Purchasing a car is one of the most significant financial decisions many individuals make, second only to buying a home. For most, this purchase involves securing an auto loan, which translates into a recurring monthly payment. Understanding how this payment is calculated isn’t just about satisfying curiosity; it’s a critical step in responsible financial planning, ensuring you can comfortably afford the vehicle without straining your budget. A seemingly small difference in interest rate or loan term can lead to thousands of dollars in extra costs over the life of the loan. This guide delves into the various components that determine your car’s monthly payment, provides methods for calculating it, and offers strategic insights to help you make an informed decision.

Understanding the Core Components of a Car Payment

At its heart, a car loan is a form of installment debt, meaning you borrow a lump sum and repay it, plus interest, over a set period through regular, equal payments. Several key factors combine to determine the exact amount of each payment.

The Principal Loan Amount

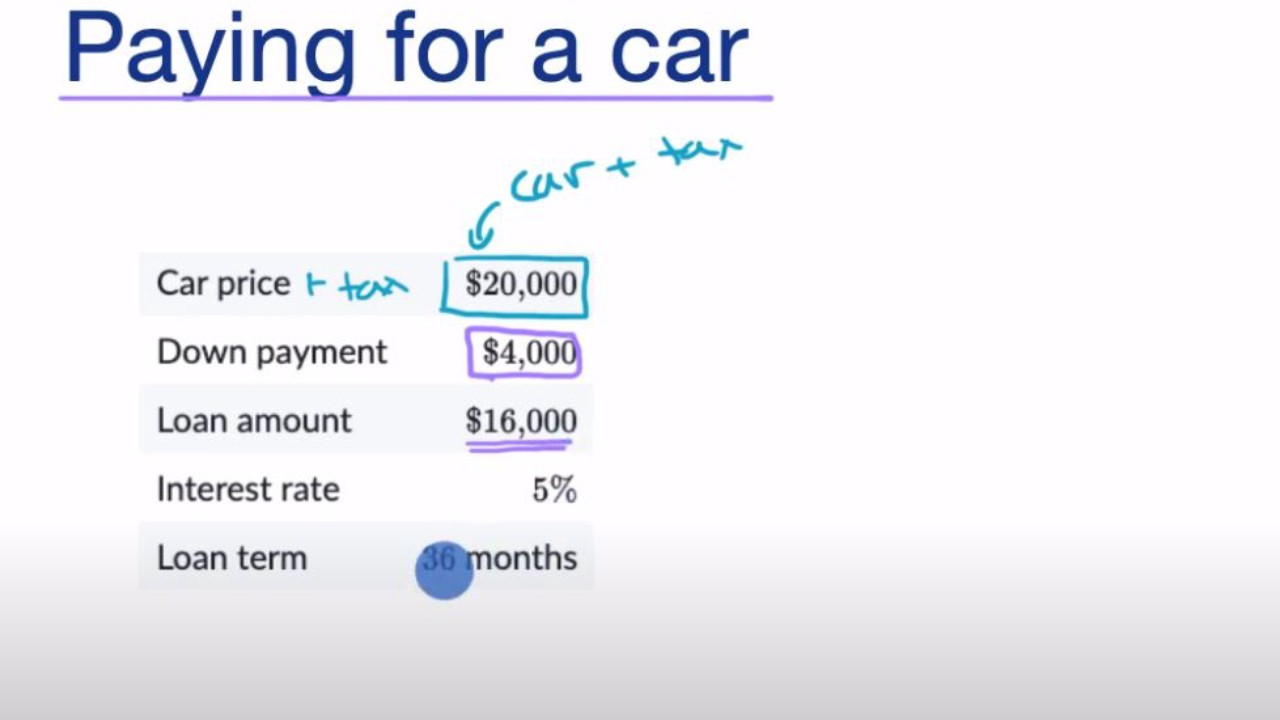

This is the actual amount of money you are borrowing. It’s not simply the sticker price of the car. Rather, it’s the agreed-upon purchase price of the vehicle, minus any down payment you make, any trade-in value from an old vehicle, and potentially any rebates or incentives applied at the point of sale. A higher principal loan amount will naturally lead to a higher monthly payment, assuming all other factors remain constant. Conversely, making a larger down payment or getting a good trade-in value reduces the principal, thereby lowering your monthly financial obligation and the total interest paid over time.

Interest Rate (APR)

The interest rate, often expressed as an Annual Percentage Rate (APR), is essentially the cost of borrowing money. It’s the percentage of the principal that the lender charges you for the privilege of using their funds. This is arguably the most impactful variable on your monthly payment and the total cost of your loan. A higher interest rate means a larger portion of each payment goes towards interest, increasing both your monthly obligation and the overall cost of the car. Your credit score is the primary determinant of the interest rate you’ll qualify for, with excellent credit scores typically securing the lowest rates, while lower scores result in higher rates to compensate lenders for perceived increased risk.

