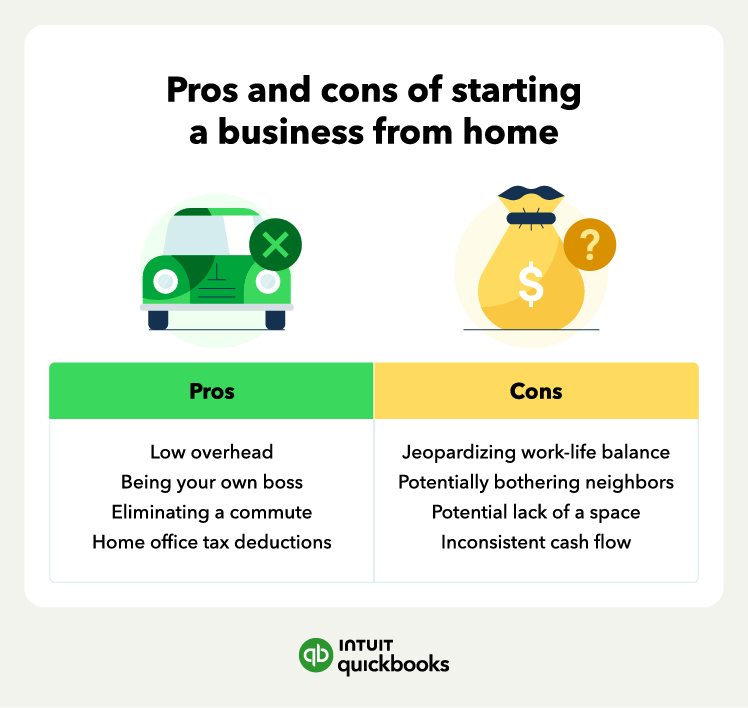

The allure of entrepreneurship, particularly from the comfort and flexibility of one’s own home, has never been stronger. In an era defined by digital connectivity and a growing demand for specialized skills and niche products, starting a home-based business offers a compelling path to financial independence and professional fulfillment. However, the dream of being your own boss and setting your own hours must be grounded in a robust understanding of financial realities. This isn’t merely about having a great idea; it’s about meticulously planning, funding, managing, and growing your venture with a keen eye on profitability and sustainability. To truly succeed, a holistic financial strategy forms the backbone of every thriving home-based enterprise. This guide will navigate you through the essential monetary considerations, from initial capitalisation to long-term financial growth, ensuring your home-based business isn’t just a passion project, but a financially sound and rewarding endeavor.

The Financial Blueprint: Pre-Launch Planning for Profitability

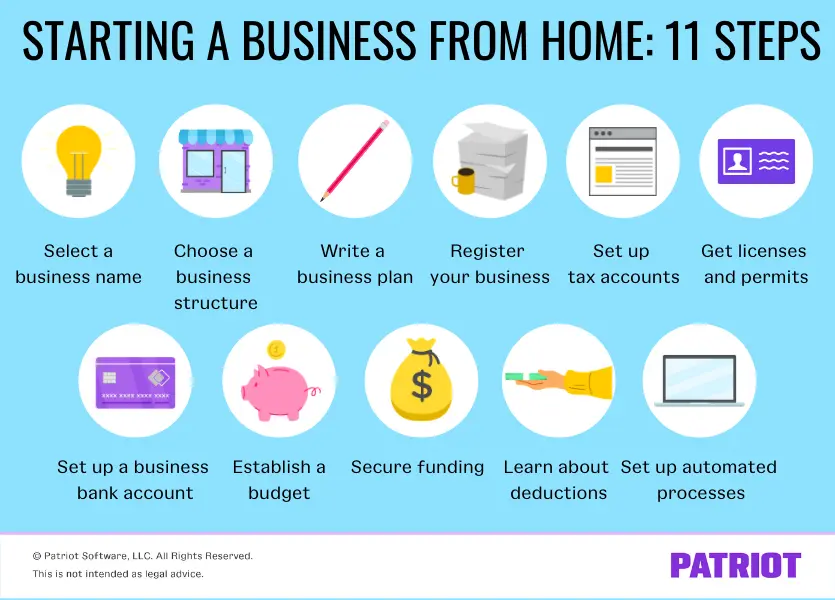

Embarking on any business venture without a clear financial roadmap is akin to sailing without a compass. For home-based businesses, this foundational planning is even more critical, as it often involves personal finances initially intertwined with nascent business operations. A meticulous pre-launch financial blueprint will not only clarify your path to profitability but also safeguard your personal financial stability.

