Securing a home loan is one of the most significant financial decisions many individuals and families will ever make. While the excitement of homeownership is palpable, the terms of your mortgage — particularly the interest rate — will profoundly impact your financial well-being for decades. A seemingly small difference in interest rate can translate into tens of thousands, or even hundreds of thousands, of dollars over the life of a 15-year or 30-year loan. Therefore, understanding how to navigate the complex world of mortgage lending to secure the most favorable rate is not just prudent; it’s financially imperative.

This comprehensive guide will demystify the process, offering insights into the factors that influence your home loan rate, practical steps to prepare for your application, and strategies for effectively comparing and negotiating offers. By equipping yourself with this knowledge, you can approach the home buying journey with confidence, ensuring you secure not just a house, but a financially sound future.

The Foundation: Understanding What Shapes Your Rate

Before you even begin shopping for a loan, it’s crucial to understand the fundamental elements that lenders assess when determining your eligibility and, more importantly, your interest rate. These factors paint a picture of your financial health and perceived risk.

Your Credit Score: The Ultimate Indicator

At the top of the list is your credit score, predominantly the FICO score. This three-digit number is a powerful summary of your creditworthiness, derived from your payment history, amounts owed, length of credit history, new credit, and credit mix. Lenders use it as a primary indicator of how reliably you’ve managed debt in the past and, by extension, how likely you are to repay your mortgage.

Borrowers with excellent credit scores (generally 760 and above) are seen as low-risk, consistently qualifying for the lowest interest rates. Conversely, a lower credit score signals higher risk to lenders, often resulting in higher interest rates to compensate for that perceived risk. Improving your credit score by making timely payments, reducing outstanding balances, and avoiding new debt is arguably the most impactful step you can take to secure a better rate.

Debt-to-Income Ratio (DTI): A Measure of Your Capacity

Your debt-to-income (DTI) ratio is another critical metric that lenders scrutinize. It represents the percentage of your gross monthly income that goes towards servicing your monthly debt payments. There are two types: front-end DTI (housing costs only) and back-end DTI (all monthly debt payments, including housing).

Lenders typically prefer a back-end DTI of 36% or lower, though some programs may allow up to 43-50%. A lower DTI indicates that you have ample disposable income to comfortably make your mortgage payments, even if unexpected expenses arise. A high DTI suggests you might be overextended, making you a riskier borrower and potentially leading to a higher rate or even loan denial. Strategies to lower your DTI include paying off existing debts, increasing your income, or a combination of both.

Down Payment Size: More Equity, Less Risk

The size of your down payment significantly influences both your loan approval and your interest rate. A larger down payment reduces the amount you need to borrow, thus decreasing the lender’s risk exposure. When you have more equity in the home from the start, you’re less likely to default on the loan, as you have more to lose.

While a 20% down payment has long been the gold standard, offering benefits like avoiding Private Mortgage Insurance (PMI), even putting down more than 20% can sometimes shave basis points off your interest rate. Lenders often offer better rates to borrowers who demonstrate stronger financial commitment and a lower loan-to-value (LTV) ratio. Moreover, a larger down payment gives you more flexibility in loan product choices and can lead to lower monthly payments overall.

