In an increasingly complex and interconnected world, the ability to manage one’s money effectively is not merely a desirable skill but a fundamental pillar of personal well-being and long-term security. From daily expenditures to ambitious retirement plans, every financial decision we make shapes our future. Yet, for many, the concept of “managing money better” can feel overwhelming, shrouded in jargon and perceived complexity. The good news is that mastering personal finance is an attainable goal for everyone, regardless of their current financial standing. It requires a combination of disciplined habits, strategic planning, and a willingness to learn and adapt.

This comprehensive guide aims to demystify the process, providing actionable insights and a structured approach to transforming your financial life. We will delve into core principles, explore practical strategies, and illuminate the mindset required to navigate the financial landscape with confidence and achieve your monetary aspirations.

Building a Solid Financial Foundation

The journey to better money management begins with understanding your current situation and laying down a robust framework. Without a clear picture of where you stand, any attempt to move forward will be based on assumptions, leading to ineffective strategies and potential frustration.

Understanding Your Current Financial Landscape

Before you can chart a new course, you must know your starting point. This involves a thorough, honest assessment of your income, expenses, and existing debts.

- Income Assessment: Accurately tally all your sources of income. This includes your primary salary, freelance earnings, rental income, dividends, or any other regular inflow of money. Understanding your net (after-tax) income is crucial, as this is the actual money you have available to work with.

- Expense Tracking: This is often the most revealing step. For a month or two, meticulously track every single dollar you spend. Categorize these expenses into essentials (rent, groceries, utilities, transportation) and non-essentials (dining out, entertainment, subscriptions, impulse purchases). Many people are surprised to discover where their money truly goes. This exercise isn’t about judgment; it’s about gaining clarity.

- Debt Inventory: List all your outstanding debts, including credit card balances, personal loans, student loans, car loans, and mortgages. For each, note the outstanding balance, interest rate, and minimum monthly payment. High-interest debts, especially, can severely impede your financial progress if not addressed strategically.

This initial audit provides the data necessary to make informed decisions and reveals areas for potential improvement, setting the stage for more effective management.

