In an increasingly complex financial world, where economic shifts are frequent and consumer choices abound, the ability to manage personal or business finances effectively has never been more critical. At the heart of sound financial management lies a fundamental yet incredibly powerful tool: the budget sheet. Far from being a restrictive exercise, a well-prepared budget sheet serves as your financial blueprint, offering clarity, fostering control, and paving the way for achieving aspirations, whether it’s saving for a down payment, funding a retirement, or steering a business towards profitability.

Many shy away from budgeting, perceiving it as a tedious chore involving complex calculations and endless restrictions. However, this perspective fundamentally misunderstands its purpose. A budget sheet is not merely a record of past transactions; it’s a proactive strategy that empowers you to make informed decisions about your money today, shaping a more secure and prosperous tomorrow. It transforms abstract financial concepts into tangible data, allowing you to see exactly where your money comes from, where it goes, and, most importantly, where it could go to better serve your goals. This comprehensive guide will demystify the process of preparing a budget sheet, providing actionable steps to build a robust financial framework tailored to your unique circumstances. We’ll delve into the essential components, explore effective methodologies, and offer insights to ensure your budget sheet becomes an invaluable asset in your financial journey.

The Imperative of Budgeting: Why a Budget Sheet is Your Financial Compass

A budget sheet is more than just a ledger; it’s a strategic instrument that provides unparalleled insight into your financial ecosystem. Without one, individuals and businesses often navigate their finances blindly, reacting to circumstances rather than proactively shaping them. Understanding its core benefits is the first step toward embracing its power.

Gaining Clarity on Your Financial Landscape

The most immediate benefit of preparing a budget sheet is the profound clarity it provides. Many people have a vague idea of their income and expenses, but a budget sheet forces a granular examination. It illuminates hidden spending patterns, reveals forgotten subscriptions, and quantifies the cumulative impact of small, seemingly insignificant expenditures. This process often uncovers surprising truths about where money is actually going, which can be a wake-up call and a powerful motivator for change. For businesses, this clarity extends to understanding operational costs, profit margins, and the efficiency of various departments, leading to more strategic resource allocation.

Empowering Financial Decision-Making

Equipped with a clear understanding of your financial inflows and outflows, you transition from reactive to proactive financial management. A budget sheet empowers you to make conscious, informed decisions rather than impulsive ones. Should you take on that new subscription? Can you afford to upgrade your equipment? Is now the right time to invest? By knowing your exact financial position, you can weigh the pros and cons of each decision against your established financial goals and current capacity. This level of control significantly reduces financial stress and replaces uncertainty with confidence.

Paving the Way for Financial Goals

Every significant financial goal—be it saving for a down payment, eliminating debt, building an emergency fund, or expanding a business—requires a roadmap. A budget sheet is precisely that roadmap. By identifying surplus funds or areas for savings, it shows you how much you can realistically allocate towards your objectives. It transforms abstract dreams into achievable targets by breaking them down into manageable, budgeted contributions. Without a budget, these goals often remain distant aspirations; with one, they become concrete plans backed by a clear financial strategy.

Foundational Steps to Construct Your Budget Sheet

Building a budget sheet from scratch might seem daunting, but by following a structured approach, you can lay a solid foundation for your financial planning. The initial steps involve gathering crucial information and selecting the right tools.

Gathering Your Financial Data: Income and Expenses

The cornerstone of any accurate budget sheet is comprehensive data. Before you can plan, you must understand your current financial reality. This involves collecting all documents that detail your income and expenditures over a defined period, typically a month. For income, gather pay stubs, bank statements showing freelance payments, investment dividends, rental income, or any other source of funds. For expenses, compile bank statements, credit card statements, utility bills, loan statements, receipts, and any other records of money spent. The more thorough you are at this stage, the more accurate and useful your budget will be. Don’t overlook cash transactions; try to recall and estimate these as best as possible.

Choosing the Right Format: Digital vs. Manual

The method you choose to create your budget sheet can significantly impact its usability and your adherence to it.

Manual Budget Sheets: These involve pen and paper or printable templates. They offer a tactile experience and can be excellent for those who prefer to write things down, providing a direct connection to their numbers. They are simple to start with and don’t require any technical expertise.

