In the modern economic landscape, the traditional 9-to-5 career model is no longer the sole path to financial stability. The “gig economy,” fueled by digital marketplaces and a global demand for specialized talent, has ushered in an era where millions of professionals operate as independent contractors. Central to this financial shift is the 1099 form—a series of documents that represent the backbone of non-employee compensation in the United States. Understanding how to “get” a 1099 is not merely about receiving a piece of mail in January; it is about mastering the ecosystem of independent income, tax strategy, and proactive business finance.

For those transitioning from a traditional W-2 environment, the 1099 lifestyle offers unparalleled freedom, but it also shifts the burden of tax withholding and financial reporting from the employer to the individual. This guide explores the nuances of the 1099 system, providing a roadmap for freelancers, side-hustlers, and investors to navigate their financial responsibilities with confidence.

Understanding the 1099 Ecosystem: Types and Requirements

The term “1099” is often used as a catch-all phrase for independent work, but in the eyes of the Internal Revenue Service (IRS), it refers to a suite of information returns. To “get” a 1099, you must first engage in an activity that generates income outside of a standard salary.

The 1099-NEC vs. 1099-MISC

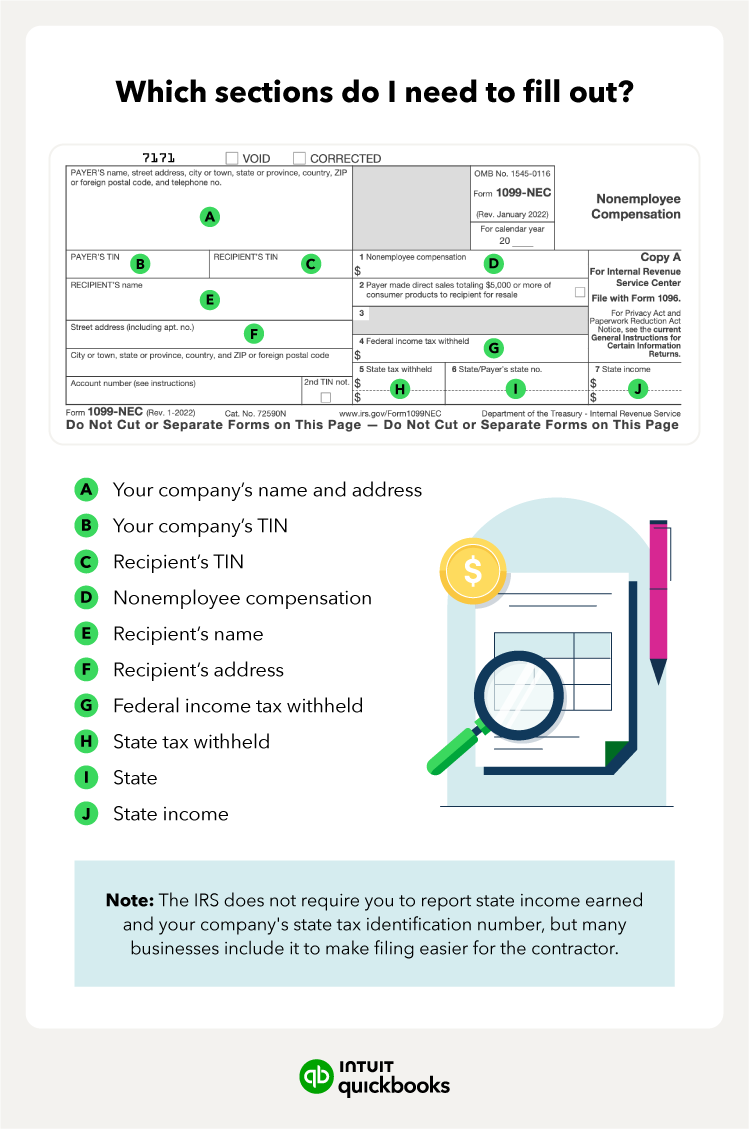

Prior to 2020, most independent contractors received their earnings reported on Box 7 of the 1099-MISC. However, the IRS reintroduced the 1099-NEC (Non-Employee Compensation) to streamline the reporting of payments made to individuals not treated as employees. If you have provided services to a business—whether as a graphic designer, a consultant, or a ride-share driver—and earned $600 or more during the tax year, that business is legally required to issue you a 1099-NEC.

