Investing for retirement is one of the most crucial financial decisions an individual can make, and for many, an Individual Retirement Account (IRA) serves as a cornerstone of that strategy. An IRA is more than just a savings account; it’s a powerful, tax-advantaged investment vehicle designed to help you build wealth specifically for your golden years. While the concept of an IRA is straightforward, the nuances of choosing the right type, understanding what to invest in, and developing an effective strategy can seem daunting.

This comprehensive guide will demystify the process, illuminating the landscape of IRAs, exploring various investment avenues, and equipping you with the knowledge to craft a robust investment strategy. Whether you’re just starting your investment journey or looking to optimize an existing retirement plan, understanding how to effectively invest with an IRA is paramount to securing a comfortable and financially stable future.

Understanding the IRA Landscape: Your Gateway to Retirement Security

Before delving into the specifics of investment, it’s essential to grasp what an IRA is and why it holds such significance in personal finance. Far from being a mere savings account, an IRA is a special type of investment account that offers unique tax benefits to encourage long-term savings for retirement.

What is an IRA?

An IRA, or Individual Retirement Account (sometimes referred to as an Individual Retirement Arrangement), is a savings plan that allows individuals to save and invest money for retirement with tax-deferred or tax-free growth. Unlike employer-sponsored plans like a 401(k), an IRA is opened and managed by an individual, though contributions may be tax-deductible depending on the type of IRA and the individual’s income. The primary purpose of an IRA is to provide a tax-efficient mechanism for individuals to accumulate a substantial nest egg for retirement, often complementing other retirement savings. Each year, the IRS sets limits on how much an individual can contribute to an IRA, ensuring that these tax advantages are leveraged responsibly.

Why Invest Through an IRA?

The allure of IRAs lies in their distinct advantages, primarily centered around tax benefits and the incredible power of compounding.

- Tax Benefits: This is the cornerstone. Depending on the IRA type, contributions might be tax-deductible, reducing your taxable income in the present (Traditional IRA), or your qualified withdrawals in retirement could be entirely tax-free (Roth IRA). This tax shield allows more of your money to work for you, rather than being eroded by annual taxes.

- Compounding Power: By sheltering your investments from annual taxes, IRAs allow your money to grow uninterrupted. The earnings on your earnings, over decades, can lead to exponential growth, a phenomenon often referred to as “the eighth wonder of the world.” This uninterrupted growth significantly accelerates your wealth accumulation compared to a taxable investment account.

- Accessibility: For individuals who don’t have access to an employer-sponsored retirement plan, or who wish to supplement one, IRAs provide a critical avenue for dedicated retirement savings. They are accessible to virtually anyone with earned income, making them a universal tool for retirement planning.

- Diversification of Retirement Savings: Even if you have a 401(k), having an IRA allows you to diversify not just your investments, but also your tax treatment in retirement. A mix of pre-tax (401(k), Traditional IRA) and after-tax (Roth IRA) accounts provides flexibility in managing your taxable income during your retirement years.

Navigating Different IRA Types: Choosing the Right Vehicle

The world of IRAs isn’t monolithic; it comprises several distinct types, each with its own rules, benefits, and ideal use cases. Understanding the differences between these vehicles is crucial for selecting the one that best aligns with your financial situation and retirement goals.

