In the intricate world of personal finance, understanding every facet of your banking relationship is paramount. One term that often arises, sometimes with a sense of dread, is “overdraft.” While the title “How to Overdraft Chase” might suggest a guide to intentionally trigger this financial event, a truly insightful exploration within the Money niche must focus on understanding, managing, and ultimately preventing overdrafts. For many, an overdraft is an accidental consequence of mismanaging funds, leading to fees and potential financial stress. This article will demystify overdrafts specifically within the context of Chase Bank, explaining what they are, how Chase handles them, and most importantly, how to navigate them effectively and avoid them altogether through proactive financial management.

Understanding Overdrafts: What They Are and Why They Happen

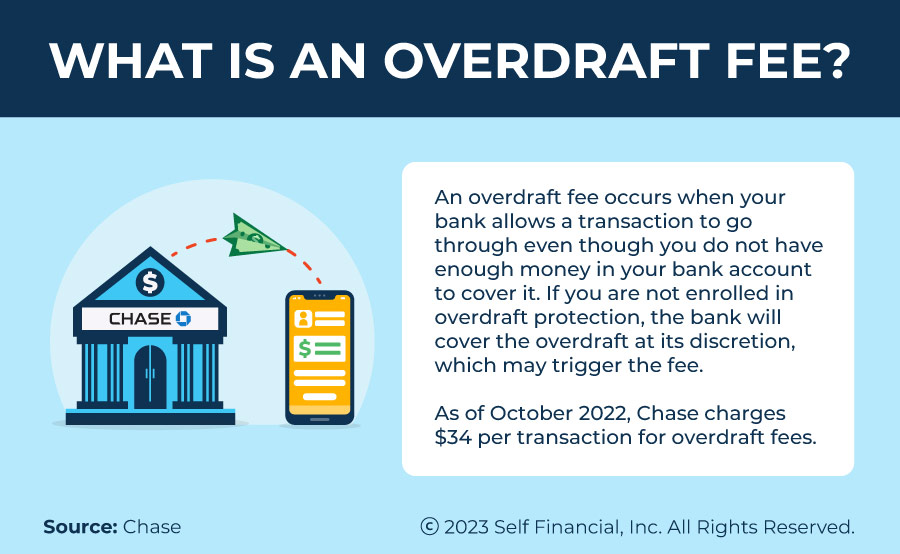

An overdraft occurs when you make a transaction, such as a debit card purchase, an ATM withdrawal, or a check payment, that exceeds the available funds in your checking account. Rather than declining the transaction, your bank may choose to cover the amount, effectively lending you the difference. While this can prevent immediate embarrassment or inconvenience, it almost always comes with a cost: an overdraft fee.

Defining Overdrafts in Banking

At its core, an overdraft is a temporary negative balance in your checking account. Banks generally have policies outlining when they will permit an overdraft. Historically, banks would often cover any transaction, but regulations have evolved to give consumers more control. For instance, for one-time debit card purchases and ATM withdrawals, banks must obtain your explicit permission (opt-in) to charge you an overdraft fee and cover the transaction. Without this opt-in, such transactions would typically be declined if funds are insufficient. However, for checks, ACH payments (like automatic bill pay), and recurring debit card payments, banks may still process the transaction and charge an overdraft fee, even if you haven’t opted into overdraft protection for debit card/ATM transactions.

Common Scenarios Leading to an Overdraft

Overdrafts aren’t always a result of outright financial neglect; they can stem from a variety of common situations:

- Timing Discrepancies: A check you wrote clears before a deposit you made is fully processed and available.

- Forgetting Automatic Payments: Recurring bills (utilities, subscriptions) may debit your account when you weren’t expecting it or when your balance was lower than anticipated.

- Miscalculating Balances: Relying solely on your “available balance” without accounting for pending transactions or holds can be misleading. For example, a gas station pre-authorization might be higher than your actual purchase, or a hotel might place a hold for incidentals.

- Unforeseen Expenses: An emergency or unexpected cost can deplete your funds quicker than planned, leaving insufficient money for subsequent transactions.

- Multiple Small Transactions: Sometimes, several small transactions in quick succession can chip away at a seemingly adequate balance, leading to an overdraft.

The Immediate and Long-Term Implications

The immediate implication of an overdraft is the fee, which can range from $30 to $35 per incident at many large banks, including Chase. Some banks also have limits on how many overdraft fees they can charge per day, or offer a “grace period” or “buffer” amount before a fee is assessed. If your account remains negative for an extended period, you might incur additional extended overdraft fees.

