In the dynamic world of entrepreneurship, securing adequate funding is often the critical linchpin that transforms a promising idea into a thriving enterprise, or propels an established business to new heights. While passion and innovation form the heart of any venture, capital is its lifeblood. From covering operational expenses and purchasing essential equipment to funding ambitious expansion plans and navigating unexpected challenges, a business loan can be the vital injection your company needs to grow and succeed.

However, the process of obtaining a business loan can seem daunting. With a multitude of lenders, loan types, and application requirements, it’s easy for business owners to feel overwhelmed. This comprehensive guide aims to demystify the journey, providing a clear, step-by-step roadmap to successfully securing the financing your business deserves. We will delve into understanding your needs, exploring various funding avenues, meticulously preparing your application, and strategically navigating the approval process, all designed to empower you with the knowledge and confidence to make informed financial decisions.

Understanding Your Business Loan Needs and Eligibility

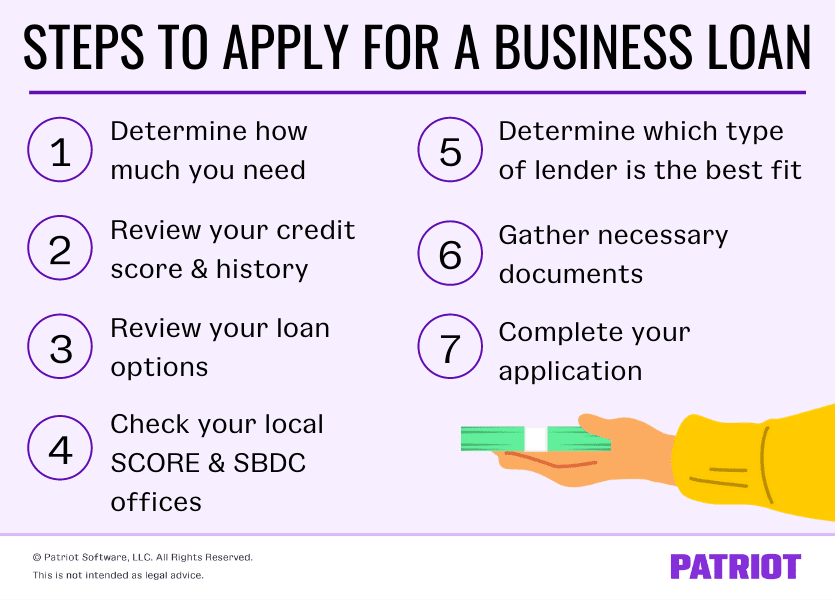

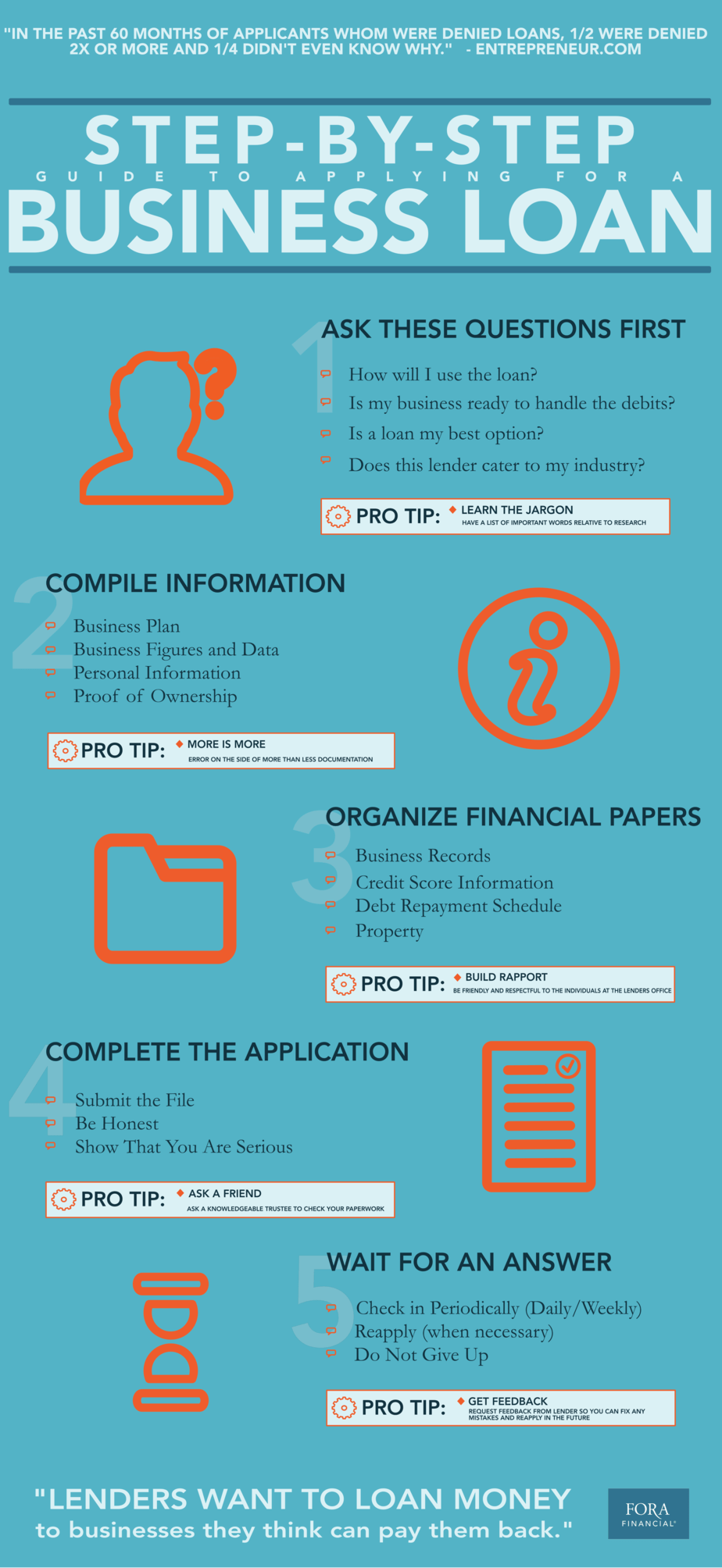

Before even considering approaching a lender, the first and most crucial step is to gain absolute clarity on your specific financial requirements and honestly assess your business’s eligibility. This foundational work will not only streamline your search but also significantly improve your chances of approval.

Defining Your Capital Requirements

