Understanding your monthly income is not just a numerical exercise; it’s a foundational pillar of personal finance, empowering you to make informed decisions about spending, saving, investing, and debt management. Many people operate with a vague idea of what they earn, often recalling only their primary salary. However, a comprehensive understanding requires a deeper dive into all revenue streams, deductions, and financial tools available. This guide will walk you through the essential steps to accurately determine your monthly income, explain why this figure is so crucial, and provide practical strategies for tracking and optimizing it.

Understanding What Constitutes “Income”

Before you can find your monthly income, you must first define what income truly means in your personal financial context. It’s more than just the number on your paycheck; it encompasses every source of money flowing into your accounts.

Differentiating Gross vs. Net Income

The very first distinction to make is between gross and net income.

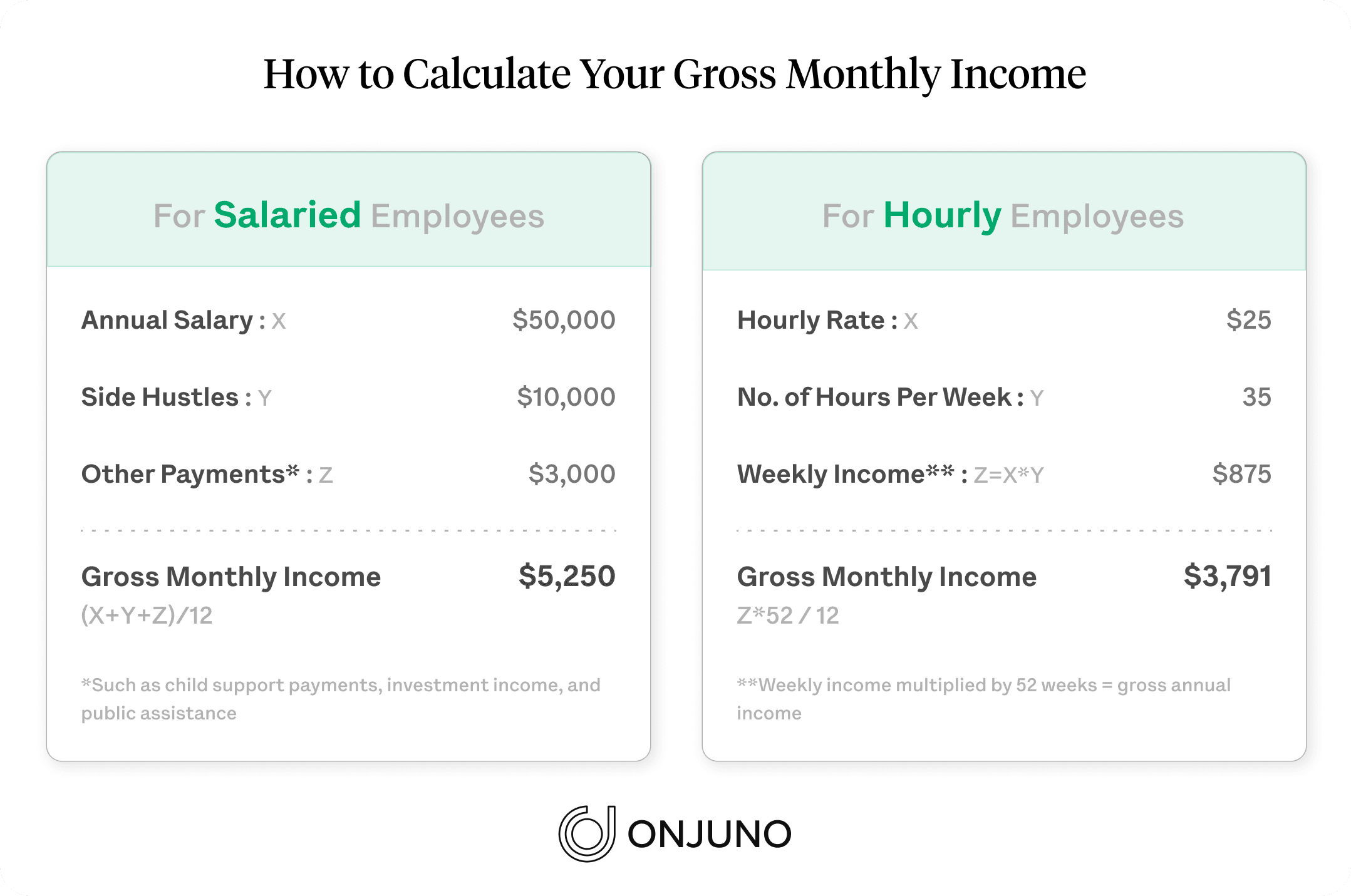

- Gross Income is your total earnings before any taxes, deductions, or withholdings are taken out. This is the figure often quoted in job offers or salary discussions. For a salaried employee, it’s straightforward. For freelancers or business owners, it’s their total revenue before business expenses.

- Net Income, also known as “take-home pay,” is the amount you actually receive after all mandatory and voluntary deductions. These deductions typically include federal, state, and local taxes, Social Security, Medicare, retirement contributions (401k, IRA), health insurance premiums, and other benefits. When discussing your disposable income for budgeting, net income is the figure that truly matters.

Understanding both is vital. Gross income gives you a full picture of your earning power, while net income reflects the funds you have available for immediate use.

Identifying All Income Streams

Most people have multiple income streams, even if they don’t consciously think of them that way. To get an accurate monthly income figure, you need to meticulously list every source of funds.

- Primary Employment Wages/Salary: This is often the most significant component. For salaried employees, it’s a fixed amount. For hourly workers, it fluctuates based on hours worked and overtime.

- Freelance or Gig Economy Earnings: Income from side hustles, consulting, ride-sharing, food delivery, creative projects, or any other independent contractor work. These often vary significantly month-to-month.

