For many, the annual tax season is a mixed bag of anxiety and anticipation. While some dread the paperwork and potential tax liability, others eagerly await the prospect of a substantial tax refund. A tax refund isn’t a gift from the government; it’s simply the return of your own money that you’ve overpaid throughout the year. However, understanding how to strategically navigate the tax landscape can significantly increase the amount of money returned to you, effectively putting more cash back in your pocket. This guide will delve into proactive strategies, leveraging deductions and credits, and understanding tax-advantaged accounts to help you maximize your tax return.

Demystifying Your Tax Return: Refund vs. Liability

Before diving into strategies, it’s crucial to understand what a tax return truly represents and the difference between a refund and your overall tax liability. Many people conflate a large refund with financial success, but often, a substantial refund simply means you’ve given the government an interest-free loan throughout the year.

What is a Tax Refund?

A tax refund occurs when the amount of tax you’ve already paid (through paycheck withholdings, estimated payments, etc.) is greater than your actual tax liability for the year. The government then returns the excess amount to you. While a refund feels good, ideally, your goal should be to owe as little as possible without overpaying during the year, ensuring your money works for you, not the government. The true objective is to minimize your overall tax bill legally.

The Goal: Minimizing Taxable Income

The fundamental principle behind getting a bigger tax return (or reducing your tax liability) is to decrease your taxable income. Your taxable income is the portion of your gross income that the government can tax after accounting for deductions, adjustments, and exemptions. The lower your taxable income, the lower your overall tax bill, and consequently, the higher your potential refund (if you’ve overpaid). This isn’t about avoiding taxes but about smart financial planning to ensure you only pay what you legitimately owe, and not a penny more.

Proactive Planning: Financial Habits for Tax Advantage

The journey to a bigger tax return doesn’t begin on April 1st; it’s a year-long endeavor. Smart financial habits and proactive planning can set the stage for significant savings.

Year-Round Record Keeping

One of the most critical, yet often overlooked, aspects of tax optimization is meticulous record-keeping. Imagine trying to reconstruct a year’s worth of financial transactions just weeks before the tax deadline. It’s a recipe for missed opportunities. Maintain organized records of all income, expenses, charitable donations, medical bills, investment statements, and any other document relevant to your financial picture. Digital tools, cloud storage, and dedicated folders can make this process seamless. Good records ensure you don’t miss any eligible deductions or credits, and they’re invaluable if you ever face an audit.

Adjusting W-4 Withholding Strategically

For most employees, federal income tax is withheld from each paycheck based on the W-4 form you submit to your employer. This form dictates how much tax is taken out. If too much is withheld, you’ll likely get a big refund. If too little, you might owe tax. Reviewing and adjusting your W-4 annually, or whenever there’s a significant life event (marriage, birth of a child, new job), can fine-tune your withholdings. The IRS Tax Withholding Estimator is an excellent online tool that can help you determine the appropriate number of allowances to claim, aiming for a smaller refund or even a small balance due at tax time, meaning you’ve had more money in your pocket throughout the year.

Tax-Loss Harvesting for Investment Portfolios

For investors, tax-loss harvesting is a powerful strategy. This involves selling investments at a loss to offset capital gains and, potentially, a limited amount of ordinary income. If your capital losses exceed your capital gains, you can deduct up to $3,000 of those losses against your ordinary income in a given year. Any remaining losses can be carried forward to future years. This strategy can reduce your current tax bill and free up cash that might otherwise go to taxes. However, be mindful of the “wash sale” rule, which prohibits repurchasing the “substantially identical” security within 30 days before or after the sale.

