In the contemporary financial landscape, the act of “sending money” has evolved from a simple physical exchange of cash into a complex ecosystem of digital ledgers, cross-border protocols, and instantaneous peer-to-peer settlements. For the modern consumer or small business owner, understanding how to send money to someone is no longer just about convenience; it is a critical component of personal financial management. Choosing the wrong method can lead to unnecessary fees, unfavorable exchange rates, and potential security risks.

This guide explores the strategic nuances of transferring funds, ensuring that your capital moves efficiently, safely, and cost-effectively through the global financial network.

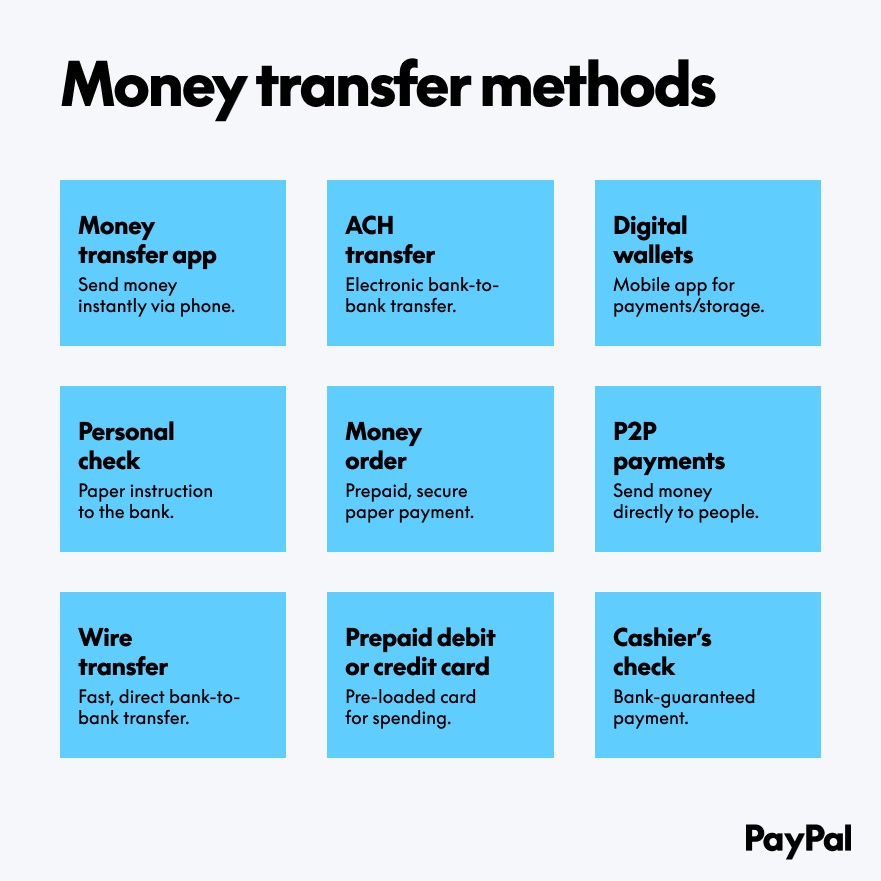

Understanding the Landscape of Personal Money Transfers

The first step in mastering financial transfers is identifying the specific category of the transaction. Not all transfers are created equal, and the financial tool you choose should align with the purpose of the payment.

Peer-to-Peer (P2P) Ecosystems

P2P platforms have revolutionized domestic personal finance. Services like Venmo, Zelle, and Cash App act as digital wallets that allow for near-instantaneous movement of funds between individuals. From a financial strategy perspective, these tools are best utilized for low-stakes, domestic transactions such as splitting a dinner bill or paying a roommate for utilities. The primary advantage here is liquidity; however, the trade-off is often a lack of robust consumer protection compared to traditional banking methods.

Traditional Banking and Wire Transfers

When dealing with large sums—such as a down payment on a home or a significant business investment—traditional bank-to-bank transfers remain the gold standard. Domestic ACH (Automated Clearing House) transfers are the backbone of the American banking system, offering a secure, though slower, way to move money. For urgent or international needs, Wire Transfers (often via the SWIFT network) provide a high-velocity solution. While these come with higher upfront fees, they offer a level of traceability and institutional oversight that P2P apps cannot match.