What exactly do you need the money for? The purpose of the loan will largely dictate the type of financing you should pursue and the amount you require.

- Working Capital: To cover day-to-day operational expenses like payroll, rent, utilities, and inventory. This often involves shorter-term loans or lines of credit.

- Equipment Financing: For purchasing machinery, vehicles, technology, or other significant assets. These loans are typically secured by the equipment itself.

- Business Expansion: For opening new locations, increasing production capacity, or entering new markets. This often requires substantial capital and a robust business plan.

- Real Estate Acquisition: To purchase commercial property for your business. These are typically long-term, secured loans.

- Debt Refinancing: To consolidate existing debt into a single, more manageable loan with potentially better terms.

- Startup Costs: For new businesses getting off the ground. These are often harder to secure due to lack of operating history and require strong personal guarantees or collateral.

Clearly defining your need allows you to accurately determine the loan amount, avoiding both over-borrowing (which incurs unnecessary interest) and under-borrowing (which leaves you short).

Assessing Your Business’s Financial Health

Lenders are primarily concerned with your ability to repay the loan. They will scrutinize your business’s financial health through various metrics:

- Revenue and Profitability: Consistent and growing revenue, along with healthy profit margins, signals a strong business.

- Cash Flow: Positive and predictable cash flow demonstrates your ability to meet financial obligations.

