The landscape of personal and business finance has undergone a profound transformation, with digital platforms revolutionizing how we manage our money. Among these changes, the ability to pay your IRS bill online stands out as a critical advancement, offering unparalleled convenience, security, and efficiency. Gone are the days when a check in the mail was the sole method for settling your tax obligations. Today, a robust suite of online tools provided by the Internal Revenue Service (IRS) empowers taxpayers to manage their financial duties with just a few clicks. This guide delves into the nuances of online IRS payments, providing insights into various methods, best practices, and strategic considerations for responsible financial management in the digital age.

The Evolution of Tax Payments: Embracing Digital Convenience

The transition from traditional paper-based transactions to digital financial management marks a significant leap forward. For decades, paying taxes often involved preparing a physical check, addressing an envelope, and trusting the postal service with sensitive financial information. While this method still exists, the advent of the internet has paved the way for a more streamlined, secure, and accessible approach to fulfilling one’s tax responsibilities.

From Paper Checks to Pixelated Payments

The journey from paper checks to pixelated payments is one driven by technological progress and the increasing demand for instant, reliable services. The IRS, like many other government agencies and financial institutions, has invested heavily in developing and securing online payment gateways. This evolution isn’t merely about convenience; it’s about building a financial ecosystem that aligns with modern living, where time is precious, and digital literacy is commonplace. The shift caters to a diverse demographic, from tech-savvy millennials managing their first independent tax filings to seasoned business owners optimizing their financial workflows.

The Benefits of Online Tax Transactions: Efficiency, Security, Record-Keeping

Opting for online IRS payments unlocks a myriad of benefits that extend beyond simple convenience:

- Efficiency: Online payments can be made 24/7, from anywhere with an internet connection. This eliminates mailing delays, trips to the post office, and the anxiety of missed deadlines due to unforeseen circumstances. Payments are processed quickly, often within a day or two, providing immediate peace of mind.

- Security: While concerns about online security are valid, the IRS’s official payment platforms employ advanced encryption and security protocols to protect taxpayer data. These systems are designed to be more secure than sending a check through the mail, which can be vulnerable to theft or loss. Authenticated access and multi-factor authentication add additional layers of protection.

- Record-Keeping: Digital payments create an immediate and verifiable electronic trail. Taxpayers receive instant confirmations, and transaction histories are often accessible through the payment portals for several years. This digital paper trail is invaluable for financial planning, auditing, and resolving any potential discrepancies with the IRS. It simplifies the process of proving that a payment was made, when it was made, and for how much.

Demystifying the IRS’s Digital Infrastructure

The IRS has built a robust digital infrastructure to support various online payment methods, each tailored to different taxpayer needs and preferences. Understanding these options is crucial for making informed financial decisions. Far from being a monolithic system, the IRS offers distinct portals and partnerships designed to cater to individual taxpayers, businesses, and tax professionals alike. This multi-faceted approach ensures accessibility and adaptability, reflecting the complex nature of tax obligations across different entities.

Official IRS Online Payment Methods Explained

The IRS offers several official methods for paying your tax bill online, each with its own features, benefits, and potential limitations. Choosing the right method depends on your specific financial situation, comfort with technology, and whether you are an individual taxpayer or a business entity.