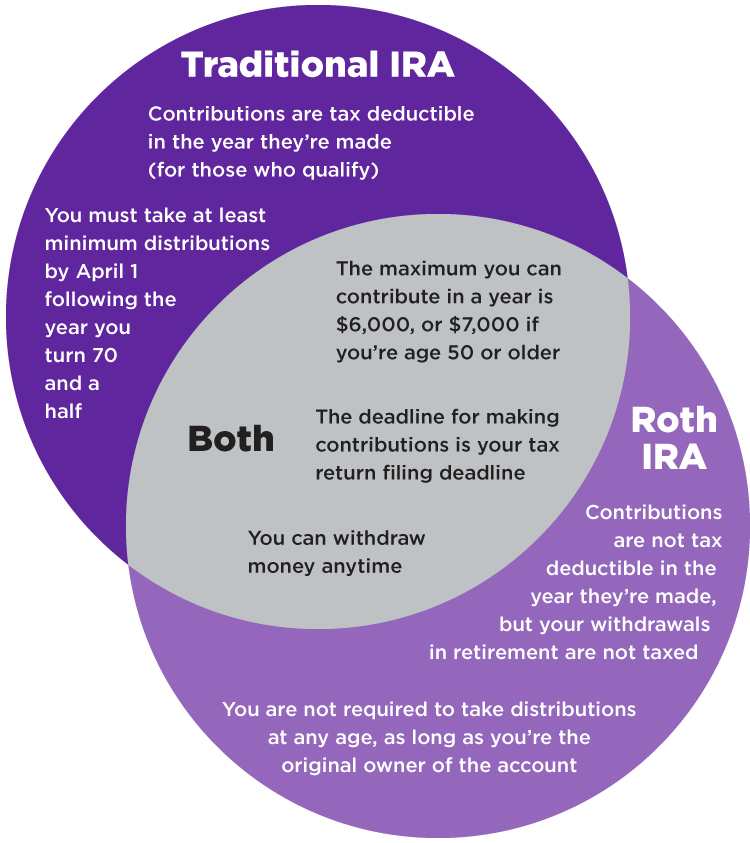

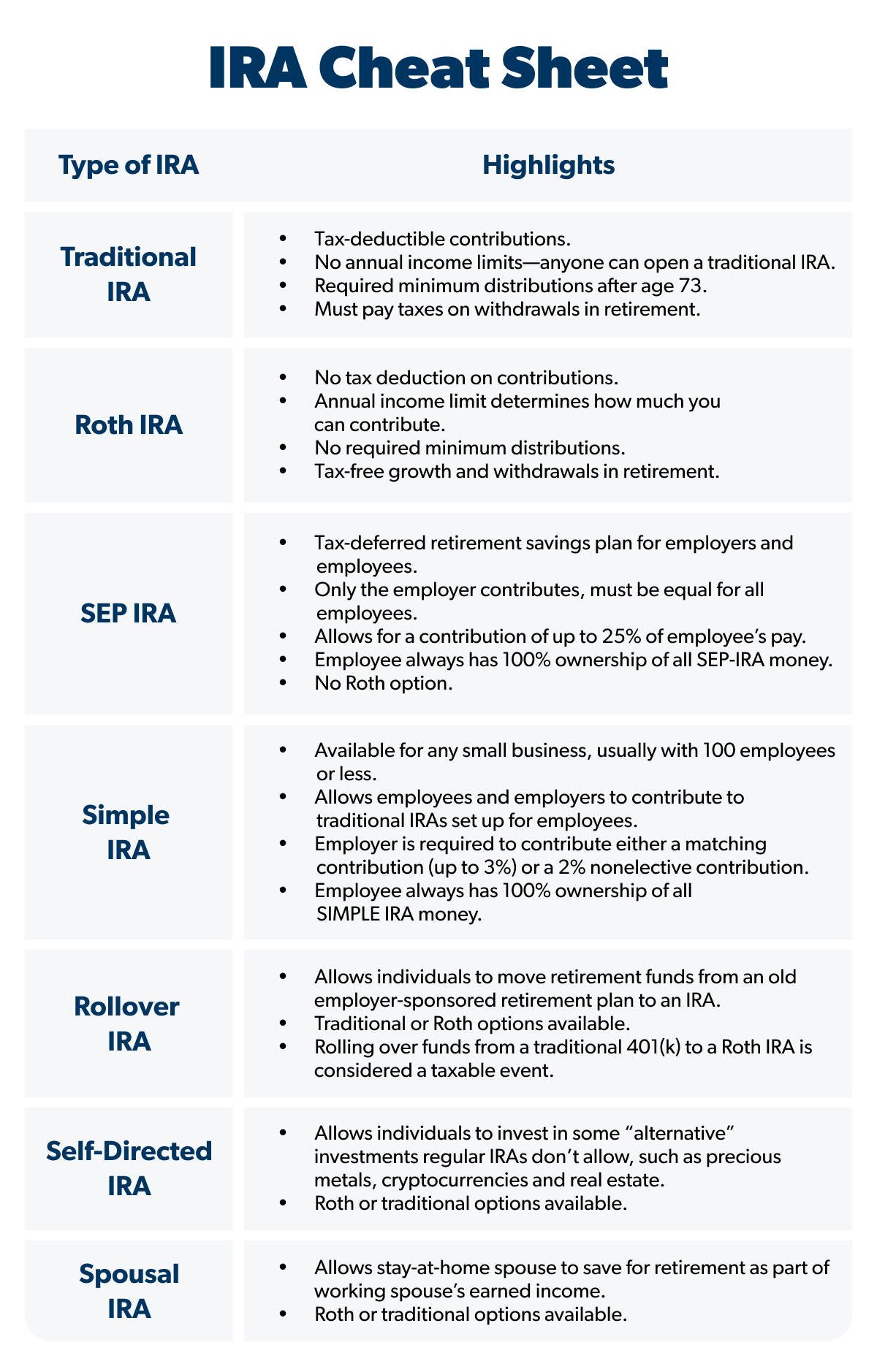

Traditional IRA: The Power of Tax-Deferred Growth

The Traditional IRA is the classic choice for many investors. Its key feature is its tax-deferred growth: your contributions may be tax-deductible in the year they are made (depending on your income and whether you have an employer-sponsored retirement plan), and your investments grow tax-free until you withdraw them in retirement. At that point, withdrawals are taxed as ordinary income.

- Who it’s Best For: Individuals who expect to be in a lower tax bracket in retirement than they are now, or those seeking an immediate tax deduction. It’s particularly attractive to high-income earners who want to reduce their current taxable income.

Roth IRA: The Allure of Tax-Free Retirement Income

The Roth IRA operates on a different tax principle. Contributions to a Roth IRA are made with after-tax dollars, meaning they are not tax-deductible in the current year. However, this upfront tax payment comes with a significant future benefit: your investments grow tax-free, and qualified withdrawals in retirement are also entirely tax-free.

- Who it’s Best For: Younger investors who anticipate being in a higher tax bracket in retirement, or those who value the certainty of tax-free income later in life. There are income limitations for directly contributing to a Roth IRA, but strategies like the “Backdoor Roth” allow higher earners to still participate.

Employer-Sponsored IRAs: SEP and SIMPLE

While Traditional and Roth IRAs are for individual contributions, there are also IRA options designed for small businesses and self-employed individuals, offering higher contribution limits.

