Transitioning from a traditional W-2 employee to a freelancer, independent contractor, or small business owner is an exciting milestone in any professional’s journey. However, with this newfound professional freedom comes a significant shift in fiscal responsibility. Unlike traditional employees who have taxes withheld from every paycheck by their employers, the self-employed are responsible for paying their own taxes directly to the government. Because the United States operates on a “pay-as-you-go” tax system, the IRS requires these individuals to make estimated tax payments four times a year.

Navigating quarterly taxes can feel daunting, but understanding the mechanics of the process is essential for maintaining healthy cash flow and avoiding costly IRS penalties. This guide provides a deep dive into who must pay, how to calculate your obligations, and the best practices for managing your business finance throughout the year.

1. Determining Your Obligations: Who Must Pay Quarterly Taxes?

The first step in mastering your quarterly taxes is determining whether the requirement applies to you. In the eyes of the IRS, if you are not having taxes withheld from your income—or if the withholding is insufficient—you are likely required to make estimated payments.

The $1,000 Threshold and the Self-Employed

Generally, individuals, including sole proprietors, partners, and S corporation shareholders, must make estimated tax payments if they expect to owe at least $1,000 in tax for the year after subtracting their withholding and refundable credits. This rule is particularly relevant for the “gig economy” participants, such as freelance writers, graphic designers, and consultants, who often receive gross payments without any tax deductions.

Identifying Diverse Income Sources

Quarterly taxes aren’t just for the self-employed. You may also need to pay estimated taxes if you receive significant income from sources that do not have withholding. This includes interest, dividends, alimony, capital gains from the sale of assets, prizes, and awards. If you have a high-yield investment portfolio or are flipping real estate for profit, you must account for the tax liability generated by these gains in real-time rather than waiting until April 15th of the following year.

Safe Harbor Rules: Avoiding Underpayment Penalties

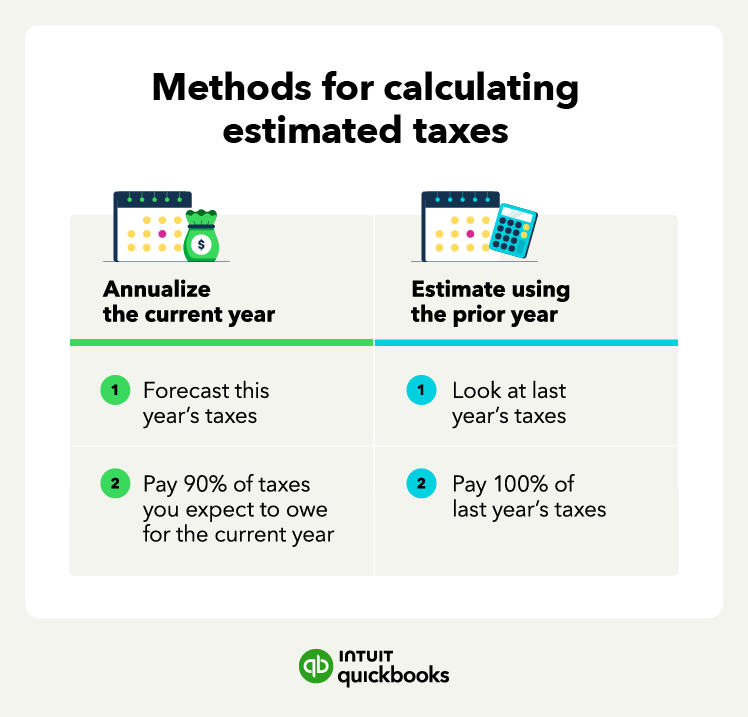

The IRS provides “Safe Harbor” provisions to protect taxpayers from penalties if their estimates aren’t perfectly accurate. Generally, you will not face a penalty if you pay at least 90% of the tax for the current year or 100% of the tax shown on your return for the prior year, whichever is smaller. For high-income earners (those with an adjusted gross income over $150,000), the safe harbor requirement increases to 110% of the prior year’s tax. Understanding these thresholds is vital for financial planning, as it provides a clear target for your quarterly outlays.

2. Calculating Your Estimated Payments: Accuracy and Strategy

Calculating exactly how much you owe can be the most complex part of the process. Because your income may fluctuate throughout the year, your quarterly payments might not always be identical.

Utilizing IRS Form 1040-ES

The primary tool for this calculation is Form 1040-ES, “Estimated Tax for Individuals.” This form includes a worksheet that helps you estimate your expected adjusted gross income, taxable income, taxes, deductions, and credits for the year. To complete this accurately, it is highly beneficial to have your prior year’s tax return on hand as a baseline. The form guides you through calculating both your income tax and your self-employment tax.

Understanding Self-Employment Tax

For many new entrepreneurs, self-employment tax comes as a surprise. When you work for an employer, you pay 7.65% for Social Security and Medicare, and your employer matches that 7.65%. When you are self-employed, you are both the employer and the employee, meaning you are responsible for the full 15.3%. While you can deduct the “employer” half of this tax on your return, you must account for the full amount when calculating your quarterly payments to ensure you aren’t underfunded.

Tracking Deductions and Business Expenses

Accuracy in your quarterly payments relies heavily on your record-keeping. The more business expenses you can legitimately deduct—such as home office costs, equipment, marketing, and professional services—the lower your taxable income will be. Using financial tools like specialized accounting software can help you track these expenses in real-time, allowing you to adjust your quarterly estimates downward based on your actual profitability rather than just your gross revenue.

