

3. Executing the Transition Without Financial Gaps

Switching insurance is a binary process; you cannot afford a lapse in coverage. Even a one-day lapse can lead to a significant increase in future premiums, as insurers view uninsured drivers as high-risk. Furthermore, many states have electronic systems that notify the DMV immediately of a cancellation, which could lead to fines or registration suspension.

Coordinating the Effective Dates

The most efficient way to switch is to set the start date of your new policy to coincide exactly with the end date of your old one—or even overlap them by 24 hours. Once you have purchased the new policy and have the digital insurance cards in hand, you should contact your previous insurer to cancel. Do not simply stop paying the bill; a formal cancellation is required to ensure your account is closed in good standing and to prevent a negative report on your credit history.

Finalizing the Cancellation and Requesting Refunds

Because auto insurance premiums are often paid in advance (either monthly or every six months), you are likely entitled to a pro-rated refund of the “unused” portion of your premium. If you paid for six months and switch at the end of month two, the company is legally obligated to return the remaining four months of premium to you. Tracking this refund is a crucial part of the process, ensuring that no capital is left on the table during the transition.

4. Advanced Strategies for Maximizing Long-Term Savings

Switching once is good, but building a system for long-term premium management is better. Personal finance is about consistency and leveraging every available tool to reduce overhead.

Leveraging Multi-Policy and Bundling Discounts

One of the most effective brand-loyalty incentives used by insurance companies is the “bundling” discount. If you have a homeowner’s policy, a renter’s policy, or a life insurance policy, moving your auto insurance to the same provider can result in a 10% to 25% discount across all products. When shopping for a new auto policy, always ask for a “bundle quote” to see if the cumulative savings outweigh the benefits of keeping the policies separate.

Exploring Telematics and Usage-Based Insurance (UBI)

For those who are disciplined drivers, telematics—technology that monitors driving habits via a smartphone app or a plug-in device—represents a significant opportunity for savings. By sharing your data with the insurer (demonstrating safe braking, low speeds, and minimal nighttime driving), you can earn discounts that traditional actuarial models don’t offer. From a financial perspective, this is essentially trading data for a lower cost of living.

Conducting Annual Policy Audits

The financial landscape changes every year. Your car depreciates, your credit score fluctuates, and insurance companies update their pricing algorithms. To maintain an optimized personal budget, you should perform an insurance audit annually. This doesn’t mean you must switch every year, but you should at least verify that your current rate remains competitive. If your current insurer sees that you are aware of the market rates, they may even offer a “retention discount” to prevent you from leaving.

Conclusion: The Wealth-Building Power of the Switch

Switching auto insurance is far more than a simple administrative task; it is a fundamental exercise in financial stewardship. By systematically evaluating your coverage, shopping the marketplace with an eye on your credit health, and executing a seamless transition, you protect your assets while freeing up cash flow.

In the broader context of personal finance, saving $50 a month on auto insurance is equivalent to adding $600 a year to your retirement account. Over a decade, with compounding interest, that simple act of “switching” can translate into thousands of dollars of additional net worth. Treat your insurance as the financial asset it is, and never be afraid to move your business to where it is treated with the most financial respect.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.