Identifying a Profitable Niche and Validating Your Business Idea

The first financial imperative is to ensure your business idea holds genuine market potential and offers a clear path to revenue generation. It’s not enough to be passionate about an idea; it must solve a problem, fulfil a need, or provide value that customers are willing to pay for. Conduct thorough market research to identify demand for your proposed products or services. Investigate existing competitors to understand their pricing models, target demographics, and unique selling propositions. This financial reconnaissance helps you assess the potential for competitive pricing and sustainable profit margins.

Furthermore, validate your business idea through preliminary surveys, focus groups, or pilot programs. Can you secure initial commitments or pre-orders? What are customers truly willing to pay? Understanding these financial parameters upfront can save you significant time and money by pivoting early if the initial financial projections are weak. A profitable niche is one where demand is robust, competition is manageable, and you can command prices that cover costs and yield a healthy return.

Crafting Your Initial Business Budget and Financial Projections

Once a profitable niche is identified, the next step is to translate your business concept into concrete financial figures. This involves creating a detailed startup budget and comprehensive financial projections. Your startup budget should list all one-time and recurring costs you anticipate before generating significant revenue. For a home-based business, these might include:

- Setup Costs: Home office equipment (desk, chair, computer, printer), initial inventory, software licenses, website development, legal fees for business registration.

- Operating Expenses: Utilities (a portion often deductible), internet service, marketing expenses, professional development, insurance, payment processing fees, and raw materials if producing goods.

Beyond startup costs, develop financial projections for at least the first one to three years. This includes forecasting realistic sales volumes, revenue streams, cost of goods sold (if applicable), and ongoing operating expenses. A critical component here is the break-even analysis: determining the point at which your total revenues equal your total costs. Knowing this number gives you a tangible sales target and helps you understand the minimum performance required for your business to sustain itself without further investment. Realistic projections, backed by market data, are crucial for demonstrating financial viability to potential investors (including yourself) and for setting achievable operational goals.

Legal and Tax Considerations: Setting Up for Financial Compliance

Before launching, it’s vital to establish the correct legal and financial framework for your home-based business. The choice of business structure (e.g., Sole Proprietorship, LLC, S-Corp) has significant implications for personal liability and, more importantly, for how your business is taxed. Consult with a legal and tax professional to understand the best option for your specific situation, as it directly impacts your tax obligations and potential deductions.

Furthermore, investigate local permits, licenses, and zoning regulations that may apply to home-based businesses in your area. Failure to comply can result in hefty fines, directly impacting your financial health. Crucially, establish a clear separation between your personal and business finances from day one. Open a dedicated business bank account and consider a business credit card. This separation is paramount for accurate financial tracking, simplified tax preparation, and maintaining professional credibility. It also provides a vital protective barrier for your personal assets should the business face financial difficulties.

Smart Capitalization: Funding Your Home-Based Venture

Securing adequate capital is a universal challenge for new businesses, but for home-based entrepreneurs, the approaches can be unique. Often starting with limited external funding, home businesses rely heavily on strategic capitalization to ensure they have the runway to become profitable.

Bootstrapping and Self-Funding: Maximizing Your Personal Capital

For many home-based entrepreneurs, bootstrapping is the most common and often most effective funding strategy. Bootstrapping involves financing your business primarily through personal savings, credit, or the initial revenue generated by the business itself, minimizing reliance on external investors or loans. This approach fosters extreme financial discipline, encouraging you to keep overhead low, operate lean, and focus intensely on generating revenue from day one.

Strategies for successful bootstrapping include:

- Minimizing initial investment: Only purchase essential equipment or software. Leverage free trials and open-source alternatives wherever possible.

- Leveraging personal skills: Perform tasks yourself that you might otherwise outsource, such as website design, social media management, or content creation, to conserve cash.

- Starting small and scaling: Begin with a minimum viable product (MVP) or service offering, validating demand, and gradually expanding as revenue grows.

- Negotiating favorable terms: Seek payment plans with suppliers or try to get paid upfront from clients to improve cash flow.

