For many investors, the allure of the stock market lies not just in the potential for capital appreciation, but in the steady, reliable stream of passive income known as dividends. Whether you are a retiree looking to cover living expenses or a young investor seeking to harness the power of compounding, understanding the mechanics of dividend timing is essential.

The question of “how often dividends are paid” is not a one-size-fits-all answer. While the financial markets follow certain conventions, the frequency of payments is ultimately at the discretion of a company’s board of directors. To build a robust income portfolio, one must look beyond the yield and delve into the schedules, the critical dates, and the strategic implications of different distribution models.

Understanding the Dividend Lifecycle: Key Dates Every Investor Must Know

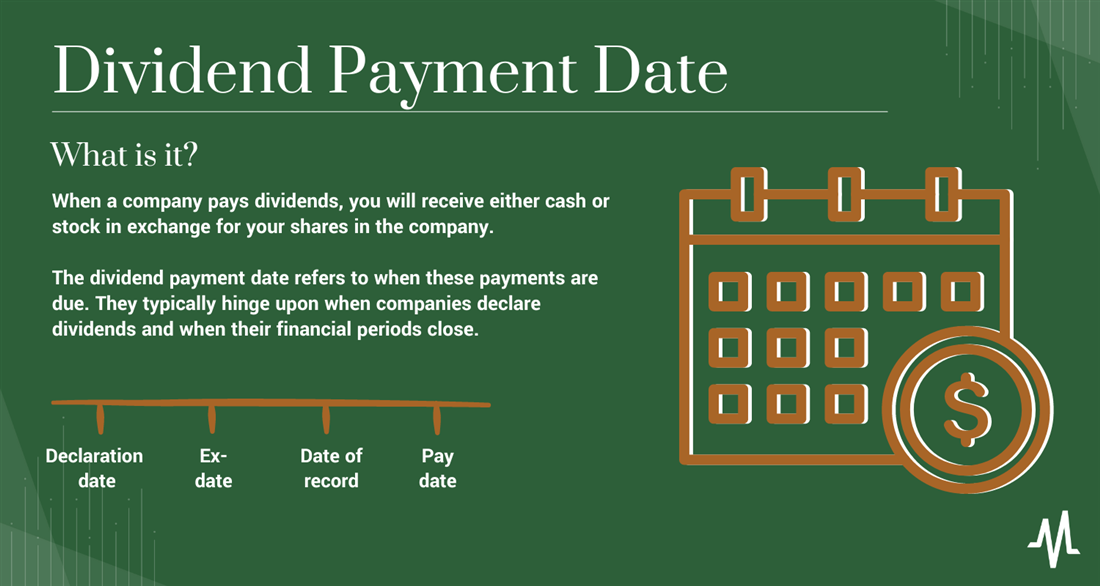

Before exploring the frequency of payments, it is vital to understand the “Dividend Lifecycle.” A dividend is not simply a transaction that happens instantaneously; it is a regulated process involving four specific milestones. Missing any of these dates can mean the difference between receiving a check and waiting another three months.

Declaration Date: The Board’s Official Word

The declaration date is the day a company’s board of directors announces its intention to pay a dividend. During this announcement, the company specifies the amount of the dividend, the “ex-dividend date,” and the “payment date.” This announcement is a signal of financial health, as it demonstrates that the company has sufficient retained earnings to reward shareholders.

Ex-Dividend Date: The Crucial Cutoff

The ex-dividend date is perhaps the most important date for a trader. It represents the day on which the stock begins trading without the subsequent dividend value. To receive the upcoming dividend, you must own the stock before this date. If you buy a stock on its ex-dividend date, the seller—not you—will receive the dividend. Historically, a stock’s price often drops by approximately the amount of the dividend on this day to reflect the outflow of cash from the company’s books.

Record Date and Payment Date

The record date usually follows the ex-dividend date by one business day. It is the date the company reviews its books to identify all official shareholders. Finally, the payment date is the day the cash is actually deposited into your brokerage account or a check is mailed. This can occur anywhere from a few days to several weeks after the ex-dividend date.

Common Dividend Payment Frequencies

While companies have the legal freedom to pay dividends whenever they choose, most adhere to established market norms. These schedules allow investors to project their annual income and help companies manage their internal cash flow.

Quarterly Distributions: The Market Standard

In the United States, the vast majority of dividend-paying companies—including blue-chip giants like Coca-Cola, Apple, and Johnson & Johnson—distribute payments on a quarterly basis. This means shareholders receive a payment four times a year, usually aligning with the company’s fiscal quarters. This frequency provides a balance between providing regular income to shareholders and minimizing the administrative costs associated with processing payments.