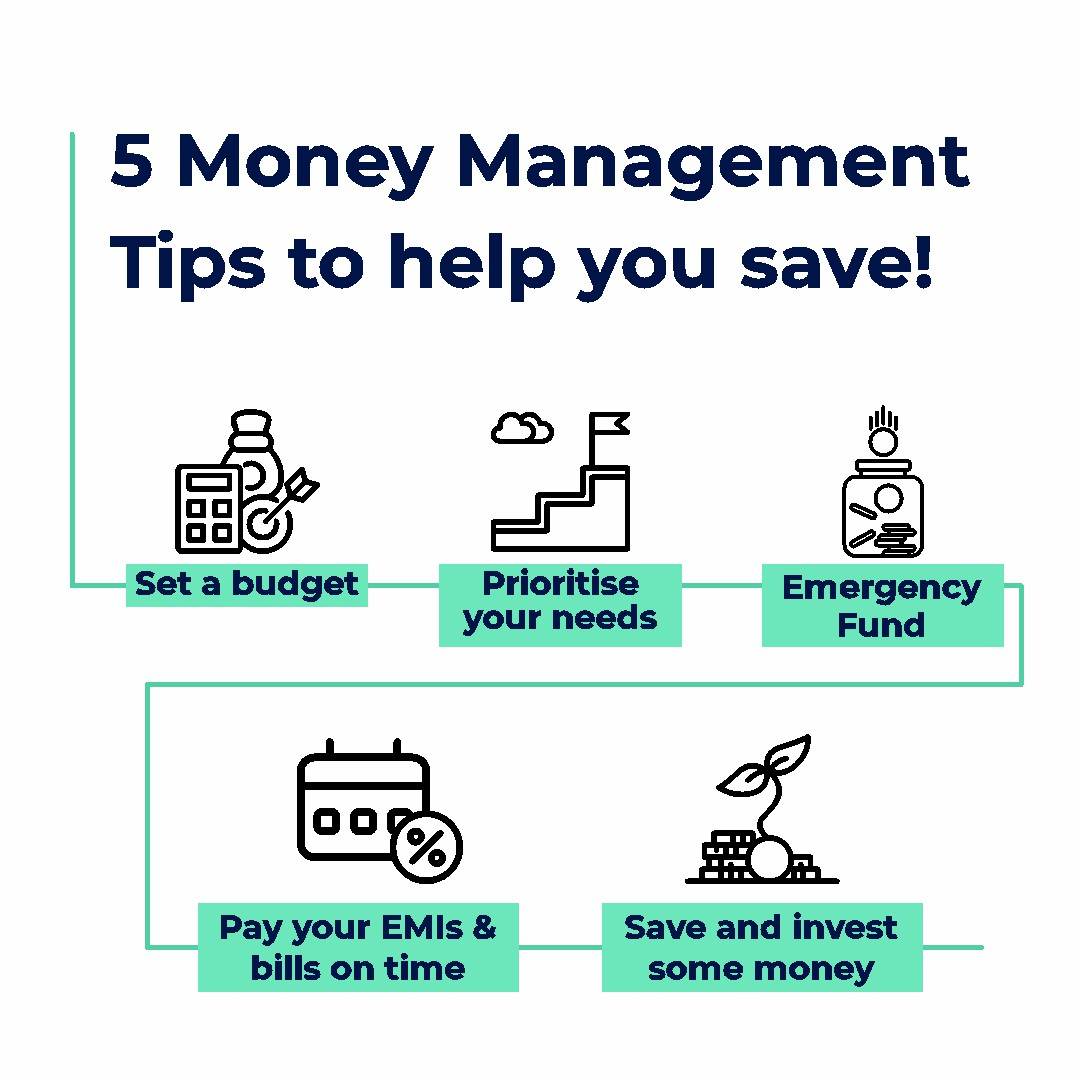

Creating a Realistic Budget That Works For You

Budgeting is not about deprivation; it’s about empowerment. It’s a strategic plan for how you allocate your money, ensuring your spending aligns with your values and goals. A good budget is realistic, flexible, and sustainable.

- Choose a Method: There are various budgeting methods. The 50/30/20 rule suggests allocating 50% of your income to needs, 30% to wants, and 20% to savings and debt repayment. The zero-based budget assigns every dollar a “job” until no money is left unaccounted for. The envelope system is a tactile approach using physical cash for different categories. Choose the method that resonates with your personality and lifestyle.

- Automate Where Possible: Set up automatic transfers from your checking account to savings or investment accounts immediately after payday. This “pay yourself first” strategy ensures you prioritize your financial goals before discretionary spending.

- Regular Review and Adjustment: A budget is a living document, not a static one. Life changes, and so should your budget. Review it monthly or quarterly, making adjustments as needed. Did you overspend in one category? Did you receive a raise? Adapt your budget accordingly.

A well-crafted budget serves as your financial roadmap, guiding your spending and helping you stay on track toward your objectives.

Establishing an Emergency Fund (The Non-Negotiable Buffer)

One of the most critical components of financial stability is an emergency fund. This is a separate savings account, easily accessible, designed to cover unexpected expenses without forcing you into debt.

- Why It’s Essential: Life is unpredictable. Car repairs, medical emergencies, job loss, or sudden home repairs can quickly derail your finances. An emergency fund acts as a financial safety net, providing peace of mind and preventing you from accumulating high-interest debt during crises.

- How Much to Save: The general recommendation is to save at least three to six months’ worth of essential living expenses. For those with unstable income or high dependents, aiming for nine to twelve months might be prudent.

- Where to Keep It: Your emergency fund should be held in a high-yield savings account separate from your primary checking account. This keeps it accessible but out of sight, reducing the temptation to dip into it for non-emergencies. Avoid investing it in volatile assets, as the primary goal is liquidity and safety, not high returns.

Building an emergency fund is a foundational step that provides a sense of security and resilience, enabling you to weather unexpected storms without compromising your long-term financial health.

