A personal loan is one of the most versatile financial tools available to modern consumers. Unlike a mortgage or an auto loan, which are earmarked for specific purchases, a personal loan provides a lump sum of capital that can be used for virtually any purpose—from consolidating high-interest credit card debt and financing home renovations to covering unexpected medical expenses. However, the ease of access to these funds does not mean the process should be taken lightly. Obtaining a personal loan requires a strategic approach to ensure you receive the most favorable terms and interest rates possible.

In this guide, we will explore the intricacies of the personal loan market, the criteria lenders use to evaluate your creditworthiness, and a step-by-step roadmap to navigating the application process with confidence and financial savvy.

Understanding the Fundamentals of Personal Loans

Before diving into the application process, it is essential to understand exactly what a personal loan is and how it functions within the broader ecosystem of personal finance. Personal loans are typically installment loans, meaning you borrow a fixed amount and pay it back with interest in monthly installments over a predetermined period, usually ranging from two to seven years.

Secured vs. Unsecured Loans

The majority of personal loans are “unsecured,” meaning they are not backed by collateral such as your home or car. Because the lender takes on more risk with an unsecured loan, interest rates are generally higher than those of secured loans. Conversely, a “secured” personal loan requires an asset to act as collateral. While these often come with lower interest rates, they carry the risk of asset seizure if you default on your payments. Choosing between the two depends heavily on your credit profile and your comfort level with risk.

Fixed vs. Variable Interest Rates

When you secure a personal loan, the interest rate will typically be fixed, meaning your monthly payment remains the same for the life of the loan. This provides predictability for your monthly budgeting. However, some lenders offer variable-rate loans, which may start with a lower interest rate but can fluctuate based on market conditions. In a rising interest rate environment, a fixed-rate loan is almost always the more prudent choice for long-term stability.

