In the complex world of personal finance and business, numbers tell a story. But raw numbers alone often lack the context needed to make informed decisions. A mere dollar amount increase or decrease in an investment, a budget line item, or a business’s revenue doesn’t fully explain the significance of that change. This is where percent increase and decrease become indispensable tools. They provide the crucial context, allowing us to understand the relative magnitude of change, benchmark performance, track progress towards financial goals, and identify critical trends.

Whether you’re an individual managing your household budget, an investor tracking portfolio performance, or a business owner analyzing quarterly reports, the ability to accurately calculate and interpret percentage changes is a cornerstone of financial literacy. It transforms static data into dynamic insights, empowering you to make smarter, more strategic monetary decisions. This comprehensive guide will demystify the process, offering clear explanations, practical formulas, and real-world applications specifically tailored to the realm of money.

The Fundamentals of Percentage Change

Before diving into the calculations, it’s essential to grasp the foundational concepts that underpin percent increase and decrease. These calculations are not just mathematical exercises; they are lenses through which we view financial performance and make comparative judgments.

Understanding Percentages as Proportions

At its core, a percentage is a way of expressing a number as a fraction of 100. For instance, 25% means 25 out of 100, or 0.25 as a decimal. In financial contexts, percentages allow us to standardize comparisons, regardless of the absolute values involved. If your stock gained $5, and another stock gained $5, a percentage tells you which gain was more significant relative to its initial value.

Why Percentage Change Matters More Than Absolute Change

Consider two scenarios:

- Your investment account grew from $1,000 to $1,100. (An absolute increase of $100).

- Your investment account grew from $100,000 to $100,100. (An absolute increase of $100).

While the absolute increase is the same ($100) in both cases, their financial significance is vastly different. In the first scenario, a $100 increase represents a substantial 10% gain ($100/$1,000), indicating strong performance. In the second, a $100 increase is a mere 0.1% gain ($100/$100,000), which is almost negligible.

This highlights why percentage change is often a more powerful metric than absolute change, especially when comparing different scales, timeframes, or entities. It provides a standardized measure of growth or decline, allowing for meaningful analysis and benchmarking across diverse financial situations. Without it, you might misinterpret success or failure, leading to suboptimal financial choices.

Calculating Percent Increase: Growing Your Financial Insight

Understanding how to calculate percent increase is crucial for recognizing positive financial trends, assessing investment returns, and tracking the growth of income or assets. It empowers you to quantify success and understand the momentum behind your financial progress.

The Core Formula for Percent Increase

The formula for percent increase is straightforward and intuitively reflects the magnitude of growth relative to an original starting point:

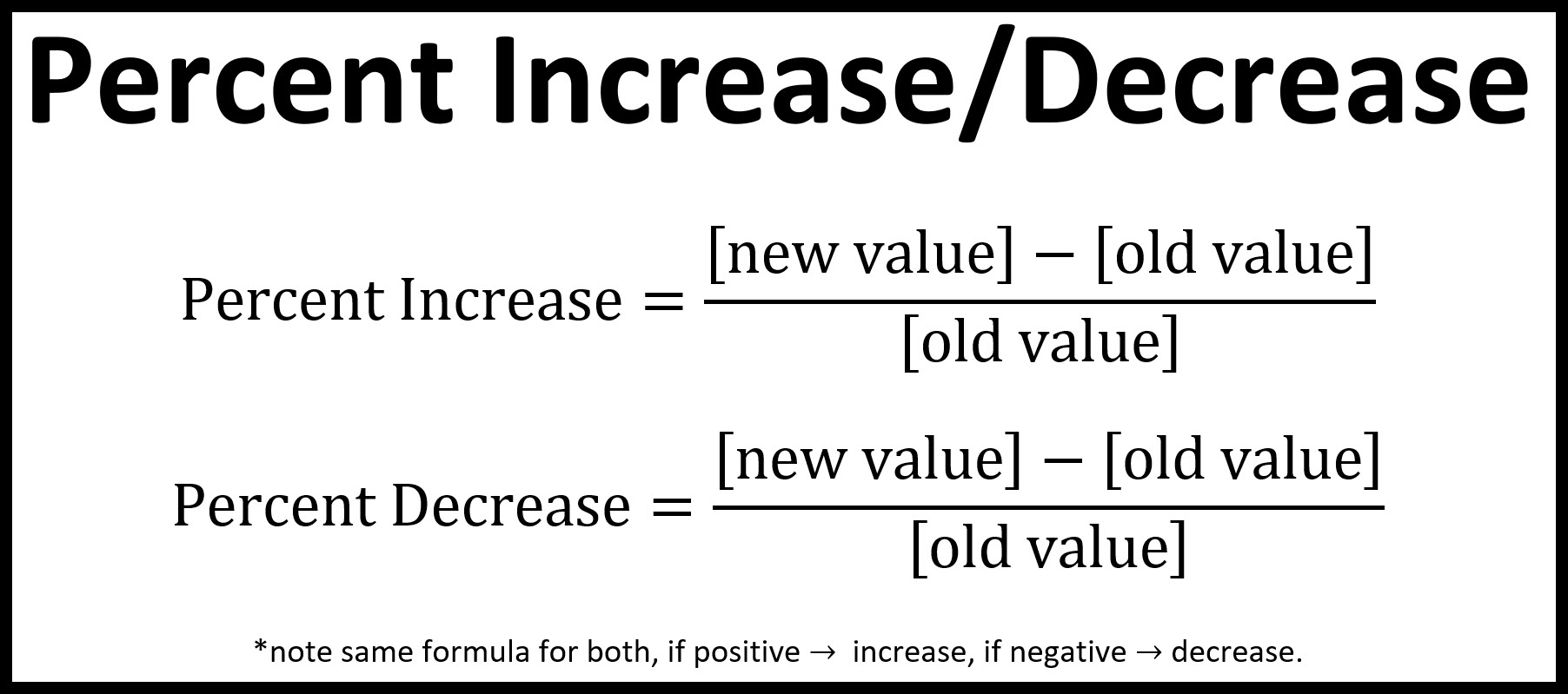

Percent Increase = ((New Value – Original Value) / Original Value) × 100%

Let’s break down each component:

- New Value: The current or final amount after the increase.

- Original Value: The starting amount before the increase.

- New Value – Original Value: This calculates the absolute amount of the increase.

- Divide by Original Value: This step normalizes the increase, expressing it as a proportion of the starting value.

- Multiply by 100%: Converts the decimal proportion into a percentage.

Example: If your stock portfolio was worth $20,000 at the beginning of the year and grew to $22,500 by year-end:

- Absolute Increase = $22,500 – $20,000 = $2,500

- Proportionate Increase = $2,500 / $20,000 = 0.125

- Percent Increase = 0.125 × 100% = 12.5%

Your portfolio experienced a 12.5% increase.

Practical Applications in Personal Finance

- Investment Growth: Calculate the return on investment (ROI) for stocks, mutual funds, or real estate. Knowing the percentage growth helps you compare different investment vehicles over various periods.

- Salary Raises and Income Growth: Track how your income is increasing year over year. A 5% raise on a $50,000 salary is a clear $2,500 bump, which is more easily understood in percentage terms when comparing it to inflation or other economic benchmarks.

- Budgetary Increases: If your grocery bill goes from $400 to $450, you’ve experienced a 12.5% increase, signaling a need to re-evaluate spending or adjust your budget.

- Inflation’s Impact: Understanding the percent increase in the cost of living helps you assess if your income growth is truly keeping pace, or if your purchasing power is diminishing.

Business Finance Perspective

For businesses, percent increase is a vital metric for evaluating performance and setting strategic goals:

- Revenue Growth: A company might aim for a 10% year-over-year revenue increase, allowing for easy comparison across quarters or against competitors.

- Profit Margin Expansion: Tracking the percentage increase in profit margins indicates improved operational efficiency or pricing power.

