For any business with employees, understanding and correctly managing payroll taxes is not just a regulatory requirement; it’s a fundamental aspect of sound financial management. Payroll taxes represent a significant portion of a company’s operational costs and carry serious implications if mismanaged. From withholding the correct amounts from employee wages to remitting funds to the appropriate federal and state agencies on time, the process can seem daunting. However, breaking it down into manageable steps and understanding the underlying principles can transform this complex task into a streamlined, routine operation. This comprehensive guide will demystify payroll taxes, equipping business owners with the knowledge to navigate their obligations confidently and efficiently.

Understanding Your Payroll Tax Obligations

Before delving into the mechanics of payment, it’s crucial to grasp the landscape of payroll taxes themselves. These are not merely a single tax but a combination of various federal, state, and sometimes local levies that employers are responsible for collecting, contributing, and remitting.

What Are Payroll Taxes?

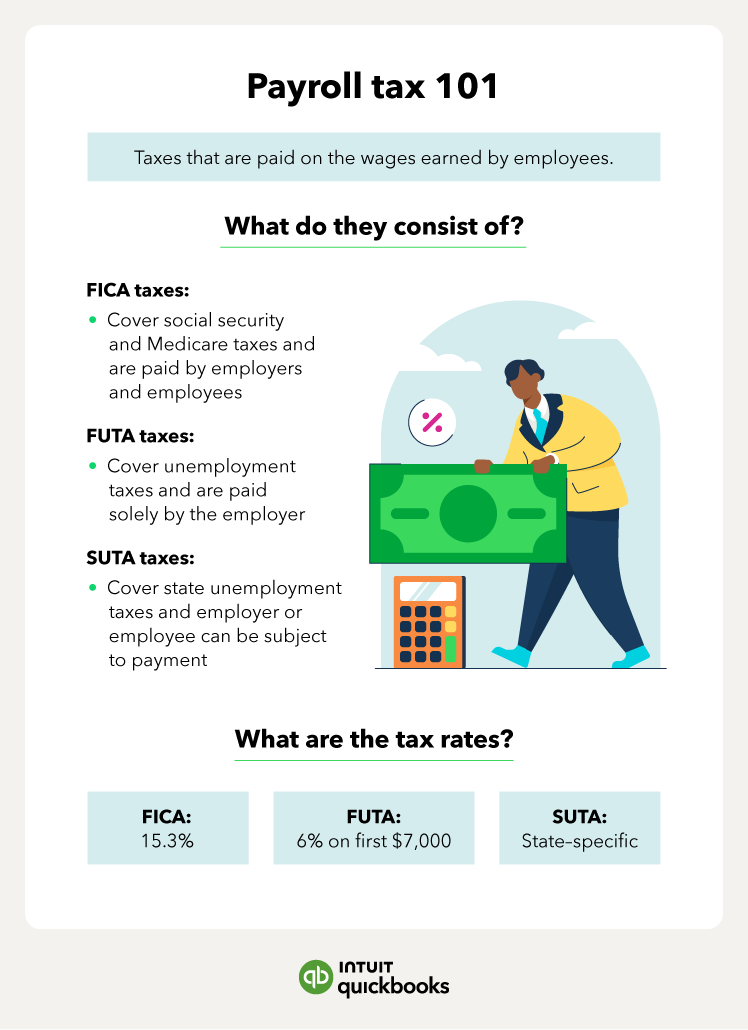

Payroll taxes are essentially taxes employers must withhold from employee paychecks or pay directly based on employee wages. They generally fall into two categories:

- Employee Contributions: These are taxes deducted directly from an employee’s gross pay. The employer’s role is to withhold these amounts and then remit them to the government on the employee’s behalf.

- Employer Contributions: These are taxes that the employer pays directly out of their own funds, in addition to the employee’s wages. These represent an additional cost to the business beyond the employee’s gross salary.

Key Federal Payroll Taxes

The federal government mandates several crucial payroll taxes that every employer must contend with. These include:

- Federal Insurance Contributions Act (FICA) Taxes: This encompasses Social Security and Medicare taxes.

- Social Security: Funds retirement, disability, and survivor benefits. Both employers and employees typically pay 6.2% each on wages up to an annually adjusted maximum (wage base limit).