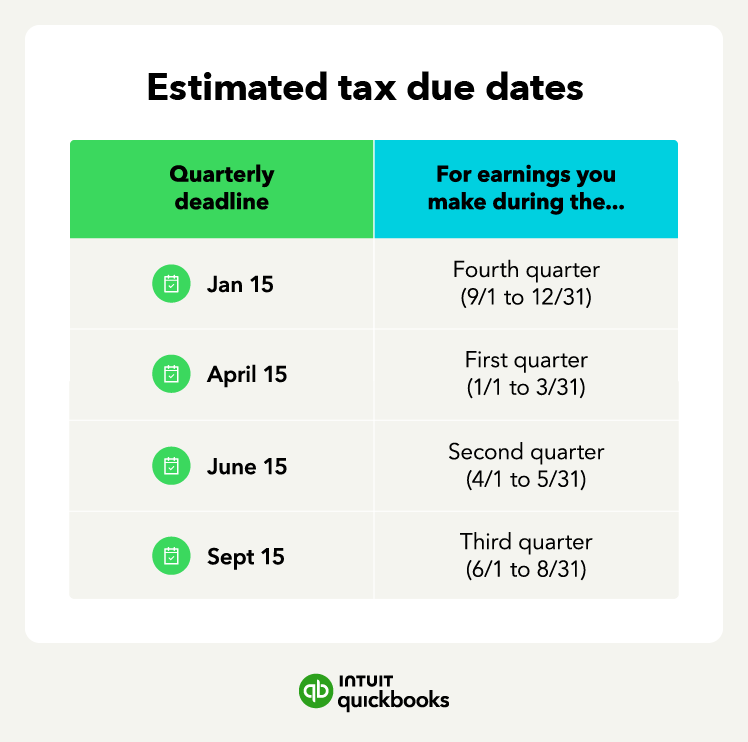

3. The Payment Calendar: Deadlines and Timing

The IRS does not follow a standard calendar quarter for estimated payments. Instead, the year is divided into four specific periods, each with its own due date. Missing these deadlines can result in interest charges and penalties, even if you are due a refund at the end of the year.

Marking the Four Critical Dates

The standard deadlines for quarterly estimated tax payments are:

- Period 1 (Jan 1 – March 31): Due April 15.

- Period 2 (April 1 – May 31): Due June 15.

- Period 3 (June 1 – August 31): Due September 15.

- Period 4 (Sept 1 – Dec 31): Due January 15 of the following year.

Note that if these dates fall on a Saturday, Sunday, or legal holiday, the payment is due on the next business day. It is a common mistake to assume the periods are all three months long; however, the second “quarter” is notably only two months, which requires careful cash flow management.

Managing Seasonal Income Fluctuations

If your business is seasonal—for example, a retail business that makes 60% of its revenue in the fourth quarter—you may not be required to pay equal amounts each period. You can use the “Annualized Income Installment Method.” This allows you to pay an amount based on what you actually earned during each specific period. While this requires more complex bookkeeping (and filing Form 2210 with your annual return), it can prevent you from overpaying early in the year when cash might be tight.

4. Payment Methods: How to Securely Send Your Money

The IRS has modernized its systems, making it easier than ever to submit payments. Choosing the right method depends on your preference for speed, record-keeping, and convenience.

IRS Direct Pay and EFTPS

The most straightforward method for individuals is IRS Direct Pay. This free service allows you to pay directly from your checking or savings account. You receive an immediate confirmation number, which is crucial for your financial records. For larger businesses or those who prefer to schedule all their payments for the year in advance, the Electronic Federal Tax Payment System (EFTPS) is a more robust option. It requires a separate enrollment process but offers comprehensive tracking and scheduling features that are ideal for serious financial management.

Mobile Apps and Digital Wallets

The IRS also offers the IRS2Go mobile app, providing a convenient way to make payments on the move. Additionally, you can pay via credit or debit card through authorized third-party processors. However, be cautious: while paying by credit card can help you earn reward points, these processors charge a convenience fee (usually between 1.8% and 2.5%), which can negate the value of any rewards and add unnecessary costs to your tax bill.

Traditional Paper Vouchers

If you prefer a paper trail and manual processing, you can mail a check or money order along with the payment vouchers found in Form 1040-ES. If you choose this route, ensure your payment is postmarked by the due date to avoid late penalties. However, in an era of digital security, electronic payments are generally recommended as they reduce the risk of mail loss and provide faster confirmation.

5. Strategic Financial Planning for Tax Success

Paying quarterly taxes shouldn’t be a source of stress. With a proactive approach to your personal and business finances, you can turn tax compliance into a seamless part of your workflow.

The 30% Rule and Dedicated Savings

A best practice for anyone in the Money niche is to “tax-proof” your income as it arrives. A common strategy is the 30% Rule: every time you receive a payment from a client, immediately transfer 30% of that gross amount into a dedicated “Tax Savings” account. This ensures that when the quarterly deadline arrives, the money is already set aside and you aren’t forced to scramble for funds or dip into your operating capital.

Leveraging High-Yield Accounts

Since you are essentially holding the government’s money for three months at a time, you should make that money work for you. By keeping your tax reserves in a High-Yield Savings Account (HYSA) or a short-term Money Market account, you can earn interest on those funds before you send them to the IRS. While the interest earned is taxable, it is a smart financial move that generates passive income from a liability.

When to Consult a Financial Professional

As your income grows and your financial situation becomes more complex—perhaps involving employees, multi-state nexus, or sophisticated investment vehicles—the DIY approach may no longer be efficient. Hiring a Certified Public Accountant (CPA) or a tax strategist can be a wise investment. These professionals can identify deductions you might have missed, help you navigate complex state-level quarterly requirements, and ensure that your overall financial strategy is optimized for both growth and compliance.

By mastering the rhythm of quarterly taxes, you gain more than just IRS compliance; you gain a clearer picture of your business’s profitability and a more disciplined approach to your overall financial health. Consistent tracking, disciplined saving, and timely payments are the hallmarks of a sophisticated professional in today’s economy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.