When it comes to securing a comfortable retirement, few financial vehicles offer the potent combination of tax efficiency and flexibility that the Roth IRA provides. Named after Senator William Roth and established as part of the Taxpayer Relief Act of 1997, this individual retirement account has become a cornerstone of modern personal finance. Unlike a Traditional IRA, where contributions are often tax-deductible but withdrawals are taxed, the Roth IRA flips the script: you contribute post-tax dollars today in exchange for tax-free growth and tax-free withdrawals in the future.

Navigating the nuances of a Roth IRA requires more than just opening an account; it requires a strategic approach to selection, funding, and asset allocation. This guide will walk you through the essential steps to mastering your Roth IRA.

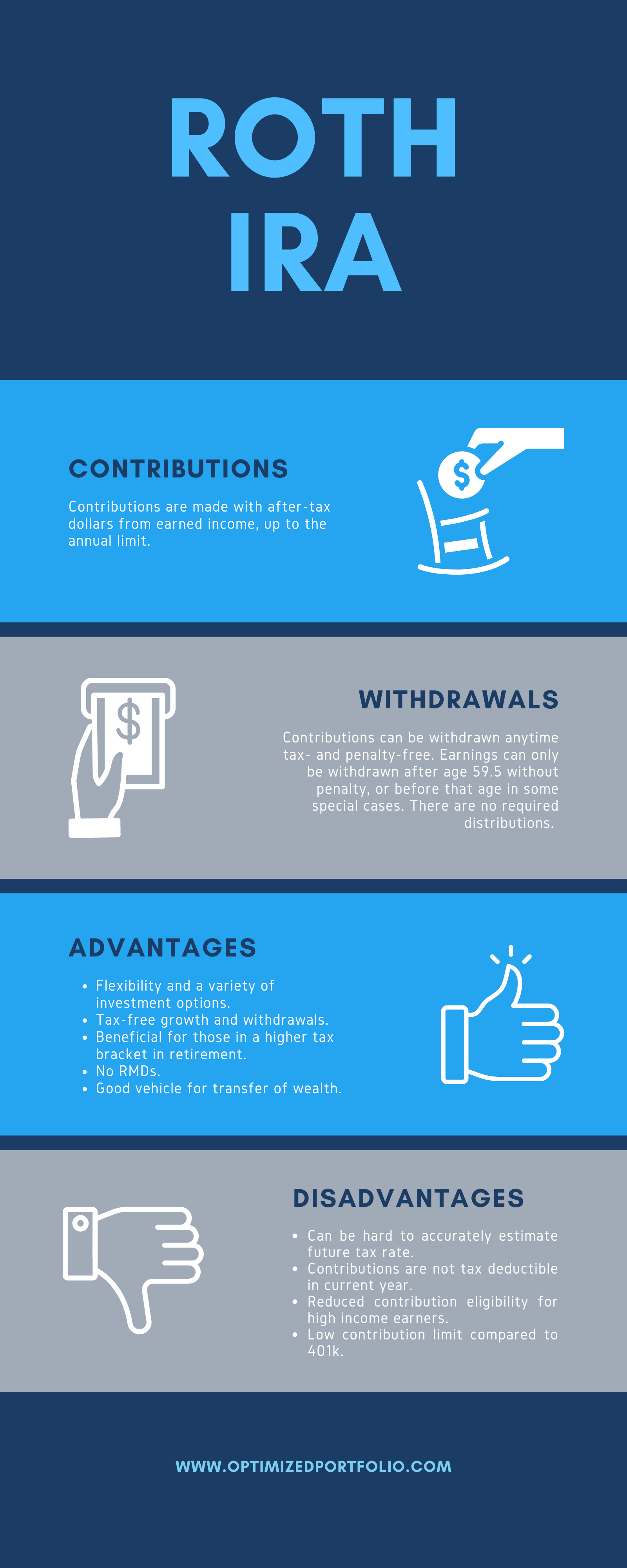

1. Understanding the Core Advantages of the Roth IRA

Before putting your money to work, it is vital to understand why the Roth IRA is often considered the “gold standard” of retirement accounts. Its unique structure offers benefits that go far beyond simple savings.