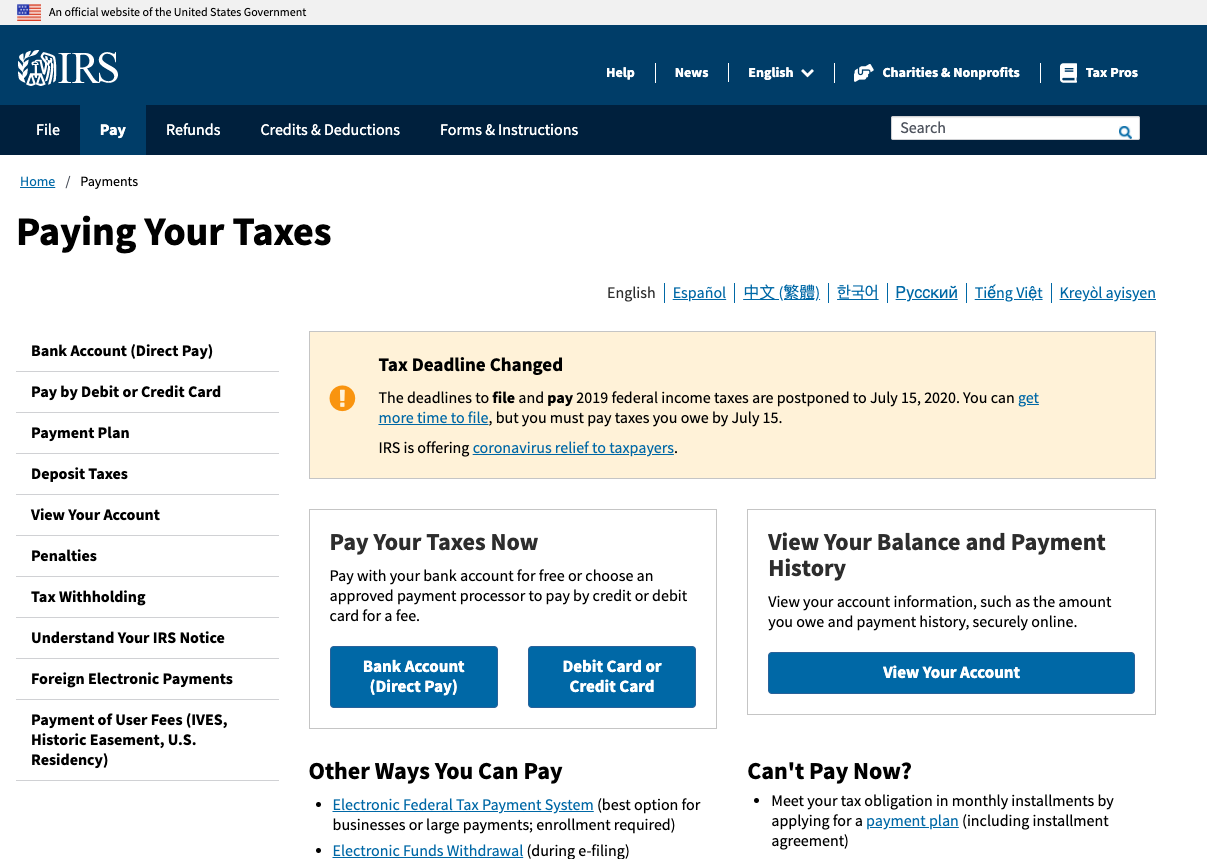

IRS Direct Pay: Your Free Bank Account Transfer Option

IRS Direct Pay is arguably the most straightforward and cost-effective method for individual taxpayers to pay their federal taxes directly from their checking or savings account.

- What it is: A free, secure web application provided by the IRS that allows you to make payments directly from your bank account (checking or savings) without any fees.

- How it works: You provide your bank account number, routing number, and verify your identity using past tax filing information (e.g., your prior year’s adjusted gross income). You can schedule payments up to 365 days in advance and modify or cancel them up to two business days before the scheduled payment date.

- Limits: Primarily for individuals. There are no payment limits, but you can make two payments within a 24-hour period.

- Benefits: Absolutely free, direct bank-to-IRS transfer, easy to use, and provides instant confirmation. This method is ideal for those who prefer to avoid third-party fees and appreciate direct control over their payments.

Electronic Federal Tax Payment System (EFTPS): The Business & Power User Choice

The Electronic Federal Tax Payment System (EFTPS) is the IRS’s long-standing electronic payment option, particularly popular among businesses and tax professionals due to its comprehensive features and flexibility.

- What it is: A free service from the U.S. Department of the Treasury that allows individual and business taxpayers to pay federal taxes electronically. It’s often mandatory for businesses with certain tax liabilities.

- Enrollment: Requires a one-time enrollment process that can take 5-7 business days to complete, as the IRS mails you a PIN after verifying your information.

- Scheduling Payments: Once enrolled, you can schedule payments up to 365 days in advance. EFTPS supports various tax types, including income tax, employment tax, estimated tax, and excise tax.

- Benefits for Businesses: EFTPS is indispensable for businesses needing to make multiple types of tax payments, manage payroll taxes, and comply with IRS regulations that often mandate electronic payments for larger entities. It offers robust record-keeping features and allows for multiple users within a single business account, making it suitable for accounting departments.

Debit/Credit Card & Digital Wallet Payments: Flexibility with a Fee

For those who prioritize flexibility and convenience, or wish to leverage credit card rewards, paying your IRS bill with a debit card, credit card, or digital wallet (like PayPal) is an option, though it comes with a processing fee.