- Medicare: Funds hospital insurance. Both employers and employees typically pay 1.45% each, with no wage base limit. Additionally, high-income employees may be subject to an Additional Medicare Tax, which only the employee pays.

- Federal Unemployment Tax Act (FUTA) Taxes: FUTA taxes fund unemployment compensation for workers who lose their jobs. This tax is paid solely by the employer. The federal FUTA tax rate is 6.0% on the first $7,000 of each employee’s wages, though employers can often receive a significant credit (up to 5.4%) for timely payment of state unemployment taxes, effectively reducing the federal rate to 0.6%.

State and Local Payroll Taxes

Beyond federal requirements, most states impose their own set of payroll taxes. These often include:

- State Unemployment Insurance (SUI) Taxes: Similar to FUTA, these funds state unemployment benefits. Rates vary significantly by state and are often experience-rated, meaning a business with more former employees claiming unemployment benefits may pay a higher rate. SUI is generally paid by the employer, though a few states require employee contributions.

- State Income Tax Withholding: Most states require employers to withhold state income tax from employee wages and remit it to the state. The rates and rules vary widely. A handful of states do not have state income tax.

- Local Payroll Taxes: Some cities or localities may impose their own income taxes or other specific payroll-related taxes. It’s essential for businesses to be aware of and comply with any local ordinances where they operate.

Who is an Employee vs. Independent Contractor?

One of the most critical distinctions in payroll tax compliance is correctly classifying workers. Misclassifying an employee as an independent contractor can lead to significant penalties, back taxes, and legal challenges. The IRS and state labor departments use various criteria to determine worker status, generally focusing on the degree of behavioral control, financial control, and the type of relationship between the worker and the business. Employees typically have income taxes, Social Security, and Medicare taxes withheld from their pay, and the employer pays FUTA and SUI taxes. For independent contractors, the business generally does not withhold taxes or pay employer-side payroll taxes; the contractor is responsible for their own self-employment taxes. Making the correct determination from the outset is paramount.

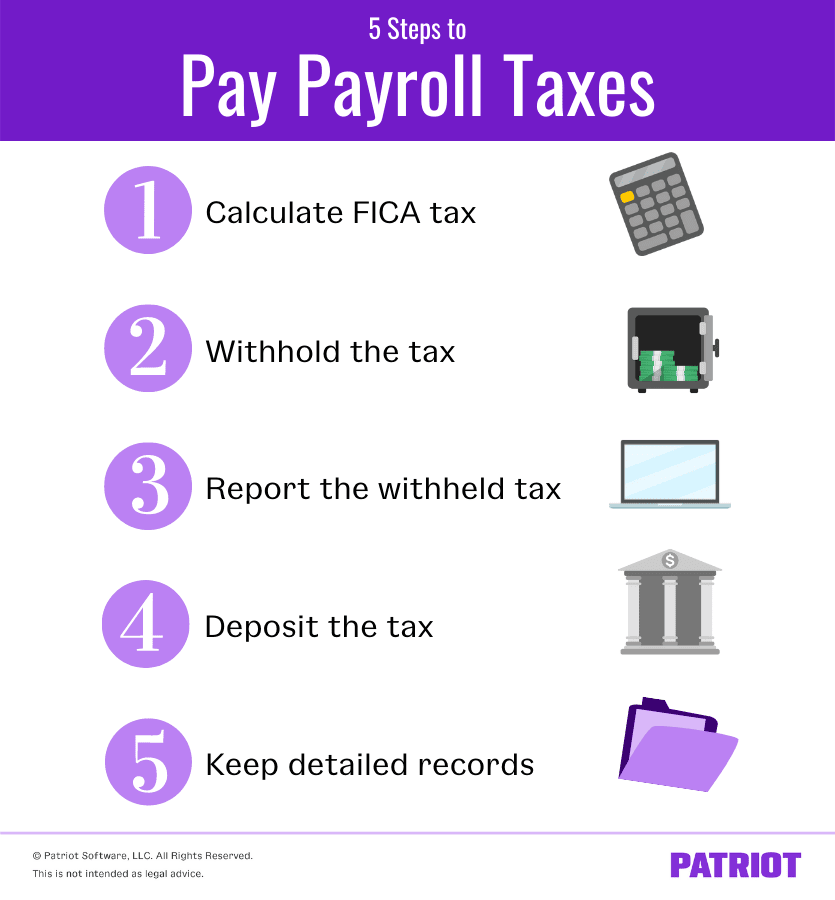

The Mechanics of Withholding and Reporting

Once the types of taxes are understood, the next step involves the practical aspects of calculation, withholding, and reporting these amounts to the government. This phase demands precision and adherence to strict deadlines.