The Power of Tax-Free Growth

In a standard brokerage account, you are subject to capital gains taxes every time you sell an asset for a profit. In a Roth IRA, your investments grow behind a “tax shield.” Whether your portfolio doubles, triples, or grows tenfold over thirty years, the Internal Revenue Service (IRS) cannot touch a single penny of those gains, provided you follow the qualified distribution rules. For young investors, this translates to decades of compounding interest that remains entirely in their pocket.

Flexibility and Accessibility

One of the most common fears regarding retirement accounts is the “locking up” of capital. The Roth IRA mitigates this concern significantly. Because you have already paid taxes on your contributions, the IRS allows you to withdraw the principal (the original money you put in) at any time, for any reason, without taxes or penalties. While it is generally advised to leave your retirement funds untouched to benefit from compounding, this liquidity serves as a powerful secondary emergency fund.

No Required Minimum Distributions (RMDs)

Unlike Traditional IRAs and 401(k)s, Roth IRAs do not require you to take distributions during your lifetime. This means if you do not need the money for living expenses, you can allow the account to continue growing tax-free indefinitely. This makes the Roth IRA an exceptional tool for estate planning, allowing you to pass on a tax-free windfall to your heirs.

2. Setting Up Your Account: The On-Ramping Process

The first practical step in your Roth IRA journey is choosing where your account will live. Not all platforms are created equal, and your choice of brokerage can impact your long-term returns through fees and available tools.

Selecting the Right Brokerage

In the modern financial landscape, you have three primary options:

- Discount Brokerages: Giants like Vanguard, Fidelity, and Charles Schwab are industry favorites. They offer zero-commission trades, low-cost index funds, and robust research tools.

- Robo-Advisors: Platforms like Betterment or Wealthfront are ideal for investors who prefer a “set it and forget it” approach. They use algorithms to manage your portfolio for a small annual fee.

- App-Based Platforms: Newer fintech apps like Robinhood or M1 Finance offer sleek interfaces and fractional shares, making them attractive to younger, tech-savvy investors.

The Application and Funding Process

Opening a Roth IRA is as simple as opening a checking account. You will need your Social Security Number, employment information, and bank details. Once the account is open, the most critical step—often missed by beginners—is moving money into the account. You can set up a one-time transfer or, more effectively, an automated recurring transfer from your bank. Remember: simply putting money into the account is not the same as “investing.” The money will sit as “cash” or in a “money market fund” until you manually select investments.

Navigating Contribution Limits

For the 2024 tax year, the contribution limit is $7,000 for those under age 50, and $8,000 for those 50 and older (the “catch-up” contribution). It is important to note that you must have “earned income” to contribute. If you earn less than the limit, you can only contribute up to the amount you earned. For example, if a teenager earns $3,000 at a summer job, their maximum Roth IRA contribution is $3,000.

3. Developing an Investment Strategy Within the Roth IRA

Once your account is funded, the real work begins. Because a Roth IRA is a “tax-advantaged bucket,” you want to fill it with assets that have high growth potential.

Asset Allocation and Risk Tolerance

Your investment choices should be dictated by your “time horizon”—the number of years until you plan to retire.

- Aggressive Growth (20s and 30s): At this stage, your focus should be on equities (stocks). Since you have decades to weather market volatility, a portfolio heavy in diversified stock funds can maximize the tax-free growth benefit.

- Moderate Growth (40s and 50s): As you approach retirement, you may choose to introduce bonds or fixed-income assets to reduce volatility, though many maintain a high stock allocation within their Roth specifically because of its tax-free status.

The Role of Low-Cost Index Funds and ETFs

For the vast majority of investors, picking individual stocks is a losing game. Instead, focusing on Exchange-Traded Funds (ETFs) or Mutual Funds that track the entire market is a proven strategy.

