Securing a business loan is a pivotal step for many entrepreneurs looking to launch, expand, or stabilize their operations. Whether you’re a startup in need of seed capital, an established enterprise planning a significant expansion, or a small business navigating a challenging economic period, understanding the landscape of business financing is crucial. The process can seem daunting, but with meticulous preparation and a clear strategy, accessing the necessary capital becomes a manageable and achievable goal.

Understanding Your Business Loan Needs

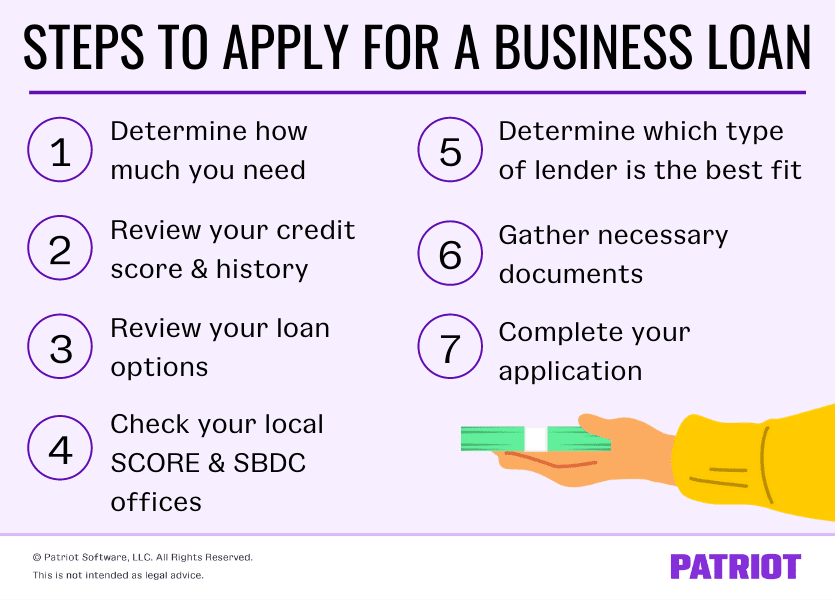

Before approaching any lender, a thorough self-assessment is paramount. Knowing precisely why you need capital and how much you require will streamline the application process and increase your chances of approval. Lenders are more inclined to support businesses with a clear vision and a robust financial understanding.

Assessing Your Financial Position

Begin by evaluating your current financial health. This involves a deep dive into your existing assets, liabilities, revenue, and expenses. Key documents like your balance sheet, profit and loss statement, and cash flow statement will provide a snapshot of your business’s financial standing. Understand your debt-to-equity ratio, liquidity, and profitability metrics. Lenders will scrutinize these figures to gauge your ability to manage and repay new debt. A strong financial history, even for a nascent business, demonstrates responsibility and potential. For startups, personal financial strength, including personal credit scores and assets, often plays a larger role in initial assessments.

Defining the Loan Purpose

Lenders want to know exactly what the funds will be used for. Is it for purchasing new equipment, expanding inventory, hiring more staff, funding marketing campaigns, or covering operational gaps? Clearly articulating the loan’s purpose demonstrates foresight and a strategic approach. Specificity is key; instead of saying “for growth,” specify “to purchase a new CNC machine that will increase production capacity by 30% and reduce per-unit cost by 15%.” This not only justifies the loan but also provides a measurable impact for the lender to evaluate. The purpose often dictates the type of loan best suited for your business.

Determining the Right Loan Amount

Over-borrowing can lead to unnecessary interest payments, while under-borrowing can leave you short of your objectives, potentially necessitating another loan sooner than expected. Create a detailed budget outlining all expenditures the loan will cover, adding a contingency fund (typically 10-20%) for unforeseen costs. Be realistic about future revenue projections that will support repayment. Using financial modeling to project cash flow with the new capital can help pinpoint the optimal loan amount, ensuring you cover your needs without overburdening your business.

Types of Business Loans Available

The financing landscape is diverse, offering a range of products tailored to different business needs and profiles. Understanding these options is critical to selecting the most appropriate funding source.

Traditional Bank Loans

These are often considered the gold standard due to their competitive interest rates and structured repayment terms.

- SBA Loans: Backed by the U.S. Small Business Administration, these loans reduce risk for lenders, making it easier for small businesses to qualify. They often feature lower down payments, flexible overhead requirements, and longer repayment periods. They come in various forms, such as 7(a) loans (for general purposes), 504 loans (for real estate and equipment), and microloans.

- Term Loans: A lump sum of capital is provided upfront and repaid with fixed interest over a set period. These are suitable for significant, one-time investments like equipment purchases or facility expansions.

