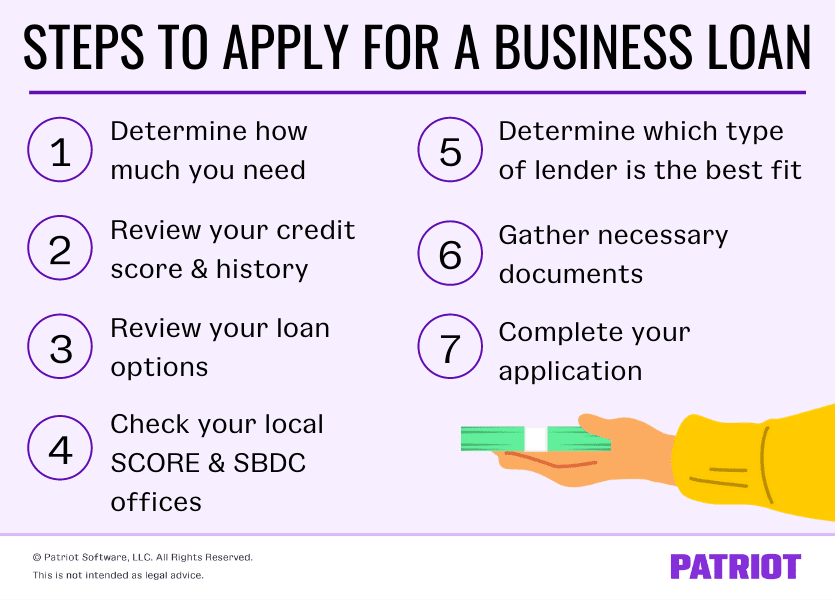

Securing the necessary capital to transform a vision into a functioning enterprise is one of the most significant hurdles an entrepreneur will face. While the landscape of business finance has evolved with the advent of digital lending and alternative financing, the core principles of obtaining a business loan remain rooted in risk assessment, financial stability, and strategic planning. For most startups, a loan is not merely a debt obligation; it is the fuel required to scale operations, purchase inventory, and bridge the gap between initial investment and profitability.

However, the process of obtaining a loan for a brand-new business is notoriously rigorous. Lenders are risk-averse by nature, and startups lack the historical financial data that established corporations use to prove their creditworthiness. To succeed, an entrepreneur must approach the lending process with a high degree of financial literacy and a meticulously prepared application. This guide explores the essential steps to navigating the financial ecosystem and securing the funding necessary to launch your venture.

Strengthening Your Financial Profile Before Applying

Before approaching a lender, you must view your business through their lens. Lenders want to ensure that the money they provide will be repaid with interest. Because a startup has no track record, the lender will heavily scrutinize the personal financial health of the founders.

Personal and Business Credit Scores

In the early stages of a business, your personal credit score is the most critical indicator of your financial responsibility. Most traditional banks and even online lenders require a personal credit score of at least 680, though 720 or higher is preferred for competitive interest rates. If your score is low, take several months to pay down existing debts and correct any errors on your credit report before applying. Simultaneously, you should begin building business credit by registering your business as a legal entity (LLC or Corporation), obtaining an EIN from the IRS, and opening a dedicated business bank account.

The Importance of a Detailed Business Plan

A business plan is not just a roadmap for the entrepreneur; it is a vital financial document for the lender. It must articulate the business model, the target market, the competitive landscape, and, most importantly, the financial projections. Lenders look for “debt service coverage”—a clear indication that the business will generate enough cash flow to cover its operating expenses plus the new loan payments. Your plan should include a break-even analysis and at least three years of projected income statements and balance sheets.

Managing Debt-to-Income Ratios

Lenders will evaluate your Debt-to-Income (DTI) ratio to ensure you are not overleveraged. If you are already carrying significant personal debt (mortgages, student loans, or personal credit lines), a lender may worry that you lack the “financial cushion” to survive a slow start in business. Consolidating high-interest debt or increasing your personal equity stake in the business can make your profile more attractive to financial institutions.

Navigating the Landscape of Small Business Loan Options

Not all loans are created equal. The type of financing you seek should align with your business’s specific needs, your credit profile, and how quickly you need the funds.

