Navigating the landscape of tax obligations can often feel complex, but understanding how to properly make payments to the Internal Revenue Service (IRS) is a fundamental aspect of sound personal and business finance. Far from being a mere procedural step, efficient and accurate tax payment is crucial for maintaining financial health, avoiding penalties, and contributing to the economic infrastructure. This comprehensive guide will demystify the process, offering practical insights and strategies to ensure your tax responsibilities are met seamlessly, securely, and effectively. Whether you’re an individual taxpayer, a small business owner, or managing complex financial portfolios, mastering IRS payment methods is an indispensable skill in your financial toolkit.

Understanding Your IRS Payment Responsibilities

Before delving into the ‘how,’ it’s essential to grasp the ‘why’ and ‘what’ of your tax obligations. The U.S. tax system operates on a “pay-as-you-go” basis, meaning taxpayers are expected to pay most of their tax liability throughout the year, rather than a lump sum at the annual tax deadline. This principle underpins the various payment requirements for different taxpayer types.

Who Needs to Pay and Why?

Virtually every working individual and profitable business in the United States is subject to federal taxes.

- Individuals: Most employees have taxes withheld from their paychecks by their employers, which are then remitted to the IRS. However, if you have significant income from other sources (e.g., investments, side gigs, retirement distributions), or if your withholding isn’t sufficient, you might need to make additional payments.

- Self-Employed Individuals: If you’re self-employed, a freelancer, or an independent contractor, you are responsible for paying both income tax and self-employment taxes (Social Security and Medicare) directly to the IRS. Since no employer withholds taxes for you, these payments are typically made quarterly as estimated taxes.

- Businesses: Corporations, partnerships, and other business entities have their own sets of tax obligations, including income tax, payroll taxes (if they have employees), and potentially excise taxes. Businesses must also adhere to strict payment schedules and reporting requirements.

The “why” is simple: taxes fund public services, infrastructure, and government operations. Adherence to tax laws ensures a functioning society and prevents legal and financial repercussions for non-compliance.

Types of Taxes You Might Owe

Beyond the general concept of “income tax,” taxpayers might encounter several specific types of federal taxes that require direct payment:

- Income Tax: The most common form, levied on earnings from wages, salaries, investments, and other sources.

- Estimated Tax: Payments made by individuals or businesses who expect to owe at least $1,000 in tax (for individuals) or $500 (for corporations) and who do not have sufficient tax withheld from other sources. These are typically paid quarterly.

- Self-Employment Tax: Covers Social Security and Medicare taxes for individuals who work for themselves.

- Payroll Taxes: For employers, these include withholding federal income tax, Social Security, and Medicare taxes from employee wages, as well as paying the employer’s share of Social Security and Medicare taxes, and federal unemployment tax (FUTA).

- Excise Taxes: Special taxes imposed on the manufacture, sale, or use of certain goods and services, such as fuel, airline tickets, and certain health-related items.

- Penalties and Interest: These can accrue if you fail to pay enough tax throughout the year, don’t file on time, or don’t pay on time.

Key Payment Deadlines to Remember

Missing a payment deadline can result in penalties and interest, so staying organized is paramount.

- April 15th (Tax Day): The primary deadline for filing individual income tax returns and paying any remaining balance due for the previous tax year. If April 15th falls on a weekend or holiday, the deadline shifts to the next business day.

- Estimated Tax Due Dates: For estimated taxes, the year is divided into four payment periods with specific due dates:

- Period 1 (Jan 1 to March 31): April 15

- Period 2 (April 1 to May 31): June 15

- Period 3 (June 1 to Aug 31): September 15

- Period 4 (Sept 1 to Dec 31): January 15 of the next year

- Again, if these dates fall on a weekend or holiday, the deadline moves to the next business day.

- Business Tax Deadlines: Vary significantly based on the business structure (e.g., March 15 for S-corps and partnerships, April 15 for C-corps with a calendar year-end). Employers also have specific payroll tax deposit schedules (monthly or semi-weekly).

A Comprehensive Guide to IRS Payment Methods

The IRS offers a variety of payment methods designed to accommodate different preferences and financial situations. Understanding each option allows taxpayers to choose the most convenient and secure way to fulfill their obligations.