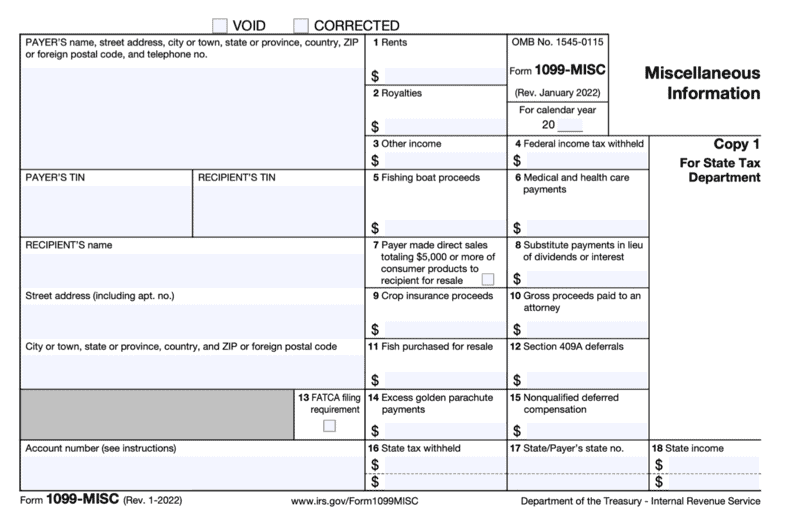

The 1099-MISC is still in use, but it is now reserved for “miscellaneous” income such as rent payments, prizes, awards, or legal settlements. Understanding this distinction is vital for accurate bookkeeping, as the NEC is specifically tied to self-employment tax obligations.

Investment and Interest Forms: 1099-INT, 1099-DIV, and 1099-B

You do not have to be a freelancer to receive a 1099. Investors and savers “get” 1099s based on the performance of their capital.

- 1099-INT: Issued by banks and financial institutions if you earned more than $10 in interest.

- 1099-DIV: Reported when you receive dividends or distributions from stocks and mutual funds.

- 1099-B: Covers proceeds from broker and barter exchange transactions, documenting the sale of stocks, bonds, or other securities.

Thresholds and Eligibility Criteria

A common misconception is that if you don’t receive a 1099, the income isn’t taxable. In reality, the $600 threshold is a requirement for the payer to report the income, but the recipient is responsible for reporting every dollar earned, regardless of whether a form was issued. For those working through third-party payment settlement entities (like PayPal or Venmo), the 1099-K is the relevant form, which has seen shifting legislative thresholds in recent years. Staying abreast of these thresholds ensures you are never blindsided by unexpected tax liabilities.

How to Ensure You Receive Your 1099 Forms

The process of “getting” a 1099 begins long before tax season. It starts the moment you agree to a contract or open an investment account. Proactive documentation is the only way to ensure your financial records align with what the IRS receives.

Onboarding and the W-9 Form

The most critical step in getting a 1099 is providing your payer with a Form W-9 (Request for Taxpayer Identification Number and Certification). This form provides the business with your legal name, business entity type (such as an LLC or Sole Proprietorship), and your Social Security Number (SSN) or Employer Identification Number (EIN). Without a W-9 on file, a company may be forced to practice “backup withholding,” where they deduct 24% of your pay upfront to send to the IRS—a scenario that can severely hamper your cash flow.

Tracking Your Earnings Throughout the Year

To verify the accuracy of the 1099s you eventually receive, you must maintain a robust internal accounting system. Utilizing financial software such as QuickBooks, FreshBooks, or even a meticulously managed spreadsheet allows you to cross-reference your bank deposits against the forms sent by clients. Discrepancies are common, often due to timing issues (e.g., a check mailed in late December but cashed in January). By tracking your “Money In” in real-time, you can request corrections early, preventing a mismatch on your tax return that could trigger an audit.

Managing Deadlines and Delivery Methods

Payers are generally required to mail or digitally provide 1099 forms by January 31st of the year following the payment. In the digital age, many platforms (like Uber, Upwork, or E*TRADE) do not mail physical copies unless specifically requested. Instead, they provide a “Tax Center” portal where you can download your forms. It is your responsibility to log into these accounts and retrieve your documents. Setting a calendar reminder for the last week of January to “sweep” your digital accounts for forms is an essential habit for the modern earner.

