Investing in the S&P 500 is often cited by financial experts, including legendary investor Warren Buffett, as one of the most effective ways for the average person to build significant wealth over time. The Standard & Poor’s 500 Index represents approximately 80% of the total value of the U.S. stock market, tracking the performance of 500 of the largest, most stable companies in the United States. Because it encompasses a broad range of sectors—from technology and healthcare to consumer staples and energy—it serves as a reliable barometer for the overall health of the American economy.

For many investors, the S&P 500 is the “gold standard” of passive investing. It removes the need to pick individual stocks, which can be risky and time-consuming, and instead offers a diversified slice of corporate America. This guide will walk you through the nuances of the S&P 500, the practical steps to start investing, and the strategies required to maximize your returns while managing risk.

1. Decoding the S&P 500 Index

Before putting your hard-earned money into the market, it is essential to understand what the S&P 500 actually is and how it functions. Unlike a simple average of stock prices, the S&P 500 is a market-capitalization-weighted index. This means that companies with higher market values have a greater impact on the index’s performance.

What Makes Up the Index?

To be included in the S&P 500, a company must meet specific criteria set by the S&P Dow Jones Indices. These include a minimum market capitalization, high liquidity, and at least four consecutive quarters of positive earnings. As a result, when you invest in the S&P 500, you are investing in “blue-chip” companies like Apple, Microsoft, Amazon, and Berkshire Hathaway. These are organizations with proven track records and massive global footprints.

Historical Performance and the Power of 10%

Historically, the S&P 500 has delivered an average annual return of approximately 10% before inflation. While the market does not go up in a straight line—experiencing “bear markets” and corrections along the way—the long-term trajectory has been consistently upward. For a “Money” niche investor, this 10% figure is the cornerstone of compound interest. At this rate, an investment traditionally doubles roughly every seven to ten years, making it a potent tool for retirement planning.