- Market Share Increase: Quantifying the growth in a company’s market share helps gauge its competitive standing.

Calculating Percent Decrease: Identifying Trends and Managing Risk

Just as important as understanding growth is the ability to quantify decline. Percent decrease helps identify areas of financial concern, track progress in debt reduction, and evaluate losses in investments or reductions in expenses. It’s a critical tool for risk management and prudent financial planning.

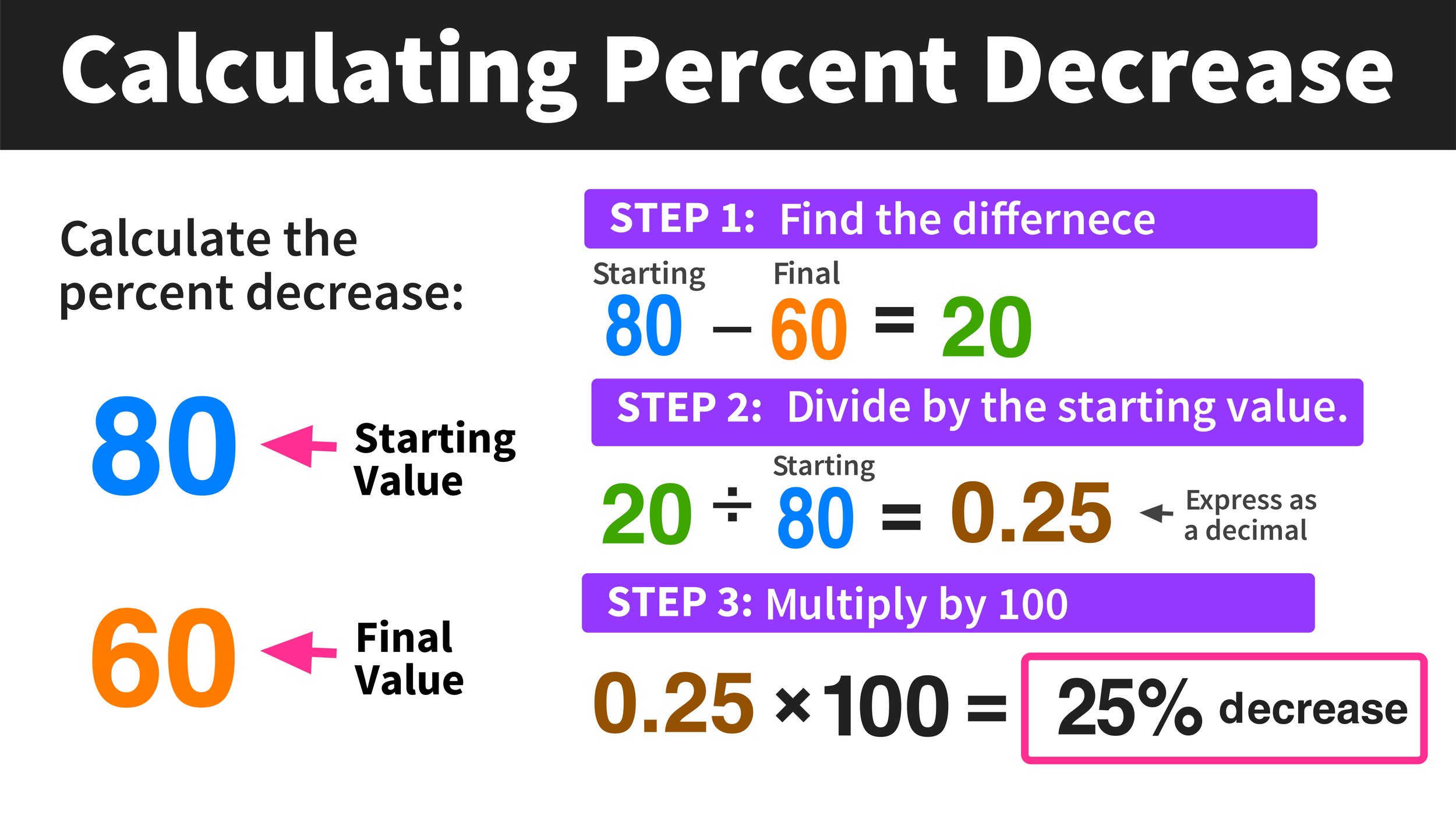

The Core Formula for Percent Decrease

The formula for percent decrease is conceptually similar to percent increase, with a slight adjustment to ensure a positive percentage result and proper contextualization:

Percent Decrease = ((Original Value – New Value) / Original Value) × 100%

Notice the change in the numerator:

- Original Value – New Value: This calculates the absolute amount of the decrease. By subtracting the new (smaller) value from the original (larger) value, we ensure the numerator is positive.

- The rest of the formula mirrors the increase calculation, dividing by the Original Value to get a proportion and then multiplying by 100%.

Example: If your monthly utility bill decreased from $150 to $120 after implementing energy-saving measures:

- Absolute Decrease = $150 – $120 = $30

- Proportionate Decrease = $30 / $150 = 0.20

- Percent Decrease = 0.20 × 100% = 20%

You achieved a 20% decrease in your utility bill.

Practical Applications in Personal Finance

- Investment Losses: If a stock you own drops from $50 per share to $45 per share, that’s a 10% decrease. Understanding this helps you assess risk and potentially make decisions about selling or holding.

- Debt Reduction: Tracking the percentage decrease in your outstanding mortgage or credit card balance provides powerful motivation and a clear measure of progress towards financial freedom.

- Expense Reductions in a Budget: Actively working to cut discretionary spending (e.g., dining out) and seeing a 25% decrease month-over-month validates your efforts and reinforces good habits.

- Depreciation of Assets: Understanding the percentage decrease in the value of assets like cars helps in financial planning for future replacements.

Business Finance Perspective

For businesses, calculating percent decrease is crucial for diagnosing problems and improving efficiency:

- Sales Declines: A 5% decrease in quarterly sales can signal market shifts, competitive pressures, or internal issues that need immediate attention.

- Cost Reductions: Successfully reducing operating costs by 15% directly impacts profitability, and this percentage allows for easy comparison of efficiency improvements.

- Inventory Shrinkage: A percentage decrease in inventory due to theft or damage highlights operational vulnerabilities.

- Market Share Contraction: A decrease in market share signals a loss of competitive standing and the need for strategic adjustments.

Common Pitfalls and Advanced Considerations

While the formulas for percent increase and decrease are straightforward, there are subtle nuances and common mistakes that can lead to misinterpretations. Being aware of these advanced considerations ensures your financial analysis is robust and accurate.

The “Base Value” Trap: Always Use the Original

One of the most frequent errors in calculating percentage change is using the wrong base value (denominator). Always remember to use the original or starting value.

Common Mistake Example: An item costs $100. It increases in price by 10%, making it $110. Then, the price decreases by 10%. Many might assume it returns to $100.

- Incorrect Calculation: 10% of $110 (the new value) is $11. So $110 – $11 = $99. This is wrong.

- Correct Calculation: The decrease is 10% of the current value ($110). So, 10% of $110 = $11. New price = $110 – $11 = $99.

- To return to $100 from $110, the decrease needed would be $10.

- Percent decrease from $110 to $100 would be (($110 – $100) / $110) * 100% = ($10 / $110) * 100% ≈ 9.09%.

- This demonstrates that a 10% increase followed by a 10% decrease does not lead back to the original amount unless the base changes. Always be clear about what your “original value” is for each calculation.

Multiple Percentage Changes: Not Simply Additive

When multiple percentage changes occur sequentially, they don’t simply add or subtract. This is known as compounding.

Example: An investment grows by 10% in Year 1 and then by another 10% in Year 2.

- If you started with $1,000:

- Year 1: $1,000 + (0.10 * $1,000) = $1,100

- Year 2: $1,100 + (0.10 * $1,100) = $1,210

- The total increase is $210, which is a 21% increase from the original $1,000, not 20%. Each percentage change applies to the new current value, not the initial starting value. This is critical in understanding investment growth, compound interest, and inflation.