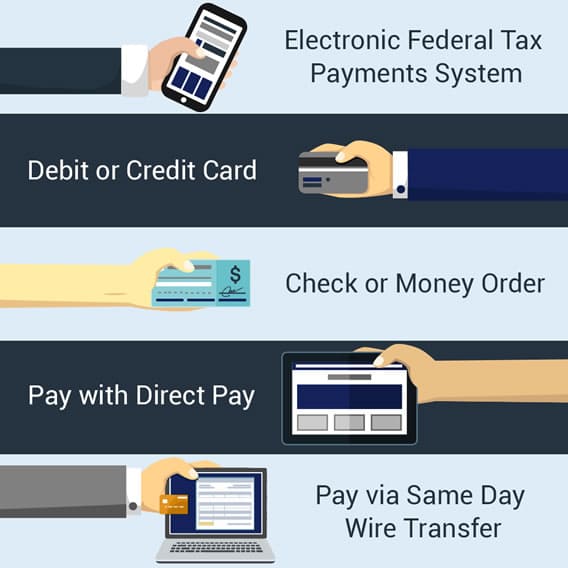

Direct Pay (IRS.gov)

IRS Direct Pay is a free, secure web-based service that allows individuals to pay their tax bills or estimated taxes directly from their checking or savings account.

- How it Works: You select the reason for payment (e.g., income tax, estimated tax), the tax year, and enter your bank account information. You’ll receive an immediate confirmation email.

- Benefits: No fees, highly secure, easy to use, and available 24/7.

- Considerations: Only for payments from checking or savings accounts.

Debit Card, Credit Card, or Digital Wallet

You can pay your taxes using a credit card, debit card, or digital wallet (such as PayPal) through one of several authorized third-party payment processors.

- How it Works: You choose a processor from the IRS website, provide your tax information and payment details, and the processor remits the payment to the IRS.

- Fees: Processors charge a convenience fee, which varies depending on the type of card/wallet used and the processor. Debit card fees are usually flat and low, while credit card fees are a percentage of the payment, typically 1.87% to 1.99%.

- Benefits: Convenience, potential to earn rewards points (for credit cards), and immediate payment confirmation.

- Considerations: The fees can add up, especially for large payments. Evaluate if the rewards outweigh the fees.

Electronic Federal Tax Payment System (EFTPS)

EFTPS is a free service provided by the U.S. Department of the Treasury that allows individuals and businesses to make federal tax payments electronically. It’s particularly useful for recurring payments like estimated taxes or payroll taxes.

- How it Works: Requires pre-enrollment and takes about 5-7 business days to receive a PIN and internet password. Once enrolled, you can schedule payments up to 365 days in advance.

- Benefits: Free, secure, reliable, offers a payment history, and allows for advance scheduling. Essential for many businesses making payroll tax deposits.

- Considerations: Requires advance enrollment, which can be a barrier for last-minute payments.

Electronic Funds Withdrawal (EFW)

If you file your tax return electronically (e-file) through tax software or with a tax professional, you can authorize an electronic funds withdrawal (EFW) from your bank account.

- How it Works: You simply provide your bank account details when e-filing, and the payment is automatically debited on your chosen date (up to the filing deadline).

- Benefits: Convenient, free, and integrated directly into the filing process.

- Considerations: Only available when e-filing an original return or certain amended returns.

Paying by Check or Money Order

For those who prefer traditional methods, you can mail a check or money order to the IRS.

- How it Works: Make your check or money order payable to the “U.S. Treasury.” Write your name, address, daytime phone number, Social Security number or EIN, the tax year, and the related tax form number (e.g., “2023 Form 1040”) on the check/money order. Include a payment voucher (Form 1040-V for individuals) and mail it to the appropriate IRS address.

- Benefits: Simple, no electronic requirements.

- Considerations: Slower, risk of mail delays or loss, no immediate confirmation. Ensure proper labeling to avoid processing delays.

Cash Payments

While less common, cash payments are possible through specific IRS retail partners.

- How it Works: You generate a payment barcode online (e.g., using ACI Payments, Inc. or PayNearMe), take it to a participating retail store (like 7-Eleven or CVS), and pay with cash.

- Benefits: Caters to those who prefer or need to pay with cash.

- Considerations: May involve a fee, daily payment limits, and requires finding a participating retailer. Keep your receipt as proof of payment.

Strategies for Managing Challenging Payment Situations

Life is unpredictable, and sometimes taxpayers face difficulties in meeting their tax obligations. The IRS offers various programs and options to help taxpayers navigate these challenges, emphasizing compliance while understanding individual circumstances.

What to Do If You Can’t Pay On Time

If you find yourself unable to pay your full tax bill by the deadline, ignoring the issue is the worst approach. The IRS offers several relief options:

- Request an Extension to File: Filing Form 4868 grants an automatic extension to file your tax return, usually until October 15th. However, this is not an extension to pay. You must still pay an estimate of your taxes by the original deadline to avoid penalties and interest.

- Short-Term Payment Plan: You can request up to 180 additional days to pay your tax liability in full, though interest and penalties still apply. This is often an administrative approval.

