Navigating the complexities of tax season can be daunting, and one of the most pressing questions many individuals face is simply, “How much do I owe the IRS?” Whether you’re proactively preparing for the upcoming tax deadline, trying to understand a recent notice, or simply seeking clarity on your financial obligations, having a clear picture of your tax liability is paramount. It’s not just about compliance; it’s about informed financial planning, avoiding penalties, and ensuring peace of mind.

Ignoring or being unaware of your tax debt can lead to significant financial repercussions, including interest accruals and various IRS penalties. Conversely, understanding your exact obligation empowers you to strategize effectively, explore payment options, and even identify potential discrepancies. This guide will walk you through the most reliable and efficient methods to ascertain your IRS tax liability, equipping you with the knowledge to manage your financial responsibilities confidently and proactively. From leveraging official IRS online tools to understanding the nuances of tax transcripts and the importance of professional advice, we’ll cover all the essential steps to demystify your tax situation.

The Indisputable Importance of Knowing Your Tax Obligation

Understanding precisely how much you owe the Internal Revenue Service (IRS) is far more than a mere administrative formality; it’s a cornerstone of sound personal finance and fiscal responsibility. The clarity it provides acts as a shield against potential pitfalls and a catalyst for strategic financial decisions.

Avoiding Penalties and Interest

One of the most compelling reasons to stay informed about your tax debt is to circumvent the costly penalties and interest charges that the IRS can levy. The IRS is meticulous about compliance, and failure to pay by the due date can result in a failure-to-pay penalty, which is typically 0.5% of the unpaid taxes for each month or part of a month that taxes remain unpaid, up to a maximum of 25%. On top of this, interest accrues on underpayments, and this interest rate can change quarterly. By knowing your exact liability, you can ensure timely payments or proactively arrange a payment plan, thereby mitigating or entirely eliminating these additional financial burdens. Proactive engagement can save you substantial amounts that would otherwise be lost to avoidable charges.

Effective Financial Planning and Budgeting

Knowing your tax obligations allows you to integrate this significant financial commitment into your overall budget and financial planning. For individuals and businesses alike, tax payments represent a substantial outgoing. Without a clear figure, it’s impossible to accurately assess your disposable income, savings potential, or investment capacity. When you’re aware of what you owe, you can allocate funds appropriately, set aside the necessary amounts, and prevent your tax bill from becoming an unexpected financial shock. This level of foresight enables better cash flow management, allows for better allocation of funds towards other financial goals like retirement savings or debt reduction, and fosters a more robust financial future.

Peace of Mind and Reduced Stress

Beyond the tangible financial benefits, there’s an invaluable psychological advantage to knowing your tax status: peace of mind. The unknown can be a significant source of stress and anxiety, particularly when it involves government agencies and potential financial penalties. Having a clear, accurate understanding of your tax liability eliminates the guesswork and allows you to address the situation head-on. This transparency reduces the lingering worry about what the IRS might communicate next and empowers you to take control. When you are informed, you can make confident decisions, whether that involves making a payment, setting up a payment plan, or seeking professional advice, all contributing to a less stressful financial life.

Primary Methods to Check Your IRS Tax Liability

The IRS has made significant strides in providing accessible tools and resources for taxpayers to ascertain their current tax liability. Leveraging these official channels is the most reliable way to get accurate information directly from the source.

