Navigating the world of student loans can often feel like deciphering a complex financial labyrinth. For millions of borrowers, understanding the exact status of their student loan debt is the critical first step towards effective financial planning and eventual liberation from debt. Whether you’re fresh out of college, years into your career, or simply reviewing your financial obligations, knowing your precise student loan balance – encompassing both federal and private loans – is paramount. This guide will walk you through the essential steps and resources available to accurately find your student loan balance, empowering you to take control of your financial future.

For many, the initial excitement of higher education often overshadows the long-term financial implications. Over time, multiple loans from different sources, varying interest rates, and changes in loan servicers can make it challenging to maintain a clear picture of your total indebtedness. Yet, without this fundamental information, making informed decisions about repayment strategies, refinancing options, or even budgeting becomes incredibly difficult. Let’s demystify the process and equip you with the knowledge to pinpoint your student loan balance with confidence.

Why Knowing Your Student Loan Balance Matters

Understanding the exact amount you owe is more than just a number; it’s a foundational element of sound personal finance. It impacts numerous aspects of your financial well-being, from daily budgeting to long-term wealth accumulation.

Financial Planning and Budgeting

Your student loan balance, alongside your interest rate and monthly payment, directly influences your cash flow and overall budget. When you have a clear picture of your total debt, you can accurately allocate funds, understand how much discretionary income you have, and make realistic plans for other financial goals like saving for a down payment, retirement, or unexpected emergencies. Without this clarity, you risk underestimating your financial obligations, leading to budget shortfalls and increased stress. Knowing your balance is the first step in creating a sustainable financial plan that accommodates your debt while still allowing for personal growth and saving.

Debt Management Strategies

A precise understanding of your student loan balance is indispensable for developing and implementing effective debt management strategies. Whether you’re considering aggressive repayment tactics like the “debt avalanche” or “debt snowball” method, exploring income-driven repayment plans, or evaluating consolidation and refinancing opportunities, every strategy hinges on accurate balance information. For instance, if you’re looking to refinance, lenders will require exact figures for each loan you wish to include. Similarly, deciding which loan to prioritize for extra payments often depends on its balance and interest rate. Without this data, your strategies are built on guesswork, potentially leading to suboptimal outcomes or missed opportunities to save money.

Avoiding Default and Understanding Repayment Options

Student loan default carries severe consequences, including damaged credit, wage garnishment, and loss of eligibility for future federal aid. Knowing your balance, along with your payment history and current status, is crucial for staying on top of your obligations and avoiding default. It allows you to proactively engage with your loan servicer if you anticipate difficulty making payments. Furthermore, a clear picture of your balance helps you understand which repayment options might be available to you – especially for federal loans – such as Income-Driven Repayment (IDR) plans, deferment, or forbearance. These options can provide much-needed flexibility during times of financial hardship, but they can only be fully utilized if you know exactly what you owe and to whom.

Locating Federal Student Loan Information

For most borrowers, federal student loans constitute a significant portion of their educational debt. Fortunately, the U.S. Department of Education provides centralized resources to help you track these loans effectively.

The National Student Loan Data System (NSLDS) – The Official Hub

The National Student Loan Data System (NSLDS) is the U.S. Department of Education’s central database for student aid. It contains information about all federal grants and loans you’ve received. This is the definitive starting point for anyone seeking to understand their federal student loan landscape.

To access your information, you’ll need your Federal Student Aid (FSA) ID. If you don’t have one, you can create one on the Federal Student Aid website (studentaid.gov). Once logged in, NSLDS provides a comprehensive overview of your federal student loans, including:

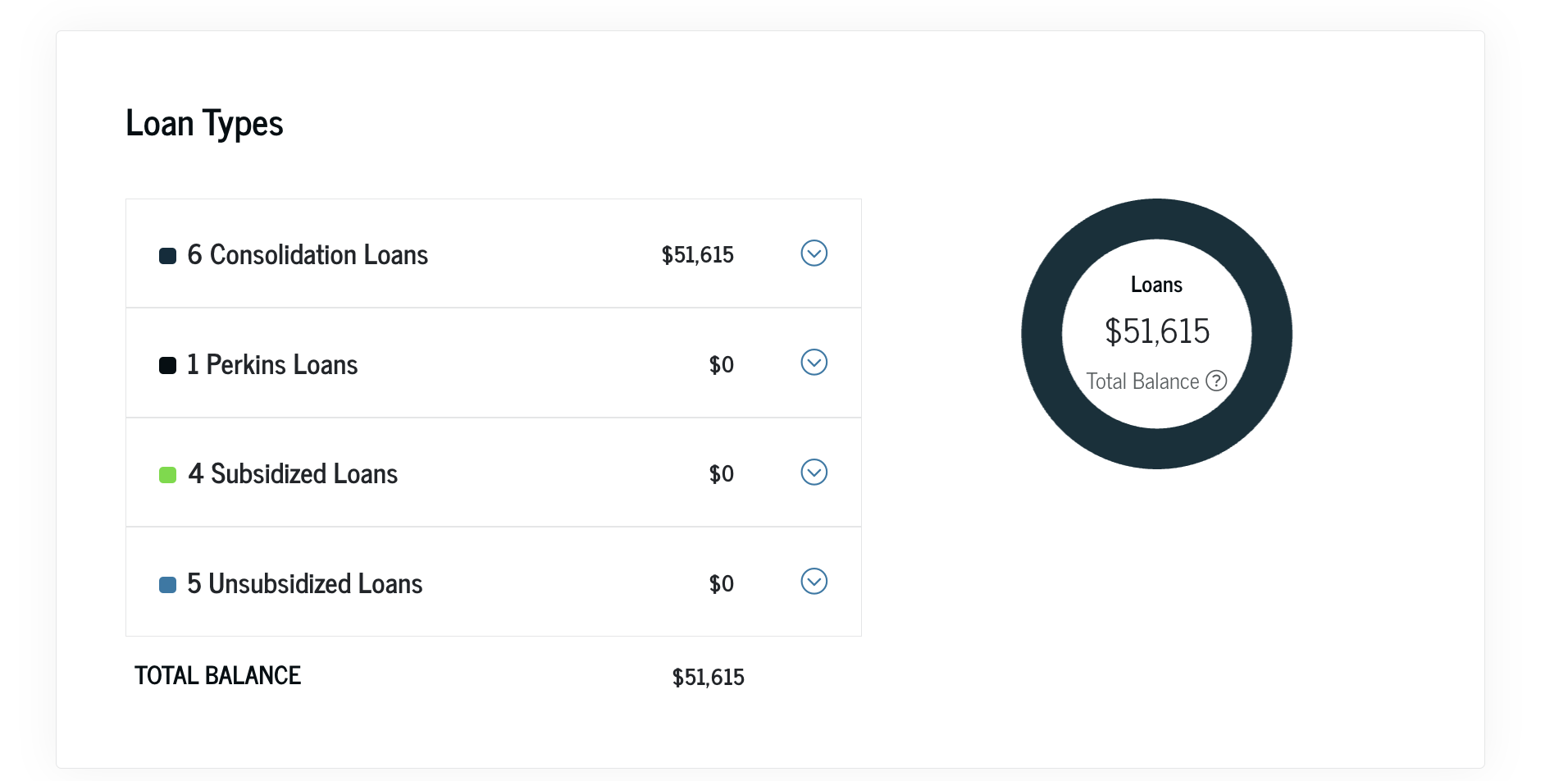

- The original loan amount

- Current outstanding balance

- Loan type (e.g., Subsidized, Unsubsidized, PLUS)

- Interest rates

- Disbursement dates

- Your current loan servicer(s)

This system is invaluable for getting a bird’s-eye view of all your federal loans in one place, especially if you’ve attended multiple institutions or taken out loans over several years.

Your Loan Servicer’s Website

While NSLDS provides a summary, your individual loan servicer holds the most up-to-date and detailed information about your federal loans. A loan servicer is a company that manages the billing and other services for your student loans. If you accessed your NSLDS data, you would have seen who your current servicers are. Common federal loan servicers include:

- Nelnet

- Great Lakes Educational Loan Services (now largely transitioning to Nelnet)

- MOHELA

- Edfinancial Services

- Aidvantage (formerly Navient’s federal loan servicing arm)

Once you identify your servicer(s), visit their official website. You’ll likely need to create an account using your Social Security number and other personal identifiers if you haven’t already. After logging in, you’ll find dashboards that display:

- Your current principal balance

- Accrued interest

- Your payment history

- Current repayment plan

- Due dates for upcoming payments

- Statements and tax documents

Checking your servicer’s website regularly is crucial, as NSLDS is updated periodically, while the servicer’s site provides real-time information.

Annual Loan Statements

Loan servicers are generally required to send you annual statements detailing your loan activity, including your current balance, interest paid, and other important information. Keep these statements organized, either digitally or physically, as they can serve as a reliable record of your loan balances over time. While not as immediate as online access, they offer a consistent snapshot of your debt at a specific point each year.

Tracking Down Private Student Loan Balances

Private student loans, offered by banks, credit unions, and other private lenders, are not managed by the U.S. Department of Education and therefore will not appear in the NSLDS. Locating these balances requires a different approach.

Contacting Your Original Lender

If you recall the institution that provided your private student loan – whether it was a bank like Sallie Mae, Discover, Wells Fargo (now often sold to other servicers), or a credit union – the most direct approach is to contact them directly. Even if your loan has since been sold to another servicer, the original lender should be able to provide you with information about who currently holds your loan. They can direct you to the correct loan servicer or provide a contact number. Be prepared to provide personal identifying information to verify your identity.

Reviewing Credit Reports

Your credit report is a powerful tool for uncovering all types of debt, including private student loans. Lenders typically report loans to the major credit bureaus (Equifax, Experian, and TransUnion). You are entitled to a free credit report from each of these bureaus once every 12 months via AnnualCreditReport.com.