- Investment Income: Dividends from stocks, interest from savings accounts, CDs, bonds, or rental income from properties. While some might be paid quarterly or annually, they can be averaged monthly.

- Social Benefits: Social Security, disability payments, unemployment benefits, child support, or alimony.

- Retirement or Pension Income: If applicable, for those in retirement.

- Miscellaneous Income: This can include reimbursements, gifts, lottery winnings, refunds, or even occasional sales of personal items. While not always predictable, significant one-off amounts should be noted.

The Importance of Consistency

When compiling your income streams, consider their consistency. Fixed salaries are easy to project. Variable income from freelancing or bonuses requires averaging over several months or even a year to get a realistic monthly figure. Ignoring less consistent income sources can lead to an underestimation of your total earnings, but over-relying on highly volatile income can create budgeting challenges.

Practical Methods for Tracking Your Income

Once you understand what income entails, the next step is to gather the data. Fortunately, various tools and methods can help you systematically track and consolidate your earnings.

Leveraging Bank Statements and Pay Stubs

These are your primary sources of verifiable income data.

- Pay Stubs (or Wage Statements): For employees, your pay stub is a treasure trove of information. It clearly outlines your gross pay, all deductions, and your net pay for that pay period. Reviewing several pay stubs (e.g., from the last three months) will help you average out any slight variations due to overtime or fluctuating benefits.

- Bank Statements: Every deposit you receive will appear on your bank statement. This is especially useful for tracking irregular income, freelance payments, investment dividends, or transfers. Go through at least three to six months of statements, highlighting every inflow that constitutes income. Be careful to differentiate actual income from transfers between your own accounts or loan disbursements.

Utilizing Budgeting Apps and Software

Technology has revolutionized personal finance tracking. Numerous apps and software solutions can automatically categorize transactions and help you visualize your income.

- Financial Aggregators: Tools like Mint, Personal Capital, YNAB (You Need A Budget), or Simplifi link directly to your bank accounts, credit cards, and investment accounts. They automatically import transactions, categorize them, and often provide dashboards that show your total income over various periods. This automation significantly reduces manual effort.