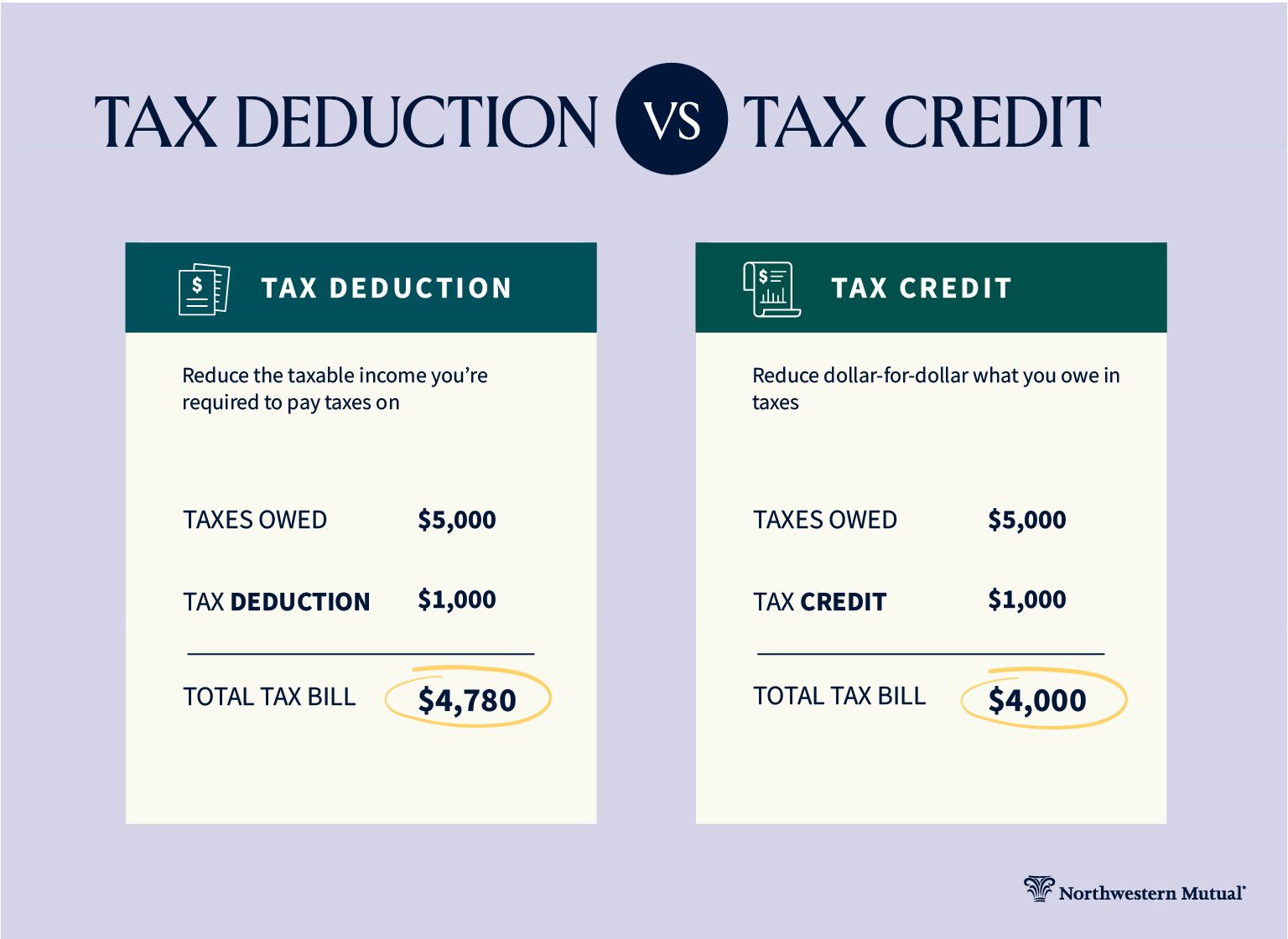

Unlocking Deductions: Reducing Your Taxable Income

Deductions are amounts that can be subtracted from your gross income to arrive at your taxable income. They directly reduce the amount of income subject to tax, leading to lower tax liability.