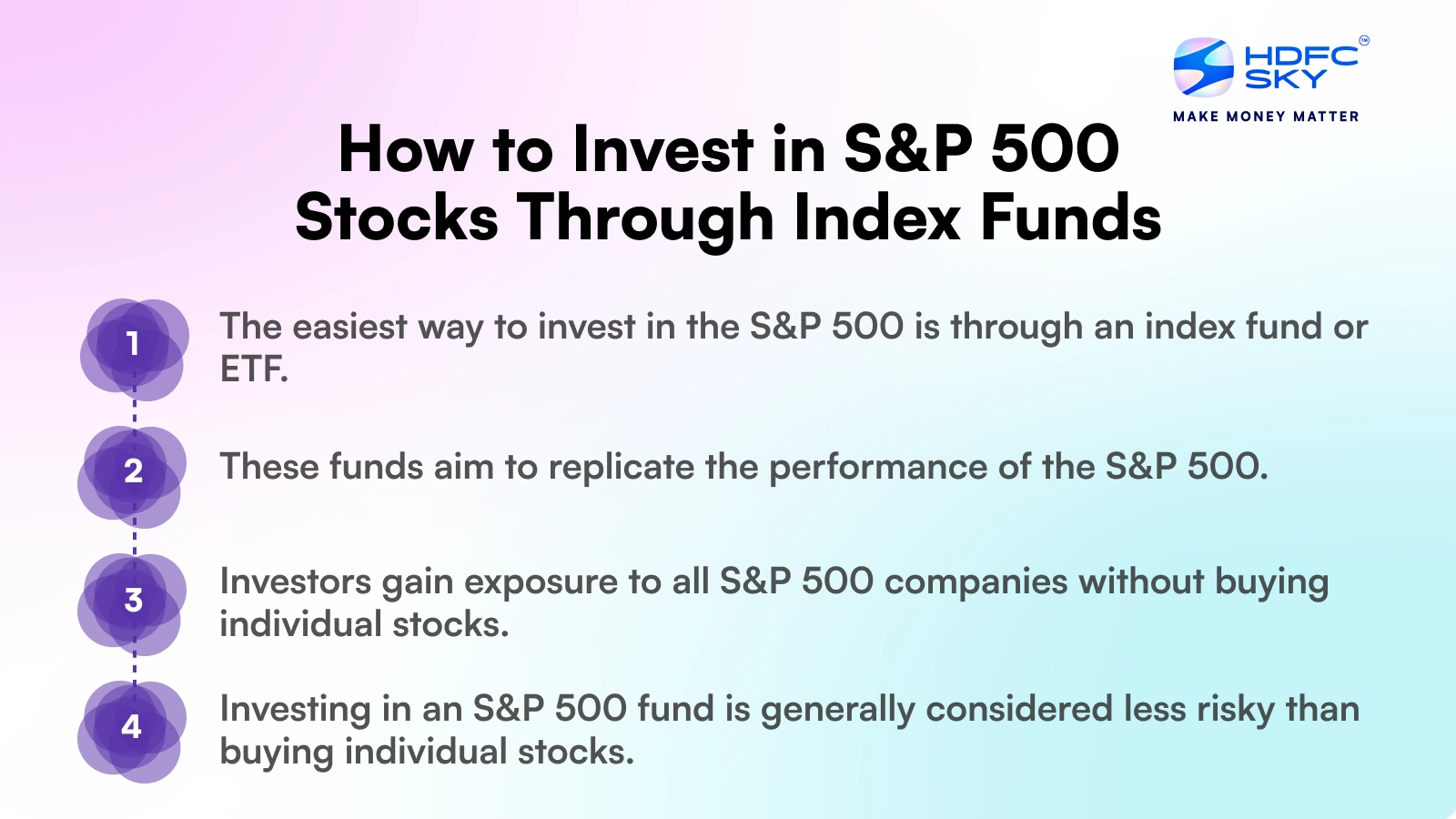

2. The Practical Roadmap: How to Start Investing

You cannot “buy” the S&P 500 index itself because it is merely a mathematical list. Instead, you must invest in a financial product that mimics the index. Here is the step-by-step process to get started.

Selecting a Brokerage Platform

The first step is opening a brokerage account. In the modern financial landscape, you have a plethora of options ranging from traditional powerhouses like Fidelity, Vanguard, and Charles Schwab to user-friendly fintech apps like Robinhood or Betterment. When choosing a broker, look for “zero-commission” trading on stocks and ETFs, a clean user interface, and robust educational resources.

Opening and Funding Your Account

Once you have chosen a broker, you will need to decide on the type of account.

- Individual Taxable Account: Offers the most flexibility, allowing you to withdraw money at any time, though you will owe taxes on capital gains and dividends.

- IRA or 401(k): These are tax-advantaged retirement accounts. Investing in the S&P 500 through a Roth IRA, for example, allows your investments to grow tax-free, which can save you hundreds of thousands of dollars in the long run.

After opening the account, link your bank and transfer the funds you intend to invest.

Executing the Trade

Once your account is funded, you will search for the “ticker symbol” of the S&P 500 fund you wish to buy (such as VOO or SPY). You can place a “Market Order,” which buys the shares immediately at the current price, or a “Limit Order,” which only buys if the price hits a specific target you set. For long-term investors, market orders are generally sufficient.