- Lines of Credit: Similar to a credit card, a business line of credit provides access to a revolving pool of funds up to a certain limit. Businesses can draw from it as needed and only pay interest on the amount borrowed. Ideal for managing short-term cash flow gaps or unexpected expenses.

Alternative Lenders

The rise of fintech has popularized alternative lending, offering faster access to capital, often with more flexible eligibility criteria than traditional banks.

- Online Lenders: These platforms provide quick approvals and funding, often relying on algorithms to assess creditworthiness. While convenient, their interest rates can be higher than traditional bank loans. They offer a variety of products, from short-term loans to lines of credit.

- Merchant Cash Advances (MCAs): Businesses receive an upfront sum in exchange for a percentage of future credit card sales. While quick and accessible, MCAs typically have a high cost of capital and should be approached with caution.

Specific Purpose Loans

Some loans are designed for particular assets or operational aspects.

- Equipment Financing: Specifically for purchasing new or used equipment. The equipment itself often serves as collateral, making these loans easier to secure.

- Invoice Factoring (Accounts Receivable Financing): Businesses sell their unpaid invoices to a third party (the factor) at a discount to get immediate cash. This improves cash flow, especially for businesses with long payment cycles from customers.

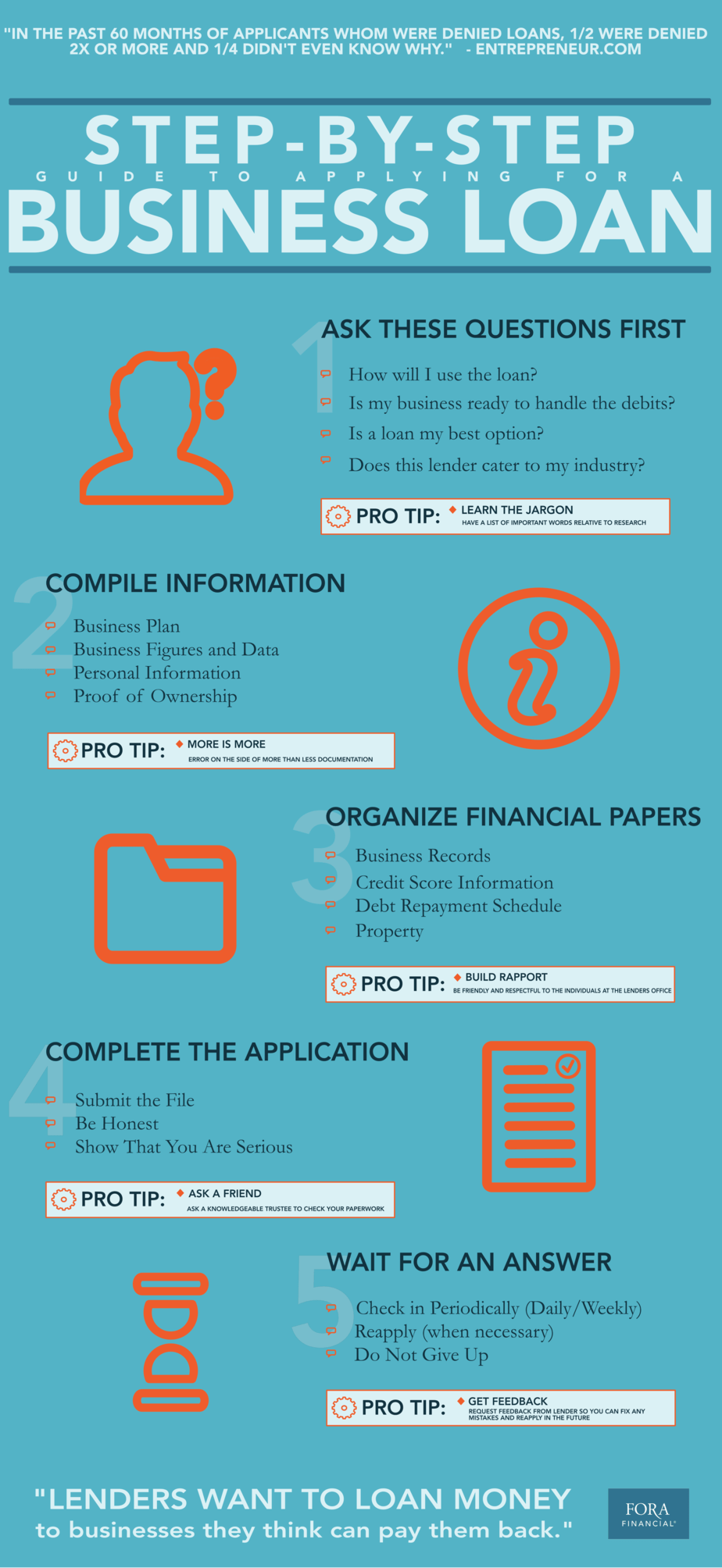

Preparing Your Loan Application

A strong application package is the cornerstone of a successful loan bid. Lenders need comprehensive documentation to assess risk and potential.