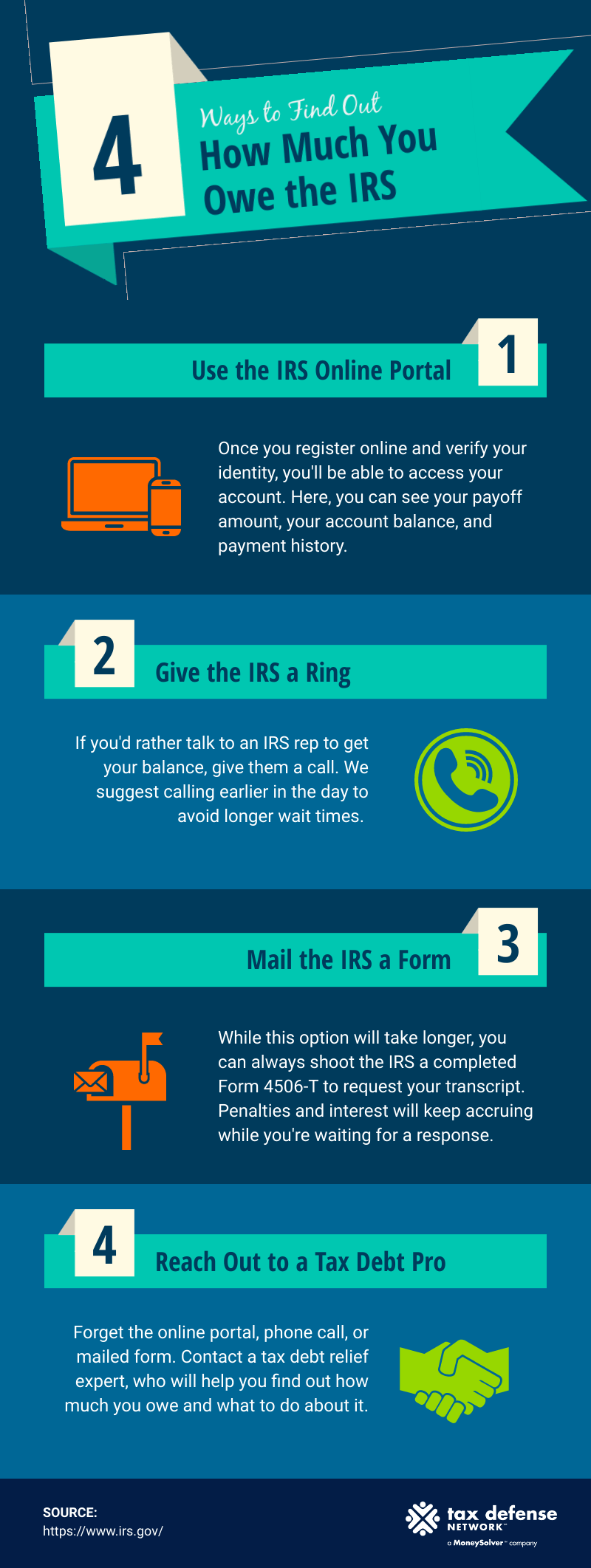

Reviewing Your IRS Online Account

The IRS Online Account is arguably the most convenient and comprehensive resource for checking your tax debt. This secure online portal allows individual taxpayers to access a wealth of information related to their federal tax accounts, often without needing to contact the IRS directly.

To access your account, you will need to register and verify your identity, a process that ensures the security of your sensitive financial data. Once logged in, you can typically:

- View Your Balance Due: This will show the total amount you owe, including any accrued penalties and interest for current or prior tax years.

- See Your Payment History: You can review payments you’ve made, which helps reconcile your records.

- Access Your Tax Records: This includes key data from your most recently filed tax return.

- Manage Payment Plans: If you have an existing payment plan, you can view details and make adjustments.

- Get Tax Transcripts: You can request and view various tax transcripts directly through your online account.

Setting up and regularly checking your IRS Online Account is a proactive step that provides an invaluable, up-to-date snapshot of your tax situation, making it an essential tool for managing your tax obligations.

Checking Your Tax Transcripts

Tax transcripts are detailed summaries of your tax information as reported to the IRS. While not a copy of your tax return, they provide line-by-line data that can help you determine your tax liability, especially if you no longer have your original returns or need to verify information. There are several types of transcripts, each serving a slightly different purpose:

- Account Transcript: This transcript shows most line items from your original tax return, along with any adjustments made by you or the IRS, and your payment history. It will clearly display any balance due.

- Record of Account Transcript: This combines the information from the account transcript with line items from your original tax return, making it a comprehensive view of your tax account.

- Wage and Income Transcript: This displays information from various forms like W-2s, 1099s, and 1098s, which is useful for reconstructing your income if you’ve lost these forms. While it doesn’t directly show your tax owed, it’s crucial for calculating it.

You can request tax transcripts online, by mail (Form 4506-T), or by phone. The “Get Transcript Online” tool on the IRS website is generally the quickest method. It’s important to review these transcripts carefully, as they directly reflect the IRS’s understanding of your tax obligations.

Consulting Your Filed Tax Returns and Records

Your own meticulously maintained records are often the first and most immediate resource for understanding your tax liability. If you have filed your tax returns, the final page of your Form 1040 (or the relevant business tax form) will clearly indicate whether you are due a refund or if you owe additional tax.