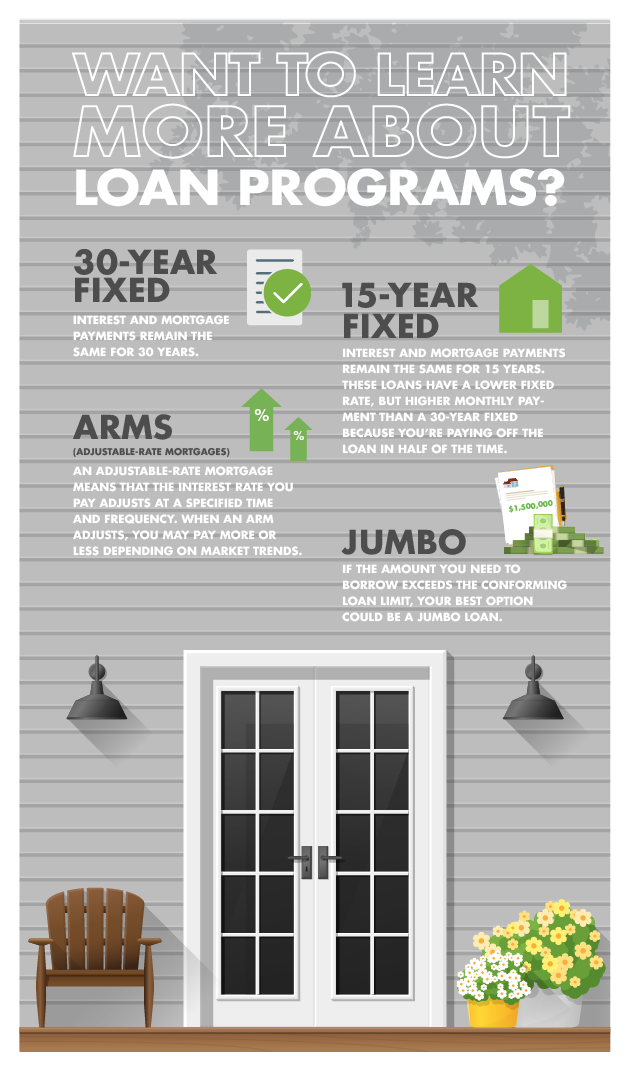

Loan Type and Term: Fixed vs. Adjustable, 15 vs. 30 Years

The type of loan you choose also directly impacts the rate. Common options include:

- Conventional Loans: Backed by private lenders, conforming to Fannie Mae and Freddie Mac guidelines. Rates vary based on credit and down payment.

- FHA Loans: Insured by the Federal Housing Administration, ideal for borrowers with lower credit scores or smaller down payments (as low as 3.5%). These often come with mortgage insurance premiums (MIP) for the life of the loan.

- VA Loans: Guaranteed by the Department of Veterans Affairs for eligible service members and veterans. These often offer competitive rates, no down payment requirements, and no PMI.

- USDA Loans: For rural properties, guaranteed by the U.S. Department of Agriculture. Zero down payment loans available to eligible low-to-moderate income borrowers.

Beyond the loan type, the loan term (e.g., 15-year vs. 30-year) also affects rates. Generally, 15-year mortgages carry lower interest rates than 30-year mortgages because the lender’s money is tied up for a shorter period, reducing their long-term risk. However, the trade-off is higher monthly payments. Similarly, fixed-rate mortgages, where the interest rate remains constant, offer predictability but might have slightly higher initial rates than adjustable-rate mortgages (ARMs), which have introductory fixed rates followed by periodic adjustments. ARMs carry the risk of rate increases in the future, making them suitable for specific financial situations.

Strategic Preparation: Setting Yourself Up for Success

Once you understand the key drivers of your home loan rate, the next step is proactive preparation. Taking these steps well in advance of your loan application can significantly improve your position.

Reviewing and Improving Your Credit Report

Before applying for a loan, obtain free copies of your credit reports from all three major bureaus (Equifax, Experian, TransUnion) via AnnualCreditReport.com. Scrutinize them for any errors, fraudulent activity, or outdated information that could be dragging down your score. Disputing errors promptly can lead to a quick score increase. Beyond error correction, focus on consistent on-time payments, keeping credit utilization below 30% (ideally below 10%), and avoiding opening new lines of credit unnecessarily.

Saving for a Substantial Down Payment

Start saving early and aggressively for your down payment. As discussed, a larger down payment can unlock better rates, reduce your monthly payments, and potentially eliminate PMI. Explore various savings strategies, such as setting up automated transfers to a dedicated savings account, cutting discretionary spending, or even considering a side hustle to accelerate your savings. Aim for at least 5-10% if 20% is out of reach, but always strive for more if possible.

Reducing Existing Debts

Prioritize paying down high-interest consumer debts like credit card balances or personal loans. Reducing these not only frees up monthly cash flow but also lowers your DTI, making you a more attractive borrower. Consider debt snowball or debt avalanche methods to tackle your debts efficiently. Even small reductions can make a difference in your DTI and overall financial profile.

Document Gathering and Organization

Lenders require a substantial amount of documentation to verify your income, assets, and liabilities. This includes pay stubs, W-2s, tax returns (typically the last two years), bank statements, investment account statements, and details on any existing debts. Gather and organize these documents in advance to streamline the application process. A well-prepared applicant signals responsibility and can expedite approval, preventing delays that could impact rate lock availability.

The Comparison Game: Shopping for Your Best Rate

With your financial house in order, it’s time to actively seek out the best loan. This isn’t a one-and-done process; comparing offers is where many borrowers secure significant savings.

Getting Quotes from Multiple Lenders

This is perhaps the most crucial step in getting the best rate. Do not settle for the first offer you receive, or even just one or two. Apply with at least three to five different lenders within a short window (typically 14-45 days, depending on the credit scoring model, to minimize the impact on your credit score). Lenders include:

- Large National Banks: Often have extensive product offerings but can sometimes be less flexible.

- Local Banks and Credit Unions: May offer more personalized service and competitive rates for their members.

- Online Lenders: Known for efficiency and often very competitive rates due to lower overheads.

