Navigating the complexities of tax season can be daunting, but fulfilling your payment obligations to the Internal Revenue Service (IRS) doesn’t have to be. For individuals, businesses, and organizations alike, understanding the various methods available to make IRS payments is crucial for compliance, avoiding penalties, and maintaining sound financial health. In an increasingly digital world, the IRS has significantly expanded its electronic payment options, offering convenience, speed, and security. However, traditional methods still exist for those who prefer them. This comprehensive guide will illuminate the diverse pathways to settle your tax dues, ensuring you choose the method that best fits your financial situation and preferences.

Understanding Your IRS Payment Obligations

Before diving into how to pay, it’s essential to understand what you’re paying and why. The IRS collects various types of taxes, and your specific obligation will dictate the appropriate payment process and necessary information. A clear understanding of your tax liabilities is the first step toward a seamless payment experience.

Types of Payments

Tax obligations aren’t a one-size-fits-all scenario. Depending on your income, business structure, and financial activities throughout the year, you might owe the IRS for several different reasons:

- Balance Due on Filed Return: This is the most common payment type, representing the additional tax you owe after filing your annual tax return (e.g., Form 1040 for individuals, Form 1120 for corporations). Even if you receive a refund, you might still owe taxes if you made certain financial moves during the year.

- Estimated Taxes: Many taxpayers, particularly those who are self-employed, own small businesses, or have significant income not subject to withholding (e.g., rental income, investment income), are required to pay estimated taxes quarterly. This ensures you pay income tax and self-employment tax as you earn income, rather than a large lump sum at year-end, helping to avoid underpayment penalties.

- Tax Extension Payments: Filing an extension (e.g., Form 4868 for individuals, Form 7004 for businesses) grants you more time to file your tax return, but it does not extend the time to pay any taxes due. If you anticipate owing money, you should estimate your tax liability and make a payment by the original due date to avoid interest and penalties.

- Underpayment/Penalty Payments: If you didn’t pay enough tax throughout the year or missed deadlines, the IRS might assess penalties. These can include penalties for failure to file, failure to pay, and accuracy-related penalties. Paying these promptly is important to prevent further interest accrual.

Key Information Needed for Payment

Regardless of the payment method you choose, you’ll almost always need to provide some fundamental information to ensure your payment is correctly attributed to your account. This typically includes:

- Taxpayer Identification Number (TIN): This could be your Social Security Number (SSN), Individual Taxpayer Identification Number (ITIN), or Employer Identification Number (EIN) for businesses.

- Tax Period: The tax year or period for which the payment is being made (e.g., 2023).

- Payment Amount: The precise amount you intend to pay.

- Payment Type: Specifying if it’s for an annual balance due, estimated tax, an extension, or a specific penalty.

Accurately providing this information is crucial to avoid processing delays or misapplication of your payment, which could lead to unnecessary IRS correspondence or penalties.

Digital Payment Methods for IRS Payments

The IRS strongly encourages taxpayers to utilize its electronic payment options, citing their security, speed, and efficiency. These methods eliminate mail delays, provide instant confirmation, and reduce the risk of errors associated with paper transactions.

IRS Direct Pay

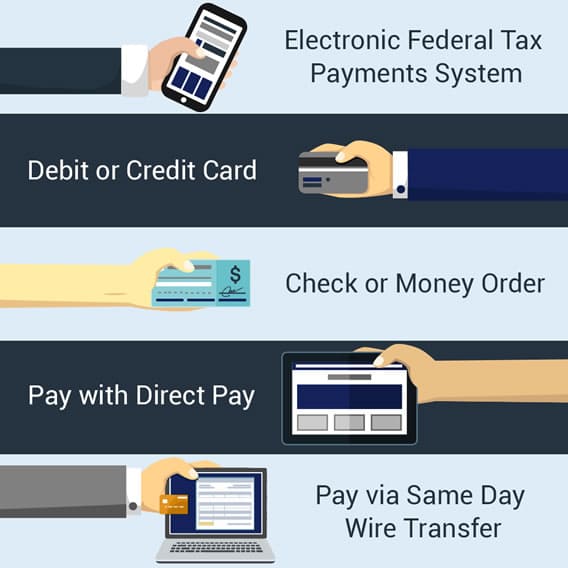

IRS Direct Pay is a free, secure, and convenient service provided directly by the IRS, allowing you to pay your tax bill or estimated taxes directly from your checking or savings account.