Key documents to review include:

- Form 1040 (U.S. Individual Income Tax Return): This is the foundational document that summarizes your income, deductions, credits, and ultimately, your tax liability. Look for the “Amount You Owe” line.

- Schedules: Any schedules attached to your 1040 (e.g., Schedule 1 for additional income/adjustments, Schedule A for itemized deductions, Schedule C for business profit/loss) contribute to the final calculation.

- W-2s, 1099s, K-1s: These forms detail your income from various sources and show federal income tax withheld. Comparing your total tax withheld against your total tax liability on Form 1040 will reveal any underpayment or overpayment.

By keeping organized digital or physical copies of all your tax filings and supporting documents, you have a ready-made audit trail and an immediate reference point for your tax obligations. This method relies on the accuracy of your original filing, but it’s an essential first step for verification.

What to Do If You Owe Money to the IRS

Discovering you owe money to the IRS, while not ideal, is a manageable situation. The critical next step is to understand your options and act promptly. The IRS offers various avenues for payment and assistance to taxpayers facing a liability.

Understanding Your Payment Options

The IRS provides several convenient methods for making tax payments. Choosing the right one depends on your preferences and financial situation.

- IRS Direct Pay: This free service allows you to pay directly from your checking or savings account. It’s a secure, fast, and simple way to make payments for various tax types, including estimated taxes and payments associated with your filed return. You’ll receive instant confirmation.

- Debit Card, Credit Card, or Digital Wallet: You can pay your taxes using a third-party payment processor. While convenient, these processors typically charge a small fee for their service. This option can be useful if you need to use a credit card for cash flow management or to earn rewards points.

- Electronic Federal Tax Payment System (EFTPS): This is a free service provided by the U.S. Department of the Treasury. It’s primarily used by businesses but is also available to individuals. It requires enrollment but allows you to schedule payments up to 365 days in advance and review your payment history.

- Check or Money Order: You can mail a check or money order directly to the IRS. Ensure it’s made payable to the “U.S. Treasury” and includes your name, address, daytime phone number, Social Security number, the tax year, and the related tax form or notice number. This is the slowest method and should be sent well in advance of the deadline.

Selecting an appropriate payment method and executing the payment promptly can help you avoid further penalties and interest.

Exploring Payment Plans and Agreements

If you can’t pay your full tax liability by the due date, it’s crucial not to panic and, more importantly, not to ignore the problem. The IRS understands that financial difficulties can arise and offers various payment arrangements.

- Short-Term Payment Plan: If you can pay your tax liability in full within 180 days, you might qualify for a short-term payment plan. While interest and penalties still apply, this option provides flexibility and prevents further enforcement actions.

- Installment Agreement: If you need more time, an installment agreement allows you to make monthly payments for up to 72 months. This option is available if you owe a combined total of under $50,000 (for individuals) or $25,000 (for businesses) in tax, penalties, and interest. While an installment agreement is in place, certain penalties may be reduced. You can apply for an installment agreement online, by phone, or by mail.

- Offer in Compromise (OIC): An OIC allows certain taxpayers to resolve their tax debt with the IRS for a lower amount than they originally owed. This option is typically considered when a taxpayer is experiencing significant financial hardship and cannot pay their full tax liability. The IRS will evaluate your ability to pay, income, expenses, and asset equity. An OIC is a complex process and is not available to everyone.

Proactively engaging with the IRS to set up a payment plan or explore an OIC demonstrates good faith and can prevent aggressive collection actions like liens or levies.

Seeking Professional Help

For complex tax situations, significant tax debt, or when you’re unsure how to proceed, seeking professional assistance is highly recommended. Tax professionals can provide invaluable guidance and representation.

- Enrolled Agents (EAs): EAs are federally authorized tax practitioners who are empowered by the U.S. Department of the Treasury to represent taxpayers before the IRS. They are experts in tax law and can help with audits, collections, and appeals.

- Certified Public Accountants (CPAs): CPAs are licensed accounting professionals who can assist with tax preparation, planning, and representation before the IRS. Their broad expertise often covers both tax and financial advisory services.

- Tax Attorneys: For highly complex cases, such as those involving significant disputes, criminal tax issues, or substantial debt, a tax attorney can provide legal counsel and representation.