Strategic Financial Management for 1099 Income Earners

Receiving a 1099 is a signal of financial independence, but it requires a more sophisticated approach to money management than a traditional paycheck. When you are a 1099 earner, you are effectively a business of one.

Estimated Tax Payments and Avoiding Penalties

Unlike W-2 employees, 1099 contractors do not have taxes withheld from their checks. This can create a false sense of wealth. The “Gross Income” you receive is not yours to keep in its entirety. You are responsible for both the employee and employer portions of Social Security and Medicare taxes (known as Self-Employment Tax), which totals approximately 15.3%.

To avoid large underpayment penalties, 1099 earners must typically make quarterly estimated tax payments to the IRS and their state tax agency. A prudent strategy is to set aside 25% to 30% of every 1099 payment into a separate high-yield savings account dedicated solely to taxes.

Deductible Business Expenses and Net Profit

The primary financial advantage of being a 1099 earner is the ability to deduct “ordinary and necessary” business expenses. While a W-2 employee is taxed on their gross salary, a 1099 contractor is taxed on their net profit. This means you can subtract costs such as:

- Home office expenses (portion of rent/utilities).

- Marketing and website hosting.

- Professional software and hardware.

- Travel and meals directly related to business.

- Health insurance premiums.

Effective expense tracking can significantly lower your taxable income, making the 1099 path more lucrative than it initially appears.

Retirement Planning for the Self-Employed

Getting a 1099 means you lose access to employer-sponsored 401(k) matches, but it opens the door to more powerful retirement vehicles. Personal finance for the 1099 earner should include exploring a SEP IRA or a Solo 401(k). These accounts often have much higher contribution limits than traditional IRAs, allowing you to shield a larger portion of your 1099 income from current taxation while building long-term wealth.

What to Do if You Don’t Receive a 1099

It is a common occurrence: January passes, and the 1099 you were expecting from a client never arrives. This does not absolve you of your reporting duties, nor does it mean the IRS isn’t aware of the income.

Verifying Records Against Bank Statements

If a form is missing, your first move should be to perform a total reconciliation of your bank statements. Confirm exactly how much was deposited from that specific payer. If you find you earned $550, the client was not required to send a form, though you still must report it. If you earned $2,000 and the form is missing, the client may have an administrative delay or an outdated address for you.

Reporting Income Without a Form

You do not need a 1099-NEC to file your taxes. You simply report the income as “Gross Receipts” on Schedule C of your Form 1040. The IRS is far more concerned with under-reporting income than they are with you reporting income that wasn’t formally documented on a 1099. As long as your records are accurate and you pay the tax owed, you are in compliance.

Contacting Payers and Correcting Errors

If you receive a 1099 that reflects an incorrect amount—perhaps a cancelled project payment was included by mistake—contact the payer immediately. Ask them to issue a “Corrected” 1099. If they refuse or are unresponsive, you can still file your taxes with the correct amount, but you should attach a brief explanation and evidence (like a bank statement) to your return to preemptively answer any IRS inquiries.

Leveraging 1099 Status for Long-Term Wealth Building

Ultimately, “getting a 1099” is more than a tax event; it is a milestone in professional autonomy. By diversifying your income streams and mastering the mechanics of independent finance, you create a more resilient financial future.

Diversifying Income Streams

The beauty of 1099 income is that it is rarely tied to a single source. Unlike a W-2 job where a layoff results in zero income, a 1099 professional can have five, ten, or twenty different clients. This diversification is a form of financial insurance. If one client cuts their budget, the others remain, providing a “buffer” that traditional employment lacks.

Scaling from Freelancer to Business Owner

As your 1099 income grows, the financial strategy often shifts from personal finance to corporate finance. Many high-earning independent contractors eventually transition from a Sole Proprietorship to an S-Corp. This allows them to pay themselves a “reasonable salary” and take the remaining profit as a distribution, potentially saving thousands of dollars in self-employment taxes. This level of financial engineering is only possible once you understand the foundational principles of the 1099 system.

In conclusion, getting a 1099 is a signifier of your role in the modern economy. Whether it comes from a side hustle, a full-time freelance career, or a savvy investment portfolio, the 1099 form is a tool for financial empowerment. By maintaining rigorous records, understanding your tax obligations, and strategically managing your expenses, you can turn these annual forms into the building blocks of lasting wealth and professional freedom.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.