Strategic Debt Management and Elimination

Debt, especially high-interest debt, can be a significant obstacle to achieving financial freedom. While some debt, like a mortgage, can be a valuable asset, consumer debt often acts as a financial drain. Managing and eliminating debt strategically is crucial for improving your financial standing.

Prioritizing High-Interest Debts

Not all debt is created equal. High-interest debts, such as credit card balances or some personal loans, are the most urgent to address due to the rapid accumulation of interest charges.

- Understanding Interest Rates: The higher the interest rate, the more expensive the debt is over time. Focusing on these first minimizes the total amount you pay back.

- Debt Snowball vs. Debt Avalanche:

- Debt Avalanche Method: This strategy involves paying off debts with the highest interest rates first, while making minimum payments on all other debts. Once the highest-interest debt is cleared, you roll that payment amount into the next highest-interest debt. This method saves you the most money on interest over the long run.

- Debt Snowball Method: This approach focuses on paying off the smallest debt balance first, regardless of the interest rate, while making minimum payments on others. Once the smallest debt is paid off, you take the money you were paying on that debt and add it to the payment of the next smallest debt. This method provides psychological wins, helping you stay motivated.

Choose the method that best aligns with your personality and financial discipline.

Strategies for Reducing and Consolidating Debt

Beyond prioritization, several strategies can help accelerate your debt repayment.

- Negotiate Interest Rates: Contact your credit card companies or lenders to inquire about lower interest rates. If you have a good payment history, they might be willing to reduce your rate, saving you money.

- Debt Consolidation: For multiple high-interest debts, consider consolidating them into a single loan with a lower interest rate. Options include a personal loan, a balance transfer credit card (with a 0% introductory APR), or a home equity loan (be cautious, as this puts your home at risk if you default).

- Increase Payments: Even a small additional payment each month can significantly reduce the total interest paid and the time it takes to become debt-free. Review your budget for areas where you can cut back and redirect those funds to debt repayment.

- Avoid Minimum Payments: Paying only the minimum on credit cards can keep you in debt for decades, costing you thousands in interest. Aim to pay as much as you possibly can above the minimum.