The Role of Credit Scores in Loan Approval

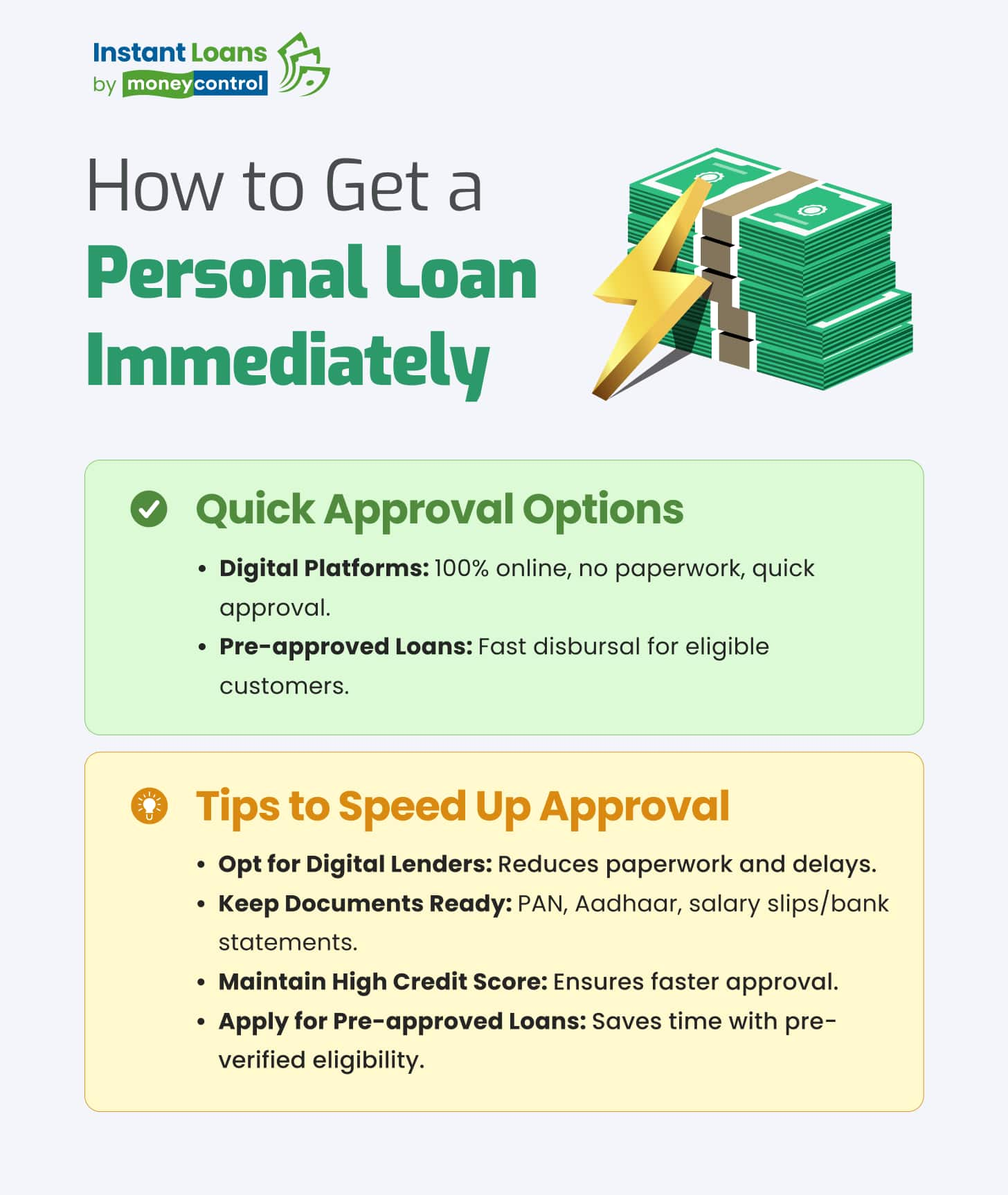

Your credit score is arguably the most significant factor in the personal loan process. It serves as a numerical representation of your reliability as a borrower. Lenders use scores from the major bureaus—Equifax, Experian, and TransUnion—to determine your “risk tier.” Those with “Excellent” credit (720+) often qualify for the lowest rates, while those with “Fair” or “Poor” credit may face significantly higher Annual Percentage Rates (APRs) or may be required to seek out specialized lenders.

Assessing Your Financial Health Before Applying

Preparation is the cornerstone of financial success. Before you approach a lender, you must perform an honest audit of your financial standing. This not only helps you understand what you can afford but also prepares you for the scrutiny your finances will undergo during the underwriting process.

Calculating Your Debt-to-Income (DTI) Ratio

Lenders don’t just look at how much you earn; they look at how much of that income is already committed to other debts. Your Debt-to-Income (DTI) ratio is calculated by dividing your total monthly debt payments by your gross monthly income. Most lenders prefer a DTI ratio below 36%, though some may accept up to 50% for high-income earners. If your DTI is too high, it may be wise to pay down existing balances before applying for new credit.

Reviewing Your Credit Report for Errors

It is surprisingly common for credit reports to contain inaccuracies—such as late payments that were actually on time or accounts that don’t belong to you. Since even a small dip in your score can cost you thousands in interest over the life of a loan, you should pull your credit report from AnnualCreditReport.com at least three months before applying. Disputing errors early ensures your report is in peak condition when a lender reviews it.

Determining the Purpose and Amount Needed

Borrowing more than you need is a common mistake that leads to unnecessary interest expenses. Define exactly what the funds are for. If you are consolidating debt, calculate the exact payoff amounts for your current creditors. If you are doing home repairs, get firm quotes from contractors. By having a precise figure, you demonstrate financial discipline and avoid the temptation of “lifestyle creep” funded by borrowed money.