Long-term, frequent overdrafts can signal poor financial health. While they generally don’t directly impact your credit score (as they aren’t reported to major credit bureaus like unpaid loans), persistent account issues could lead to your bank closing your account. If your account is closed with an outstanding negative balance that goes to collections, that could negatively affect your credit score. Furthermore, a history of frequent overdrafts can be reported to specialized consumer reporting agencies like ChexSystems, which banks use to assess risk when opening new accounts, potentially making it difficult to open a checking account elsewhere.

Chase Bank’s Overdraft Policies and Services

As one of the largest financial institutions in the U.S., Chase Bank has comprehensive policies regarding overdrafts. Understanding these is crucial for anyone banking with them. Their approach is structured around standard practices and various protection options.

Chase’s Standard Overdraft Practices

Chase typically charges an overdraft fee of $34 for each transaction they cover that overdraws your account by more than $50. They limit the number of overdraft fees to a maximum of three per business day. This means if you have multiple transactions pushing your account into the negative, you could potentially accrue up to $102 in fees in a single day. Chase also offers a “buffer” system where transactions that overdraw your account by $50 or less generally won’t incur an overdraft fee. If your account is overdrawn by more than $5, and you make a deposit or transfer to bring your account positive by the end of the business day, Chase may waive the fee.

Opt-in vs. Opt-out for Overdraft Protection

Federal regulations distinguish between different types of transactions when it comes to overdrafts:

- Debit Card Purchases and ATM Withdrawals: For these “one-time” transactions, Chase requires your explicit consent (an “opt-in”) to charge you an overdraft fee and process the transaction. If you don’t opt-in, such transactions will simply be declined if you don’t have enough money, incurring no fee. This is generally the recommended approach for most consumers unless the absolute certainty of a transaction clearing is critical (e.g., medical emergency).

- Checks, ACH Payments, and Recurring Debit Card Transactions: For these types of transactions (e.g., automatic bill payments, direct debits), Chase may still process the payment and charge an overdraft fee, even if you haven’t opted in for debit card/ATM overdraft protection. This is an important distinction often misunderstood, highlighting the need for careful balance monitoring.

You can typically manage your overdraft settings through your Chase online banking portal, mobile app, or by contacting customer service.

Exploring Chase’s Overdraft Protection Options

Chase offers several ways to help prevent overdrafts, or at least mitigate their costs:

- Linked Savings Account: You can link a Chase savings account to your checking account. If you overdraw, funds are automatically transferred from your savings to cover the deficit. While this helps avoid an overdraft fee, Chase does charge a $12 “Overdraft Protection Transfer Fee” per day the transfer occurs. This is still significantly less than an overdraft fee.

- Linked Line of Credit: For eligible customers, Chase may offer an overdraft line of credit. If your checking account is overdrawn, funds are automatically drawn from this line of credit. This functions like a small loan, accruing interest, but again, it typically avoids the higher overdraft fees.

- Chase Overdraft Assist℠: This program may waive the Overdraft Protection Transfer Fee (from a linked savings account) and the Overdraft Fee if you bring your checking account balance to a positive amount by the end of the next business day after the account goes negative. This is a significant benefit designed to help customers quickly rectify an overdraft without incurring fees, provided they act promptly. Eligibility criteria may apply.

Navigating an Overdraft with Chase: Practical Steps

Discovering an overdraft can be stressful, but knowing what to do can help you manage the situation effectively and minimize repercussions. Prompt action is key.

Identifying an Overdraft: Notifications and Account Monitoring

Chase is generally good about notifying customers of potential or actual overdrafts. You might receive an email, text alert, or notification within the mobile app. However, it’s always best practice to proactively monitor your account:

- Regularly Check Your Balance: Don’t just check once a week; glance at your account daily, especially if you have pending transactions or automatic payments due.

- Set Up Account Alerts: Utilize Chase’s online banking features to set up low-balance alerts, transaction alerts, and actual overdraft alerts. These can be customized to your preferred threshold and delivery method.

- Review Your Transaction History: Regularly compare your spending with your bank statement to catch discrepancies or forgotten transactions.

Resolving an Overdraft: Funding Your Account

If you do find yourself with a negative balance, prompt action is critical to avoid additional fees or further issues:

- Immediate Deposit: The quickest way to resolve an overdraft is to deposit funds into your checking account. This could be a direct deposit, a mobile check deposit, an ATM deposit, or a transfer from another account (if available and not already linked for protection).

- Know Your Bank’s Cut-off Times: Understand when Chase processes transactions and when deposits need to be made to count for the current business day. Making a deposit before the cut-off can often prevent additional fees or even waive the initial one, especially with programs like Overdraft Assist℠.

