In the contemporary financial landscape, the methodology of exchanging value has undergone a radical transformation. We have moved from the era of physical currency and handwritten checks to an age defined by instantaneous, digital peer-to-peer (P2P) transactions. At the forefront of this revolution is Venmo, a service that has transitioned from a simple utility to a cornerstone of modern personal finance. Understanding how to sign up for Venmo is no longer just a technical necessity; it is a fundamental step in managing one’s liquid assets and social expenditures efficiently. This guide explores the strategic setup of a Venmo account through the lens of financial optimization, security, and long-term fiscal management.

Understanding the Role of P2P Apps in Modern Financial Management

Before diving into the mechanics of account creation, it is essential to understand where Venmo sits within your broader financial ecosystem. Peer-to-peer payment platforms serve as the “connective tissue” between traditional banking institutions and the fast-paced world of social commerce.

The Shift from Cash to Digital Wallets

The traditional “cash-only” economy for small transactions—such as splitting a dinner bill or paying a roommate for utilities—is rapidly becoming obsolete. For the modern consumer, digital wallets provide a level of accounting transparency that cash cannot match. By routing these micro-transactions through a platform like Venmo, users create a digital paper trail, allowing for better budgeting and expense tracking. This shift represents a broader trend in personal finance where convenience meets data-driven money management.

Why Venmo Leads the Peer-to-Peer Payment Space

While competitors like Zelle and Cash App offer similar services, Venmo has carved out a unique niche by blending financial utility with a social interface. From a financial perspective, Venmo’s strength lies in its ubiquity. Because it is widely adopted, it reduces the “friction” of financial transfers. When everyone in a social or professional circle uses the same tool, the velocity of money increases, ensuring that debts are settled faster and personal cash flow remains steady.

The Step-by-Step Financial Onboarding Process

Setting up a Venmo account is a straightforward process, but doing so with an eye toward financial security and accuracy is paramount. Because Venmo handles sensitive banking data and real-world currency, the setup phase should be treated with the same diligence as opening a new bank account.