- Mortgage Brokers: Act as intermediaries, working with multiple lenders to find you the best deal.

Each lender will have different rate structures, fees, and underwriting guidelines. Shopping around allows you to see the full spectrum of options available to you based on your unique financial profile.

Understanding Loan Estimates (LEs)

Once you apply, lenders are required to provide a Loan Estimate (LE) within three business days. This standardized three-page document details your interest rate, monthly payment, estimated closing costs, and other key loan terms. It’s designed to make direct comparisons between offers straightforward. Pay close attention to:

- Interest Rate vs. APR: The interest rate is what you pay on the principal. The Annual Percentage Rate (APR) represents the total cost of the loan, including the interest rate and most fees, expressed as a yearly percentage. APR is often a better measure for true cost comparison.

- Origination Fees: Fees charged by the lender for processing your loan.

- Third-Party Fees: Costs for appraisals, title insurance, credit reports, etc.

- Prepayment Penalties: Though less common now, ensure your loan doesn’t have them.

- Rate Lock Period: How long the quoted rate is guaranteed.

Compare line by line across all your LEs to identify the best overall deal, not just the lowest stated interest rate.

Negotiating Your Rate and Terms

Many people don’t realize that mortgage rates and fees can often be negotiated. Once you have multiple LEs, use the best offer as leverage. Go back to other lenders you’re considering and ask if they can beat or match the best rate and terms you’ve received. Be polite but firm. Lenders want your business and may be willing to adjust their offer, especially if you’re a strong candidate. This negotiation isn’t just about the rate; it can also involve reducing origination fees or other closing costs.

Considering Mortgage Brokers vs. Direct Lenders

Deciding between a mortgage broker and a direct lender (like a bank or credit union) is an important consideration.

- Mortgage Brokers: Can be invaluable if you have a complex financial situation, need a specialized loan product, or simply want someone to do the legwork of finding the best rate from multiple wholesale lenders. They can access a wide range of loan products and may find options you wouldn’t discover on your own. Their compensation typically comes from the lender (a “lender-paid” commission) or directly from you (a “borrower-paid” fee).

- Direct Lenders: Offer their own proprietary loan products. Going directly can sometimes simplify the process, as you’re dealing with one institution from application to closing. However, you’re limited to their specific offerings.

Both avenues can lead to great rates, but it’s often beneficial to explore both types of sources during your shopping process.

Beyond the Rate: Hidden Costs and Long-Term Considerations

While the interest rate is paramount, a truly “best” home loan rate also considers the entire financial picture, including upfront costs and future flexibility.

Analyzing APR vs. Interest Rate

Reiterating its importance, the APR provides a more holistic view of the loan’s cost. A loan with a slightly higher interest rate but lower fees might ultimately have a lower APR and be a better deal than a loan with a lower interest rate but higher fees. Always prioritize comparing APRs when evaluating different loan offers, as it helps you understand the true annual cost of borrowing.

Understanding Closing Costs

Closing costs are the fees and expenses you pay when you close on your home loan. These can typically range from 2% to 5% of the loan amount and include items like appraisal fees, title insurance, legal fees, recording fees, and points. While some closing costs are unavoidable, others can be negotiated or shopped for. Being aware of these costs, and having funds set aside for them, ensures there are no surprises at the closing table. Some lenders might offer “no closing cost” loans, but often these simply roll the fees into a higher interest rate, so always evaluate the total cost.

The Impact of Discount Points

Discount points are essentially prepaid interest. One point equals 1% of the loan amount. By paying points upfront at closing, you can “buy down” your interest rate, resulting in lower monthly payments over the life of the loan. Whether buying points makes financial sense depends on how long you plan to stay in the home. Calculate the break-even point: how long it will take for the savings from the lower monthly payment to offset the upfront cost of the points. If you plan to move before reaching that break-even point, paying points might not be advantageous.

Future Refinancing Opportunities

Even if you secure a great rate today, economic conditions can change. Interest rates fluctuate, and your financial situation might improve. Keep an eye on market trends. If rates drop significantly or your credit score improves substantially years down the line, refinancing could be an option to secure an even lower rate. A good loan today doesn’t preclude a better one tomorrow, especially if it helps you save more over your homeownership journey.

In conclusion, obtaining the best home loan rate is not a matter of luck but rather a result of informed decision-making, meticulous preparation, and diligent comparison shopping. By understanding the factors that influence your rate, proactively improving your financial profile, and engaging critically with multiple lenders, you position yourself to secure a mortgage that genuinely supports your long-term financial goals and enhances your homeownership experience. The effort invested upfront will pay dividends for decades to come.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.