- Spreadsheet Software: For those who prefer a more hands-on approach, Google Sheets or Microsoft Excel offer immense flexibility. You can create custom templates to log each income source, calculate totals, and even build charts to visualize your income trends over time. While requiring manual entry or careful data import, it offers complete control.

Manual Tracking: Spreadsheets and Notebooks

For individuals who prefer a non-digital approach or have very simple finances, a physical notebook or a simple spreadsheet can be effective.

- Income Log: Dedicate a section to logging every income payment received. Include the date, source, gross amount, deductions (if applicable), and net amount. Summing these up at the end of the month will give you your total.

- Calendar Method: Mark your paydays and other expected income on a calendar. When the money arrives, note the amount. This provides a visual record of your cash flow.

Reviewing Tax Documents

Your tax returns (e.g., Form 1040) and supporting documents (W-2s, 1099s) from previous years offer an excellent summary of your total annual income. While this is an annual figure, dividing it by 12 gives you a solid estimate of your average monthly income from the past year. This is particularly useful for consolidating all taxable income sources, including those you might have overlooked.

Calculating Your Average Monthly Income

Once you’ve identified all your income streams and gathered the relevant data, the next step is to consolidate and calculate your average monthly income. This is crucial, especially when dealing with variable income.

Handling Irregular Income Streams

This is where many people get tripped up. If you have income that fluctuates (e.g., freelance work, commissions, bonuses), you can’t just use the last month’s figure.