- Overview: It’s designed for individual taxpayers and offers a straightforward way to make a payment without any fees. You can schedule payments up to 365 days in advance.

- Pros: No fees, instant confirmation number, secure and direct, available 24/7. It’s user-friendly and doesn’t require pre-registration. You can view your payment history for up to 15 months.

- Cons: Limited to two payments within a 24-hour period (for two different tax types or periods), and daily payment limits may apply depending on the bank. It’s primarily for individual income tax payments.

- Use Cases: Ideal for individuals paying their annual balance due, estimated taxes, or an extension payment.

Electronic Federal Tax Payment System (EFTPS)

EFTPS is the government’s flagship electronic payment service, suitable for virtually all types of federal taxes. It’s particularly favored by businesses and taxpayers who make frequent or large tax payments.

- Overview: EFTPS requires a one-time enrollment process, which can take several business days to complete. Once enrolled, you can schedule payments up to 365 days in advance and review your payment history for up to 15 months. Payments are made directly from your bank account.

- Pros: Highly versatile, accommodating all federal tax types (income, payroll, excise, etc.), offers robust scheduling features, and provides a clear audit trail. It’s free to use.

- Cons: Requires enrollment, which can be time-consuming for first-time users. It may not be as intuitive for sporadic individual payments as IRS Direct Pay.

- Use Cases: Essential for businesses paying payroll taxes, corporate income taxes, or excise taxes. Also highly recommended for individuals making regular estimated tax payments.

Debit/Credit Card or Digital Wallet

For those who prioritize convenience and potentially earning rewards points, paying taxes via debit card, credit card, or a digital wallet (like PayPal or Click to Pay) through an authorized third-party payment processor is an attractive option.

- Overview: The IRS does not directly process credit or debit card payments. Instead, it partners with several approved third-party payment processors. You’ll visit their websites, enter your tax information, and process the payment there.

- Pros: Extreme convenience, often allowing payments from anywhere with an internet connection. Credit card payments offer the potential for rewards points, cash back, or sign-up bonuses, which might offset the processing fee for some high-spenders. Digital wallets add an extra layer of security as your card details aren’t directly shared with the processor.

- Cons: Processing fees apply. These fees are charged by the third-party processor, not the IRS, and typically range from 1.87% to 2.29% for credit cards, and a flat fee (e.g., $2.50) for debit cards. These fees can add up, especially for large tax bills.

- Providers: The IRS website lists approved processors such as PayUSAtax, ACI Payments, Inc., and OfficialPayments. It’s crucial to use only IRS-authorized processors.

Traditional and Alternative Payment Options

While digital methods are increasingly popular, the IRS still provides traditional and alternative payment options to ensure accessibility for all taxpayers. These methods might be preferred by those less comfortable with online transactions or who have specific needs.

Electronic Funds Withdrawal (EFW) During E-Filing

This method integrates payment directly into the tax filing process when using tax preparation software or a tax professional.

- Overview: When you electronically file your tax return (e-file) using tax software or through a tax preparer, you can authorize an electronic funds withdrawal from your designated bank account. This effectively combines filing and paying into a single, streamlined transaction.

- Pros: Highly convenient, reduces the chance of errors as information is typically pulled directly from your return, and ensures the payment is linked to your e-filed return. No separate steps required after filing.

- Cons: Only available at the time of e-filing. If you file a paper return or need to make an additional payment later, you’ll need to use another method. It also can’t be used for estimated tax payments throughout the year, only for the balance due on the return.

- Use Cases: Ideal for taxpayers who e-file their annual return and wish to pay any balance due simultaneously.

Check, Money Order, or Cashier’s Check

For those who prefer a tangible payment method, mailing a check or money order remains a viable option.

- Overview: You can send a personal check, money order, or cashier’s check made payable to the “U.S. Treasury.” It’s critical to include the correct payment voucher (e.g., Form 1040-V for individual income tax) with your payment. This voucher ensures your payment is correctly identified and applied to your account. Write your name, address, daytime phone number, Social Security number (or EIN), the tax year, and the related tax form number (e.g., “2023 Form 1040”) on the check or money order.