A qualified professional can help you understand your full financial picture, negotiate with the IRS on your behalf, ensure you comply with all regulations, and ultimately work towards the most favorable outcome for your tax debt situation. Their expertise can save you time, stress, and potentially a significant amount of money.

Proactive Measures to Prevent Future Surprises

While knowing how much you owe is crucial, preventing future tax surprises is an even better strategy. A proactive approach to tax planning can help you avoid underpayment penalties, manage your cash flow effectively, and maintain a healthier financial outlook year after year.

Adjusting Your Withholding (Form W-4)

For most wage earners, federal income tax is withheld from each paycheck by their employer based on the information provided on Form W-4, Employee’s Withholding Certificate. If too little is withheld, you’ll owe tax at the end of the year and might face penalties. If too much is withheld, you’ll get a refund, but you’re essentially giving the government an interest-free loan throughout the year.

Reviewing and adjusting your W-4 annually, or whenever there’s a significant life event (marriage, divorce, birth of a child, new job, or significant change in income), is critical. The IRS Tax Withholding Estimator tool on their website is an excellent resource to help you accurately determine how much tax should be withheld from your pay. Properly adjusted withholding ensures that you pay just enough throughout the year to cover your liability, minimizing both underpayment and excessive overpayment.

Making Estimated Tax Payments (Form 1040-ES)

If you’re self-employed, own a business, receive income that isn’t subject to withholding (like interest, dividends, rent, or alimony), or if your W-4 adjustments aren’t sufficient, you might need to make estimated tax payments. The U.S. tax system operates on a “pay-as-you-go” basis, meaning you’re expected to pay income tax as you earn or receive income throughout the year.

Estimated taxes are typically paid in four equal installments throughout the year using Form 1040-ES, Estimated Tax for Individuals. Missing these payments or underpaying can lead to penalties. It’s vital to accurately project your income and deductions for the year to calculate these payments. If your income fluctuates, you may need to adjust your estimated payments quarterly. Keeping good records of your income and expenses is paramount for accurate estimation.

Maintaining Meticulous Records

The foundation of accurate tax preparation and effective financial planning lies in diligent record-keeping. Organized records are your best defense in case of an IRS inquiry or audit, and they make preparing your tax return significantly easier and more accurate.

Keep all documents related to your income (W-2s, 1099s, K-1s), expenses (receipts for deductible items, business expenses), deductions (mortgage interest statements, charitable contributions), and credits (child care expenses, education expenses) in a centralized and accessible manner. Digital copies, cloud storage, or dedicated tax software can simplify this process. Having these records readily available allows you to verify figures, justify claims, and quickly ascertain your financial standing relative to your tax obligations.

Staying Informed About Tax Law Changes

Tax laws are not static; they change regularly, often annually, due to new legislation or adjustments by the IRS. These changes can significantly impact your tax liability, affecting everything from tax brackets and standard deductions to available credits and deductions.

Subscribing to IRS news releases, reputable financial news outlets, or consulting with a tax professional can help you stay abreast of these changes. Understanding how new laws might affect your income, investments, or business operations enables you to adjust your financial strategies proactively, ensuring ongoing compliance and optimizing your tax position. Ignorance of tax law is not an excuse for non-compliance, so continuous learning is a key aspect of preventing tax surprises.

Conclusion

Understanding “how to find out how much you owe to the IRS” is a fundamental aspect of responsible financial management. It’s a proactive step that safeguards you from unforeseen penalties, empowers effective budgeting, and ultimately brings invaluable peace of mind. By leveraging the comprehensive tools offered by the IRS – from your personalized Online Account to detailed tax transcripts – and diligently maintaining your own financial records, you can gain a clear, accurate picture of your tax liability.

Moreover, knowing your obligations isn’t just about discovery; it’s about action. Whether you utilize the IRS’s various convenient payment options or explore flexible payment plans like installment agreements or offers in compromise, there are structured pathways to resolve your debt. For those navigating particularly complex situations, the expertise of enrolled agents, CPAs, or tax attorneys can prove indispensable, offering professional guidance and representation.

Beyond addressing immediate debt, cultivating proactive tax habits is the ultimate strategy. Regularly adjusting your withholding, making timely estimated tax payments, meticulously maintaining records, and staying informed about evolving tax laws will help prevent future surprises and foster a more stable financial future. Empower yourself with knowledge, take timely action, and transform the often-dreaded task of tax management into a confident and controlled aspect of your personal finance journey.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.