While challenging, bootstrapping helps you retain full ownership and control of your business, preventing dilution of equity and reducing financial pressure from external stakeholders.

Exploring External Funding Options for Home Businesses

While bootstrapping is often the starting point, some home-based businesses may require additional capital to scale or to cover more significant initial investments. Several external funding options exist, though they may differ from those available to traditional brick-and-mortar businesses:

- Micro-loans: These small loans, often from non-profit organizations or government-backed programs, are designed to support small businesses and startups that might not qualify for traditional bank loans. They typically have lower interest rates and more flexible repayment terms.

- Small Business Grants: Various organizations, foundations, and government agencies offer grants specifically for small businesses, often targeting specific demographics (e.g., women-owned, veteran-owned) or industries. Grants do not need to be repaid, making them highly desirable, though competitive.

- Family and Friends: Approaching trusted individuals for investment or loans can be a viable option, but it’s crucial to formalize any agreements with clear terms, interest rates (if applicable), and repayment schedules to avoid personal misunderstandings.

- Crowdfunding: Platforms like Kickstarter or Indiegogo can be effective for product-based home businesses, allowing you to raise capital from a large number of individuals in exchange for early access to products, perks, or even equity. This also serves as a market validation tool.

When seeking external funding, understand the financial commitments involved. Evaluate interest rates, repayment schedules, and any equity dilution carefully to ensure the funding aligns with your long-term financial strategy and doesn’t place undue strain on your business.

Managing Startup Costs: Investing Wisely and Avoiding Overspending

The excitement of starting a new business can sometimes lead to impulsive spending. However, wise management of startup costs is paramount for a home-based business, where initial capital might be limited. Prioritize essential expenditures that directly contribute to generating revenue or meeting legal requirements. Differentiate between “needs” and “wants” in your budget. Do you truly need the premium subscription, or will the free tier suffice initially? Is a brand-new, top-of-the-line gadget essential, or can a refurbished model or a more basic option serve your needs for now?

Seek cost-effective solutions wherever possible. Leverage free or low-cost online tools for accounting, project management, and basic marketing. Invest in durable, multi-purpose equipment rather than specialized items with limited use. Remember, every dollar saved on unnecessary startup costs is a dollar that can be reinvested into growth, used for marketing, or kept as working capital to navigate early lean periods. A disciplined approach to initial spending lays a strong foundation for future financial stability.

Revenue Generation and Pricing Strategies for Home Entrepreneurs

Generating consistent and predictable revenue is the lifeblood of any business, and for home-based entrepreneurs, understanding diverse income streams and mastering pricing strategies are critical for financial success. Your ability to convert your efforts into measurable income will determine the longevity and profitability of your venture.

Diversifying Income Streams from Home

Relying on a single source of income can leave your home business vulnerable to market fluctuations or shifts in customer demand. Diversifying your income streams creates financial resilience and can accelerate growth. Consider the following common models for home-based businesses:

- Product-Based Businesses: Selling physical products through e-commerce platforms (Etsy, Shopify), direct-to-consumer sales, or local markets. This includes handmade goods, curated products, or dropshipped items.

- Service-Based Businesses: Offering professional services like consulting (marketing, business, financial), freelance writing, graphic design, virtual assistance, coaching, or technical support. Your expertise is the product.

- Digital Products: Creating and selling downloadable content such as e-books, online courses, templates, stock photos, or software. These often have high-profit margins once developed.

- Affiliate Marketing and Advertising: Earning commissions by promoting other companies’ products or services, or generating revenue through ads on a blog or YouTube channel. While not always the primary income, it can supplement other streams.

- Subscription Models: Offering recurring services (e.g., membership sites, software-as-a-service, curated product boxes) that provide predictable monthly or annual revenue.

Analyzing which combination of these streams aligns with your skills, niche, and target audience is vital for building a robust revenue model.

Strategic Pricing: Valuing Your Products and Services Appropriately

Pricing is not just about covering costs; it’s about communicating value, positioning your brand, and ultimately, maximizing profitability. Underpricing can undervalue your offerings and deplete your margins, while overpricing can deter potential customers. Several strategies can be employed:

- Cost-Plus Pricing: Calculating your total costs (materials, labor, overhead) and adding a desired profit margin. Simple, but may not reflect market value.

- Value-Based Pricing: Setting prices based on the perceived value your product or service delivers to the customer, rather than just your costs. This requires understanding your customer’s pain points and the tangible benefits you provide.

