The dream of entrepreneurship is a powerful one, often fueled by a desire for independence, innovation, and the pursuit of a passion. However, transforming an idea into a thriving business requires more than just enthusiasm; it demands meticulous planning, strategic decision-making, and, most critically, a robust understanding and management of finances. Opening your own company is fundamentally a financial endeavor, intertwining capital, costs, cash flow, and compliance at every stage. This guide will walk you through the essential financial considerations and steps to establish your venture on a solid economic footing.

Laying the Financial Foundation: Pre-Launch Essentials

Before you even register your business, the groundwork you lay in financial planning will dictate your company’s viability and future trajectory. This initial phase is where abstract ideas meet concrete numbers.

Business Plan & Financial Projections

A comprehensive business plan is your company’s blueprint, and its financial section is the most critical component. This isn’t just a document for investors; it’s a roadmap for you. It should detail your startup costs, projected revenue and expenses for at least the first three to five years, break-even analysis, and cash flow forecasts.

- Startup Costs: A detailed list of every initial expense required to get your business off the ground.

- Operating Costs: An estimation of recurring monthly expenses (rent, utilities, salaries, marketing, supplies).

- Revenue Projections: Realistic forecasts of how much money your business expects to generate, broken down by product, service, or customer segment.

- Break-Even Analysis: The point at which your total revenue equals your total costs, signifying when your business starts to become profitable.

- Cash Flow Forecast: A projection of the money expected to come in and go out, crucial for managing liquidity.

These projections not only help you understand the financial demands of your venture but also serve as a benchmark against which you can measure actual performance, making adjustments as needed.

Understanding Startup Costs

Every new business incurs expenses before generating revenue. Identifying and quantifying these startup costs accurately is paramount. They fall into several categories:

- Legal & Administrative: Business registration fees, licenses, permits, legal consultation for contracts, accounting setup.

- Equipment & Inventory: Purchases of machinery, tools, computers, office furniture, initial stock of products, raw materials.

- Technology & Software: Website development, essential software subscriptions (CRM, accounting, project management), hardware.

- Marketing & Branding (Initial Phase): Logo design, initial website content, basic advertising, public relations.

- Premises: Security deposits, initial rent, renovation costs if applicable.

- Working Capital: A reserve fund to cover initial operating expenses before your revenue streams become consistent. This often overlooked cost can be the difference between survival and failure in the early months.

Failing to account for all startup costs can lead to undercapitalization, forcing you to seek additional funding under pressure or even close shop prematurely.

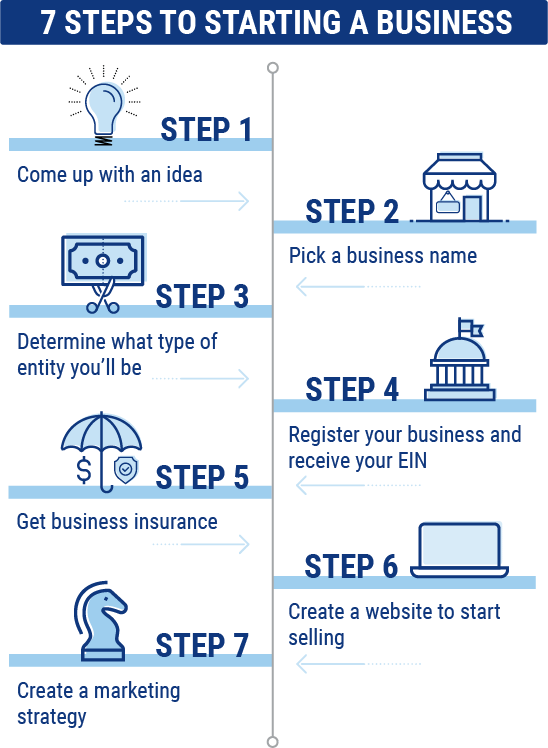

Choosing the Right Legal Structure

The legal structure you select for your company has significant financial and tax implications. It affects your personal liability, how profits are taxed, and the administrative burden you’ll face.