Calculating Withholdings

The process begins with accurately calculating how much to withhold from each employee’s paycheck.

- Form W-4: Every new employee must complete a Form W-4, Employee’s Withholding Certificate. This form provides the employer with critical information, such as the employee’s marital status, number of dependents, and any additional amounts to withhold, which are used to determine the correct federal income tax withholding. Employees can adjust their W-4 at any time to reflect changes in their financial situation.

- Tax Tables and Withholding Calculators: The IRS provides detailed tax tables and various calculation methods (e.g., wage bracket method, percentage method) to help employers determine the exact amount of federal income tax to withhold based on an employee’s W-4 and gross pay. Similar tables and guidelines exist for state income tax withholding.

- Fixed Percentage Taxes: FICA taxes (Social Security and Medicare) are generally calculated as a fixed percentage of an employee’s gross wages, up to the annual Social Security wage base limit.

The Importance of Accurate Record-Keeping

Meticulous record-keeping is not just good practice; it’s a legal necessity. Businesses must maintain detailed records for each employee, including:

- Name, address, and Social Security number

- Dates of employment

- Wages paid (gross and net)

- Amounts and dates of tax withholdings and deposits

- Dates and amounts of fringe benefits provided

- Forms W-4 and W-2

These records are crucial for generating year-end forms, responding to inquiries from tax authorities, and substantiating tax filings.

Forms and Deadlines

Payroll taxes are remitted and reported through a series of specific forms, each with its own filing frequency and deadlines.

- Form 941, Employer’s QUARTERLY Federal Tax Return: Most employers use Form 941 to report federal income tax, Social Security, and Medicare taxes withheld from employee wages and the employer’s share of Social Security and Medicare taxes. This form is typically filed quarterly.

- Form 940, Employer’s Annual Federal Unemployment (FUTA) Tax Return: This form is used to report FUTA taxes and is filed annually.

- Form W-2, Wage and Tax Statement: Employers must provide each employee with a Form W-2 by January 31st of the following year, reporting their annual wages and taxes withheld.

- Form W-3, Transmittal of Wage and Tax Statements: This form is filed with the Social Security Administration along with all copies of the W-2s.

- State and Local Forms: Businesses will also need to comply with state-specific filing requirements, which often include quarterly or annual unemployment tax reports and state income tax withholding returns.

Depositing Taxes (EFTPS)

While reporting is done through forms, the actual payment of federal payroll taxes is typically made via the Electronic Federal Tax Payment System (EFTPS). Most employers are required to use EFTPS to deposit federal income tax, Social Security, and Medicare taxes. Deposit schedules (monthly or semi-weekly) depend on the total tax liability reported during a look-back period. FUTA taxes also have their own deposit requirements, often triggered when the cumulative FUTA tax liability exceeds a certain threshold. Failing to deposit taxes on time and correctly can result in significant penalties.

Setting Up Your Payroll System

Managing payroll taxes manually can be incredibly time-consuming and prone to error, especially as a business grows. Establishing an efficient payroll system is key to ensuring compliance and freeing up valuable business resources.

Manual Payroll: Pros and Cons

For very small businesses with only one or two employees, manual payroll might seem like a cost-saving option initially. This involves calculating withholdings, preparing checks, tracking tax liabilities, and remembering deposit schedules all by hand or using spreadsheets.

- Pros: Minimal direct cost for software or services.

- Cons: Extremely time-intensive, high risk of calculation errors, difficulty keeping up with changing tax laws, easily misses deposit deadlines, and provides no direct integration with accounting. For most businesses, the risks far outweigh the perceived savings.

Payroll Software Solutions

A more scalable and reliable approach is to use dedicated payroll software. These solutions automate many of the complex calculations and administrative tasks.

- Features: Automate tax withholdings, calculate gross-to-net pay, generate paychecks or direct deposits, track accrued leave, remind of tax deadlines, and often prepare many of the required federal and state tax forms.