- Total Stock Market Index Funds: These provide exposure to every publicly traded company in the U.S.

- S&P 500 Funds: These focus on the 500 largest U.S. companies and have historically returned about 10% annually over long periods.

- International Funds: These provide diversification by investing in companies outside the U.S., protecting you against a domestic economic downturn.

Target Date Funds: The Simplified Path

If the idea of balancing different funds feels overwhelming, a Target Date Fund (TDF) is an excellent solution. You choose the fund with the year closest to your expected retirement (e.g., “Target 2060”). The fund automatically adjusts its holdings from aggressive to conservative as you get older. This ensures professional management without the need for constant manual rebalancing.

4. Understanding Income Limits and the “Backdoor” Strategy

While the Roth IRA is a fantastic tool, it is not available to everyone through traditional means. The IRS sets income thresholds that determine who can contribute directly to a Roth IRA.

Modified Adjusted Gross Income (MAGI) Thresholds

In 2024, if you are a single filer with a MAGI above $161,000, or a married couple filing jointly with a MAGI above $240,000, you are ineligible to contribute directly to a Roth IRA. Between certain ranges (the “phase-out” range), your allowed contribution amount gradually decreases. It is essential to monitor your income annually to ensure you do not over-contribute and trigger IRS penalties.

The Backdoor Roth IRA Explained

For high earners who exceed the income limits, the “Backdoor Roth IRA” is a perfectly legal strategy to get money into a Roth account. The process involves:

- Contributing post-tax money to a Traditional IRA (which has no income limits for contributions).

- Immediately converting that Traditional IRA into a Roth IRA.

Because you didn’t take a tax deduction on the Traditional IRA contribution, and the money hasn’t had time to grow, the conversion typically triggers little to no tax liability. This allows high-income professionals to still benefit from the Roth’s tax-free growth.

Pro-Rata Rules and Tax Implications

When performing a Backdoor Roth conversion, you must be aware of the “Pro-Rata Rule.” If you already have existing pre-tax money in other Traditional IRAs, the IRS views all your IRAs as one entity. This means you cannot just convert the post-tax money; you must convert a proportional amount of pre-tax and post-tax money, which could lead to an unexpected tax bill. Consulting a tax professional is highly recommended for high-earning investors.

5. Maximizing Long-Term Success Through Discipline

Investing in a Roth IRA is a marathon, not a sprint. The greatest threat to your retirement security is often not market performance, but human behavior.

The Importance of Consistency and Automation

Market timing is a fool’s errand. The most successful Roth IRA investors use a strategy called “dollar-cost averaging.” By setting up a monthly contribution, you buy more shares when prices are low and fewer shares when prices are high. Over time, this lowers your average cost per share and removes the emotional stress of trying to “buy the dip.”

Periodic Rebalancing

Over time, certain sectors of your portfolio will outperform others, causing your asset allocation to drift. For example, if your goal was 80% stocks and 20% bonds, a great year in the stock market might push your allocation to 90/10. Rebalancing involves selling some of the “winners” and buying more of the “underperformers” to return to your target risk level. Within a Roth IRA, this rebalancing is tax-free, making it the perfect environment for active portfolio management.

Staying the Course During Volatility

The market will inevitably crash. During these periods, the headlines will be frightening, and your account balance will drop. However, history shows that the market has a 100% recovery rate over long durations. Because the Roth IRA is a long-term vehicle, short-term fluctuations are irrelevant. Maintaining your contribution schedule during a bear market is often when the most significant wealth is built, as you are essentially buying assets at a “discounted” price.

By understanding the tax advantages, selecting a low-cost brokerage, implementing a diversified investment strategy, and maintaining disciplined contribution habits, you turn the Roth IRA from a mere savings account into a powerful engine for generational wealth. The best time to start was yesterday; the second best time is today.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.