- Sole Proprietorship: Simple to set up, but offers no personal liability protection; your personal and business assets are indistinguishable. Taxes are pass-through.

- Partnership: Similar to sole proprietorships but with multiple owners. Shared liability and profits, pass-through taxation. Requires a robust partnership agreement.

- Limited Liability Company (LLC): Offers personal liability protection (separates personal from business assets) while providing flexible tax treatment (can be taxed as a sole proprietorship, partnership, or corporation). This is a popular choice for many small businesses.

- Corporation (S-Corp or C-Corp): Provides the strongest liability protection. C-Corps are subject to “double taxation” (corporate profits are taxed, and then dividends paid to shareholders are taxed again). S-Corps avoid double taxation by passing profits and losses directly to the owners’ personal income without being subject to corporate tax rates. Corporations are more complex to establish and maintain, with more stringent regulatory requirements.

Consulting with an attorney and an accountant is highly recommended to determine the most advantageous structure for your specific business goals and financial situation.

Securing Capital: Funding Your Vision

Once you’ve mapped out your financial needs, the next critical step is to secure the capital required to launch and sustain your company. Various funding avenues exist, each with its own advantages, disadvantages, and implications for your ownership and control.

Self-Funding & Bootstrapping

Many entrepreneurs start by funding their businesses themselves, using personal savings, credit cards, or loans from family and friends. This approach, known as bootstrapping, allows you to maintain full ownership and control without incurring debt interest or giving up equity to outside investors.

- Pros: Full control, no debt obligations (initially), high motivation to succeed.

- Cons: Limited capital can restrict growth, higher personal financial risk, potential strain on personal relationships.

- Strategy: Focus on generating revenue quickly, minimize expenses, and reinvest profits back into the business.

Debt Financing Options

Debt financing involves borrowing money that must be repaid, typically with interest, over a set period.

- Traditional Bank Loans: Banks offer various business loans, including term loans, lines of credit, and Small Business Administration (SBA) loans. Eligibility often depends on a solid business plan, good personal credit, collateral, and sometimes even existing revenue.

- Microloans: Smaller loans (typically under $50,000) offered by non-profit organizations or credit unions, often to underserved entrepreneurs.

- Equipment Financing: Loans specifically for purchasing business equipment, where the equipment itself serves as collateral.

- Invoice Factoring: Selling your unpaid invoices to a third party at a discount to get immediate cash.

Debt financing allows you to retain full ownership, but it comes with fixed repayment obligations that can be challenging during lean periods.

Equity Financing: Attracting Investors

Equity financing involves selling a portion of your company’s ownership (equity) to investors in exchange for capital. This can provide substantial funding without the burden of repayment, but it means giving up a share of future profits and decision-making power.

- Angel Investors: High-net-worth individuals who invest their personal capital in early-stage startups, often providing mentorship alongside funding.

- Venture Capital (VC) Firms: Professional investment firms that fund high-growth potential companies, typically in exchange for significant equity stakes and board representation. VCs usually seek a substantial return on investment.

- Crowdfunding: Raising small amounts of capital from a large number of people, often through online platforms. Equity crowdfunding allows individuals to invest in exchange for a stake in the company.

Equity financing can accelerate growth, but it requires a compelling pitch, a strong team, and a willingness to share ownership and control.

Grants & Government Programs

Various government agencies and private foundations offer grants to businesses that meet specific criteria, often related to innovation, social impact, or particular industries (e.g., R&D, environmental solutions, women-owned businesses).

- Pros: Non-dilutive funding (no equity given up, no repayment required).

- Cons: Highly competitive, strict eligibility criteria, extensive application process.

Searching for grants requires diligent research and a thorough understanding of the requirements.

Managing Your Company’s Finances: Post-Launch Strategies

Securing funds is just the beginning. Effective financial management is an ongoing process crucial for sustainability and growth once your company is operational.

Setting Up Business Banking & Accounting Systems

Separating personal and business finances from day one is non-negotiable.

- Business Bank Account: Open dedicated checking and savings accounts for your company. This simplifies tracking income and expenses, makes tax preparation easier, and projects professionalism.