Avoiding New Debt: Cultivating Mindful Spending Habits

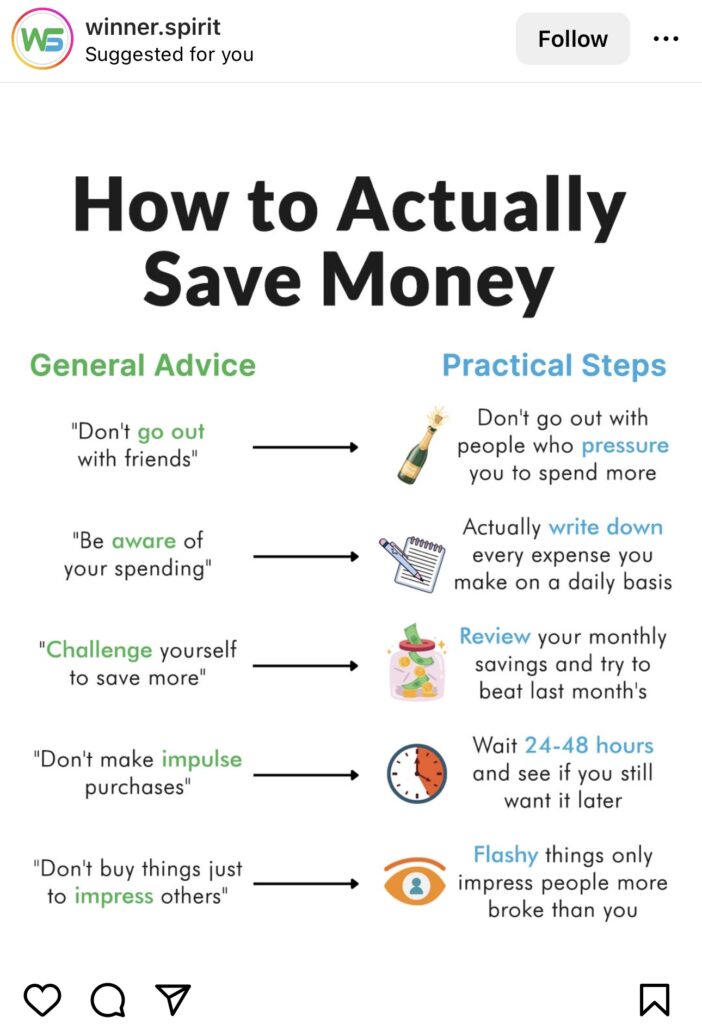

The best way to manage debt is to prevent accumulating new debt. This requires a shift in mindset and cultivating mindful spending habits.

- Distinguish Needs from Wants: Before making a purchase, pause and consider if it’s truly a need or a want. If it’s a want, ask yourself if it aligns with your financial goals.

- Use Cash or Debit: If credit card spending is an issue, switch to using cash or a debit card for everyday purchases. This provides a tangible limit to your spending.

- Implement a Waiting Period: For larger “want” purchases, impose a 24-48 hour waiting period. Often, the urge to buy passes, or you realize the item isn’t as essential as you initially thought.

- Understand Your Triggers: Identify what prompts you to overspend – stress, boredom, social pressure, online sales. Once you recognize your triggers, you can develop healthier coping mechanisms.

By actively working to eliminate existing debt and adopting habits that prevent new debt, you pave the way for true financial liberation and create more room in your budget for savings and investments.

Smart Saving and Investing for Future Growth

Once you have a handle on your spending and are actively managing debt, the next crucial step is to strategically save and invest your money. This is where your money starts working for you, building wealth and securing your long-term financial future.

Setting Clear Financial Goals

Effective saving and investing begin with defining what you’re saving and investing for. Goals provide motivation and direction.

- Short-term Goals (1-3 years): Examples include saving for a down payment on a car, a significant vacation, or replacing an aging appliance. These usually require highly liquid and low-risk savings accounts.

- Mid-term Goals (3-10 years): This might involve a down payment on a home, funding a child’s education, or starting a small business. These might benefit from a mix of savings and more conservative investments.

- Long-term Goals (10+ years): Retirement planning is the quintessential long-term goal, along with potentially leaving an inheritance or achieving financial independence. These goals often require a more aggressive investment strategy, leveraging the power of time.

Make your goals SMART: Specific, Measurable, Achievable, Relevant, and Time-bound. This makes them more concrete and easier to track.

Automating Your Savings and Investments

Consistency is key in saving and investing. Automating transfers ensures you consistently contribute to your financial goals without relying on willpower alone.

- “Pay Yourself First”: Set up automatic transfers from your checking account to your savings, investment, or retirement accounts on payday. Treat these transfers like any other bill – non-negotiable.

- Direct Deposit Allocation: Many employers allow you to split your direct deposit, sending a portion directly to a savings or investment account. This makes saving truly effortless.

- Increasing Contributions Over Time: As your income grows, or as you eliminate debts, incrementally increase your automated savings and investment contributions. Even a small annual increase can have a significant impact over decades.

Exploring Diverse Investment Avenues

Investing doesn’t have to be complicated, but understanding your options and choosing those that align with your risk tolerance and goals is essential.

- Retirement Accounts: Maximize contributions to tax-advantaged accounts like 401(k)s (especially if your employer offers a match – it’s free money!), IRAs (Traditional or Roth), or other pension plans. These accounts offer significant tax benefits and are designed for long-term growth.

- Stocks: Represent ownership in companies. They offer potential for high returns but also come with higher risk and volatility. Diversification through ETFs (Exchange-Traded Funds) and Mutual Funds is generally recommended for beginners, as these pool money from many investors to buy a diversified portfolio of stocks (and/or bonds).

- Bonds: Essentially loans to governments or corporations. They are generally less volatile than stocks and provide more predictable income (interest payments), making them a good option for diversification and lower-risk portfolios.