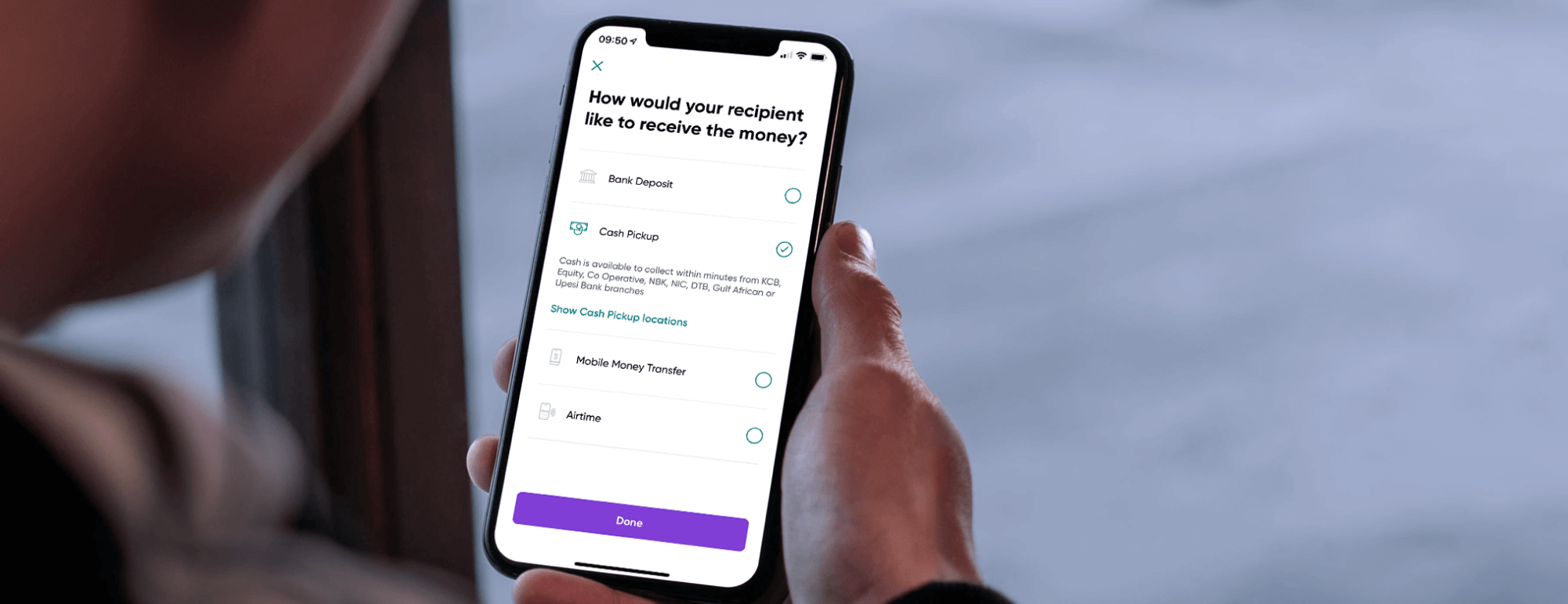

International Remittance Services

Sending money across borders introduces the complexity of currency conversion and international regulation. Specialist providers like Wise (formerly TransferWise), Revolut, and Remitly have disrupted the traditional banking monopoly on international transfers. These platforms focus on transparency, often offering the mid-market exchange rate while charging a clearly defined service fee. For the financially savvy, using these specialized tools instead of a traditional bank can save between 3% and 7% on the total transaction value.

Optimizing for Cost, Speed, and Efficiency

In personal finance, every dollar lost to a fee is a dollar that isn’t working for you in an investment or savings account. To send money effectively, one must balance the “Iron Triangle” of transfers: Speed, Cost, and Convenience.

Deciphering Fee Structures and “Hidden” Costs

Many financial institutions advertise “zero-fee” transfers, but it is essential to look closer at the exchange rate. This is where many banks and older transfer services generate profit—by padding the exchange rate. If the mid-market rate for USD to EUR is 0.92, but your bank offers you 0.89, they are effectively charging a 3% hidden fee. Always compare the offered rate against a neutral source like Reuters or Google Finance to calculate the true cost of your transfer.

Settlement Times and Liquidity Management

Speed is a luxury that often carries a premium. A standard ACH transfer might take 3-5 business days but is usually free. An Instant Transfer on a P2P app might cost 1.75% of the total. When managing your personal cash flow, it is vital to plan ahead. By initiating transfers several days before they are needed, you can avoid “convenience fees” and keep that capital within your own interest-bearing accounts for as long as possible.

The Role of Transfer Limits

Different financial tools have varying “velocity limits”—the amount of money you can move in a day, week, or month. High-net-worth individuals or those making significant purchases must be aware of these caps. For instance, Zelle often limits daily transfers to a few thousand dollars, whereas a bank wire has virtually no limit as long as the funds are verified. Understanding these limits prevents the financial “bottleneck” that occurs when you need to move a large sum urgently but are restricted by a platform’s policy.