- Installment Agreement: If you need more than 180 days, you may qualify for an installment agreement, allowing you to make monthly payments for up to 72 months. You’ll need to submit Form 9465, and interest and late-payment penalties generally continue to accrue, though the late-payment penalty rate may be reduced.

- Offer in Compromise (OIC): An OIC allows certain taxpayers to resolve their tax liability with the IRS for a lower amount than what they originally owe. This option is typically for individuals experiencing extreme financial hardship and requires the IRS to determine that there is “doubt as to collectibility.” It’s a complex process and not every applicant qualifies.

Making Estimated Tax Payments

For self-employed individuals, freelancers, gig workers, and those with significant investment income, estimated taxes are critical.

- Who Needs to Pay: Generally, if you expect to owe at least $1,000 in tax for the year and your withholding and credits are less than 90% of your current year’s tax liability or 100% of your prior year’s tax liability (110% for high-income taxpayers).

- How Often: Payments are typically made quarterly, as outlined in the “Key Payment Deadlines” section.

- Calculation: Use Form 1040-ES, Estimated Tax for Individuals, to calculate your estimated tax. This involves estimating your total income, deductions, and credits for the year. Adjustments may be necessary throughout the year if your income or deductions change significantly.

Paying Penalties and Interest

Penalties and interest are assessed by the IRS for various reasons, primarily for underpayment of estimated tax, late filing, and late payment.

- Understanding Why They Occur: Penalties are often a fixed percentage or amount, while interest is charged on underpayments and applies to any unpaid tax from the due date until the date of payment.

- How to Remit: If you receive a notice from the IRS assessing penalties and interest, the notice will typically explain how to pay the amount due. You can use any of the standard payment methods. In some cases, you may be able to request penalty abatement if you can show reasonable cause and acted in good faith.

Best Practices for Seamless Tax Payments and Record-Keeping

Effective tax payment isn’t just about knowing how to pay; it’s about adopting practices that ensure accuracy, security, and long-term financial clarity. Proactive management can significantly reduce stress and potential issues.

Ensuring Accuracy and Avoiding Errors

Mistakes can be costly. Double-checking your figures and payment information is paramount.

- Review Thoroughly: Before making any payment, meticulously review the amount, the tax year it applies to, and your personal identifying information (SSN/EIN).

- Utilize Professionals: Consider using tax software or a qualified tax professional (CPA, Enrolled Agent) for complex situations or if you’re unsure about your calculations. They can help ensure accuracy and identify potential deductions or credits you might miss.

- Confirm Account Details: If paying electronically, double-check bank account numbers to prevent payments from being sent to incorrect accounts.

Safeguarding Your Financial Information

With digital payments becoming the norm, protecting your financial data is more critical than ever.

- Secure Connections: Always ensure you are on a secure website (look for “https://” and a padlock icon) when making online payments. Only use official IRS channels or authorized third-party processors.

- Phishing Awareness: Be wary of suspicious emails, texts, or calls claiming to be from the IRS. The IRS typically initiates contact via mail for official matters. Never click on suspicious links or provide personal information in response to unsolicited communications.

- Strong Passwords: Use unique, strong passwords for any online tax accounts (like EFTPS) and consider two-factor authentication where available.

Maintaining Diligent Records

Thorough record-keeping is the backbone of responsible financial management and essential for tax purposes.

- Why It’s Important: Proof of payment is vital. In case of discrepancies or audits, having clear records can save you significant headaches and potential penalties.

- What to Keep: Retain confirmation numbers for electronic payments, copies of canceled checks, receipts for cash payments, and copies of all filed tax returns and payment vouchers.

- How Long: The IRS generally recommends keeping tax records for at least three years from the date you filed your original return or two years from the date you paid the tax, whichever is later. For complex situations (e.g., claiming a loss from worthless securities), this period can extend up to seven years. Store records securely, whether digitally or physically.

Leveraging Financial Planning for Tax Efficiency

Beyond merely paying taxes, integrating tax considerations into your broader financial planning can lead to greater efficiency and savings.

- Proactive Planning: Understand the tax implications of your financial decisions throughout the year, not just at tax time. This includes investment choices, retirement contributions, and major purchases.

- Tax-Advantaged Accounts: Maximize contributions to tax-advantaged retirement accounts (401(k)s, IRAs) and health savings accounts (HSAs) to reduce your taxable income.

- Professional Guidance: Work with a financial advisor who can help you develop a comprehensive strategy that minimizes your tax burden while aligning with your financial goals.

By understanding your obligations, utilizing the appropriate payment methods, managing potential challenges, and adopting robust record-keeping practices, you can transform the often-dreaded task of paying the IRS into a well-managed and straightforward financial responsibility. This proactive approach not only ensures compliance but also contributes to your overall financial well-being and peace of mind.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.