Digital Budget Sheets: These typically use spreadsheet software (like Microsoft Excel, Google Sheets, or Apple Numbers) or dedicated budgeting apps. Digital options offer greater flexibility for categorization, calculations, analysis, and often automation. Spreadsheets allow for custom formulas, charts, and graphs, while apps often link directly to bank accounts for automatic transaction tracking, simplifying data entry. The choice largely depends on your comfort level with technology and your preference for manual input versus automation. For most, a digital spreadsheet strikes a good balance between flexibility and control.

Defining Your Budgeting Period

A budget is a snapshot of your finances over a specific timeframe. The most common and practical budgeting period is monthly. This aligns with most income cycles (bi-weekly, semi-monthly, or monthly paychecks) and bill cycles (rent, mortgage, utilities). However, depending on your income variability or specific financial goals, you might also consider a bi-weekly budget, especially if your paychecks are consistent. The key is to choose a period that makes sense for your cash flow and allows for consistent tracking and review. Once chosen, stick to it for consistency in analysis.

Populating Your Budget Sheet: Income and Expense Categorization

With your data gathered and your format chosen, the next critical step is to accurately populate your budget sheet by systematically categorizing all your financial ins and outs. This is where the real insights begin to emerge.

Accurately Recording Income Sources

Start by listing all your sources of income for your chosen budgeting period. This includes your primary salary or wages, any freelance income, rental income, investment dividends, benefits, or any other money you receive. Be precise with the figures. If your income varies, aim for a conservative average or use the lowest income month as a baseline to avoid overestimating your available funds. Clearly labeling each income source provides a comprehensive overview of your financial inflow. For businesses, this would include sales revenue, service fees, interest income, and any other cash inflows.

Deconstructing Expenses: Fixed vs. Variable

Expenses are the outgoing funds, and categorizing them is crucial for understanding spending patterns. A fundamental distinction to make is between fixed and variable expenses:

- Fixed Expenses: These are costs that generally remain the same each month and are often contractual. Examples include rent/mortgage payments, loan repayments (car, student), insurance premiums, subscription services, and certain fixed utility bills. These are relatively easy to budget for because their amounts are predictable.

- Variable Expenses: These costs fluctuate from month to month and are often discretionary. Examples include groceries, dining out, entertainment, transportation (gas, public transport), clothing, and personal care items. These are the areas where you often have the most control and where significant savings can be found through mindful spending.

List every expense you can identify, no matter how small. Create logical categories for these expenses (e.g., Housing, Transportation, Food, Utilities, Debt Payments, Personal Care, Entertainment, Savings, etc.) to make the sheet organized and easy to analyze.

Identifying Discretionary Spending and Opportunities for Savings

Once all income and expenses are listed and categorized, pay special attention to discretionary spending within your variable expenses. These are the “wants” rather than the “needs” and represent the primary area where you can exercise control to free up funds for savings or debt repayment. This might include daily coffees, impulse purchases, excessive entertainment, or subscriptions you no longer use.

The act of itemizing expenses often highlights areas of “leakage” where money is spent without much thought. These insights present immediate opportunities for savings. For instance, realizing you spend a significant amount on eating out might prompt you to plan meals and cook at home more often. Identifying unused subscriptions could lead to immediate cancellations. This step transforms raw data into actionable insights for financial optimization.

Analyzing and Optimizing Your Budget Sheet for Financial Health

Once your budget sheet is populated, the real work of analysis and optimization begins. This is where you transform data into strategic action, pushing your finances towards your desired goals.