When you pull your credit reports, carefully review the “accounts” or “trade lines” section. Each private student loan you’ve taken out should be listed, showing:

- The lender’s name

- The original loan amount

- The current balance

- Your payment status

This method is particularly effective if you’ve forgotten which institutions provided your private loans or if your loans have been transferred multiple times. Discrepancies or unfamiliar accounts should be investigated further.

Bank Statements and Payment Records

Another way to jog your memory about private student loans is to review your past bank statements or payment records. Look for recurring payments made to student loan providers. The names of the companies you’ve been paying will likely be your current private loan servicers. If you find payments but can’t immediately identify the lender, you can often trace the payment back through your bank to obtain contact information for the recipient. This might require digging through several years of records, but it can be a reliable method for those with detailed financial tracking.

Strategies for Managing Multiple Student Loans

Once you’ve successfully gathered all your federal and private student loan balances, the next step is to organize this information to develop a cohesive repayment strategy. Many borrowers face the challenge of managing multiple loans, each with its own terms, interest rates, and servicers.

Creating a Master Spreadsheet

The most effective way to manage multiple loans is to create a master spreadsheet. This central document should include:

- Loan Type: Federal (Subsidized, Unsubsidized, PLUS) or Private

- Original Lender/Servicer: Who holds the loan

- Original Balance: The amount borrowed

- Current Balance: The precise outstanding amount

- Interest Rate: Fixed or variable, and the percentage

- Minimum Monthly Payment: What you are required to pay

- Due Date: When the payment is due each month

- Repayment Plan: (e.g., Standard, Graduated, IDR)

- Status: (e.g., In repayment, Deferment, Forbearance)

A comprehensive spreadsheet allows you to visualize your entire debt portfolio at a glance, making it easier to identify high-interest loans to prioritize, track overall progress, and avoid missing payments.

Exploring Consolidation and Refinancing Options

With a clear view of all your balances, you can effectively evaluate options like loan consolidation or refinancing.

- Federal Loan Consolidation: This allows you to combine multiple federal student loans into a single Direct Consolidation Loan. This simplifies repayment by giving you one monthly payment and often extends your repayment period, which can lower your monthly outlay (though it may increase the total interest paid over the life of the loan). Your interest rate will be the weighted average of your previous loans, rounded up to the nearest one-eighth of a percent.

- Private Student Loan Refinancing: This involves taking out a new loan from a private lender to pay off one or more existing student loans (federal, private, or both). The goal is usually to secure a lower interest rate, reduce your monthly payment, or simplify repayment with a single bill. Eligibility for refinancing largely depends on your credit score, income, and debt-to-income ratio. Be cautious, however: refinancing federal loans into a private loan means forfeiting federal benefits like income-driven repayment plans, generous deferment options, and potential loan forgiveness programs.

Carefully weigh the pros and cons of each option based on your financial situation and future goals.

Understanding Different Repayment Plans

For federal student loans, there are various repayment plans designed to accommodate different financial circumstances.

- Standard Repayment Plan: Fixed payments over 10 years.

- Graduated Repayment Plan: Payments start low and increase every two years, over 10 years.

- Extended Repayment Plan: Fixed or graduated payments over 25 years for borrowers with more than $30,000 in federal loans.

- Income-Driven Repayment (IDR) Plans: Payments are capped at a percentage of your discretionary income and adjusted annually based on your income and family size. These plans can lead to loan forgiveness after 20 or 25 years of payments (depending on the plan).

Knowing your total balance and income is crucial for determining which IDR plan offers the most benefit to you.

Next Steps After Finding Your Balance

Finding your student loan balance is just the beginning. The real power comes from using this information to create an actionable plan.

Developing a Repayment Strategy

Once you have a comprehensive understanding of all your loans, interest rates, and balances, you can formulate a strategic repayment plan. Consider which loans to prioritize (e.g., highest interest rate first, smallest balance first), how much extra you can afford to pay each month, and how to allocate those extra payments. Set realistic goals for when you want to be debt-free and continuously monitor your progress against these goals. This proactive approach transforms daunting debt into a manageable project.

Utilizing Financial Tools and Resources

Leverage technology to help you manage your debt. Many personal finance apps and websites offer student loan tracking features that can integrate with your bank accounts and loan servicers. These tools can help you visualize your debt, track payments, project payoff dates, and even provide insights into refinancing opportunities. Beyond apps, reputable non-profit credit counseling agencies can offer free or low-cost advice on debt management.

Seeking Professional Financial Advice

If your student loan situation is particularly complex, involves a large sum, or if you’re struggling to create a viable repayment plan, consider seeking advice from a qualified financial advisor. A certified financial planner (CFP) or a student loan specialist can provide personalized guidance, help you explore all available options, and integrate your student loan strategy into your broader financial planning goals, ensuring a holistic approach to your financial well-being.

In conclusion, knowing your student loan balance is not merely a bureaucratic task; it’s an essential act of financial empowerment. By systematically gathering this crucial information for both federal and private loans, organizing it, and then strategically planning your next steps, you move from feeling overwhelmed to taking confident control. Embrace this fundamental step in your financial journey, and you’ll be well on your way to achieving debt freedom and securing a more prosperous future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.