- Competitive Pricing: Researching what competitors charge for similar offerings and positioning your prices accordingly (e.g., slightly lower to attract, or higher to denote premium quality).

- Tiered Pricing/Package Deals: Offering different levels of service or product bundles at varying price points. This caters to different customer segments and can upsell clients to higher-value options.

Always consider your target market’s willingness to pay, your unique selling proposition, and your desired profit margins. Regularly review and adjust your pricing based on market feedback, cost changes, and perceived value. Transparent pricing and clear value propositions can build trust and attract the right customers.

Setting Up Payment Systems and Invoicing

Efficient payment processing is crucial for turning sales into actual cash flow. For a home-based business, setting up reliable and convenient payment systems is non-negotiable.

- Online Payment Processors: Platforms like Stripe, PayPal, Square, or others allow you to accept credit card payments, bank transfers, and digital wallets securely. Choose one that integrates well with your website or e-commerce platform and offers competitive transaction fees.

- Invoicing Software: Tools like FreshBooks, Wave, or QuickBooks Self-Employed simplify creating professional invoices, tracking payment statuses, and sending automated reminders. Prompt and clear invoicing prevents delays in payment.

- Payment Terms: Clearly state your payment terms (e.g., “Net 30,” “Due upon receipt”) on all invoices. Consider requesting partial upfront payments for larger projects or retainer fees for ongoing services to improve cash flow.

Proactive management of payments, including following up on overdue invoices, is essential for maintaining healthy cash flow and ensuring your hard work translates into financial reward.

Day-to-Day Financial Management from Your Home Office

Once your home business is operational, consistent and disciplined financial management becomes paramount. Without a dedicated finance department, the responsibility falls squarely on the entrepreneur to maintain accurate records, manage cash flow, and prepare for tax obligations.

Budgeting and Expense Tracking: Keeping a Tight Financial Ship

Effective budgeting and meticulous expense tracking are the cornerstones of sound financial management. Revisit your initial budget regularly, comparing actual income and expenses against your projections. This allows you to identify discrepancies, adjust spending, and make informed financial decisions.

Implement robust systems for tracking every business-related transaction. This can involve dedicated accounting software (like QuickBooks Self-Employed, FreshBooks, or Wave) which automates categorization, or even detailed spreadsheets initially. Categorize all expenses clearly (e.g., office supplies, marketing, utilities, software subscriptions, travel) as this is critical for tax purposes and understanding where your money is going. Regular review of your budget and expenditures helps you identify areas for cost-cutting, ensures you’re staying within your financial parameters, and provides a clear picture of your business’s financial health.

Cash Flow Management: Ensuring Liquidity and Financial Stability

Cash flow is the movement of money in and out of your business. Positive cash flow means you have more money coming in than going out, indicating liquidity. Negative cash flow, even in a profitable business, can lead to financial distress. For home-based businesses, managing cash flow effectively is vital to prevent running out of funds.

- Forecast short-term cash flows: Regularly project your expected cash inflows (from sales, payments received) and outflows (bills, payroll, operating expenses) over the next 30-90 days. This helps anticipate shortages or surpluses.

- Build a business emergency fund: Just like personal finance, having a reserve fund for unexpected expenses or lean periods provides a crucial safety net.

- Optimize working capital: Strategies include accelerating receivables (prompt invoicing, follow-ups), managing inventory efficiently to avoid tying up capital, and negotiating favorable payment terms with suppliers.

- Control variable costs: While fixed costs are steady, variable costs (tied to production or sales volume) can be managed to improve cash flow during slower periods.

Effective cash flow management ensures your business always has enough ready cash to meet its obligations, avoiding late fees, missed opportunities, or the need for emergency borrowing.

Preparing for Taxes: Annual Obligations and Deductions

Tax obligations can be complex for self-employed individuals and home-based businesses. Proactive tax planning is essential to avoid surprises and maximize legitimate deductions.

- Estimated Taxes: As a self-employed individual, you are generally required to pay estimated taxes quarterly rather than annually. Failing to do so can result in penalties. Budget for these payments throughout the year.

- Home Office Deduction: One of the significant advantages of a home-based business is the potential for a home office deduction. Understand the criteria (regular and exclusive use) and how to calculate it (simplified option or actual expenses).