Business Plan & Executive Summary

Your business plan isn’t just for you; it’s a critical tool for lenders. It should clearly outline your business model, market analysis, management team, marketing strategy, and financial projections. The executive summary, a concise overview, should grab the lender’s attention and compel them to delve deeper. It should highlight your business’s unique value proposition and its potential for success and repayment.

Financial Statements

These are the backbone of your application. Provide recent and accurate statements:

- Profit & Loss (Income) Statement: Shows your revenue, expenses, and profit over a period (e.g., quarterly, annually).

- Balance Sheet: A snapshot of your assets, liabilities, and equity at a specific point in time.

- Cash Flow Statement: Details how cash is generated and used by your business, indicating liquidity.

- Financial Projections: Forecasts of future revenue, expenses, and cash flow for the loan’s term, demonstrating your ability to repay. These should be realistic and well-supported.

Legal Documents & Business Registration

Ensure all legal aspects of your business are in order. This includes your business registration documents (e.g., Articles of Incorporation/Organization), EIN, business licenses, and any relevant permits. Lenders need to confirm your business is legitimate and legally compliant.

Personal Financial Information & Credit Score

Lenders will often assess your personal credit history, especially for small businesses or startups. A strong personal credit score (FICO) indicates responsible financial management. You’ll likely need to provide personal tax returns, bank statements, and a personal financial statement detailing your assets and liabilities outside the business. For secured loans, personal guarantees may be required, meaning you are personally liable if the business defaults.

Collateral and Guarantees

For many loans, particularly traditional ones, lenders require collateral to mitigate their risk. Collateral can include real estate, equipment, accounts receivable, or inventory. Understand what assets your business has that can be pledged. A personal guarantee signifies your commitment to repay the loan even if your business fails.

The Application Process: From Submission to Approval

Once your documentation is ready, navigating the application and approval process involves several key stages.

Researching and Comparing Lenders

Don’t settle for the first lender you find. Research various institutions—banks, credit unions, online lenders, and specific SBA-approved lenders. Compare their loan products, interest rates, fees, repayment terms, and eligibility requirements. Read reviews and consider their reputation for customer service. A lender who understands your industry can be a significant asset.

Submitting Your Application Package

Carefully review all application forms for completeness and accuracy. Any missing information or discrepancies can cause delays or outright rejection. Be prepared to answer follow-up questions promptly and provide additional documentation as requested.

Underwriting and Due Diligence

This is where the lender thoroughly reviews your entire application. Underwriters assess your creditworthiness, financial stability, business viability, and ability to repay the loan. They may conduct interviews, site visits, and request additional reports (e.g., credit reports, background checks). Be transparent and forthcoming with all information.

Reviewing Loan Offers and Terms

If approved, you’ll receive a loan offer outlining the principal amount, interest rate (fixed or variable), repayment schedule, fees (origination, closing, etc.), and any specific covenants (conditions you must meet, such as maintaining certain financial ratios). Critically evaluate these terms. Understand the total cost of the loan and ensure the repayment schedule is feasible for your cash flow. Don’t hesitate to negotiate if you believe certain terms are unfavorable or request clarification on anything unclear.

Closing the Loan

Once you agree to the terms, you’ll proceed to the closing. This involves signing legal documents, and the funds will then be disbursed according to the agreed-upon schedule. Ensure you have a clear understanding of when the funds will be available and when the first repayment is due.

Post-Approval: Managing Your Business Debt Responsibly

Securing a loan is an achievement, but responsible debt management is crucial for your business’s long-term health.

Adhering to Loan Covenants

Many business loans come with covenants, which are conditions you must meet throughout the loan term. These might include maintaining specific financial ratios, submitting regular financial reports, or refraining from taking on additional debt without the lender’s consent. Failing to comply can lead to penalties or even default.

Monitoring Cash Flow

Continuously monitor your business’s cash flow to ensure you can meet your repayment obligations. Regularly update your financial projections and compare them against actual performance. Proactive management allows you to address potential shortfalls before they become critical.

Strategizing for Repayment

Develop a clear strategy for repayment. Integrate loan payments into your regular budgeting. If your business experiences unexpected growth, consider if early repayment is beneficial to reduce overall interest costs, provided there are no prepayment penalties. Conversely, if you foresee difficulties, communicate openly with your lender to explore potential solutions like refinancing or payment adjustments before defaulting. Responsible management of your business loan can build a strong credit history, paving the way for easier financing in the future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.