In the modern financial landscape, the ability to access critical banking information instantaneously is not just a convenience—it is a necessity. As traditional brick-and-mortar banking continues to evolve into a digital-first experience, tools like the Chase Mobile® app have become the central hub for personal finance management. One of the most frequent tasks users need to perform is locating their routing number. Whether you are setting up a new direct deposit, organizing an electronic tax payment, or initiating a domestic wire transfer, your routing number is the primary key that identifies your financial institution within the vast global banking network.

This guide explores the specific steps to finding your routing number within the Chase app, while also providing a deeper look into the financial significance of these numbers and how to manage them securely within your broader personal finance strategy.

1. Understanding the Role of Routing Numbers in Modern Personal Finance

Before diving into the technical steps, it is essential to understand why the routing number is a cornerstone of your financial identity. Formally known as an ABA (American Bankers Association) routing transit number (RTN), this nine-digit code serves as an address for your bank. Just as a zip code helps the postal service deliver mail to the correct town, the routing number ensures that funds moving through the electronic banking system find their way to the correct institution.

What is an ABA Routing Number?

The ABA routing number was developed in 1910 to make check processing more efficient. Today, it serves as the backbone for the Automated Clearing House (ACH) network and wire transfers. For a giant like JPMorgan Chase, routing numbers can vary depending on the state where you opened your account. This is a critical distinction in personal finance: using the wrong routing number—such as one for a different region—can lead to delayed payments or failed transfers, which can incur fees or disrupt your financial planning.

Why Your Routing Number Matters for Automated Transactions

In the context of wealth management and side hustles, the routing number is the bridge between your labor and your liquid assets. When you onboard with a new employer or a freelance platform, you are asked for your routing and account numbers to facilitate direct deposit. Similarly, when you automate your savings—transferring a portion of your paycheck to a high-yield savings account or a brokerage firm—the routing number ensures the “handshake” between the two institutions is valid. Understanding how to find and verify this number quickly allows you to maintain the momentum of your financial growth without administrative friction.

2. Step-by-Step Guide: Accessing Your Routing Number via the Chase Mobile® App

The Chase Mobile® app is designed with a focus on user experience, but because it contains a wealth of sensitive data, certain identifiers like routing and account numbers are tucked behind layers of security. Following these steps will allow you to retrieve your information in seconds.

Navigating the Account Dashboard

Upon opening the Chase app, the first screen you encounter is your account dashboard. This view provides a high-level summary of your checking, savings, and credit card balances. To find your routing number, you must first select the specific checking or savings account for which you need the information. In the world of personal finance, it is a common mistake to assume all accounts under one name have the same routing number; while they often do at Chase, it is always best practice to verify the specific account details to ensure accuracy.

Locating the “Account Details” Section

Once you have selected the specific account, look for a link or tab labeled “See details” or “Account details,” usually located near the top of the screen just below your available balance. Tapping this will expand a menu that reveals your full account number (often masked for security) and your nine-digit routing number.

Chase often provides two different routing numbers: one for “Electronic” (ACH/Direct Deposit) and one for “Wire” transfers. It is a vital financial nuance to select the correct one. Electronic routing is used for standard payroll and bill pay, whereas Wire routing is specifically for real-time, high-value transfers that often carry a bank fee. Using an ACH routing number for a wire transfer is a frequent point of failure for many banking customers.

3. Essential Financial Tasks Requiring Your Routing and Account Numbers

Knowing where to find your routing number is the first step toward optimizing your financial workflows. Several key pillars of personal finance rely heavily on the accurate application of these numbers.

Setting Up Direct Deposits for Seamless Income

Direct deposit is the most efficient way to manage cash flow. By providing your Chase routing number to your employer’s payroll department, you eliminate the “float” time associated with paper checks. From a financial strategy perspective, direct deposit also often unlocks premium banking features, such as fee waivers or higher interest rates on linked savings accounts. Ensuring you have the correct regional routing number from the app prevents the administrative headache of a rejected payroll file.

Executing ACH Transfers and Peer-to-Peer Payments

While apps like Zelle (which is integrated into Chase) use phone numbers or emails, traditional ACH transfers between different banks still require routing numbers. If you are moving money from Chase to an external investment account, such as Vanguard or Fidelity, you will need to input your Chase routing details into the external platform. This “pull” or “push” of capital is the engine of an automated investment strategy, allowing you to pay yourself first before you have the chance to spend your discretionary income.

Paying Bills and Managing Recurring Expenses

Automating bill payments through your routing number (using the ACH network) is often more secure and reliable than using a debit card number. Debit cards can expire, be canceled due to fraud, or hit spending limits. A routing number, however, remains constant as long as your account is open. By linking your utility, mortgage, or insurance payments directly to your Chase account via the routing number, you reduce the risk of missed payments and the subsequent negative impact on your credit score.

4. Security and Privacy: Protecting Your Financial Identifiers

In an era of increasing digital fraud, your routing and account numbers are sensitive pieces of financial data. While a routing number is not “secret” in the same way a password is (after all, it is printed on every check you write), it is half of the key required to access your funds.