- Other Business Deductions: Keep meticulous records of all eligible business expenses, including business-related travel, professional development, insurance premiums, software subscriptions, and a portion of utility costs. These deductions reduce your taxable income.

- Record-Keeping: Maintain an organized system for all financial records, including invoices, receipts, bank statements, and payroll records. This is crucial for accurate tax filing and essential if you are ever audited.

Consider consulting a tax professional who specializes in small businesses and self-employment. Their expertise can ensure compliance, identify all applicable deductions, and help you strategize for tax efficiency, allowing you to retain more of your hard-earned profits.

Scaling, Sustainability, and Long-Term Financial Growth

Building a financially sound home business extends beyond day-to-day operations; it involves strategic planning for growth, ensuring long-term sustainability, and continuously monitoring financial performance.

Reinvesting Profits Strategically for Expansion

Once your home business begins generating consistent profits, a critical financial decision arises: how to allocate those earnings. While it’s tempting to draw all profits for personal use, strategic reinvestment is key to scaling and achieving long-term growth.

Consider reinvesting profits into areas that will directly enhance future revenue or operational efficiency:

- Marketing and Advertising: Allocate funds to expand your reach, acquire new customers, or launch new product lines.

- Product Development/Service Enhancement: Invest in improving existing offerings or creating new ones to stay competitive and meet evolving customer needs.

- Technology and Tools: Upgrade essential software, hardware, or automation tools that can boost productivity and streamline operations.

- Skill Development: Invest in courses, workshops, or coaching for yourself or any hired help to improve expertise and service quality.

- Hiring Assistance: If overwhelmed, hiring virtual assistants, freelancers, or part-time staff can free up your time for higher-value tasks, directly contributing to scaling.

The goal is to strike a balance between taking a reasonable personal income and fueling your business’s expansion. A well-planned reinvestment strategy transforms current profits into future growth potential.

Financial Monitoring and Performance Analysis

Continuous financial monitoring and analysis are vital for understanding your business’s health and making data-driven decisions. Beyond basic bookkeeping, regular analysis of key performance indicators (KPIs) provides invaluable insights:

- Gross Margin: (Revenue – Cost of Goods Sold) / Revenue. Indicates the profitability of your core products/services.

- Net Profit Margin: Net Profit / Revenue. Shows the overall profitability after all expenses.

- Customer Acquisition Cost (CAC): Total Marketing & Sales Spend / Number of New Customers. How much it costs to acquire a new customer.

- Customer Lifetime Value (CLTV): The total revenue a customer is expected to generate over their relationship with your business. Comparing CLTV to CAC is crucial for sustainable growth.

- Cash Flow Cycle: How long it takes for your investments in inventory/services to convert into cash.

Regularly reviewing financial statements (income statements, balance sheets, cash flow statements) and these KPIs allows you to identify trends, spot potential problems early, and adjust your strategies proactively. Are marketing efforts yielding a good return on investment? Are costs creeping up? Is your pricing still appropriate? Performance analysis helps answer these questions and guides your strategic financial decisions.

Planning for the Future: Financial Forecasting and Exit Strategies

Looking beyond immediate operations, consider the long-term financial trajectory of your home business. Develop financial forecasts that extend several years into the future, incorporating potential growth scenarios, market changes, and major investments. This long-term view helps in setting ambitious yet realistic goals and planning for future capital needs.

Furthermore, even if it seems distant, contemplate potential exit strategies. Will you eventually sell the business? Pass it on to a family member? Gradually wind it down? Thinking about an exit strategy influences current decisions, particularly regarding building transferable assets, establishing strong financial records, and creating repeatable systems that add value to the business independently of your day-to-day involvement. Building a business that is financially valuable and attractive to potential buyers requires foresight and consistent financial discipline, ensuring your efforts culminate in a significant return on your entrepreneurial investment.

Starting a home-based business is an incredibly rewarding journey, offering unparalleled flexibility and the potential for substantial financial gain. However, its success is inextricably linked to a thorough, ongoing commitment to financial planning and management. By meticulously addressing capitalization, revenue generation, daily financial operations, and long-term growth strategies, you not only establish a stable foundation but also empower your home-based venture to thrive, adapt, and consistently deliver value, ensuring your entrepreneurial dream translates into tangible, lasting financial success.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.