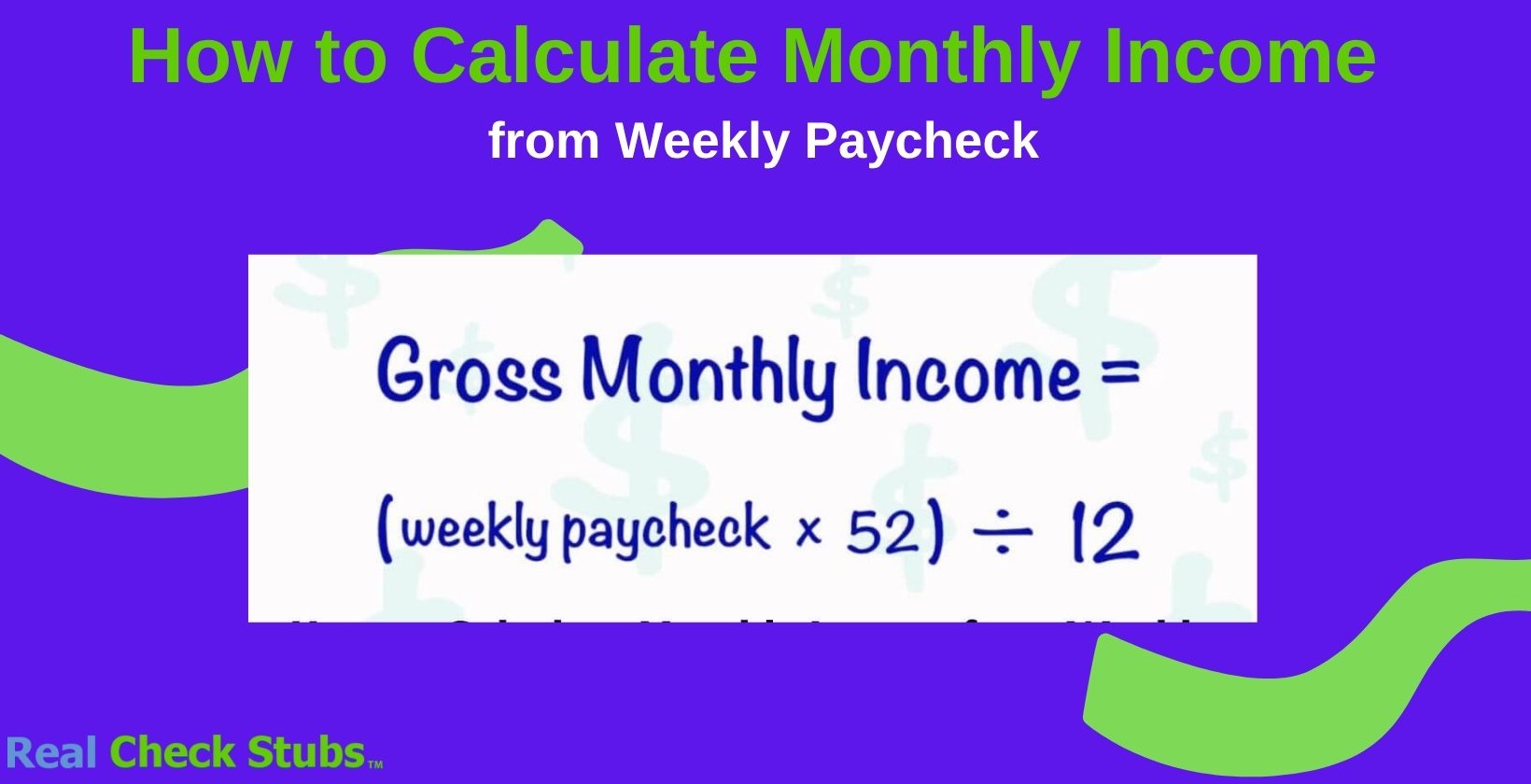

- Average Over Time: Take your total income from these variable sources over a longer period, such as 3, 6, or even 12 months, and then divide by the number of months. For example, if you earned $12,000 from freelance work over the past year, your average monthly freelance income is $1,000.

- Conservative Estimates: When in doubt or if your irregular income is highly unpredictable, it’s often wise to use a conservative estimate. Budget with a lower average to avoid overspending based on an unusually good month.

Annualizing and Averaging

For truly fixed income sources (like a salary), you might have quarterly or semi-annual payments (e.g., some investment dividends). To get a monthly figure:

- Annualize: Multiply your fixed pay-period income by the number of pay periods in a year (e.g., bi-weekly pay x 26, semi-monthly x 24). This gives you your annual income.

- Average: Divide your total annual income (sum of all annualized sources + averaged irregular sources) by 12. This provides your comprehensive average monthly income.

The Role of Historical Data

Consistent tracking over several months or even a year provides the most accurate picture. Historical data allows you to:

- Identify Trends: See if your income is growing, stagnant, or declining.

- Account for Seasonality: Some businesses or jobs have peak seasons. Historical data helps you factor these fluctuations into your monthly average.

- Forecast: A robust history allows for more accurate future income projections.

Adjusting for Seasonal Variations

If your income is highly seasonal (e.g., a landscaper, a retail worker during holidays), calculating a simple 12-month average is essential. However, for budgeting purposes, you might consider creating a “seasonal budget” where your spending adjusts to anticipated income variations, or you could aim to save aggressively during peak months to cover leaner periods.

Why Knowing Your Monthly Income Is Crucial

Calculating your monthly income isn’t just an academic exercise; it’s the bedrock of sound financial health. This single figure underpins almost every major financial decision you’ll make.

Foundation for Budgeting and Financial Planning

The most immediate and critical application of knowing your monthly income is budgeting. Without this figure, any budget you create is merely guesswork.

- Realistic Spending Limits: Knowing exactly how much you take home allows you to set realistic limits on discretionary spending (e.g., entertainment, dining out, shopping) and allocate funds for fixed expenses (rent, utilities).

- Savings Allocation: You can confidently decide how much to allocate to various savings goals, whether it’s an emergency fund, a down payment, or retirement.

- Expense-to-Income Ratio: You can assess if your expenses are sustainable relative to your income. A general rule of thumb, like the 50/30/20 rule (50% needs, 30% wants, 20% savings/debt repayment), relies entirely on knowing your net monthly income.

Debt Management and Loan Qualification

Lenders heavily rely on your income figures to assess your creditworthiness and ability to repay debt.

- Debt-to-Income (DTI) Ratio: This crucial metric is calculated by dividing your total monthly debt payments by your gross monthly income. Lenders use it to determine how much new debt you can take on. A lower DTI ratio generally qualifies you for better loan terms.