- Benefits: Reduces errors, saves time, helps ensure compliance, and often integrates with general ledger accounting software.

- Examples: QuickBooks Payroll, Patriot Payroll, Gusto, ADP Run (small business focus). These range from basic to comprehensive, often with tiered pricing based on the number of employees and features needed.

Full-Service Payroll Providers

For businesses that prefer to completely outsource their payroll responsibilities, full-service payroll providers are an excellent option.

- Services: Handle everything from calculating wages and taxes, processing direct deposits, filing all federal and state payroll tax forms, making tax deposits on behalf of the business, and managing year-end W-2 and 1099 distribution.

- Benefits: Complete peace of mind, minimizes internal administrative burden, ensures expert compliance with complex and ever-changing tax laws, and often includes robust reporting and HR support.

- Examples: ADP, Paychex, TriNet, Insperity. These services typically come with a higher cost but offer unparalleled convenience and risk mitigation.

Integrating Payroll with Accounting

Seamless integration between payroll and accounting systems is crucial for accurate financial reporting and analysis. When these systems are linked, payroll entries (wages, taxes, benefits) automatically flow into the general ledger, updating expense accounts, liability accounts, and cash balances. This eliminates manual data entry, reduces reconciliation errors, and provides real-time visibility into labor costs and overall financial health. Most modern payroll software and full-service providers offer robust integration capabilities with popular accounting platforms like QuickBooks, Xero, and Sage.

Avoiding Common Payroll Tax Pitfalls

Even with a robust system, pitfalls can emerge. Proactive awareness and adherence to best practices are essential for long-term compliance and financial health.

Penalties for Late or Incorrect Payments

The IRS and state tax authorities are stringent about payroll tax compliance. Penalties can be severe for:

- Failure to deposit taxes on time: Penalties can range from 2% to 15% of the underpayment, depending on how late the deposit is.

- Failure to file correct information returns (e.g., Form 941, W-2s): Penalties vary based on the size of the business and how late the filing is.

- Failure to pay the correct amount of tax: This can lead to assessments of back taxes, interest, and additional penalties.

- Trust Fund Recovery Penalty (TFRP): Perhaps the most serious, this penalty can be levied against individuals (e.g., business owners, officers, or responsible employees) if income taxes and FICA taxes withheld from employees’ wages are not paid to the government. The TFRP can be equal to the full amount of the unpaid trust fund taxes.

The Dangers of Misclassifying Workers

As mentioned, incorrectly classifying employees as independent contractors is a significant risk. If the IRS or state authorities determine misclassification, the business could be liable for:

- Back payroll taxes (both employer and employee portions, including interest and penalties).

- Unemployment taxes.

- Workers’ compensation premiums.

- Employee benefits (if applicable).

- Potential lawsuits from misclassified workers.

It’s always better to err on the side of caution or seek professional advice when in doubt about a worker’s classification.

Keeping Up with Regulatory Changes

Payroll tax laws are not static. They are subject to frequent changes at federal, state, and local levels, including changes to tax rates, wage base limits, filing thresholds, and new regulations (e.g., changes related to COVID-19 relief or new state family leave programs). Businesses must have a system in place to monitor these changes and adjust their payroll processes accordingly. This is where payroll software or a full-service provider proves invaluable, as they typically update their systems automatically to reflect the latest regulations.

The Importance of Professional Advice

While this guide provides a solid foundation, payroll tax is a complex area. Business owners should consider consulting with qualified professionals, such as a Certified Public Accountant (CPA) or a payroll specialist, particularly when:

- Starting a new business or hiring the first employees.

- Operating in multiple states or localities.

- Experiencing significant growth or changes in workforce structure.

- Unsure about worker classification.

- Facing complex benefit structures or compensation plans.

A professional can offer tailored advice, ensure compliance, and help optimize tax strategies, safeguarding the business from costly errors.

Paying payroll taxes correctly is a non-negotiable aspect of running a legitimate business. It involves a detailed understanding of various tax types, meticulous record-keeping, timely deposits, and accurate reporting. By establishing a robust payroll system, whether through advanced software or a full-service provider, and by staying vigilant against common pitfalls, business owners can navigate these obligations with confidence. This commitment to compliance not only protects the business from penalties but also fosters trust with employees and maintains a healthy financial standing, allowing the business to focus on its core mission and growth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.