Loan Term (Loan Length)

The loan term refers to the duration over which you agree to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). This factor directly influences the size of your monthly payment. A longer loan term will result in lower monthly payments because the principal and interest are stretched out over more installments. However, this convenience comes at a significant cost: you’ll pay more in total interest over the life of the loan. Conversely, a shorter loan term means higher monthly payments, but you’ll pay less in total interest and own the car outright sooner. Striking a balance between affordability and minimizing total interest is key here.

Sales Tax and Fees

When purchasing a car, various additional costs are involved beyond the vehicle’s price. Sales tax, determined by your state or local municipality, can add a substantial amount to the total cost. Other fees may include title and registration fees, documentation fees charged by the dealership, and sometimes destination charges. While these are not part of the principal loan amount itself, they are often rolled into the total financing package, effectively increasing the amount you borrow and, consequently, your monthly payment. It’s crucial to understand these additional costs and how they impact your overall financial commitment.

Manual Calculation Methods: The Mathematical Approach

While financial calculators are widely available, understanding the underlying mathematical formula can provide a deeper insight into how car payments are determined and empower you to verify calculations.

The Auto Loan Payment Formula

The standard formula used to calculate a fixed-rate, amortizing loan payment (like a car loan) is:

M = P [ i(1 + i)^n ] / [ (1 + i)^n – 1]

Where:

- M = Your monthly loan payment

- P = The principal loan amount (the amount you borrowed after down payment, trade-in, etc.)

- i = Your monthly interest rate (your annual interest rate divided by 12)

- n = The total number of payments (your loan term in years multiplied by 12)

This formula may look intimidating, but breaking it down reveals its logic. It accounts for both the principal repayment and the interest accruing each month over the life of the loan.

Step-by-Step Walkthrough with an Example

Let’s illustrate with an example:

- Principal (P): $25,000

- Annual Interest Rate: 6% (or 0.06 as a decimal)

- Loan Term: 5 years (60 months)

Step 1: Calculate the monthly interest rate (i)

i = Annual Interest Rate / 12

i = 0.06 / 12 = 0.005

Step 2: Calculate the total number of payments (n)

n = Loan Term in years * 12

n = 5 * 12 = 60

Step 3: Plug the values into the formula:

M = 25,000 [ 0.005(1 + 0.005)^60 ] / [ (1 + 0.005)^60 – 1]

First, calculate (1 + i)^n:

(1 + 0.005)^60 = (1.005)^60 ≈ 1.34885

Now, substitute back into the formula:

M = 25,000 [ 0.005 * 1.34885 ] / [ 1.34885 – 1 ]

M = 25,000 [ 0.00674425 ] / [ 0.34885 ]

M = 168.60625 / 0.34885

M ≈ $483.39

So, for a $25,000 loan at 6% over 5 years, your estimated monthly payment would be approximately $483.39.

Limitations of Manual Calculations

While helpful for understanding, manually calculating loan payments can be tedious and prone to error, especially when dealing with decimal places and exponents. Even a slight rounding mistake can lead to an inaccurate figure. For practical purposes and to ensure precision, leveraging dedicated financial tools is generally recommended. This approach saves time, reduces the risk of error, and often provides additional insights like the total interest paid.

Leveraging Financial Tools: Easier and More Accurate Ways

Fortunately, you don’t need to be a math whiz to determine your car’s monthly payment. A variety of accessible financial tools make this process quick, accurate, and user-friendly.

Online Car Loan Calculators

Online car loan calculators are arguably the most popular and convenient method for estimating monthly payments. These tools are ubiquitous, found on nearly every financial institution’s website, automotive sites, and independent personal finance portals. You simply input the principal loan amount, the interest rate (APR), and the loan term, and the calculator instantly provides the estimated monthly payment. Many advanced calculators also allow you to factor in a down payment, trade-in value, sales tax, and other fees, providing a more comprehensive and accurate picture of your potential payment. They are invaluable for comparing different loan scenarios and understanding how changes in variables impact your payment.

Dealership Financial Departments

When you’re at a dealership, the finance department will calculate your monthly payment based on the terms they offer. While they use the same underlying formulas, their calculations will include all specific fees and charges associated with that particular vehicle and deal. It’s crucial to approach these calculations with a critical eye. Always come prepared with your own pre-calculated estimates from independent sources. This allows you to verify their figures and ensures you’re not accepting unfavorable terms or hidden costs. Remember, dealerships often have incentives to maximize their profit, so cross-referencing their numbers is a smart financial move.

Bank and Credit Union Calculators

Before even stepping foot in a dealership, it’s highly advisable to use car loan calculators provided by banks, credit unions, and other lenders. These calculators often allow you to get pre-qualified for a loan, giving you a clear idea of the interest rate you might expect based on your creditworthiness. Armed with this information, you can calculate your potential payments for various car prices and loan terms, effectively setting your budget before you start shopping. Getting pre-approved for a loan also strengthens your negotiating position at the dealership, as you’re no longer solely reliant on their financing offers.

Factors Beyond the Basic Payment: Hidden Costs and Strategic Considerations

Focusing solely on the monthly payment figure can be misleading. A car’s true cost of ownership extends far beyond the loan installment, and smart financial planning considers all associated expenses.