- Authorized Third-Party Processors: The IRS does not directly process these payments. Instead, it authorizes third-party payment processors (e.g., ACI Payments, Inc., PayUSAtax, Official Payments) to handle these transactions. Each processor sets its own fees, which typically range from 1.87% to 1.98% for credit cards and a flat fee for debit cards (usually around $2.50-$3.95).

- Fees: It’s crucial to check the fee structure of each processor before making a payment, as these fees can add up, especially for large tax bills.

- Convenience vs. Cost: This method offers immense flexibility, allowing you to use funds from your credit card, potentially earning rewards points or managing cash flow. However, the convenience comes at a cost, which should be weighed against the benefits. For some, the ability to delay payment or earn rewards outweighs the processing fee. For others, particularly those with a large tax liability, the fees can be substantial, making Direct Pay or EFTPS a more financially prudent choice.

Other Digital Methods (e.g., Electronic Funds Withdrawal during e-filing)

Beyond these primary methods, there are other integrated digital payment options:

- Electronic Funds Withdrawal (EFW): If you e-file your tax return (either through tax preparation software or a tax professional), you often have the option to authorize an electronic funds withdrawal directly from your bank account. This is usually set up when you submit your return and is a seamless way to pay simultaneously with filing.

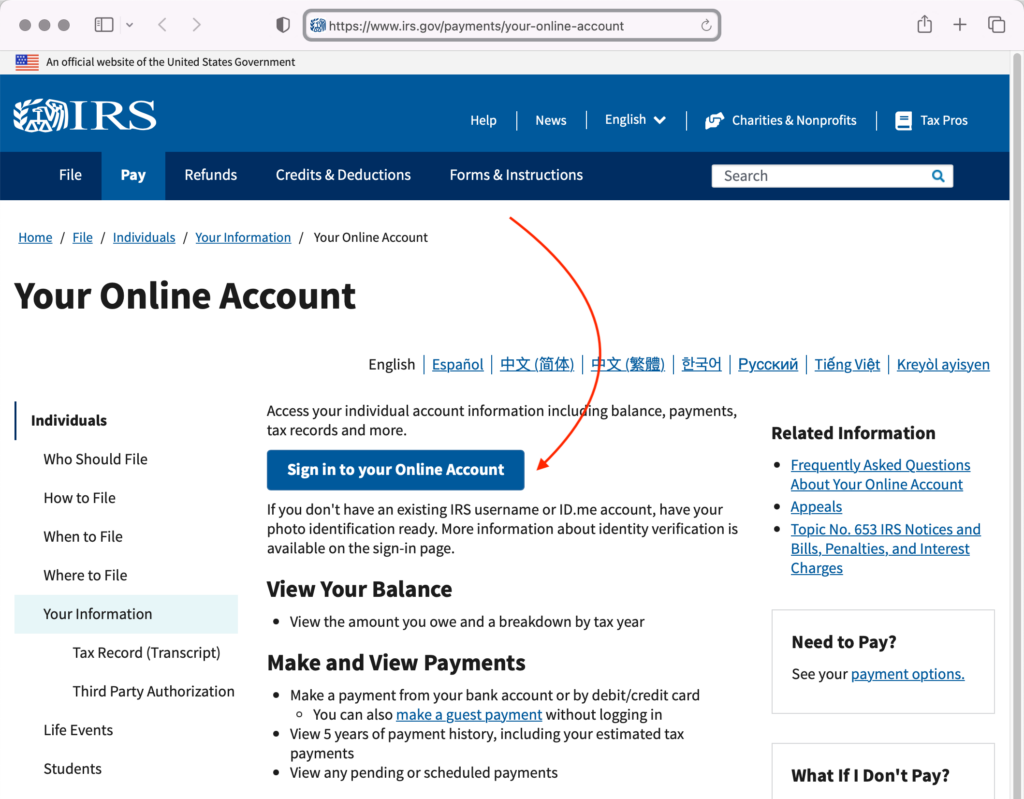

- IRS Tax Account: Through your online IRS account, you can access your tax records, view payment history, and make payments using a secure portal, often linking back to Direct Pay or other methods.

Navigating Common Pitfalls and Ensuring Secure Transactions

While online payments offer unparalleled convenience, it’s essential to approach them with diligence to avoid common pitfalls and ensure the security of your financial data. Responsible online financial management requires vigilance and attention to detail.

Verifying Official IRS Channels: Avoiding Scams and Phishing

The digital realm, while efficient, is also a breeding ground for scams. Taxpayers are frequently targeted by sophisticated phishing attempts, imposter scams, and fraudulent websites designed to mimic official IRS portals.