- SEP IRA (Simplified Employee Pension): Ideal for self-employed individuals and small business owners, a SEP IRA allows employers to contribute to their own and their employees’ retirement accounts. Contribution limits are significantly higher than Traditional or Roth IRAs, calculated as a percentage of compensation.

- SIMPLE IRA (Savings Incentive Match Plan for Employees): Designed for small businesses with 100 or fewer employees, a SIMPLE IRA allows both employee contributions and mandatory employer contributions (either a matching contribution or a non-elective contribution). It’s a simpler, less administrative alternative to a 401(k).

Spousal IRAs

It’s worth noting that if you are married and filing jointly, and one spouse earns income but the other does not, the working spouse can contribute to an IRA on behalf of their non-working spouse. This “spousal IRA” allows families to double their retirement savings potential, utilizing the same Traditional or Roth IRA rules.

Investment Avenues within Your IRA: Building Your Portfolio

Once you’ve chosen the right type of IRA, the next critical step is deciding what to invest in. An IRA itself is merely the account wrapper; the real growth happens through the underlying investments you select. The good news is that IRAs offer a vast universe of investment options, allowing you to tailor your portfolio to your risk tolerance and financial goals.

Stocks and Exchange-Traded Funds (ETFs)

- Individual Stocks: Investing in individual company stocks allows you to directly own a piece of a company. This offers the potential for high growth but also comes with higher risk. You can choose growth stocks, value stocks, or dividend stocks depending on your strategy.