Identifying Potential Risks of Sharing Routing Numbers

The primary risk of a leaked routing and account number combination is unauthorized ACH withdrawals. Criminals can theoretically use these numbers to pay their own bills or initiate “e-check” payments. As a sophisticated bank user, you should only provide these details to trusted entities, such as your employer, government agencies (like the IRS), or established financial institutions. Avoid sending these numbers via unencrypted email or text messages, as these are vulnerable to interception.

Best Practices for Digital Banking Safety

The Chase app provides several security features to protect your data. Always ensure that biometric authentication (FaceID or Fingerprint) is enabled to prevent unauthorized access to the “Account Details” screen. Furthermore, utilize the “Alerts” feature within the app. By setting up notifications for all “Money Out” transactions, you will receive an immediate push notification if someone uses your routing and account numbers for a transaction, allowing you to contact Chase’s fraud department before the funds have fully cleared the system.

5. Troubleshooting and Alternative Methods to Find Your Details

Occasionally, technology may fail, or the app might be undergoing maintenance. In these instances, there are alternative financial tools and documents at your disposal to find your routing information.

Using the Chase Website or Physical Checks

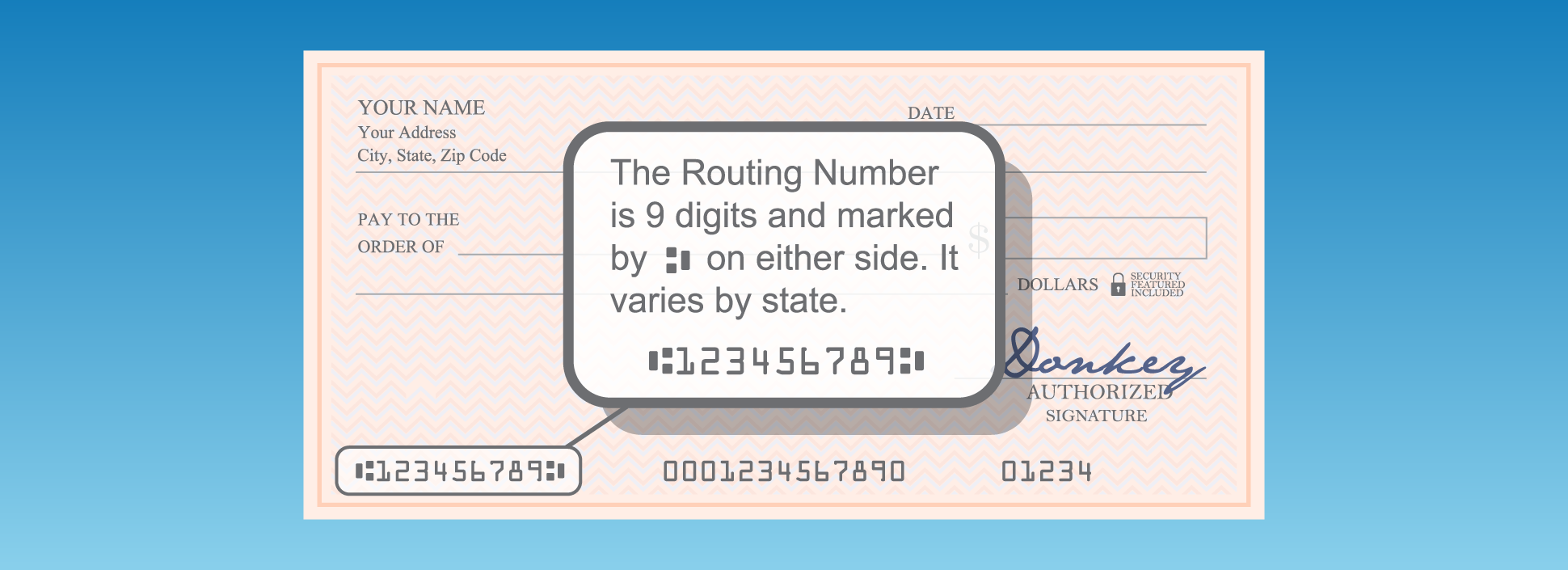

If you cannot access the mobile app, the Chase Online℠ website provides the same information under the “Account Services” tab. Additionally, for those who still use physical checkbooks, your routing number is the first set of nine digits printed at the bottom-left corner of your checks. The second set of digits is your account number, and the third is the check number. Understanding the “anatomy of a check” is a foundational skill in financial literacy that remains relevant even in the digital age.

Contacting Chase Customer Service for Verification

If you are unsure which routing number to use—particularly for international wires or complex business transactions—contacting a Chase representative is the safest route. You can do this through the “Secure Message Center” in the app or by calling the number on the back of your debit card. In the world of finance, it is always better to double-check a number than to deal with the repercussions of a misdirected five-figure wire transfer.

By mastering the navigation of the Chase app and understanding the strategic importance of your routing number, you position yourself as a more capable and secure participant in the digital economy. Whether you are automating your investments or simply ensuring your bills are paid on time, this nine-digit number is a small but mighty tool in your personal finance arsenal.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.