- Avoid Further Spending: Refrain from making any new transactions until your account balance is positive and stable. Each new transaction while overdrawn could potentially trigger another fee.

Communicating with Chase: When and How to Get Help

Sometimes, despite your best efforts, an overdraft occurs. Don’t hesitate to contact Chase directly:

- Call Customer Service: Explain your situation. Especially if it’s your first overdraft or an unusual occurrence, the bank may be willing to waive a fee as a goodwill gesture. Be polite, explain what happened, and assure them you are taking steps to prevent it from happening again.

- Visit a Branch: For more complex issues or if you prefer face-to-face interaction, visiting a local Chase branch can be helpful. A banker can review your account, explain your options, and potentially assist with fee waivers.

- Understand Your Options: Don’t just accept the fee. Ask about Overdraft Assist℠, setting up linked accounts, or any other programs that might help you avoid future incidents.

Strategies to Avoid Overdrafts and Manage Your Finances Proactively

The best way to handle an overdraft is to avoid it entirely. Proactive financial planning and diligent account management are your strongest defenses.

Budgeting and Cash Flow Management

A solid budget is the foundation of preventing overdrafts.

- Track Your Income and Expenses: Know exactly how much money comes in and goes out each month. Categorize your spending to identify areas where you can cut back.

- Create a Buffer: Aim to always have a buffer of at least a few hundred dollars in your checking account, separate from your bill money. This acts as a mini-emergency fund for unexpected small expenses or timing issues.

- Regularly Reconcile Your Account: Compare your own records of spending with your bank statements to ensure accuracy and catch any discrepancies.

Setting Up Account Alerts and Notifications

Leverage technology to your advantage:

- Low Balance Alerts: Configure alerts to notify you when your checking account balance drops below a certain threshold (e.g., $100 or $200).

- Large Transaction Alerts: Get notified for any single transaction exceeding a specific amount.

- Daily Balance Updates: Some banks offer daily email or text summaries of your account balance.

- Transaction Alerts: Receive a notification every time a transaction posts to your account.

Utilizing Financial Tools and Apps for Real-time Tracking

Beyond your bank’s app, consider third-party budgeting and money management tools:

- Budgeting Apps (e.g., Mint, YNAB, Personal Capital): These apps can link to your bank accounts and credit cards, providing a holistic view of your finances in real-time. They help you track spending, set budgets, and monitor cash flow.

- Spreadsheets: For a more hands-on approach, a simple spreadsheet can be highly effective for tracking income and expenses.

- Virtual Envelopes: Some apps or personal systems allow you to allocate funds digitally to different spending categories, making it easier to see how much you have for each purpose.

Building an Emergency Fund

While often thought of for larger financial crises, a small emergency fund can also prevent overdrafts. If an unexpected bill or expense arises, you can tap into this fund rather than overdrawing your primary checking account. Even a few hundred dollars can make a significant difference in preventing fee accumulation.

The Broader Financial Health Perspective

Understanding how to navigate an overdraft is a crucial part of financial literacy. However, the ultimate goal should be to build a financial system that makes overdrafts a rare, if not entirely absent, event. This contributes to overall financial well-being and reduces unnecessary stress and costs.

Impact on Credit Scores (Indirectly)

As mentioned, overdrafts typically don’t directly impact your credit score. However, if an overdrawn account is closed by the bank and sent to a collections agency, that collection account will appear on your credit report and negatively affect your score. This indirect impact underscores the importance of resolving overdrafts quickly and maintaining good standing with your bank.

The Cost of Convenience: Weighing Overdraft Fees

Overdraft fees are a significant revenue source for banks, but they represent a high cost for consumers. A $34 fee on a $5 transaction represents an exorbitant annual percentage rate if viewed as a short-term loan. While overdraft protection can offer a safety net, relying on it too frequently can be an expensive habit. It’s essential to weigh the convenience of a covered transaction against the substantial cost of the fee.

Cultivating Responsible Banking Habits

Ultimately, preventing overdrafts is about cultivating responsible banking habits. This includes regularly checking your balances, understanding your bank’s policies, proactively setting up alerts and protections, and adhering to a realistic budget. By taking control of your financial habits, you can transform the potential stress of an overdraft into a rare occurrence, leading to greater financial stability and peace of mind.

In conclusion, while the mechanism of “how to overdraft Chase” is relatively straightforward – spending more than you have available – the more valuable knowledge lies in understanding the consequences, utilizing the bank’s protective measures, and implementing robust personal finance strategies to avoid such situations entirely. Responsible banking is about empowerment, and that begins with informed decision-making.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.