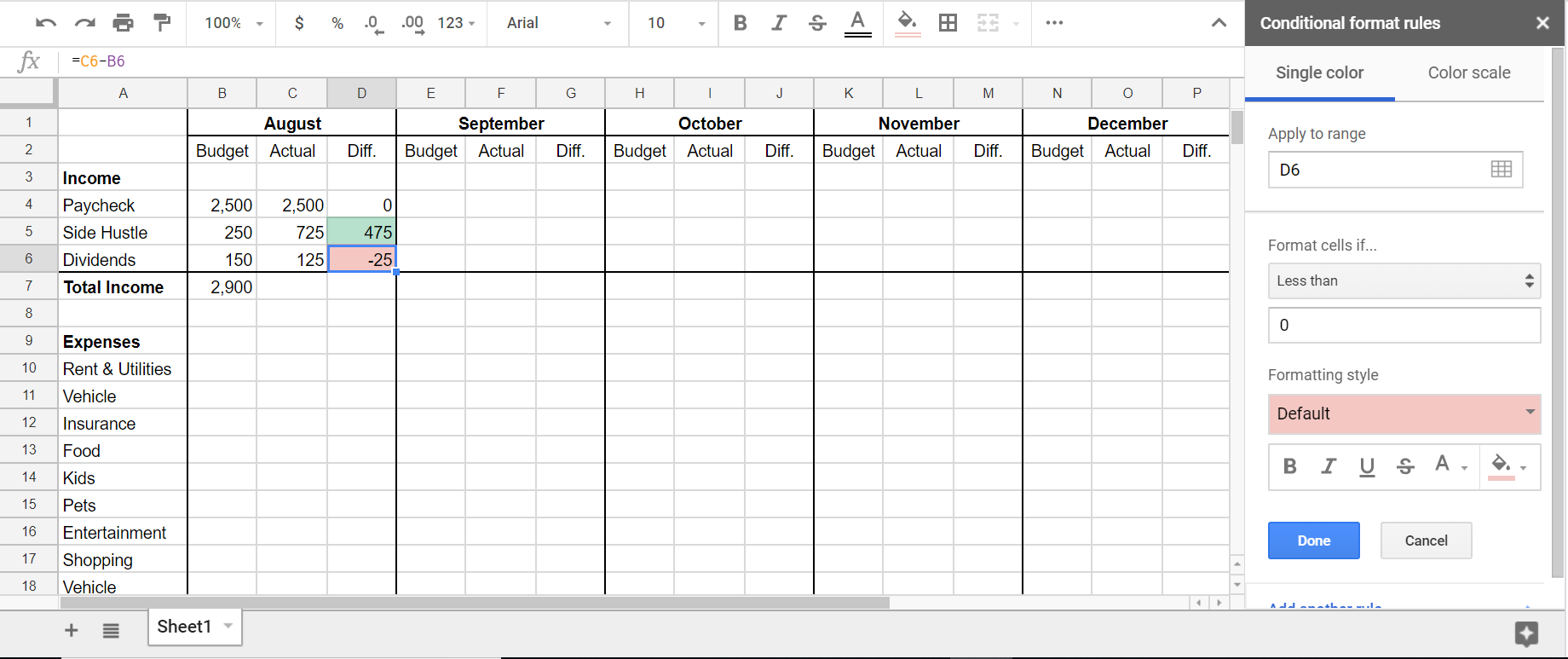

Calculating Net Income and Understanding Your Cash Flow

The most fundamental calculation on your budget sheet is determining your net income (or net cash flow). This is simply your total income minus your total expenses.

- Positive Net Income: If your income exceeds your expenses, you have a surplus. This surplus is where your financial freedom lies—it’s the money you can strategically allocate towards savings, investments, debt acceleration, or additional financial goals.

- Negative Net Income: If your expenses exceed your income, you have a deficit. This indicates overspending and is a critical red flag. It means you are likely accumulating debt or depleting savings, which is unsustainable in the long run. A negative net income demands immediate action to either increase income or, more commonly, reduce expenses.

Understanding this cash flow is paramount. It tells you whether you are living within your means and whether your current spending habits are sustainable.

Spotting Trends and Identifying Overspending

Beyond the simple surplus or deficit, a well-maintained budget sheet allows you to spot trends over time. Are certain categories consistently over budget? Does your spending spike at particular times of the month or year? For instance, you might notice that your grocery bill is consistently higher than anticipated, or that discretionary spending on entertainment consistently pushes you into a deficit.

Regular review (e.g., weekly or bi-weekly check-ins) helps identify these patterns early. Pinpointing areas of overspending is not about judgment, but about identifying opportunities for adjustment. It allows you to ask targeted questions: “Why is this category consistently high?” “Could I find a cheaper alternative here?” This analytical step transforms raw numbers into actionable intelligence for budget refinement.