- Debt-to-Income Ratio: A lower ratio indicates less existing debt and a greater capacity to take on more.

- Industry Stability and Growth: Lenders prefer businesses in stable or growing industries with a proven track record.

- Time in Business: Most traditional lenders prefer businesses that have been operational for at least two years, though online lenders might be more flexible.

Knowing Your Credit Score (Personal and Business)

Both your personal credit score and your business credit score play a pivotal role.

- Personal Credit Score: For small businesses, especially startups, your personal credit history (FICO score) is often a primary indicator of your financial responsibility. A score of 680 or higher is generally considered good, with 720+ being excellent. It’s crucial to check your credit report for errors and work to improve any negative marks.

- Business Credit Score: This is separate from your personal score and is built over time as your business obtains credit and makes timely payments. Agencies like Dun & Bradstreet, Experian Business, and Equifax Business provide these scores. A strong business credit profile can unlock better loan terms and higher loan amounts.

Crafting a Solid Business Plan

A well-researched, comprehensive business plan is not merely a formality; it’s a powerful tool that demonstrates your vision, strategy, and understanding of your market. It convinces lenders that you have a viable business model and a clear path to profitability and loan repayment. Key components include:

- Executive Summary: A concise overview of your business, mission, products/services, and growth strategy.

- Company Description: What your business does, its legal structure, and its unique selling proposition.

- Market Analysis: In-depth research on your target market, industry trends, competition, and how you differentiate yourself.

- Organization and Management: Your team’s experience and roles.

- Service or Product Line: Details about what you offer.

- Marketing and Sales Strategy: How you will reach customers and generate revenue.

- Financial Projections: Crucial for lenders, including income statements, balance sheets, cash flow projections for at least 3-5 years, and a clear explanation of how the loan will be used and repaid.

Exploring Different Types of Business Loans

The lending landscape is diverse, offering various financing solutions tailored to different business needs and profiles. Understanding these options is key to choosing the right fit.

Traditional Bank Loans

- Description: Offered by conventional banks (e.g., Chase, Wells Fargo, Bank of America). These are typically term loans with fixed interest rates and repayment schedules.

- Pros: Generally offer the lowest interest rates and most favorable terms; established relationships can be beneficial.

- Cons: Strict eligibility requirements; lengthy application and approval processes; often require collateral and strong credit history.

- Best For: Established businesses with strong financials, good credit, and significant collateral.

SBA Loans (Small Business Administration)

- Description: Government-backed loans, not direct loans from the SBA. The SBA guarantees a portion of the loan, reducing risk for lenders and making it easier for small businesses to qualify.

- Pros: Lower down payments, flexible overhead requirements, competitive interest rates, and longer repayment terms.

- Cons: Can still involve a lengthy application process due to both lender and SBA requirements; some restrictions on use of funds.

- Best For: Small businesses that might not qualify for conventional bank loans but still have a solid business plan and decent credit. Popular programs include 7(a) and 504 loans.

Online Lenders

- Description: A rapidly growing segment, online lenders (e.g., Kabbage, OnDeck, Fundbox) use technology to streamline applications and underwriting.

- Pros: Fast application and approval times (sometimes within hours or days); less stringent credit requirements than traditional banks; wider range of products.

- Cons: Often higher interest rates and fees; may offer shorter repayment terms.

- Best For: Businesses needing quick access to capital, those with less-than-perfect credit, or those with shorter operating histories.

Alternative Financing Options

Beyond the mainstream, several other financing options cater to specific situations:

- Lines of Credit: Provides access to a revolving credit line up to a certain limit, allowing businesses to draw and repay funds as needed. Ideal for managing cash flow fluctuations.

- Merchant Cash Advances (MCAs): Businesses receive a lump sum in exchange for a percentage of future credit card sales. Fast but extremely expensive; often seen as a last resort.

- Equipment Financing: Specific loans for purchasing new or used equipment, with the equipment serving as collateral.