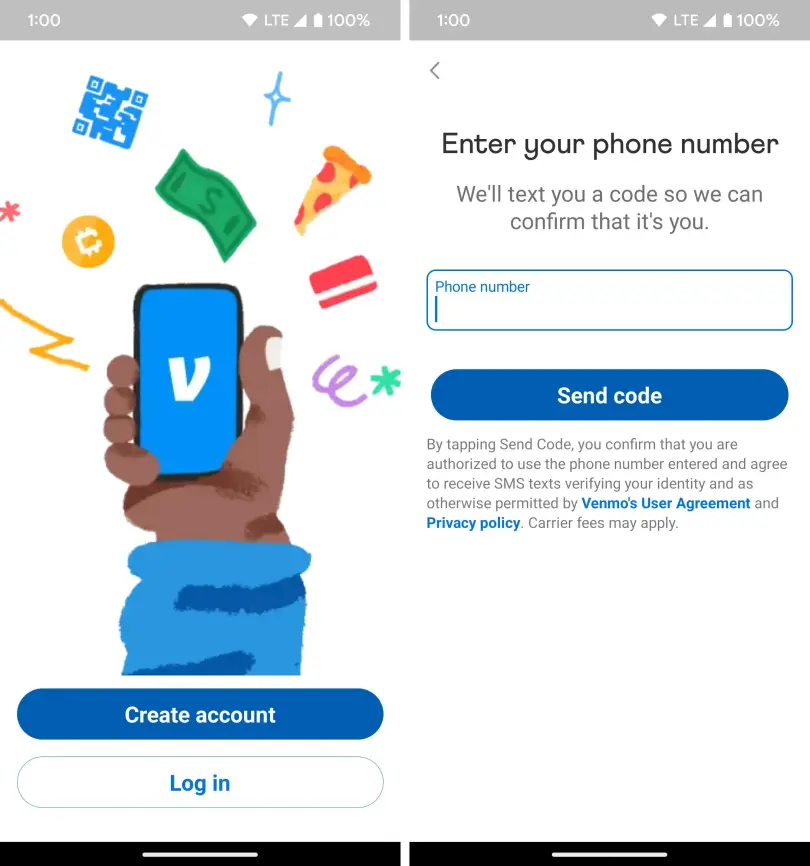

Account Creation and Identity Verification

To begin, download the app from your respective mobile store. Upon launching, you will be prompted to choose between a “Personal” or “Business” profile. From a money management standpoint, this choice is critical. Personal accounts are designed for splitting costs with friends, while Business profiles are structured to handle payments for goods and services, coming with different fee structures and tax implications.

After selecting your account type, you will provide your legal name, email address, and phone number. However, the most vital stage is identity verification. Under the USA PATRIOT Act, financial institutions are required to verify the identity of their users. Venmo will eventually ask for your Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN). Providing this information is not just a formality; it unlocks higher transaction limits and allows you to maintain a “Venmo Balance,” which acts as a secondary liquid account.

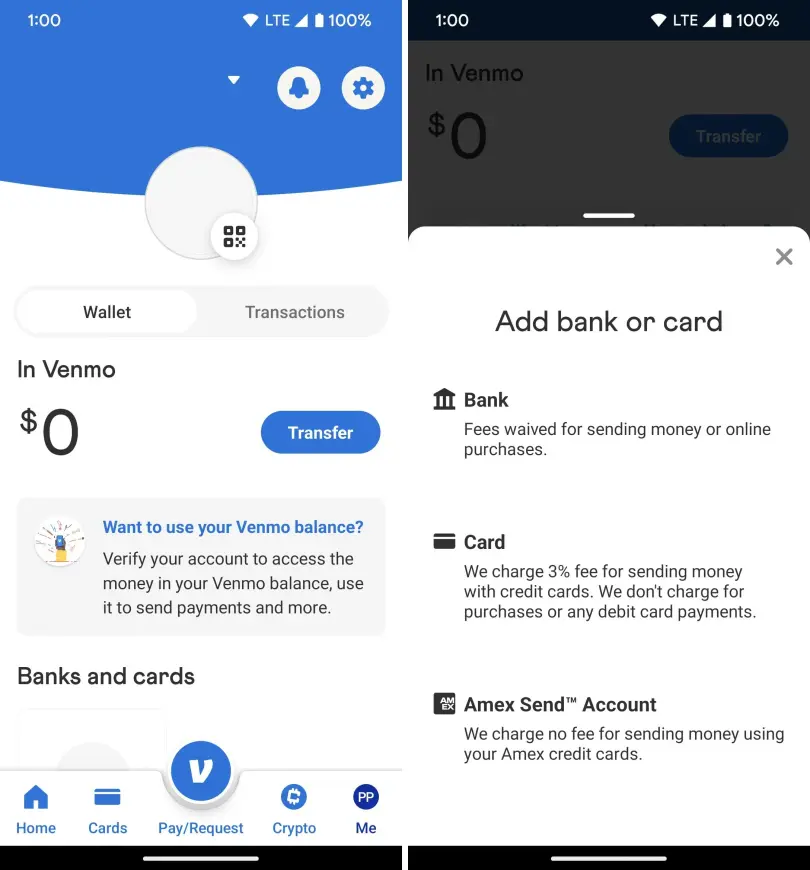

Linking Financial Institutions: Credit vs. Debit vs. Bank Accounts

Once your profile is established, you must link a funding source. This is where strategic financial decision-making comes into play. You generally have three options:

- Bank Accounts (ACH): This is the most cost-effective method for transferring large sums, as there are no fees for standard transfers.

- Debit Cards: Ideal for those who want the speed of a card transaction without the interest rates of a credit line.

- Credit Cards: While convenient, Venmo charges a 3% fee for transactions funded by a credit card. From a wealth-building perspective, using a credit card on Venmo is generally discouraged unless the user is leveraging a specific rewards program that offsets the 3% cost.