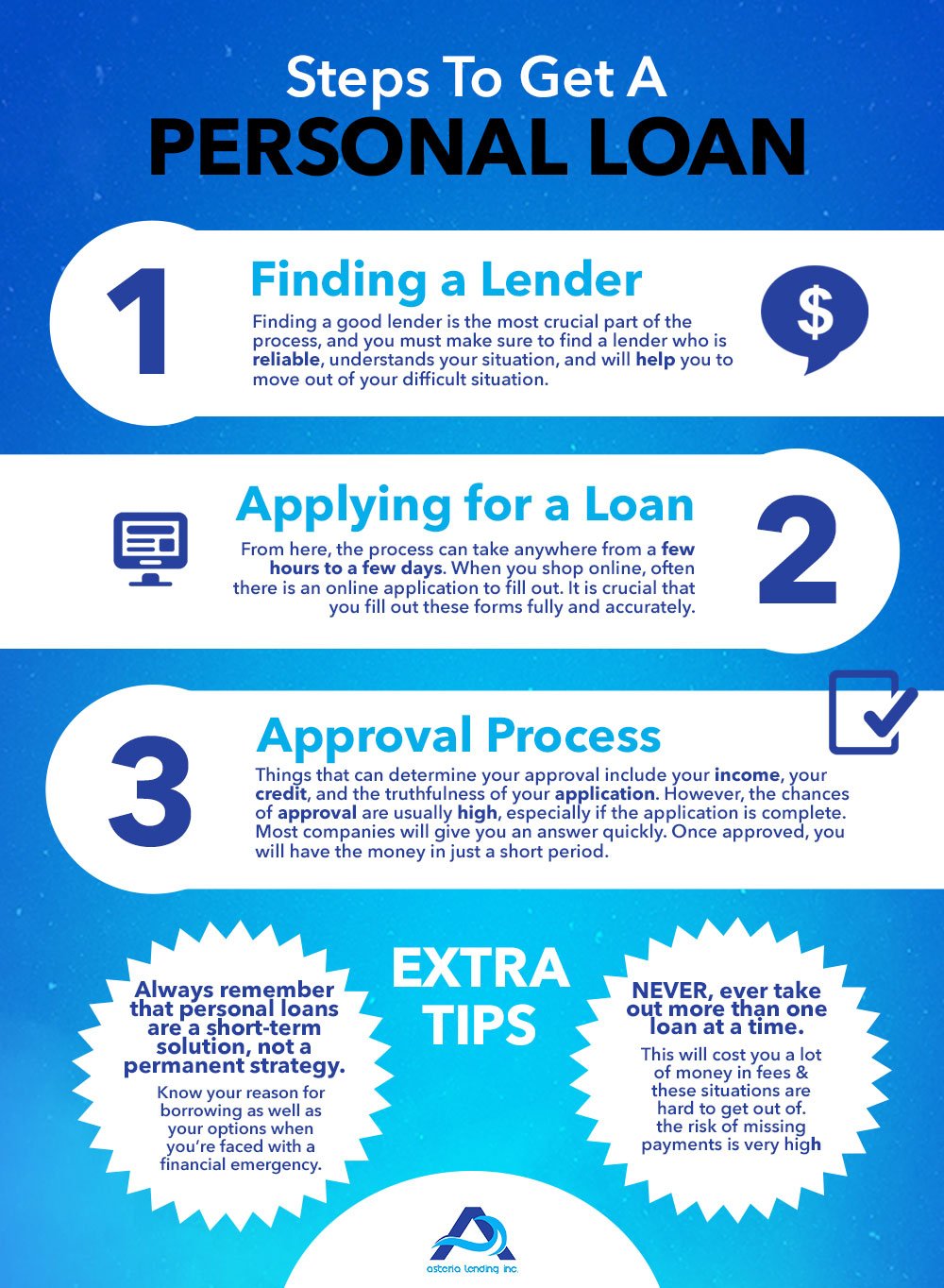

The Step-by-Step Process of Obtaining a Personal Loan

Once you have assessed your financial health, the actual process of getting the loan begins. This journey involves moving from broad research to specific applications.