Insurance Costs

A car loan payment covers only the cost of the vehicle and its financing. It does not include car insurance, which is a mandatory and often significant monthly expense. Insurance premiums vary widely based on the vehicle type, your driving record, age, location, and the coverage you choose. Before committing to a car purchase, obtain insurance quotes for the specific make and model you’re considering. A lower monthly car payment might be appealing, but if the insurance costs are exorbitant, your total monthly transportation expenses could still be too high for your budget.

Maintenance and Repairs

All cars require regular maintenance (oil changes, tire rotations, brake checks, etc.) and, eventually, repairs. These costs can range from minor to substantial, particularly as a vehicle ages. While a brand-new car might come with a warranty covering initial issues, you’ll still have routine maintenance expenses. Budgeting for these ongoing costs, which are separate from your loan payment, is crucial for long-term financial stability. Consider a vehicle’s reliability ratings and average maintenance costs when making your purchase decision.

Fuel Costs

Unless you’re opting for an electric vehicle with home charging, fuel will be a regular and recurring expense. The cost of gasoline fluctuates, and your specific vehicle’s fuel efficiency (MPG) will significantly impact this budget line item. A car with poor fuel economy might have a manageable monthly payment but could become a financial drain due to high fuel bills, especially if you drive frequently. Calculate your estimated monthly fuel costs based on your anticipated mileage and the car’s MPG to get a complete picture.

The Impact of Down Payment and Trade-in

As briefly mentioned, your down payment and any trade-in value from your old car directly reduce the principal loan amount. This has a dual benefit: it lowers your monthly payment and significantly reduces the total amount of interest you’ll pay over the life of the loan. A larger upfront investment means you’re borrowing less, making the loan less costly in the long run. Strategic financial planning often involves saving for a substantial down payment to minimize monthly obligations and overall interest expenses.

Understanding Total Cost of Ownership vs. Monthly Payment

The savvy car buyer understands that the “true cost” of a vehicle isn’t just its monthly payment. It’s the Total Cost of Ownership (TCO), which encompasses the purchase price, interest, sales tax, insurance, fuel, maintenance, repairs, and even depreciation. Focusing solely on a low monthly payment can lead to overlooking high TCO factors. For example, a car with a low monthly payment but poor fuel economy, high insurance premiums, and rapid depreciation might cost you more in the long run than a slightly more expensive car with better efficiency and lower overall operating costs. Always evaluate the full financial picture before making a commitment.

Strategic Tips for Managing Your Car Payment

Navigating the car buying process can be daunting, but with a few strategic approaches, you can secure a favorable loan and manage your payments effectively.

Improve Your Credit Score

Your credit score is the single most influential factor in determining the interest rate you’ll be offered. Lenders use it to assess your creditworthiness and the risk associated with lending to you. Before you start car shopping, take steps to improve your credit score. This could include paying down existing debts, ensuring all bill payments are on time, and checking your credit report for errors. Even a slight improvement in your score can translate into a lower APR, saving you hundreds or thousands of dollars in interest over the life of the loan and lowering your monthly payment.

Shop Around for Rates

Never settle for the first loan offer you receive, particularly from a dealership. Instead, shop around and compare loan offers from multiple lenders, including banks, credit unions, and online lenders. Each institution has different lending criteria and rates, and what one offers might be significantly better than another. Getting pre-approved for a loan from an independent lender before visiting a dealership gives you a baseline interest rate and empowers you to negotiate more effectively. You can use their offer to leverage a better deal from the dealership’s finance department.

Consider a Shorter Loan Term (If Affordable)

While longer loan terms result in lower monthly payments, they come at the significant cost of increased total interest paid. If your budget allows, opting for a shorter loan term (e.g., 48 or 60 months instead of 72 or 84 months) will save you a substantial amount of money in interest over time. You’ll own the car outright sooner, freeing up that portion of your budget for other financial goals. Weigh the trade-off carefully: can you comfortably afford the higher monthly payment of a shorter term without jeopardizing other financial obligations?

Don’t Forget the Budget

Ultimately, the most crucial tip is to integrate your potential car payment into your overall personal budget. A car payment should not exceed a comfortable percentage of your take-home pay (many financial experts suggest no more than 10-15% of your net income, including insurance). Create a detailed budget that accounts for all your income and expenses, and determine how much you can realistically allocate to a car payment, including insurance, fuel, and maintenance, without feeling financially stretched. This proactive approach ensures your new car is a source of joy, not financial stress.

In conclusion, finding the monthly payment of a car is a fundamental step in the vehicle acquisition process. By understanding the interplay of principal, interest rate, and loan term, and by leveraging available financial tools, you can accurately estimate your monthly obligation. However, true financial wisdom extends beyond this single figure, encompassing the total cost of ownership, including insurance, maintenance, and fuel. By approaching car buying with a clear understanding of all financial implications and strategic planning, you can make a choice that aligns with your budget and long-term financial goals.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.