SBA 7(a) and Microloan Programs

The U.S. Small Business Administration (SBA) does not lend money directly to entrepreneurs. Instead, it guarantees a portion of loans made by partner banks, reducing the risk for the lender. The SBA 7(a) loan is the most popular option for startups because it offers long repayment terms and relatively low interest rates. For smaller amounts (up to $50,000), the SBA Microloan program is an excellent choice for new businesses, often channeled through non-profit community lenders who provide additional mentorship.

Traditional Commercial Bank Loans

National and community banks offer term loans and lines of credit. These are often the most difficult for startups to secure because banks typically require two years of profitable operation. However, if you have substantial collateral (such as real estate or equipment) and a perfect credit history, a traditional bank can offer the lowest cost of capital. Building a relationship with a local community bank can be advantageous, as they often have a greater interest in supporting local economic development than larger national chains.

Online Lenders and Fintech Solutions

The rise of financial technology (Fintech) has revolutionized business lending. Online lenders offer speed and convenience, often providing a decision within 24 to 48 hours. These loans are more accessible for those with slightly lower credit scores, but they come with a trade-off: higher interest rates and shorter repayment windows. This type of financing is best suited for short-term needs, such as purchasing initial inventory or equipment, rather than long-term foundational capital.

Essential Documentation and the Application Workflow

Once you have identified the right type of loan, the application process requires a high level of organizational discipline. Any missing documentation can result in immediate rejection or significant delays.

Financial Statements and Projections

You must provide personal financial statements for all owners with a 20% or greater stake in the company. This includes a list of assets and liabilities. For the business side, you will need a “Sources and Uses of Funds” statement, which explicitly details how much money you need and exactly what every dollar will be spent on. Lenders are wary of vague requests for “working capital”; they prefer to see specific allocations, such as “$50,000 for manufacturing equipment” and “$20,000 for a six-month lease deposit.”

Legal Documents and Tax Returns

Expect to provide at least two to three years of personal tax returns. If the business has already begun limited operations, business tax returns are also required. Additionally, you will need to provide legal documents such as your Articles of Incorporation, business licenses, and any existing contracts or leases. These documents prove that your business is a legitimate entity and that you have the legal right to operate in your chosen industry and location.

Identifying and Valuing Collateral

Most startup loans are “secured,” meaning you must pledge assets that the lender can seize if you default on the loan. Collateral can include business assets (inventory, equipment, accounts receivable) or personal assets (home equity, vehicles). Providing collateral significantly increases your chances of approval and can help you secure a lower interest rate. If you lack physical collateral, you may be required to provide a “personal guarantee,” which legally binds your personal assets to the repayment of the business debt.

Understanding the “5 Cs” of Credit for Business Success

Lenders often use a framework known as the “5 Cs” to evaluate a loan application. Understanding these five dimensions can help you tailor your pitch and your documentation to address the lender’s primary concerns.

Character and Capacity

Character refers to the borrower’s reputation and track record. This is where your credit score, professional experience, and references come into play. Lenders want to know that you are a person of integrity who takes financial obligations seriously. Capacity measures your ability to repay the loan. The lender will look at your projected cash flow to determine if the business can realistically handle the monthly payments after all other expenses are paid.

Capital, Conditions, and Collateral

Capital refers to the amount of your own money you have invested in the business. Lenders are hesitant to take 100% of the risk; they want to see that you have “skin in the game.” Usually, an equity contribution of 10% to 20% is expected. Conditions involve external factors, such as the state of the economy, industry trends, and the specific purpose of the loan. For example, it might be easier to get a loan for a healthcare startup than for a luxury retail store during a recession. Finally, Collateral, as discussed previously, acts as a secondary source of repayment, providing a safety net for the lender.

Conclusion: Orchestrating a Successful Financial Launch

Getting a loan to start a business is rarely an overnight achievement. It is the culmination of months of financial preparation, strategic planning, and rigorous documentation. By understanding the different lending tiers—from SBA-guaranteed loans to high-speed Fintech options—entrepreneurs can choose the path that best fits their risk profile and operational needs.

The key to success lies in transparency and preparation. By maintaining a strong personal credit score, crafting a data-driven business plan, and understanding the “5 Cs” of credit, you position yourself as a low-risk, high-potential candidate for investment. While the burden of debt must be managed carefully, a well-structured business loan provides the essential leverage needed to turn an entrepreneurial dream into a sustainable, profitable reality. Focus on building a solid financial foundation today, and the capital required for tomorrow’s growth will follow.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.