For decades, the S&P 500 has stood as the definitive barometer of the American economy. It is the yardstick by which professional fund managers are measured and the vehicle through which millions of everyday investors build their retirement nest eggs. When people talk about “the market,” they are almost always referring to the Standard & Poor’s 500.

Investing in the S&P 500 is often cited by legendary investors like Warren Buffett as the single most effective strategy for the average person to build wealth over time. However, for a beginner, the process can seem daunting. This guide will walk you through the nuances of what the S&P 500 is, the practical steps to purchase it, and the strategic mindset required to succeed in index fund investing.

Understanding the Foundation of the S&P 500

Before committing capital, an investor must understand the mechanics of the index. The S&P 500 is a stock market index that tracks the performance of 500 of the largest companies listed on stock exchanges in the United States. Unlike other indices that might focus on a specific sector, the S&P 500 covers approximately 80% of the available market capitalization of the U.S. equity market, spanning tech, healthcare, finance, and consumer goods.

What Makes a Company S&P 500 Material?

Not just any company can join the index. To be included, a company must meet strict criteria set by the S&P Dow Jones Indices committee. These include a minimum market capitalization (currently in the billions), high liquidity, and, crucially, positive earnings over the most recent four quarters. Because of these requirements, the S&P 500 acts as a filter, automatically removing companies that are failing and adding rising stars. This “self-cleansing” nature is one of the primary reasons the index has historically trended upward over long periods.

The Power of Market-Cap Weighting

The S&P 500 is a market-capitalization-weighted index. This means that larger companies, such as Apple, Microsoft, and Amazon, have a more significant impact on the index’s performance than smaller ones. While this can lead to concentration in the technology sector, it also ensures that your investment is automatically tilted toward the most successful and dominant players in the global economy. As an investor, you don’t have to guess which company will win; you simply own the winners by default.

Practical Steps to Start Your Investment Journey

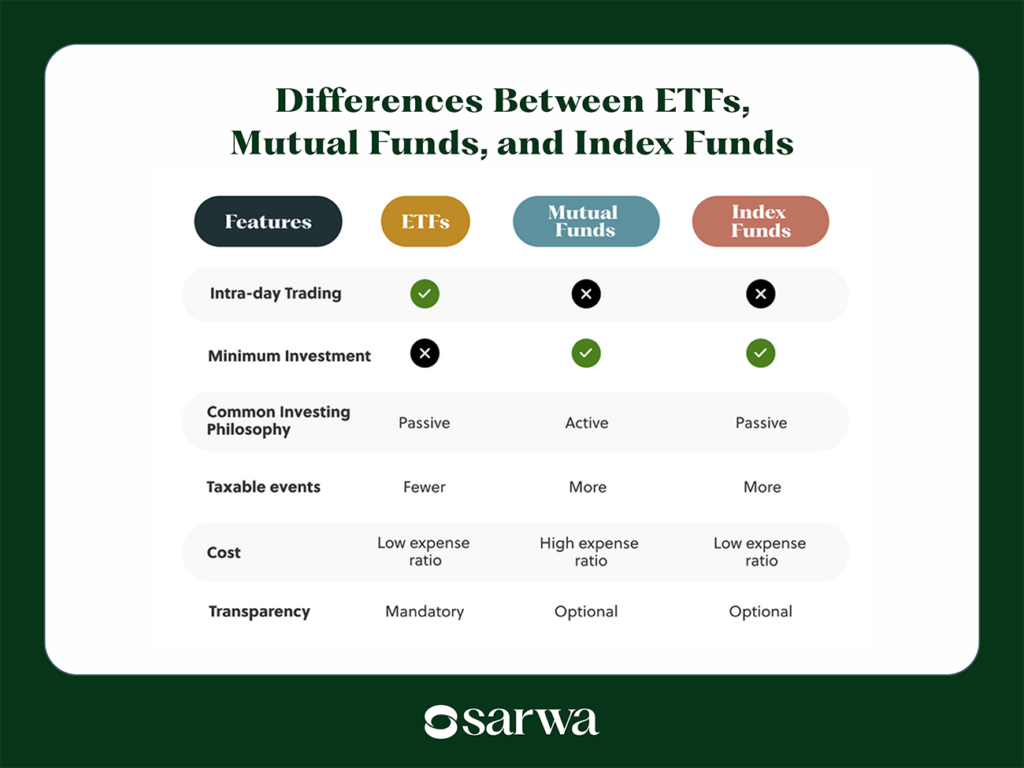

Since you cannot “buy” an index directly (it is just a list of companies), you must use an investment vehicle that mimics its performance. These are typically Index Mutual Funds or Exchange-Traded Funds (ETFs).