- Always Start with IRS.gov: The golden rule is to always initiate your payment process directly from the official IRS website (www.irs.gov). Never click on links in unsolicited emails or text messages claiming to be from the IRS. The IRS typically communicates via mail for official matters and does not demand immediate payment via phone or email.

- Look for Secure Connections: Ensure the website address begins with “https://” (the ‘s’ indicates a secure connection) and look for a padlock icon in your browser’s address bar.

- Beware of Pressure Tactics: Scammers often use aggressive tactics, threatening legal action or arrest for non-payment. The IRS will never threaten you in this manner or demand payment via gift cards or wire transfers.

Understanding Payment Deadlines and Penalties

A crucial aspect of managing your tax obligations is understanding and adhering to payment deadlines. Missing a deadline can result in penalties and interest, adding to your financial burden.

- Standard Deadlines: Tax Day (usually April 15th) is the primary deadline for filing returns and paying any taxes due. However, estimated tax payments for self-employed individuals and those with significant non-wage income have quarterly deadlines.

- Extensions vs. Payment Extensions: Filing an extension for your tax return (Form 4868) extends the time to file, but not the time to pay. You are still expected to pay any estimated tax due by the original deadline to avoid penalties.

- Penalties and Interest: The IRS charges penalties for late filing, late payment, and underpayment of estimated tax. Interest also accrues on unpaid balances. Understanding these can motivate timely payments and proactive financial planning. Online payment methods make it easier to meet these deadlines, especially when making payments close to the cut-off time.

Record Keeping: The Digital Paper Trail for Peace of Mind

One of the most significant advantages of online payments is the automatic creation of a digital record. However, it’s prudent to go a step further to ensure comprehensive record-keeping.

- Save Confirmations: Always save or print the confirmation screen or email you receive after making an online payment. This serves as immediate proof of transaction.

- Maintain Digital Files: Organize your digital tax records in a dedicated folder on your computer or cloud storage. This includes your tax returns, payment confirmations, and any related correspondence.

- Check Your IRS Account: Regularly review your IRS online account (if you have one) to confirm that payments have been posted correctly and to monitor your overall tax liability and payment history.

Addressing Payment Issues and Seeking Assistance

Despite the efficiency of online systems, issues can sometimes arise. Knowing how to address them is part of robust financial management.

- Contact Your Bank/Processor First: If a payment shows as successful on the IRS side but not on your bank statement, or vice-versa, contact your bank or the third-party payment processor first.

- Contact the IRS: If you’ve exhausted other avenues or suspect an IRS-specific issue, contact the IRS directly. Have all your payment confirmations and relevant tax information ready.

- Payment Plans: If you genuinely cannot pay your tax bill in full by the deadline, the IRS offers various payment options, including short-term payment plans and installment agreements. It’s always better to communicate with the IRS and set up a plan than to ignore the bill.

Strategic Considerations for Managing Your Tax Liability

Paying your IRS bill online is not just a transactional act; it’s an integral part of broader financial planning and strategy. Effective tax management requires foresight, discipline, and an understanding of available financial tools.

Budgeting for Tax Season: Proactive Financial Planning

One of the most effective strategies for managing tax liabilities is proactive budgeting throughout the year. Instead of facing a large, unexpected bill on Tax Day, responsible financial planning allocates funds specifically for taxes.

- Estimated Tax Payments: For self-employed individuals, freelancers, and those with significant non-wage income, making quarterly estimated tax payments is crucial. This avoids a large tax bill at year-end and prevents underpayment penalties.

- Dedicated Savings: Consider setting up a separate savings account solely for tax obligations. Regularly transfer a percentage of your income into this account, ensuring funds are available when tax payments are due.

- Cash Flow Management: For businesses, incorporating tax payments into cash flow projections is vital. This ensures sufficient liquidity to meet operational needs while fulfilling tax responsibilities.

The Role of Estimated Taxes and Quarterly Payments

Estimated taxes are designed to ensure that taxpayers with income not subject to withholding (like self-employment income, interest, dividends, rent, alimony, etc.) pay their income tax as they earn it throughout the year.

- “Pay-as-You-Go”: The U.S. tax system operates on a “pay-as-you-go” principle. If you don’t have enough tax withheld from your salary or pension, you may need to make estimated tax payments.