Strategies for Budget Adjustment and Savings Maximization

Once overspending or opportunities are identified, it’s time to adjust your budget. This isn’t a one-time fix but an ongoing process.

- Expense Reduction: Focus on variable expenses first. Can you cut back on dining out, limit impulse purchases, or find cheaper alternatives for services? Even small reductions in multiple categories can add up significantly. Re-evaluate fixed expenses periodically too; could you refinance a loan, negotiate insurance rates, or cancel unused subscriptions?

- Income Enhancement: While not always immediately feasible, explore options to increase your income, such as taking on a side hustle, negotiating a raise, or selling unused items.

- “Pay Yourself First”: A highly effective strategy is to budget for savings as a fixed expense. Before you pay any bills or indulge in discretionary spending, automatically transfer a set amount to a savings or investment account. This ensures your financial goals are prioritized.

- The 50/30/20 Rule: A popular guideline suggests allocating 50% of your income to needs, 30% to wants, and 20% to savings and debt repayment. While not a strict rule, it provides a useful framework for balancing your budget.

The goal of optimization is to align your spending with your values and financial goals, ensuring that every dollar serves a purpose.

Maintaining and Evolving Your Budget: A Dynamic Financial Tool

A budget sheet is not a static document you create once and forget. It’s a living tool that requires ongoing attention and adaptation to remain effective. Its true power lies in its dynamic nature, evolving alongside your financial situation and life circumstances.

Regular Review and Reconciliation

The consistency of your budget sheet’s effectiveness hinges on regular review and reconciliation. At a minimum, reconcile your actual spending against your budgeted amounts weekly or bi-weekly. This involves comparing your bank and credit card statements with the entries on your budget sheet. This process helps:

- Catch errors: Ensure all transactions are correctly recorded.

- Identify discrepancies: See where your actual spending deviated from your plan.

- Stay informed: Keep a pulse on your financial health throughout the month, rather than waiting until the end.

Regular reconciliation ensures accuracy and keeps you engaged with your financial plan, preventing small overspends from snowballing into larger problems.

Adapting to Life Changes and Financial Goals

Life is unpredictable, and your financial situation will undoubtedly change over time. Job promotions, new dependents, unexpected expenses, shifts in income, or changes in major life goals (e.g., buying a home, starting a family, retiring) all necessitate adjustments to your budget.

- Proactive Adjustments: When a significant life event is on the horizon, anticipate its financial impact and proactively modify your budget.

- Reactive Adjustments: If an unexpected expense arises, evaluate how it affects your current budget and make temporary or permanent changes to other categories to accommodate it.

A flexible mindset is key. Your budget should serve you, not the other way around. Be prepared to revisit your categories, reallocate funds, and set new targets as your circumstances evolve.

Leveraging Technology for Ongoing Budget Management

While a manual spreadsheet provides a solid foundation, leveraging modern financial tools can significantly enhance your budget management efforts.

- Budgeting Apps: Many apps (e.g., YNAB, Mint, Personal Capital) offer automated transaction categorization, direct bank linking, goal tracking, and visual reports. These can save time on data entry and provide powerful insights.

- Spreadsheet Templates: Even if you prefer a more hands-on approach, advanced spreadsheet templates can automate calculations, generate charts, and integrate complex scenarios, making budget tracking more efficient.

- Financial Software: For businesses, comprehensive accounting software provides integrated budgeting features, allowing for detailed expense tracking, forecasting, and reporting.

By embracing technology, you can streamline the maintenance process, gain deeper analytical capabilities, and ensure your budget sheet remains an accurate and effective tool for sustained financial well-being.

In conclusion, preparing a budget sheet is a foundational step towards achieving financial mastery. It’s an empowering exercise that provides clarity, fosters control, and illuminates the path to your financial aspirations. By meticulously gathering data, systematically categorizing income and expenses, and consistently analyzing and adapting your plan, you transform a simple sheet into a dynamic financial compass. Embrace the process, commit to regular review, and allow your budget sheet to guide you confidently towards a future of financial stability and prosperity.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.