- Exchange-Traded Funds (ETFs): ETFs are funds that hold a basket of assets, like stocks, bonds, or commodities, and trade on stock exchanges like individual stocks. They offer instant diversification, often at a lower cost than mutual funds, and can track broad market indices (e.g., S&P 500), specific sectors, or entire countries.

Mutual Funds

Mutual funds pool money from multiple investors to invest in a diversified portfolio of securities. They are managed by professional fund managers who make investment decisions on behalf of the fund’s investors.

- Actively Managed Funds: Managers aim to outperform a specific market index by actively buying and selling securities. These typically have higher expense ratios.

- Index Funds: These are a type of mutual fund (or ETF) designed to passively track the performance of a specific market index. They generally have lower fees and are a popular choice for long-term investors seeking broad market exposure.

Bonds and Fixed-Income Securities

Bonds are debt instruments where you lend money to a government or corporation in exchange for regular interest payments and the return of your principal at maturity. They generally offer lower returns than stocks but provide more stability and income.

- Government Bonds: Issued by national, state, or municipal governments (e.g., Treasury bonds, municipal bonds).

- Corporate Bonds: Issued by companies to raise capital.

- Bond Funds/ETFs: Provide diversification across many different bonds, managed by professionals.

Real Estate Investment Trusts (REITs)

REITs are companies that own, operate, or finance income-producing real estate. They trade on stock exchanges like regular stocks, allowing you to invest in a portfolio of real estate without directly owning physical properties. REITs are known for providing consistent income through dividends.

Cash Equivalents and Money Market Funds

While not growth-oriented, cash equivalents like money market funds are crucial for liquidity and as a temporary holding place for funds. They offer low risk and preserve capital, making them suitable for emergency funds within your IRA or for funds awaiting deployment into other investments.

Crafting Your IRA Investment Strategy: Principles for Success

Having access to a myriad of investment options is only half the battle; the other half is developing a sound strategy to guide your choices. A well-thought-out investment strategy is crucial for navigating market fluctuations and achieving your long-term retirement goals.

Define Your Risk Tolerance and Time Horizon

Your investment strategy must align with your personal comfort level with risk and the length of time you have until retirement.

- Risk Tolerance: How much fluctuation in your portfolio value can you comfortably withstand? Are you aggressive, moderate, or conservative? This will dictate your asset allocation.

- Time Horizon: If you’re decades away from retirement, you have a longer time horizon and can generally afford to take on more risk (e.g., higher allocation to stocks). As you approach retirement, you might shift towards more conservative investments to preserve capital.

Asset Allocation and Diversification

Asset allocation is the process of dividing your investment portfolio among different asset categories, such as stocks, bonds, and cash. Diversification involves spreading your investments across various securities within those asset categories to minimize risk.

- Importance: Diversification reduces “specific risk” – the risk that a single investment performs poorly. A well-diversified portfolio aims to balance risk and reward, ensuring that no single investment can disproportionately harm your overall returns.

- Common Rule of Thumb: A frequently cited guideline suggests subtracting your age from 110 or 120 to determine the percentage of your portfolio that should be allocated to stocks, with the remainder in bonds. This is a starting point and should be adjusted based on individual circumstances.

The Power of Dollar-Cost Averaging

Dollar-cost averaging (DCA) is an investment strategy where you invest a fixed amount of money at regular intervals, regardless of the market’s performance.

- Benefits: This approach helps mitigate the risk of market timing. When prices are high, your fixed dollar amount buys fewer shares; when prices are low, it buys more shares. Over time, this tends to result in a lower average cost per share and smooths out the impact of market volatility. It also instills discipline and consistency in your investing habits.

Rebalancing Your Portfolio

Over time, market fluctuations will cause your initial asset allocation to drift. Rebalancing is the process of adjusting your portfolio back to your target asset allocation.

- Why Rebalance? If stocks have performed exceptionally well, they might now represent a larger percentage of your portfolio than you initially intended, increasing your overall risk. Rebalancing involves selling some of your overperforming assets and buying more of your underperforming assets to restore your desired risk level. This can be done annually or when your allocation drifts by a certain percentage (e.g., 5-10%).