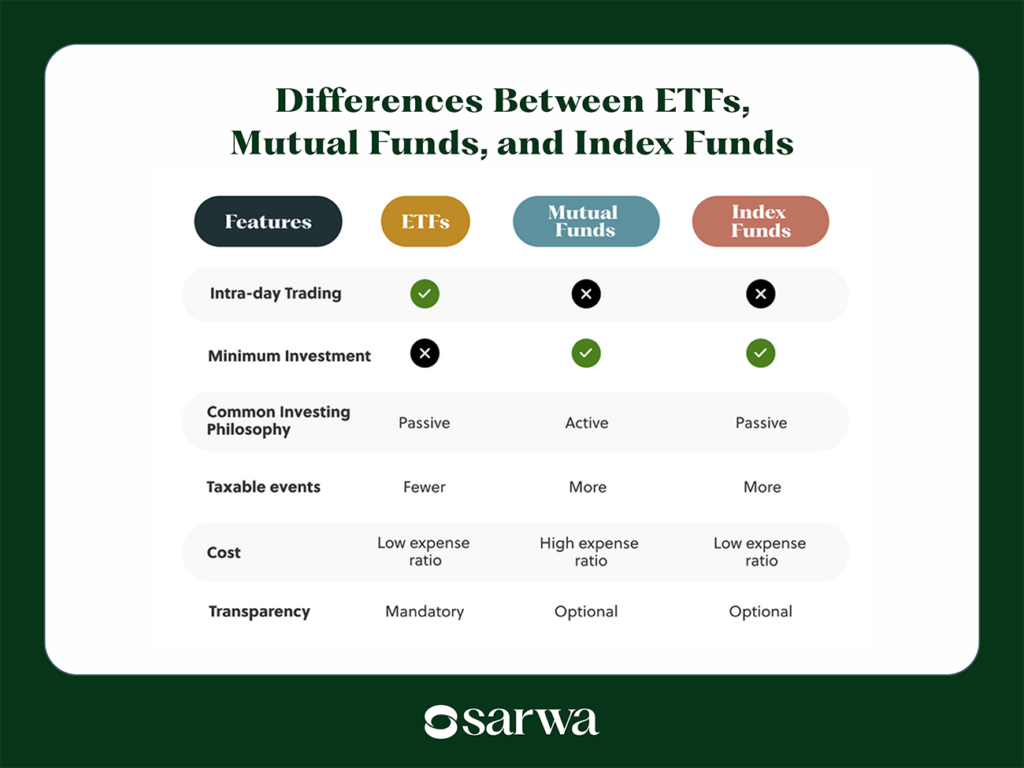

3. Index Funds vs. ETFs: Choosing Your Vehicle

There are two primary ways to track the S&P 500: Mutual Funds (Index Funds) and Exchange-Traded Funds (ETFs). While they both achieve the same goal of diversification, they operate differently.

S&P 500 Mutual Funds (Index Funds)

An index mutual fund is a pool of money managed by an investment firm to track the S&P 500. These funds are priced only once a day at the end of the trading session.

- Pros: They often allow for automatic investment (e.g., $500 every month), and you can buy fractional shares easily.

- Cons: Some may have higher “minimum initial investments” (e.g., $3,000).

S&P 500 Exchange-Traded Funds (ETFs)

ETFs are currently the most popular way to invest in the index. They trade on the stock exchange just like individual stocks, meaning their price fluctuates throughout the day.

- Popular Tickers: Vanguard S&P 500 ETF (VOO), iShares Core S&P 500 ETF (IVV), and SPDR S&P 500 ETF Trust (SPY).

- Pros: ETFs are generally more tax-efficient than mutual funds and have no minimum investment other than the price of a single share (and many brokers now allow fractional shares of ETFs as well).

4. Key Metrics to Consider Before You Buy

Not all S&P 500 funds are created equal. Even though they track the same 500 companies, the underlying costs and management style can impact your final net worth.

Expense Ratios and Fees

The “expense ratio” is the annual fee you pay the fund manager to run the fund. It is expressed as a percentage. For example, the Vanguard S&P 500 ETF (VOO) has an expense ratio of 0.03%. This means for every $10,000 you invest, you only pay $3 a year in fees. In the world of finance, high fees are the enemy of growth. Always look for funds with an expense ratio below 0.10%.

Dividend Reinvestment Plans (DRIP)

Most companies in the S&P 500 pay dividends—a portion of their profits distributed to shareholders. To maximize wealth, you should set your brokerage account to “DRIP.” This automatically uses your dividend payments to buy more shares of the fund. Over decades, dividend reinvestment can account for nearly half of the total returns of the S&P 500.

Tracking Error

A tracking error measures how closely a fund follows the actual S&P 500 index. While most major funds from firms like BlackRock or Vanguard have negligible tracking errors, it is a metric worth checking to ensure the fund manager is accurately reflecting the index’s movements.

5. Strategic Approaches to Index Investing

Simply buying the S&P 500 is a great start, but how you manage that investment over time will determine your ultimate success.

Dollar-Cost Averaging (DCA)

The stock market is volatile. Trying to “time the market” by waiting for a crash often leads to missed opportunities. Instead, many successful investors use Dollar-Cost Averaging. This involves investing a fixed amount of money at regular intervals (e.g., $200 every payday), regardless of whether the market is up or down. This strategy lowers your average cost per share over time and removes the emotional stress of market fluctuations.

The Importance of Time Horizon

The S&P 500 is not a short-term trading vehicle; it is a long-term wealth builder. If you need your money in less than five years, the volatility of the stock market might make the S&P 500 a risky choice. However, if your time horizon is 10, 20, or 30 years, the probability of losing money in the S&P 500 has historically been near zero. Patience is the most valuable asset in personal finance.

Managing Risk and Volatility

While the S&P 500 is diversified, it is still 100% equities (stocks). This means that during a recession, the index can drop by 20%, 30%, or even more. To manage this risk, seasoned investors often pair their S&P 500 holdings with other asset classes, such as bonds or international stocks, to create a balanced portfolio. However, for young investors with a long road to retirement, a heavy concentration in the S&P 500 is often viewed as an acceptable risk for the higher potential reward.

In conclusion, investing in the S&P 500 is a fundamental strategy for anyone serious about their financial future. By choosing a low-cost ETF or index fund, consistently contributing through dollar-cost averaging, and reinvesting your dividends, you are positioning yourself to benefit from the growth of the world’s most powerful companies. It is a simple, effective, and time-tested path to financial independence.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.