Monthly Dividends: Ideal for Cash Flow

Certain types of investments, particularly Real Estate Investment Trusts (REITs) and Business Development Companies (BDCs), often pay dividends monthly. Companies like Realty Income (famously known as “The Monthly Dividend Company”) cater specifically to income-focused investors. Monthly dividends are highly sought after by retirees because they align perfectly with monthly bills and mortgage payments, making personal budgeting significantly easier.

Semi-Annual and Annual Payments

Outside of the United States, particularly in Europe and Australia, many companies opt for semi-annual or even annual distributions. In a semi-annual model, a company might pay a smaller “interim” dividend mid-year and a larger “final” dividend at the end of the fiscal year. While this requires more patience from the investor, it allows the company to retain more capital throughout the year for operational growth or debt reduction.

Special Dividends: The Occasional Bonus

A “special dividend” is a non-recurring payment that falls outside the normal schedule. These are usually the result of an exceptionally profitable year, the sale of a business segment, or a large influx of cash. For example, a company might pay its regular quarterly dividends but then issue a one-time special dividend of $5.00 per share because of a legal settlement or a windfall. While exciting, special dividends should not be relied upon for long-term financial planning.

Why Companies Choose Specific Payment Schedules

The decision regarding how often to pay dividends is a strategic one, influenced by a company’s business model, its industry standards, and its target investor base.

Aligning with Corporate Cash Flow

Capital-intensive industries or those with seasonal revenue cycles may find it difficult to commit to monthly payments. A retail giant might have massive cash reserves after the holiday season but tighter margins in the summer. By choosing a quarterly or annual schedule, the company ensures it has the liquidity necessary to cover the dividend without jeopardizing its daily operations or capital expenditures.

Attracting Specific Investor Demographics

A company’s dividend policy acts as a beacon for certain types of capital. Firms that pay monthly or have a long history of quarterly increases (often referred to as “Dividend Aristocrats” or “Dividend Kings”) attract long-term, “sticky” institutional and retail investors. These investors are less likely to sell during market volatility because they are focused on the income stream, which in turn helps stabilize the stock price.

Maintaining the “Dividend Aristocrat” Reputation

In the world of finance, consistency is key. A “Dividend Aristocrat” is an S&P 500 company that has increased its dividend every year for at least 25 consecutive years. For these companies, the frequency and reliability of the payment are matters of corporate pride and market signaling. Even a minor delay or a “flat” dividend (one that doesn’t increase) can lead to a sharp sell-off, as it may signal to the market that the company’s growth is stalling.

Strategic Investing: Maximizing Your Dividend Income

Once you understand the “how often” and the “why,” you can begin to use this knowledge to optimize your personal financial strategy.

Building a “Dividend Calendar” for Monthly Income

A common strategy for income investors is to ladder their portfolio. Since different companies pay their quarterly dividends in different months (e.g., Company A pays in Jan/Apr/Jul/Oct, while Company B pays in Feb/May/Aug/Nov), an investor can hand-pick 3–6 stocks that, together, ensure a paycheck arrives in their account every single month. This “synthetic monthly income” allows you to benefit from the growth of quarterly payers while maintaining the cash flow of a monthly schedule.

The Power of Dividend Reinvestment Plans (DRIPs)

For those who do not need the cash immediately, the frequency of dividends becomes a tool for compounding. A Dividend Reinvestment Plan (DRIP) automatically uses your dividend payment to buy more shares of the company, often with no commission fees. Because these new shares will also pay dividends in the next cycle, your “share count” grows exponentially over time. The more frequent the dividend (such as quarterly vs. annually), the more often your income is put back to work, accelerating the compounding effect.

Evaluating Yield vs. Sustainability

It is a common trap to chase the highest dividend yield without looking at the frequency or the “payout ratio.” A company paying a massive 12% yield monthly might be in financial distress, paying out more than it earns to keep investors from fleeing. Conversely, a company paying a modest 2% yield quarterly might have a payout ratio of only 30%, meaning the dividend is incredibly safe and has significant room to grow. Always prioritize the sustainability of the payment over the immediate size of the check.

Conclusion: Navigating the World of Passive Income

Understanding how often dividends are paid is a fundamental building block of financial literacy. Whether you are navigating the quarterly cycles of the S&P 500, the monthly distributions of REITs, or the occasional windfall of a special dividend, the timing of these payments dictates your liquidity and your long-term growth trajectory.

By mastering the dividend lifecycle—from the declaration date to the payment date—and strategically selecting companies that align with your cash flow needs, you can transform a volatile stock portfolio into a reliable “private pension.” Remember that consistency often outweighs the sheer volume of a payment. In the realm of personal finance, the goal is not just to get paid, but to build a system where the frequency and reliability of your income provide the freedom to pursue your long-term goals.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.