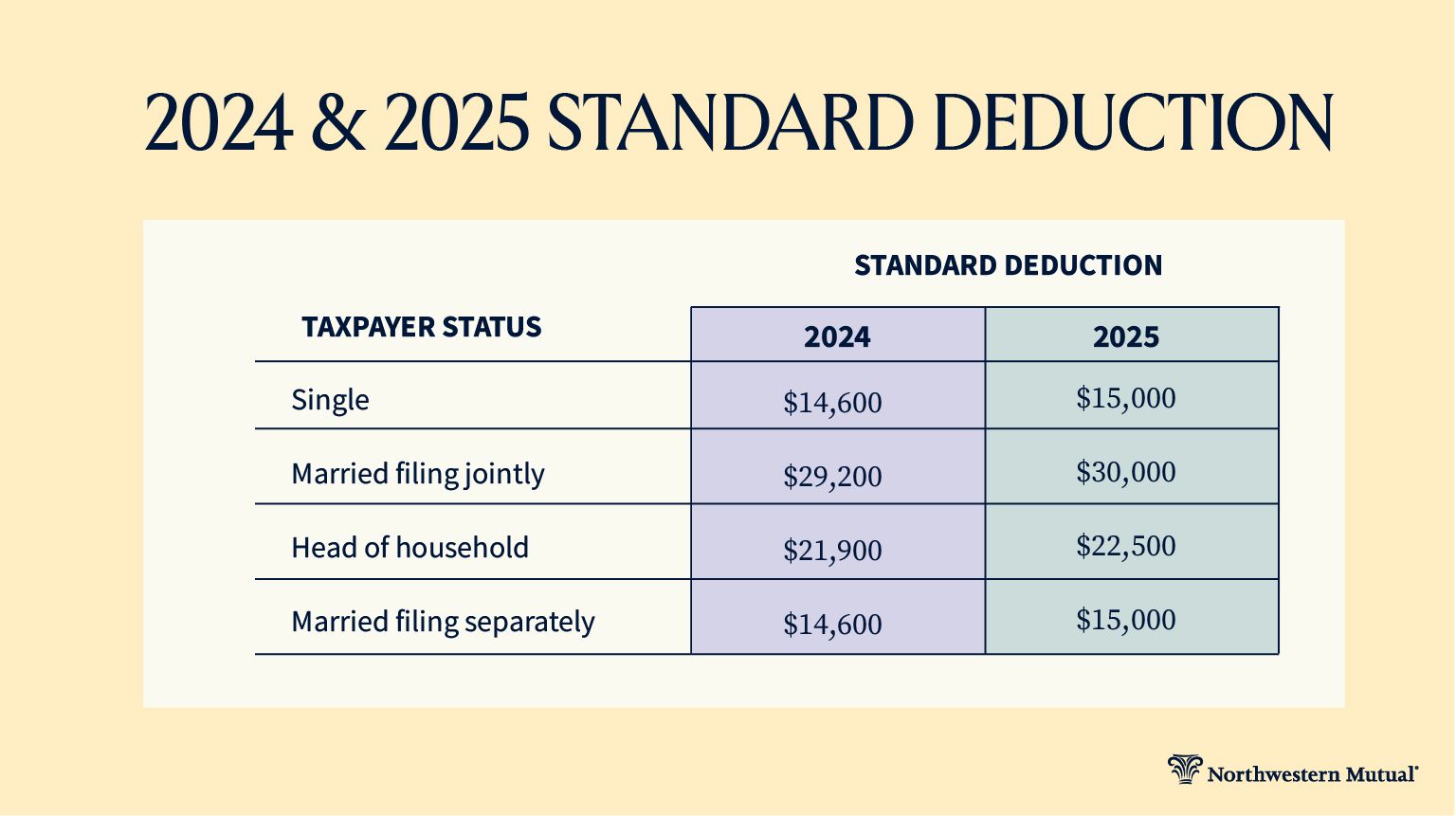

Standard Deduction vs. Itemized Deductions

Every taxpayer has a choice: take the standard deduction or itemize deductions. The standard deduction is a fixed dollar amount determined by the IRS, which varies based on your filing status (single, married filing jointly, head of household, etc.). Itemized deductions allow you to list out specific eligible expenses. You should choose whichever method results in a lower taxable income. For many, especially with the increased standard deduction in recent years, the standard deduction is more advantageous. However, if your eligible itemized deductions (like mortgage interest, state and local taxes, significant medical expenses, or large charitable contributions) exceed the standard deduction, itemizing is the way to go.

Common Itemized Deductions

If you choose to itemize, here are some common areas to explore:

- Mortgage Interest: Interest paid on a mortgage for your primary home and a second home (up to certain limits).

- State and Local Taxes (SALT): Property taxes, and either state income tax or sales tax (limited to $10,000 per household per year).

- Medical and Dental Expenses: If your qualified unreimbursed medical expenses exceed 7.5% of your Adjusted Gross Income (AGI).

- Charitable Contributions: Cash and non-cash donations to qualified charities.

Above-the-Line Deductions

These are particularly valuable because they reduce your AGI (Adjusted Gross Income), which can impact eligibility for certain credits and other deductions. They are “above the line” because they are subtracted before you even consider the standard or itemized deduction.

- IRA Contributions: Contributions to a traditional IRA are often deductible, depending on your income and whether you’re covered by a retirement plan at work.

- HSA Contributions: Contributions to a Health Savings Account (HSA) are 100% tax-deductible.