Choosing Between ETFs and Index Mutual Funds

Both vehicles offer a way to own all 500 companies in one transaction, but they function differently.

- ETFs (Exchange-Traded Funds): These trade like individual stocks. You can buy them throughout the day at fluctuating prices. Popular examples include Vanguard’s VOO or State Street’s SPY. ETFs are often favored for their tax efficiency and lack of minimum investment requirements.

- Index Mutual Funds: These are priced once at the end of the trading day. While some have minimum investment requirements (e.g., $3,000), they are ideal for investors who want to set up automatic recurring investments of a specific dollar amount, such as $100 every Friday.

Opening a Brokerage Account

To purchase these funds, you need a brokerage account. In the modern era, most major brokerages have eliminated commissions for trading S&P 500 ETFs. When selecting a broker, look for “the big three”: Vanguard, Fidelity, or Charles Schwab. These institutions offer low-cost or zero-cost funds that track the S&P 500 with extreme precision. Once your account is funded, you simply search for the “ticker symbol” (like VOO or IVV) and execute a buy order.

Strategies for Maximizing Your Returns

Simply buying the S&P 500 is a great start, but how you manage that investment over time will determine your ultimate level of wealth. Success in the “Money” niche is as much about behavior as it is about mathematics.

The Magic of Dollar-Cost Averaging (DCA)

One of the biggest mistakes new investors make is trying to “time the market.” They wait for a “dip” that may never come, missing out on gains in the meantime. Dollar-Cost Averaging involves investing a fixed amount of money at regular intervals, regardless of whether the market is up or down. When prices are high, your money buys fewer shares; when prices are low, your money buys more. Over decades, this strategy lowers your average cost per share and removes the emotional stress of volatility.

Harnessing the Dividend Reinvestment Program (DRIP)

Most companies in the S&P 500 pay dividends—a share of their profits sent to shareholders. While you can take this cash and spend it, the path to true wealth lies in a DRIP. By checking a simple box in your brokerage account, those dividends are automatically used to buy more shares of the S&P 500. This creates a powerful compounding effect: your shares produce dividends, which buy more shares, which produce even more dividends. Over a 30-year period, reinvested dividends can account for nearly half of the total return of the S&P 500.

Navigating Risks and the Psychological Game

No investment is without risk. While the S&P 500 has an average annual return of roughly 10% over the last century, that return is rarely “smooth.” There will be years when the index drops by 20% or even 30%.

Managing Market Volatility

Understanding that “volatility is the price of admission” is vital. In the Money niche, we often say that the biggest risk to your portfolio isn’t the market dropping—it’s you panic-selling during the drop. The S&P 500 has recovered from every single crash in its history, including the Great Depression, the 2008 financial crisis, and the 2020 pandemic. Maintaining a long-term horizon (10+ years) is the best way to mitigate the risk of a temporary market downturn.

The Role of Expense Ratios

While you cannot control the market, you can control your costs. Every index fund charges an “expense ratio”—a fee for managing the fund. For a high-quality S&P 500 ETF, this should be incredibly low, often between 0.03% and 0.09%. If you are paying more than 0.20% for an S&P 500 tracker, you are losing thousands of dollars in potential gains over your lifetime to unnecessary fees. Always opt for low-cost institutional funds to ensure more money stays in your pocket.

Conclusion: The Path of Patience

Investing in the S&P 500 is not a “get rich quick” scheme; it is a “get wealthy surely” strategy. By owning the 500 most profitable companies in the United States, you are essentially betting on human ingenuity and the continued growth of the global economy.

To succeed, you must move past the noise of daily financial news and focus on the fundamentals: open a low-cost brokerage account, choose an efficient ETF or mutual fund, automate your contributions through dollar-cost averaging, and reinvest your dividends. If you can master your emotions and stay the course for 20, 30, or 40 years, the S&P 500 remains one of the most reliable engines for financial independence ever created. The best time to start was ten years ago; the second-best time is today.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.