- Real Estate: Can include purchasing a primary residence, rental properties, or investing in Real Estate Investment Trusts (REITs). Offers potential for appreciation and rental income but often requires significant capital and can be illiquid.

- Diversification is Key: Don’t put all your eggs in one basket. A well-diversified portfolio spreads risk across different asset classes, industries, and geographies, reducing the impact of poor performance in any single area.

The Power of Compound Interest: Starting Early

Compound interest is often called the “eighth wonder of the world” for a reason. It’s the interest you earn on your initial investment plus the accumulated interest from previous periods.

- Time is Your Greatest Ally: The longer your money is invested, the more time it has to compound, leading to exponential growth. Starting early, even with small amounts, can outperform larger contributions made later in life.

- Illustrative Example: Investing $100 per month from age 25 to 65 at an average 7% annual return could yield over $250,000. Waiting until age 35 for the same contribution and return would yield significantly less.

By consistently saving, intelligently investing, and leveraging the power of compounding, you can build substantial wealth over time and achieve even your most ambitious financial aspirations.

Leveraging Financial Tools and Technology

In the digital age, managing money better has been significantly simplified and empowered by a plethora of financial tools and technology. These resources can help you track spending, automate savings, and even manage your investments with greater efficiency and insight.

Budgeting Apps and Software for Seamless Tracking

Gone are the days of manual ledger entries. Modern budgeting apps provide real-time insights into your financial health.

- Automated Transaction Categorization: Many apps link directly to your bank accounts and credit cards, automatically importing and categorizing your transactions. This eliminates manual data entry and provides an accurate overview of your spending.

- Customizable Budgets and Alerts: Create custom budget categories, set spending limits, and receive alerts when you’re approaching or exceeding those limits. This proactive approach helps you stay within your financial boundaries.

- Net Worth Tracking: Some advanced apps allow you to track your overall net worth by integrating all your assets (bank accounts, investments, property) and liabilities (debts).

- Popular Options: Apps like Mint, YNAB (You Need A Budget), Personal Capital, and PocketGuard offer different features and approaches to suit various user preferences, from simple expense tracking to comprehensive financial planning.

Robo-Advisors for Automated Investing

For those new to investing or who prefer a hands-off approach, robo-advisors offer an accessible and cost-effective solution.

- Algorithm-Driven Portfolios: Robo-advisors use algorithms to build and manage diversified investment portfolios tailored to your financial goals, risk tolerance, and time horizon.

- Low Fees: They typically charge significantly lower management fees compared to traditional human financial advisors, making investing more accessible for smaller portfolios.

- Automatic Rebalancing: These platforms automatically rebalance your portfolio to maintain your desired asset allocation, ensuring it stays aligned with your long-term strategy.

- Fractional Shares: Many robo-advisors allow you to invest in fractional shares, meaning you can invest any dollar amount without needing to buy a full share, making it easier to start with less capital.

- Examples: Betterment, Wealthfront, and Vanguard Digital Advisor are popular robo-advisor platforms.

Online Banking Features for Better Control

Your bank’s online portal and mobile app are powerful tools for day-to-day money management.

- Real-time Account Monitoring: Instantly check balances, review transaction history, and monitor for any suspicious activity.

- Bill Pay and Transfers: Schedule recurring bill payments and set up automatic transfers between your accounts or to external accounts.

- Budgeting Tools (Bank-Specific): Many banks now offer their own basic budgeting tools, categorization features, and spending insights directly within their platforms.

- Alerts and Notifications: Set up alerts for low balances, large transactions, or when bills are due, helping you stay on top of your finances.

Protecting Your Digital Financial Footprint

While technology offers convenience, it also necessitates vigilance in protecting your financial information.

- Strong, Unique Passwords: Use complex passwords for all financial accounts and enable two-factor authentication (2FA) wherever possible.

- Beware of Phishing: Be wary of suspicious emails or messages asking for personal financial information. Always verify the sender and never click on dubious links.