- Student Loan Interest: You can deduct up to $2,500 in student loan interest paid.

- Self-Employment Tax: If you’re self-employed, you can deduct one-half of your self-employment taxes paid.

- Educator Expenses: K-12 educators can deduct up to $300 for unreimbursed classroom expenses.

Maximizing Tax Credits: Dollar-for-Dollar Savings

While deductions reduce your taxable income, tax credits directly reduce the amount of tax you owe, dollar for dollar. A $1,000 credit reduces your tax bill by $1,000, which is often more impactful than a $1,000 deduction.

Understanding Refundable vs. Non-Refundable Credits

This distinction is crucial:

- Non-Refundable Credits: Can reduce your tax liability to $0, but you won’t get a refund for any amount that exceeds your tax bill.

- Refundable Credits: Can reduce your tax liability below $0, resulting in a refund even if you didn’t owe any tax.

Key Credits for Families and Individuals

There are numerous credits available; here are some of the most common and impactful:

- Child Tax Credit (CTC): A significant non-refundable credit for qualifying children.

- Earned Income Tax Credit (EITC): A refundable credit for low-to-moderate income working individuals and families, designed to provide financial relief and incentive to work.

- Education Credits (American Opportunity Tax Credit & Lifetime Learning Credit): Designed to help with the costs of higher education. The American Opportunity Tax Credit is partially refundable.

- Child and Dependent Care Credit: For expenses paid for the care of a qualifying child or dependent to allow you to work or look for work.

- Credit for Other Dependents: A non-refundable credit for dependents who do not qualify for the Child Tax Credit.

- Retirement Savings Contributions Credit (Saver’s Credit): A non-refundable credit for eligible low and moderate-income taxpayers who contribute to retirement accounts.

Energy-Efficient Home Improvements

The government often provides tax credits for making energy-efficient upgrades to your home, such as installing solar panels, energy-efficient windows, or certain types of insulation. These can be significant, multi-year credits, promoting both environmental stewardship and personal savings. Keep an eye on current tax laws for specific eligibility and credit amounts.

The Role of Tax-Advantaged Accounts & Professional Expertise

Beyond deductions and credits, leveraging specific financial accounts can offer substantial tax benefits, both in the present and for your future.

Retirement Accounts (401(k), IRA)

Contributing to tax-advantaged retirement accounts like a 401(k) or traditional IRA is one of the most effective ways to reduce your current taxable income. Contributions to these accounts are typically made with pre-tax dollars, meaning the money is deducted from your income before taxes are calculated. This immediately lowers your taxable income for the year. The money then grows tax-deferred until retirement, when withdrawals are taxed as ordinary income. For those seeking immediate tax reduction and long-term savings, these accounts are indispensable.

Health Savings Accounts (HSAs)

For individuals enrolled in a high-deductible health plan (HDHP), an HSA offers a unique “triple tax advantage”:

- Tax-deductible contributions: Money you put in reduces your taxable income.

- Tax-free growth: Investments within the HSA grow without being taxed.

- Tax-free withdrawals: Funds can be withdrawn tax-free for qualified medical expenses.

This makes HSAs an extremely powerful tool for both current healthcare costs and long-term retirement savings.

The Value of a Tax Professional

While self-preparing your taxes is common, especially with user-friendly software, the complexity of tax law means that many individuals miss out on valuable deductions or credits. A qualified tax professional (like a CPA or Enrolled Agent) can provide personalized advice, identify often-overlooked opportunities, and ensure accuracy. They can be particularly valuable if you have a complex financial situation, are self-employed, have significant investments, or have recently experienced major life changes. The fee for their services is often well worth the peace of mind and the potential tax savings.

Review and File Accurately

Before submitting your tax return, conduct a thorough review. Double-check all entries, calculations, and personal information. Incorrect Social Security numbers, bank account details for direct deposit, or overlooked forms can delay your refund or lead to complications. If you’re using tax software, ensure all relevant questions are answered completely. Accuracy is paramount, not only to get your maximum refund but also to avoid potential IRS inquiries or penalties.

In conclusion, getting a bigger tax return isn’t about finding loopholes; it’s about intelligent financial planning and a thorough understanding of the tax code. By proactively managing your finances, meticulously tracking expenses, leveraging all available deductions and credits, and utilizing tax-advantaged accounts, you can significantly reduce your tax liability and increase the money you get back each year. Embrace the power of knowledge and preparation, and turn tax season into an opportunity for financial gain.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.