Security and Risk Mitigation in Digital Transactions

The digital nature of modern money transfers makes them a primary target for financial fraud. Protecting your capital requires a multi-layered approach to security and a healthy dose of skepticism regarding “irreversible” transactions.

Avoiding the “Instant Transfer” Scam

The greatest risk in the P2P space is that many transactions are treated like cash; once the “Send” button is pressed, the money is gone. Fraudsters often use social engineering to trick individuals into sending money for products that don’t exist or to “verify” their bank accounts. From a financial safety standpoint, never send money via P2P apps to someone you do not know personally. For transactions with strangers, always use platforms that offer “Goods and Services” protections, such as PayPal, which allows for dispute resolution and clawbacks.

Implementing Multi-Factor Authentication (MFA)

Your financial tools are only as secure as the gatekeeper. Ensuring that every app and banking portal used for sending money is protected by hardware-based MFA (like a YubiKey) or at least an authenticator app is non-negotiable. SMS-based codes are increasingly vulnerable to “SIM swapping” attacks. In the realm of personal finance, securing the “pipes” through which your money flows is just as important as the money itself.

Verification of Recipient Identity

One of the most common errors in sending money is the “fat-finger” mistake—inputting the wrong phone number, email, or account digit. Unlike a credit card charge, which can be easily contested, a mistaken transfer to a stranger can be nearly impossible to recover. Always perform a “micro-transfer” (sending $1 first) to verify the recipient’s identity before sending a significant sum. This is a standard practice in corporate finance that every individual should adopt for their personal finances.

Choosing the Right Tool for Your Financial Goals

The final step in understanding how to send money is matching the tool to the objective. Every financial decision should be viewed through the lens of your overall wealth strategy.

Small-Scale Personal Payments

For the “coffee and dinner” category of transfers, focus on ubiquity and ease of use. If your social circle uses Venmo, use Venmo. The financial impact of fees here is negligible, but the “social friction” of using an obscure app is high. Just ensure you don’t keep a high balance in these apps; they are not banks, and your money there typically does not earn interest and may not be FDIC-insured.

Large-Scale Asset Acquisitions

If you are sending money to buy a vehicle, a boat, or real estate, prioritize security and the paper trail. A cashier’s check or a bank wire provides a legal record of payment that is essential for tax purposes and ownership disputes. Furthermore, these methods often trigger the necessary anti-money laundering (AML) checks that protect the integrity of the financial system, ensuring that your large-scale movements of capital are fully compliant with federal regulations.

Business-Related and Professional Fees

When sending money for professional services—such as to a contractor, an accountant, or a freelancer—it is wise to use systems that integrate with accounting software like QuickBooks or Xero. Sending money through a business bank account via ACH or a business credit card allows for easier expense tracking and tax deductions. Mixing personal and business transfers (often called “commingling”) is a significant financial mistake that can complicate your tax filings and weaken legal protections like corporate veils.

The Future of Sending Money: From Central Banks to Decentralized Finance

The landscape of money transfers is currently undergoing its most significant shift since the introduction of the credit card. Understanding these trends is vital for staying ahead of the curve in personal finance.

Real-Time Payment (RTP) Systems

The Federal Reserve’s “FedNow” service and the private sector’s “RTP Network” are moving the United States toward a 24/7/365 instant payment system. This will eventually make the concept of “waiting for a check to clear” obsolete. For the consumer, this means better cash flow management and the ability to pay bills at the very last second without penalty, keeping money in interest-bearing accounts for the maximum duration.

The Role of Stablecoins and Blockchain

While volatile cryptocurrencies like Bitcoin are often viewed as investments, “Stablecoins” (digital assets pegged to the US Dollar) are becoming a legitimate tool for international transfers. By using a blockchain to send a stablecoin, an individual can bypass the SWIFT network entirely, sending funds across the globe in seconds for a fraction of the cost of a traditional wire. However, this requires a high degree of technical literacy and an understanding of the regulatory environment, which is still evolving.

Central Bank Digital Currencies (CBDCs)

Governments worldwide are exploring CBDCs, which would essentially be a digital version of a country’s fiat currency. If implemented, sending money could become as simple as a direct transfer on a government-verified ledger, potentially eliminating the need for private intermediaries like banks for simple transfers. While this remains a prospective trend, it represents the logical conclusion of the “digitization of cash.”

In conclusion, knowing how to send money to someone is a multifaceted discipline that sits at the intersection of technology and personal finance. By prioritizing security, optimizing for fees, and selecting the appropriate vehicle for each transaction, you can ensure that your capital moves with precision. In an era where “money” is increasingly just data on a screen, the ability to manage that data effectively is one of the most important financial skills an individual can possess.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.