- Avoiding Penalties: Failing to pay enough tax throughout the year through withholding or estimated payments can result in an underpayment penalty. The IRS provides Form 1040-ES, Estimated Tax for Individuals, and Publication 505, Tax Withholding and Estimated Tax, to help you calculate and pay your estimated taxes correctly. Online payment methods like IRS Direct Pay and EFTPS are ideal for making these quarterly payments promptly.

Payment Plans and Offers in Compromise: When You Can’t Pay in Full

Life happens, and sometimes, despite best efforts, you might find yourself unable to pay your entire tax bill by the deadline. The IRS offers solutions for taxpayers facing financial hardship.

- Short-Term Payment Plan: You may be granted up to 180 days to pay your tax liability in full, although interest and penalties still apply.

- Installment Agreement: This allows you to make monthly payments for up to 72 months. While penalties and interest still accrue, they may be reduced. This option is available if you owe $50,000 or less in combined tax, penalties, and interest (for individuals), or $25,000 or less (for businesses) and have filed all required returns. You can often set up an installment agreement online.

- Offer in Compromise (OIC): An OIC allows certain taxpayers to settle their tax liability with the IRS for a lower amount than what they originally owe. This is typically an option when you can prove that paying the full amount would create a significant financial hardship, or there’s doubt about the amount owed or collectibility. An OIC is a more complex process and is generally a last resort.

- Proactive Engagement: The key is to be proactive. If you anticipate difficulty paying, contact the IRS or a tax professional as soon as possible. Ignoring the issue will only lead to more severe penalties and stress.

Leveraging Online Tools for Financial Foresight

The availability of online payment options is just one facet of the digital financial ecosystem. Taxpayers can leverage a host of other online tools for greater financial foresight and control:

- Tax Software: Modern tax preparation software not only helps you file but can also integrate with payment options, helping you calculate estimated taxes and schedule payments.

- Budgeting Apps: Personal finance apps can help track income and expenses, making it easier to set aside funds for taxes and monitor overall financial health.

- IRS Online Account: This portal allows you to access your tax records, view past payments, check payment history, and even view notices and communications from the IRS. This central hub for your tax information is invaluable for managing your financial relationship with the agency.

The Future of Tax Payments: Trends and Innovations

The digital evolution of tax payments is an ongoing process. As technology advances, we can anticipate further innovations that will enhance the user experience, security, and efficiency of fulfilling our tax obligations.

Enhanced User Experience and Integration

Future developments will likely focus on creating a more seamless and intuitive user experience. This could involve:

- Streamlined Interfaces: More user-friendly interfaces for all IRS online services, reducing complexity and increasing accessibility for a wider range of taxpayers.

- Greater Integration: Tighter integration between tax preparation software, banking platforms, and IRS payment systems, allowing for real-time payment scheduling and automated compliance checks.

- Mobile-First Design: Optimized mobile apps and responsive website designs to cater to the growing number of taxpayers who manage their finances on smartphones and tablets.

Blockchain and Distributed Ledger Technology in Taxation

While still in its nascent stages for government applications, blockchain technology holds promise for future tax administration.

- Enhanced Security and Transparency: Blockchain’s inherent security and immutable ledger could revolutionize how tax payments are recorded and verified, potentially reducing fraud and increasing public trust.

- Automated Compliance: Smart contracts built on blockchain could automate certain tax calculations and payments, especially for complex transactions or cross-border trade, offering real-time compliance.

- Digital Identity: Secure digital identities powered by blockchain could simplify taxpayer authentication and further protect personal information.

AI-Powered Tax Assistants and Automation

Artificial intelligence and machine learning are poised to transform various aspects of finance, including tax management.

- Personalized Guidance: AI-powered chatbots and virtual assistants could provide personalized guidance on tax questions, payment options, and compliance requirements, available 24/7.

- Predictive Analytics: AI could analyze financial data to predict potential tax liabilities, recommend optimal payment strategies, and flag anomalies that might indicate errors or fraud.

- Automated Reconciliation: AI tools could automate the reconciliation of payments and records, reducing manual effort and improving accuracy for both taxpayers and the IRS.

In conclusion, paying your IRS bill online is no longer a niche option but a mainstream, secure, and highly efficient method of fulfilling your tax obligations. By understanding the various official payment channels, adhering to best practices for security and record-keeping, and integrating tax management into your broader financial strategy, taxpayers can navigate the complexities of the tax system with greater confidence and control. As digital finance continues to evolve, embracing these tools and staying informed about future innovations will be key to smart, responsible financial stewardship.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.