Comparing Lenders (Banks, Credit Unions, and Online Lenders)

Not all lenders are created equal. Traditional banks often offer the best rates to existing customers with high credit scores. Credit unions, being member-owned, may offer more flexible terms and lower fees for those with average credit. Meanwhile, online lenders (FinTechs) have revolutionized the industry with rapid approval times and highly accessible digital interfaces. It is vital to compare “apples to apples” by looking at the APR, which includes both the interest rate and any fees.

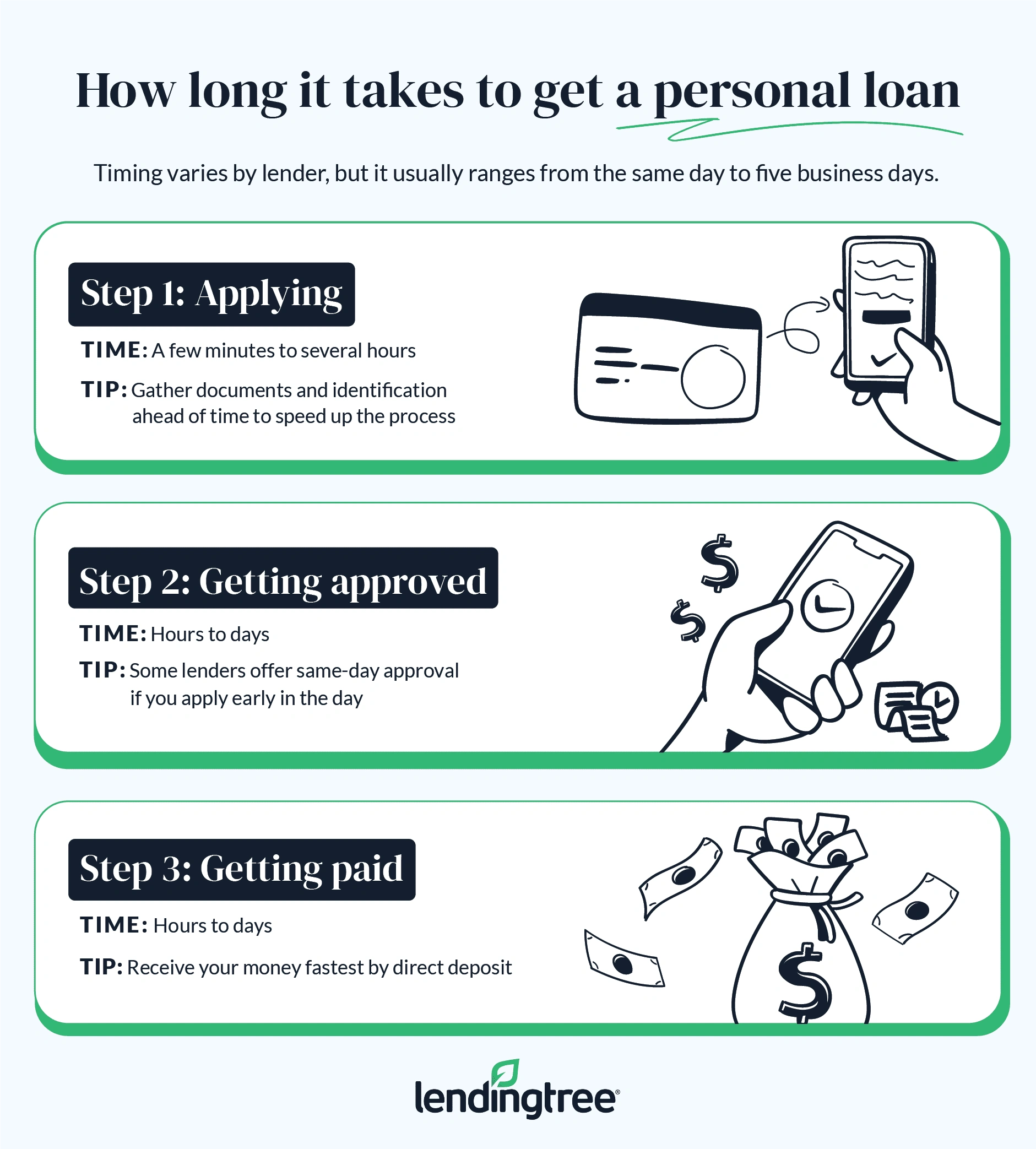

Prequalification and the “Soft” Credit Pull

One of the best features of modern lending is the ability to “prequalify.” This process involves providing basic information to a lender to see what rates you might qualify for. Crucially, prequalification usually involves a “soft” credit pull, which does not impact your credit score. This allows you to shop around and compare offers from multiple lenders without damaging your credit profile.

Submitting a Formal Application and Documentation

After selecting the best offer, you will move to the formal application. This stage requires a “hard” credit pull, which may cause a temporary, slight dip in your credit score. You will need to provide documentation to verify your identity and income. Common requirements include:

- Government-issued ID (Driver’s license or passport).

- Proof of residence (Utility bills or lease agreements).

- Proof of income (W-2s, pay stubs, or tax returns for the self-employed).

- Bank statements to verify cash flow.

Optimizing Your Chances of Approval and Better Terms

If you find that your initial offers are not as favorable as you hoped, there are several levers you can pull to improve the strength of your application.

The Power of a Co-signer

If your credit score is in the “Fair” range, adding a co-signer with excellent credit can drastically improve your chances of approval and lower your interest rate. A co-signer is legally responsible for the debt if you fail to pay, so this requires a high level of trust and a clear understanding of the risks involved for both parties.

Strategies to Boost Your Credit Score Quickly

If you aren’t in a rush, taking 30 to 60 days to optimize your score can pay off. The fastest way to do this is by lowering your “credit utilization ratio”—the amount of credit you are using compared to your total limits. Paying down a credit card balance to below 10% of its limit can result in a rapid score increase as soon as the lender reports the new balance to the bureaus.