- Accounting Software: Implement reliable accounting software (e.g., QuickBooks, Xero, FreshBooks) from the outset. This automates bookkeeping, facilitates invoicing, tracks expenses, manages payroll, and generates essential financial reports (profit & loss statements, balance sheets, cash flow statements). Good record-keeping is vital for decision-making and compliance.

Budgeting and Cash Flow Management

A well-constructed budget serves as a financial roadmap, allocating resources and setting spending limits. Regular monitoring against this budget helps identify overspending and areas for cost reduction.

- Cash Flow is King: Understand that profit does not equal cash. A profitable company can still fail if it runs out of cash. Implement robust cash flow forecasting to anticipate periods of surplus and deficit, allowing you to plan for working capital needs or investment opportunities.

- Expense Tracking: Diligently track every business expense. Not only is this crucial for accurate financial reporting, but it also maximizes tax deductions.

Understanding Taxes and Compliance

Navigating the tax landscape is complex and varies by legal structure, industry, and location.

- Federal, State, and Local Taxes: Be aware of your obligations regarding income tax, sales tax (if you sell goods or services), payroll taxes (if you have employees), and potentially excise taxes.

- Tax Deadlines: Missing tax deadlines can result in penalties and fines. Calendar all important tax dates.

- Professional Help: Engaging a qualified accountant or tax professional is invaluable. They can help you understand your obligations, identify eligible deductions, ensure compliance, and strategically plan for tax efficiency.

Pricing Strategies & Revenue Generation

How you price your products or services directly impacts your profitability and cash flow.

- Cost-Plus Pricing: Adding a markup percentage to your total costs.

- Value-Based Pricing: Pricing based on the perceived value to the customer, rather than just cost.

- Competitive Pricing: Setting prices based on what competitors charge.

- Revenue Streams: Diversifying your revenue streams can reduce risk and provide stability. Explore recurring revenue models, upsells, cross-sells, and new product/service offerings.

Protecting Your Financial Future: Risk Management & Growth

Even with sound financial management, unforeseen challenges can arise. Proactive risk management and a forward-looking approach to growth are essential.

Business Insurance Essentials

Insurance is a critical financial safeguard, protecting your company from various risks that could otherwise lead to devastating financial losses.

- General Liability Insurance: Covers claims of bodily injury or property damage caused by your business operations, products, or services.

- Professional Liability Insurance (E&O): For service-based businesses, protects against claims of negligence, errors, or omissions in your professional services.

- Property Insurance: Protects your physical assets (buildings, equipment, inventory) from damage or loss due to events like fire, theft, or vandalism.

- Workers’ Compensation Insurance: (If you have employees) Covers medical costs and lost wages for employees injured on the job.

- Cyber Liability Insurance: Becoming increasingly important, covers costs associated with data breaches and cyberattacks.

Consult with an insurance broker to assess your specific risks and tailor a comprehensive insurance plan.

Building an Emergency Fund

Just as individuals need personal emergency funds, businesses need cash reserves. An emergency fund can help your company weather unexpected downturns, sudden expenses, or periods of slow sales without having to take on high-interest debt or make drastic operational cuts. Aim to have at least three to six months of operating expenses saved in an easily accessible business savings account.

Financial Monitoring and Adaptation

The business landscape is dynamic. Your financial strategy should be too.

- Regular Review: Consistently review your financial statements, comparing actual performance against your projections. Identify trends, variances, and areas for improvement.

- Key Performance Indicators (KPIs): Track relevant financial KPIs (e.g., gross profit margin, net profit margin, customer acquisition cost, customer lifetime value) to gauge health and efficiency.

- Adaptability: Be prepared to adapt your financial strategies based on market shifts, economic conditions, and internal performance. This might involve adjusting pricing, cutting non-essential expenses, or exploring new funding rounds for expansion.

Opening your own company is an exhilarating journey, but its success hinges on a robust financial framework. By diligently planning, securing capital responsibly, managing finances meticulously, and proactively mitigating risks, you lay the groundwork for a resilient and prosperous enterprise. The path of entrepreneurship is challenging, yet with sound financial stewardship, it is profoundly rewarding.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.