Understanding Basis Points

While percentage changes are common, in professional financial contexts, especially regarding interest rates, bond yields, and market fluctuations, you might encounter “basis points” (bps). One basis point is equal to 0.01% (one-hundredth of a percent), or 0.0001 as a decimal.

- A change of 50 basis points means a 0.50% change.

- This precision is often used to describe very small but significant shifts in financial markets.

Real vs. Nominal Changes

When discussing financial changes over time, particularly income, investment returns, or the cost of living, it’s crucial to distinguish between nominal and real values.

- Nominal Change: The raw percentage increase or decrease without accounting for inflation.

- Real Change: The percentage increase or decrease after adjusting for inflation, reflecting the actual change in purchasing power.

For instance, if your salary increases by 3% (nominal increase) but inflation was 2.5%, your real salary increase is only 0.5%. Understanding this distinction is vital for accurate long-term financial planning and wealth preservation.

Leveraging Percent Change for Strategic Financial Decisions

Mastering the calculation of percent increase and decrease is not merely an academic exercise; it’s a practical skill that directly translates into more effective financial management. By applying these calculations strategically, you can gain deeper insights and make more informed decisions across various financial domains.

Goal Setting and Tracking

Percentage changes provide a clear and quantifiable way to set financial goals and monitor your progress towards them.

- Savings Goals: Instead of saying “I want to save more,” you can set a target: “I want to increase my monthly savings by 15% this quarter.” This gives you a tangible benchmark to aim for and track.

- Debt Repayment: Monitor the percentage decrease in your outstanding loan balances. Seeing that your credit card debt has decreased by 20% in six months can be highly motivating.

- Investment Performance: Set goals for annual portfolio growth (e.g., “I aim for a 7% average annual return”). Regularly calculating percent increase helps you stay on track or adjust your strategy if you’re falling short.

Comparative Analysis

Percentage changes are invaluable for comparing financial performance across different entities, timeframes, or benchmarks.

- Benchmarking Investments: Compare the percentage return of your investment portfolio against relevant market indices (e.g., S&P 500) or industry averages. A 10% return might sound good, but if the market returned 15%, you’ve underperformed.

- Evaluating Business Performance: A business can compare its current quarter’s revenue growth percentage to previous quarters, annual targets, or the growth rates of competitors to assess its relative success.

- Budgetary Review: Compare the percentage change in various spending categories month-over-month or year-over-year. Did your housing costs increase disproportionately compared to your income?

Risk Assessment and Opportunity Identification

Analyzing percentage changes can highlight potential financial risks or lucrative opportunities.

- Identifying Financial Red Flags: A sustained percentage decrease in business revenue or a sudden percentage increase in an expense category can be an early warning sign of underlying problems that require immediate attention. Similarly, a significant percentage drop in a stock’s price might signal trouble, prompting a review of your investment.

- Spotting Investment Opportunities: A stock that has historically shown consistent percentage growth, or one that has experienced a temporary but sharp percentage decrease due to external factors (not fundamental issues), might represent a buying opportunity.

- Managing Debt: Tracking the percentage increase in interest rates on variable loans helps you anticipate rising costs and plan for potential refinancing or accelerated repayment.

Conclusion

The ability to calculate and interpret percent increase and decrease is far more than a basic mathematical skill; it is a fundamental pillar of financial literacy. In a world saturated with data, these simple yet powerful calculations provide the context needed to transform raw numbers into actionable insights.

From monitoring personal investment growth and managing household budgets to analyzing business performance and identifying market trends, percentage changes offer a standardized, comparable, and deeply insightful perspective on financial dynamics. By understanding the core formulas, recognizing common pitfalls like the base value trap, and applying these concepts strategically, you empower yourself to make smarter, more confident, and ultimately more successful financial decisions. Embrace these calculations, integrate them into your financial routines, and unlock a deeper understanding of your money’s journey.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.