- Loan Approvals: Whether applying for a mortgage, car loan, or personal loan, your documented income is paramount. Understanding your true monthly income ensures you apply for loans you can realistically afford and have a higher chance of approval.

- Debt Repayment Strategy: If you’re struggling with debt, knowing your surplus income (income minus essential expenses) can help you create an aggressive repayment plan, such as the snowball or avalanche method.

Setting Financial Goals and Savings Targets

Clear financial goals require clear metrics. Your monthly income provides those metrics.

- Emergency Fund: Experts recommend having 3-6 months of living expenses saved. To calculate this, you need to know your average monthly expenses, which is directly linked to your income.

- Major Purchases: Saving for a down payment on a house, a new car, or a significant vacation becomes tangible when you know how much you can consistently put aside each month.

- Retirement Planning: Contributions to retirement accounts like 401(k)s or IRAs are often a percentage of your income. Knowing your income helps you set appropriate contribution levels to reach your long-term retirement goals.

Identifying Opportunities for Growth or Reduction

A clear picture of your income can highlight areas for improvement.

- Income Growth: If your income is stagnant or declining, it might prompt you to seek promotions, negotiate a raise, explore new skills, or develop additional income streams.

- Expense Reduction: If your expenses are consistently exceeding your income or leaving little room for savings, you’ll know where you need to cut back.

- Resource Allocation: You can identify if certain income streams are disproportionately costly (e.g., a side hustle with high expenses) or if others are under-leveraged.

Beyond the Basics: Optimizing Your Income Analysis

Once you’ve mastered finding and understanding your monthly income, you can leverage this knowledge for more advanced financial strategies.

Forecasting Future Income

With historical data and an understanding of your income sources, you can begin to forecast your future income.

- Projected Bonuses or Raises: If you anticipate a raise or a bonus, factor it into your future income projections (conservatively).

- New Income Streams: If you plan to start a side hustle or make an investment, estimate its potential contribution.

- Life Changes: Account for upcoming maternity leave, career breaks, or shifts in employment. This proactive approach allows you to plan ahead for potential income fluctuations.

Analyzing Income Growth and Trends

Don’t just look at your income as a static number. Periodically review your income over several months or years.

- Year-over-Year Comparison: Are you earning more than you were last year? If not, why?

- Income Diversification: Assess the stability of your income sources. Are you overly reliant on one unpredictable source? This might prompt you to seek diversification.

- Inflation Adjustment: Consider your income in real terms, adjusted for inflation. Is your purchasing power increasing or decreasing?

The Impact of Taxes and Deductions

While net income is what you take home, understanding gross income and the deductions that bridge the gap is crucial for tax planning and financial optimization.

- Tax Withholdings: Are you withholding the correct amount of federal and state taxes? Over-withholding means you’re giving the government an interest-free loan, while under-withholding can lead to penalties. Use the IRS Tax Withholding Estimator.

- Pre-Tax Contributions: Contributions to 401(k)s, traditional IRAs, or HSAs are often pre-tax, reducing your taxable income. Maximizing these not only saves for retirement but also reduces your current tax burden.

- Itemized Deductions: For freelancers or business owners, understanding deductible business expenses can significantly impact your taxable income and, therefore, your effective net income.

Seeking Professional Guidance

For complex financial situations, self-employment, or significant wealth, consulting a financial advisor or tax professional can be invaluable. They can help you:

- Optimize Tax Strategies: Identify deductions and credits you might be missing.

- Develop Investment Plans: Align your income with your investment goals.

- Create Comprehensive Financial Plans: Integrate your income with long-term goals like retirement, estate planning, and wealth accumulation.

In conclusion, knowing how to find your monthly income is more than just counting cash. It’s about empowering yourself with clarity, control, and confidence over your financial life. By systematically tracking all your income streams, understanding the difference between gross and net, and leveraging modern tools, you lay the groundwork for effective budgeting, goal setting, and ultimately, achieving true financial independence. Start today, and transform your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.