- Invoice Factoring/Financing: Selling your unpaid invoices to a third party (a factor) at a discount for immediate cash. Good for businesses with long payment cycles.

- Crowdfunding: Raising small amounts of money from a large number of people, often through online platforms. Can be equity-based or rewards-based.

Preparing Your Loan Application Package

Once you’ve identified the right type of loan and a potential lender, the next phase involves meticulously preparing your application. A complete, organized, and compelling submission speaks volumes about your professionalism and readiness.

Gathering Essential Financial Documents

This is arguably the most critical step. Lenders require a comprehensive view of your financial history. Be prepared to provide:

- Business Bank Statements: Typically for the last 6-12 months.

- Business Tax Returns: For the past 2-3 years.

- Personal Tax Returns: For the past 2-3 years, especially for small businesses.

- Profit and Loss (P&L) Statements: Also known as Income Statements, showing revenue, costs, and profit over a period.

- Balance Sheets: Snapshot of your assets, liabilities, and equity at a specific point in time.

- Cash Flow Projections: Detailed forecasts of your expected cash inflows and outflows.

- Accounts Receivable and Payable Aging Reports: Showing who owes you money and who you owe.

- Personal Financial Statement: A summary of your personal assets and liabilities.

Developing a Compelling Loan Proposal

While a business plan is foundational, a loan proposal specifically highlights your financing needs and repayment strategy. It should include:

- A concise overview of your business and its track record.

- The exact amount of funding requested and its specific purpose.

- A clear, data-driven explanation of how the loan will generate revenue or save costs.

- Detailed projections demonstrating your ability to repay the loan on time.

- Information on any collateral offered.

Collateral and Guarantees

Many business loans, especially traditional ones, require collateral to secure the loan.

- Collateral: Assets pledged by the borrower to the lender as security for repayment (e.g., real estate, equipment, inventory, accounts receivable). If you default, the lender can seize these assets.

- Personal Guarantee: For small businesses, owners often must provide a personal guarantee, meaning they are personally responsible for repaying the loan if the business cannot. This is a significant commitment and should be understood thoroughly.

Legal and Business Registrations

Ensure all your business registrations and legal documents are in order and up-to-date. This includes:

- Business licenses and permits.

- Articles of incorporation or organization.

- EIN (Employer Identification Number).

- Any relevant industry-specific certifications.

Navigating the Application and Approval Process

With your application package ready, it’s time to engage with lenders and navigate the review process. This stage requires patience, clear communication, and a proactive approach.

Researching and Comparing Lenders

Do not limit yourself to just one lender. Research multiple options that fit your identified loan type and business profile.

- Compare interest rates, fees (origination fees, prepayment penalties), repayment terms, and collateral requirements.

- Read reviews and seek recommendations from other business owners.

- Consider both national banks, local credit unions, and specialized online lenders.

The Application Submission

Follow each lender’s specific application instructions carefully. Whether it’s an online portal or a paper application, ensure every field is filled accurately and completely. Attach all required documents in an organized manner. A complete application signals professionalism and saves time.

Underwriting and Due Diligence

After submission, the lender’s underwriting team will conduct a thorough review of your financials, credit history, business plan, and collateral.

- They may request additional documentation or clarification on specific items. Respond promptly and comprehensively.

- Be prepared for questions about your business operations, market strategy, and financial projections.

- Some lenders might conduct site visits or interviews.

Understanding Loan Terms and Conditions

If your application is approved, you will receive a loan offer outlining the terms. Carefully review:

- Interest Rate: Fixed or variable.

- APR (Annual Percentage Rate): The true cost of borrowing, including interest and fees.

- Repayment Schedule: Monthly, bi-weekly, or weekly payments, and the loan term.

- Fees: Origination fees, closing costs, administrative fees, late payment fees.

- Covenants: Conditions or restrictions imposed by the lender (e.g., maintaining certain financial ratios, not taking on additional debt without permission).