- Pros: A traditional method familiar to many. No processing fees charged by the IRS. Provides a physical record (canceled check).

- Cons: Slower due to mail processing, potential for mail delays or loss, less secure than electronic methods, and no instant confirmation. Requires accurate completion of payment voucher and correct mailing address.

- Instructions: The IRS website provides specific mailing addresses for different types of payments and locations. Always verify the correct address before mailing.

Cash Payments

While less common, it is possible to make cash payments through IRS-authorized retail partners.

- Overview: The IRS has partnered with various retail stores across the country to allow taxpayers to pay their federal taxes in cash. You’ll typically need to visit an IRS website or use an app to generate a payment barcode, which you then present at a participating retailer.

- Pros: Provides an option for those without bank accounts or who prefer to deal solely in cash. Can be convenient if a retail partner is nearby.

- Cons: Requires finding an authorized retail partner. May involve small fees charged by the retailer. Not a direct payment to the IRS, adding an intermediary step. Maximum payment limits may apply.

- Use Cases: Primarily for taxpayers who do not have access to traditional banking services or prefer to pay in cash.

Important Considerations and Best Practices

Making your IRS payments correctly and on time is a cornerstone of responsible financial management. Adhering to best practices can save you from unnecessary stress, penalties, and interest.

Payment Deadlines and Penalties

Tax deadlines are non-negotiable. Missing a payment deadline can result in penalties and interest charges, which accrue from the original due date until the payment is received.

- Importance of Meeting Deadlines: Understand the key dates for your annual tax return, estimated tax payments, and extension payments. Calendar these dates to ensure timely action.

- Extensions to File vs. Extensions to Pay: Remember that an extension to file your return (e.g., Form 4868) does not grant an extension to pay any taxes due. If you anticipate owing money, you must estimate and pay by the original due date to avoid penalties and interest.

- Penalties and Interest: The IRS charges penalties for failure to file, failure to pay, and underpayment of estimated tax. Interest is charged on underpayments and applies to unpaid taxes from the due date until the date of payment. These can significantly increase your overall tax burden.

Record Keeping

Meticulous record keeping is vital for financial accountability and for resolving any discrepancies that may arise with the IRS.

- Importance of Records: Always retain confirmation numbers for electronic payments, bank statements showing debits, copies of checks (front and back), and proof of mailing for paper payments.

- Duration: Keep these records with your tax documents for at least three years from the date you filed your original return or two years from the date you paid the tax, whichever is later. Some records, particularly for investments or property, should be kept even longer.

- Digital vs. Physical: Whether you prefer digital files or physical folders, ensure your payment records are organized, accessible, and securely stored.

What to Do If You Can’t Pay

Sometimes, despite best efforts, taxpayers face situations where they cannot pay their full tax liability by the deadline. It’s crucial not to ignore the problem.

- Contact the IRS Proactively: If you cannot pay, contact the IRS as soon as possible. They have programs designed to help taxpayers in financial distress.

- Payment Plans:

- Installment Agreement: Allows you to make monthly payments for up to 72 months. You’ll still owe penalties and interest, but they might be reduced.

- Offer in Compromise (OIC): Allows certain taxpayers to resolve their tax liability with the IRS for a lower amount than what they originally owe. This is typically an option when taxpayers are in severe financial difficulty.

- Short-Term Payment Plan: You might be granted up to 180 days to pay your tax liability in full, although interest and penalties still apply.

- Reducing Penalties: In some cases, the IRS may waive penalties if you have a reasonable cause for failure to pay. However, interest cannot typically be waived. Always pay as much as you can, even if you can’t pay the full amount, to minimize interest and penalties.

In conclusion, making IRS payments has evolved significantly, offering a spectrum of choices from instant digital transfers to traditional mail-in options. By understanding your obligations, selecting the most appropriate payment method, and adhering to critical deadlines, you can fulfill your tax responsibilities efficiently and confidently. Proactive planning, accurate record-keeping, and seeking assistance when needed are the pillars of managing your IRS payments effectively, contributing to your overall financial well-being and peace of mind.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.