Navigating the Financial Security and Privacy Landscape

In the world of online income and digital banking, security is synonymous with solvency. A compromised Venmo account is not just a technical glitch; it is a direct threat to your personal capital.

Protecting Your Funds with Multi-Factor Authentication

The first line of defense in your digital financial life is Multi-Factor Authentication (MFA). During the sign-up process, Venmo will verify your phone number via SMS. However, for robust security, you should navigate to the “Security” settings immediately after setup to enable biometric locks (FaceID or Fingerprint) and explore third-party authentication apps if supported. Treating your Venmo app with the same security rigor as your primary checking account is the only way to ensure your side hustle income and personal savings remains protected.

Understanding Public vs. Private Transaction Histories

One of Venmo’s most controversial features is its social feed. By default, many transactions are visible to a user’s network. From a professional and financial privacy standpoint, it is often advisable to set your default privacy setting to “Private.” This ensures that your spending habits, the frequency of your transactions, and the identities of those you transact with are not visible to the public or your contacts. Maintaining financial privacy is a key component of sophisticated money management.

Strategic Financial Use Cases for the Savvy User

Once your account is active, the goal shifts from setup to optimization. Venmo is a versatile tool that can facilitate various aspects of your financial life beyond simple bill splitting.

Managing Shared Expenses and Side Hustle Income

For individuals engaged in the gig economy or those with multiple roommates, Venmo acts as an informal accounting ledger. The “Request” feature allows for proactive receivables management. Instead of waiting for a client or friend to remember a debt, a formal request creates a notification that serves as a professional reminder. For those managing “side hustle” income, keeping these payments separate in a Venmo Business profile can simplify your end-of-year accounting by segregating taxable income from personal gifts.

Navigating Fees and Transfer Speed Options

Understanding the “time value of money” is crucial when moving funds from Venmo to your external bank account. Venmo offers two primary withdrawal methods:

- Standard Transfer: This is free and typically takes 1–3 business days. For the disciplined budgeter, this is the preferred method.

- Instant Transfer: For a small percentage fee (currently 1.75% with a minimum and maximum cap), you can move funds to your bank account within minutes.

While the convenience of an Instant Transfer is tempting, a savvy financial manager recognizes that these fees compound over time. Planning your cash flow to allow for the 1–3 day standard transfer window is a simple way to preserve your capital.

Tax Implications and Regulatory Compliance in the Digital Economy

As your usage of Venmo grows, so does its impact on your tax profile. The Internal Revenue Service (IRS) has become increasingly focused on P2P platforms to ensure that taxable income is properly reported.

Understanding the 1099-K Threshold for Business Profiles

If you use Venmo for business purposes, it is vital to stay informed about the 1099-K reporting requirements. The threshold for receiving a 1099-K form has been subject to legislative changes, but generally, if you cross a certain dollar amount in “Goods and Services” payments, Venmo is required to report that income to the IRS. When signing up, ensure you are using the correct labels for your transactions. Labeling a business payment as “Friends and Family” to avoid fees or reporting is a violation of the terms of service and can lead to financial audits.

Best Practices for Financial Record Keeping

To maintain a high level of financial health, you should treat Venmo as a legitimate account in your bookkeeping software (like Quickbooks, Mint, or a manual spreadsheet). At the end of each month, download your transaction history. This habit ensures that you are aware of your “leakage”—small, unnoticed spends that can derail a budget—and provides a clear record of your financial activity should you ever need to dispute a charge or verify a payment for legal or tax reasons.

In conclusion, signing up for Venmo is the first step toward participating in a more fluid, digital-first economy. However, the truly successful user views the app not just as a convenience, but as a sophisticated financial tool. By prioritizing identity verification, choosing the right funding sources, securing the account, and understanding the tax implications of their transactions, users can leverage Venmo to enhance their overall financial well-being. In the modern age, your digital wallet is an extension of your financial identity; manage it with the care it deserves.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.