Do not hesitate to ask questions and clarify any terms you don’t fully understand before signing.

What to Do If Your Application is Denied

A denial is not the end of the road. It’s an opportunity to learn and improve.

- Request Feedback: Ask the lender why your application was denied. This feedback is invaluable.

- Address Weaknesses: Use the feedback to identify and address weaknesses in your financials, business plan, or credit score.

- Improve Credit: Work on improving both personal and business credit scores.

- Re-evaluate Needs: Perhaps the requested loan amount was too high, or the loan type was unsuitable.

- Seek Guidance: Consult with a financial advisor, SCORE mentor, or small business development center (SBDC) for help.

- Explore Alternatives: Consider other lenders or alternative financing options that might be a better fit.

Post-Approval and Responsible Borrowing

Receiving loan approval is a moment of triumph, but it also marks the beginning of a crucial phase: responsible management of your new capital. Your actions post-approval directly impact your financial health and future borrowing capacity.

Managing Your Loan Funds Wisely

Stick rigorously to the purpose outlined in your loan application.

- Budget Adherence: Use the funds exactly as planned in your business plan and loan proposal. Diverting funds for unrelated purposes can lead to financial strain and, in some cases, violate loan covenants.

- Track Expenditures: Keep meticulous records of how the loan money is spent. This is essential for financial reporting and for proving responsible use to your lender if required.

- Avoid Unnecessary Spending: Resist the temptation to use loan funds for non-essential items or extravagant purchases. Every dollar should contribute to your business’s growth and ability to repay the loan.

Maintaining Good Financial Practices

Your commitment to financial discipline doesn’t end after securing the loan; it deepens.

- Consistent Cash Flow Monitoring: Continuously track your cash inflows and outflows to ensure you always have enough liquidity to cover loan payments and operational costs.

- Regular Financial Reviews: Periodically review your profit and loss statements, balance sheets, and cash flow reports. This helps you identify trends, address potential issues early, and make informed business decisions.

- Stay Organized: Maintain accurate and up-to-date financial records. This makes future audits or applications for additional financing much smoother.

- Build Reserves: Where possible, aim to build a financial cushion to protect your business against unexpected downturns or emergencies, which can impact your ability to repay the loan.

Building a Strong Relationship with Your Lender

Your lender is a partner in your business’s financial journey. Nurturing a positive relationship can yield significant long-term benefits.

- Open Communication: If you anticipate any difficulty in making a payment or foresee a change in your business that might affect your repayment ability, communicate proactively with your lender. They are often more willing to work with you if they are informed in advance, potentially offering temporary adjustments or solutions.

- Transparency: Be transparent about your business’s performance, both good and bad. Lenders appreciate honesty and trust.

- Timely Payments: Consistently making payments on time is the single most important factor in building trust and a positive credit history. It enhances your creditworthiness for future financing needs.

- Provide Updates: Share positive business updates or achievements with your lender. Keeping them informed about your success reinforces their confidence in your business.

A strong relationship with your initial lender can pave the way for easier access to future financing, whether it’s a larger loan, a line of credit, or other financial products, often on more favorable terms.

Conclusion

Obtaining a business loan is a journey that demands thorough preparation, strategic decision-making, and unwavering financial diligence. It’s not merely about filling out forms; it’s about presenting a compelling narrative of your business’s potential, backed by solid financial data and a clear repayment strategy.

By meticulously defining your capital needs, understanding the diverse landscape of lending options, diligently preparing your application with all necessary documentation, and proactively navigating the approval process, you significantly enhance your chances of success. And once funded, responsible management of the capital and fostering a strong relationship with your lender are paramount for your business’s sustained growth and future financial health.

Approach the process with a professional mindset, embrace the learning opportunities, and remember that securing the right business loan is a strategic move that can unlock new possibilities, fuel expansion, and solidify your company’s foundation for years to come.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.