- Secure Networks: Avoid accessing financial accounts on public Wi-Fi networks, which can be vulnerable to security breaches.

- Regular Software Updates: Keep your operating system, browser, and security software updated to protect against the latest threats.

- Monitor Statements: Regularly review your bank and credit card statements for any unauthorized transactions.

By embracing and intelligently using financial tools and technology, you can streamline your money management processes, gain deeper insights into your financial behavior, and ultimately make more informed decisions to reach your goals faster.

Cultivating a Mindset for Lasting Financial Wellness

Managing money better isn’t just about numbers and spreadsheets; it’s profoundly influenced by your mindset, habits, and willingness to learn. Achieving lasting financial wellness requires more than just following a set of rules; it demands an ongoing commitment to personal growth and adaptation.

Continuous Learning and Financial Literacy

The financial world is constantly evolving, with new products, regulations, and investment opportunities emerging regularly. A commitment to continuous learning is crucial for staying informed and making sound decisions.

- Read Books and Blogs: There’s a wealth of information available from renowned financial experts. Dedicate time to reading books on personal finance, investing, and wealth building. Follow reputable financial blogs and news sources.

- Listen to Podcasts: Financial podcasts offer an engaging way to learn about various money topics while commuting or exercising.

- Attend Webinars/Workshops: Many financial institutions and educational platforms offer free webinars and workshops on budgeting, investing, retirement planning, and more.

- Understand Economic Trends: While you don’t need to be an economist, having a basic understanding of inflation, interest rates, and market cycles can help you make better financial decisions.

Seeking Professional Financial Advice When Needed

While self-education is powerful, there are times when professional guidance is invaluable.

- Complex Situations: If you have significant assets, a complex estate, or are facing major life changes (marriage, divorce, inheritance, starting a business), a financial advisor can provide tailored strategies.

- Investment Guidance: For those who feel overwhelmed by investment choices or want a more personalized investment strategy, a certified financial planner (CFP) can be an excellent resource.

- Accountability and Perspective: An advisor can also provide an objective perspective, help you stay accountable to your goals, and guide you through challenging market conditions.

- Choosing an Advisor: Look for fee-only fiduciaries who are legally obligated to act in your best interest and transparently disclose their fees.

Regular Financial Reviews and Adjustments

Your financial plan is not a “set it and forget it” endeavor. Regular reviews are essential to ensure it remains relevant and effective.

- Monthly Budget Review: Revisit your budget at least once a month. Compare actual spending to planned spending, identify discrepancies, and make minor adjustments.

- Quarterly/Annual Financial Check-up: Schedule a more comprehensive review a few times a year. Assess your progress towards short-term and mid-term goals, check your emergency fund balance, review your investment performance, and re-evaluate your debt repayment strategy.

- Major Life Event Adjustments: Any significant life event – a new job, marriage, birth of a child, home purchase, health issue – should trigger an immediate review and potential overhaul of your financial plan.

The Psychological Aspect of Money Management

Finally, recognizing and managing the psychological elements of money is crucial for long-term success.

- Emotional Spending: Understand how emotions (stress, boredom, excitement) influence your spending habits and develop strategies to counteract impulsive purchases.

- Delayed Gratification: Cultivate the ability to forgo immediate pleasure for greater future rewards. This is fundamental to saving and investing.

- Overcoming Financial Shame: Many people feel shame or guilt about past financial mistakes. Acknowledge them as learning experiences and focus on moving forward positively.

- Celebrating Small Wins: Acknowledge and celebrate progress, no matter how small. Paying off a credit card, reaching a savings milestone, or sticking to your budget for a month can boost morale and reinforce positive habits.

By nurturing a mindset of continuous learning, seeking expert advice when necessary, regularly reviewing your progress, and understanding the psychological interplay with money, you build a resilient framework for sustained financial wellness and ultimately achieve a life of greater financial freedom and peace of mind. Managing money better is a journey, not a destination, and with dedication, anyone can master its intricacies.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.