Avoiding Common Pitfalls: Origination Fees and Prepayment Penalties

The headline interest rate isn’t the only cost of a loan. Some lenders charge an “origination fee,” which is a percentage of the loan amount deducted before you receive the funds. For example, if you borrow $10,000 with a 5% origination fee, you only receive $9,500 but still owe interest on the full $10,000. Additionally, check for “prepayment penalties.” You want the flexibility to pay the loan off early to save on interest without being penalized for doing so.

Managing Your Loan Post-Approval for Long-Term Success

Getting the money is only the beginning. The final stage of “how to get a personal loan” is successfully managing the debt so that it improves your financial life rather than hindering it.

Automating Payments to Avoid Penalties

The single most important rule of debt management is to never miss a payment. Late payments can stay on your credit report for seven years and cause your score to plummet. Most lenders offer a small interest rate discount (often 0.25%) if you sign up for “autopay.” This ensures your payments are always on time and reduces your total interest cost.

Understanding the Impact on Your Monthly Budget

A personal loan is a fixed monthly obligation. Before the funds hit your account, you should already have a revised budget in place. This may mean cutting back on discretionary spending like dining out or subscriptions to ensure the loan payment is covered. If the loan was used for debt consolidation, it is imperative that you do not run up new balances on the credit cards you just cleared; otherwise, you will end up with twice the debt.

Integrating Loan Repayment into Your Financial Goals

While you are required to make the minimum payment, you are rarely forbidden from paying more. If you receive a tax refund, a bonus at work, or a cash gift, applying it toward the principal of your loan can significantly shorten the repayment period and save you hundreds or thousands of dollars in interest. View your personal loan as a temporary bridge to a better financial state, and work aggressively to cross that bridge as quickly as possible.

By understanding these nuances of the lending world—from credit mechanics to fee structures—you can transform a personal loan from a simple debt into a strategic asset that helps you achieve your most important financial objectives.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.