Understanding Fees and Expenses

Fees can significantly erode your long-term returns. Always be vigilant about the costs associated with your investments.

- Expense Ratios: This is the annual fee charged by mutual funds and ETFs, expressed as a percentage of your investment. Even seemingly small differences (e.g., 0.1% vs. 1.0%) can translate into tens of thousands of dollars over decades.

- Trading Fees: Some brokers charge commissions for buying or selling individual stocks or ETFs, though many now offer commission-free trading.

- Advisory Fees: If you work with a financial advisor, understand how they are compensated. Prioritize low-cost index funds and ETFs whenever possible, as their lower expense ratios leave more of your money invested and growing.

Optimizing Your IRA for Long-Term Growth: Advanced Tips and Considerations

Beyond the foundational strategies, several advanced tips can help you maximize the long-term growth potential of your IRA and navigate potential complexities.

Maximize Contributions Annually

The most straightforward way to supercharge your IRA growth is to consistently contribute the maximum allowable amount each year. This maximizes the tax advantages and gives your money more time to compound.

- Catch-Up Contributions: For individuals aged 50 and over, the IRS allows additional “catch-up” contributions to IRAs, acknowledging that those nearing retirement might need to accelerate their savings. Make sure to take advantage of these if eligible.

The Backdoor Roth Strategy

For high-income earners whose Modified Adjusted Gross Income (MAGI) exceeds the IRS limits for direct Roth IRA contributions, the “Backdoor Roth” is a popular and legal strategy. It involves contributing to a non-deductible Traditional IRA and then immediately converting those funds to a Roth IRA. While the contribution to the Traditional IRA wasn’t deductible, the conversion itself is tax-free if no pre-tax funds are involved (Pro-Rata Rule is important here if you have other Traditional IRAs with pre-tax dollars). This allows high earners to still benefit from tax-free growth and withdrawals of a Roth IRA.

Tax Efficiency Within Your IRA

While IRAs are already tax-advantaged, you can optimize them further by strategically placing certain types of investments within them.

- Place Tax-Inefficient Assets in IRAs: Assets that generate significant taxable income annually, such as high-dividend stocks, actively managed funds with high turnover, or bonds that generate interest income, are often best held within an IRA. This shields that income from current taxation, allowing it to compound tax-deferred or tax-free.

- Keep Tax-Efficient Assets in Taxable Accounts: Growth stocks or low-turnover index funds that generate minimal taxable events until sale can be more suitable for taxable brokerage accounts, as their long-term capital gains often receive more favorable tax treatment than ordinary income.

Regular Review and Adjustment

Your financial situation, risk tolerance, and even the market environment can change over time. It’s crucial to review your IRA investments and overall financial plan periodically, ideally at least once a year.

- Life Events: Marriage, children, a new job, or a significant salary change should prompt a review of your investment strategy.

- Market Performance: While you shouldn’t react to every market swing, prolonged bull or bear markets might necessitate rebalancing or a reevaluation of your risk exposure.

Avoiding Common Pitfalls

Successful investing often boils down to avoiding common mistakes:

- Market Timing: Attempting to predict market highs and lows is notoriously difficult and often leads to lower returns than a buy-and-hold strategy.

- Emotional Decisions: Panic selling during downturns or chasing hot stocks can derail your long-term plan. Stick to your strategy and remember that investing is a marathon, not a sprint.

- Excessive Trading: Frequent buying and selling can rack up transaction costs and potentially trigger taxable events (though less of an issue in an IRA, it indicates poor strategy).

- Ignoring Fees: As discussed, even small fees compound over time, significantly impacting your final nest egg.

Investing with an IRA is a powerful and essential component of a robust retirement strategy. By understanding the different types of IRAs, exploring the vast array of investment options, and diligently applying sound investment principles, you can effectively harness the tax advantages and compounding power these accounts offer. Consistent contributions, strategic asset allocation, and regular portfolio reviews are key to maximizing your IRA’s potential and building the financial security you deserve for your future. Remember, securing professional financial advice can always provide personalized guidance tailored to your unique circumstances.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.