In the modern financial landscape, your bank account number is more than just a string of digits; it is the fundamental key to your personal economy. Whether you are setting up a direct deposit for a new job, authorizing an automated bill payment, or executing a wire transfer for a major investment, knowing exactly where to find and how to verify your account number is essential. Despite its importance, many consumers often confuse it with their debit card number or their bank’s routing number.

Understanding the architecture of your financial identity is a cornerstone of fiscal literacy. This guide provides a deep dive into the various methods—both traditional and digital—to locate your bank account number, while also exploring the critical security measures necessary to protect this sensitive information.

Locating Your Account Number Through Physical Documentation

Before the advent of smartphone applications and 24/7 web portals, finding a bank account number was a matter of looking through physical records. These traditional methods remain some of the most reliable ways to verify your details without needing an internet connection.

The Anatomy of a Personal Check

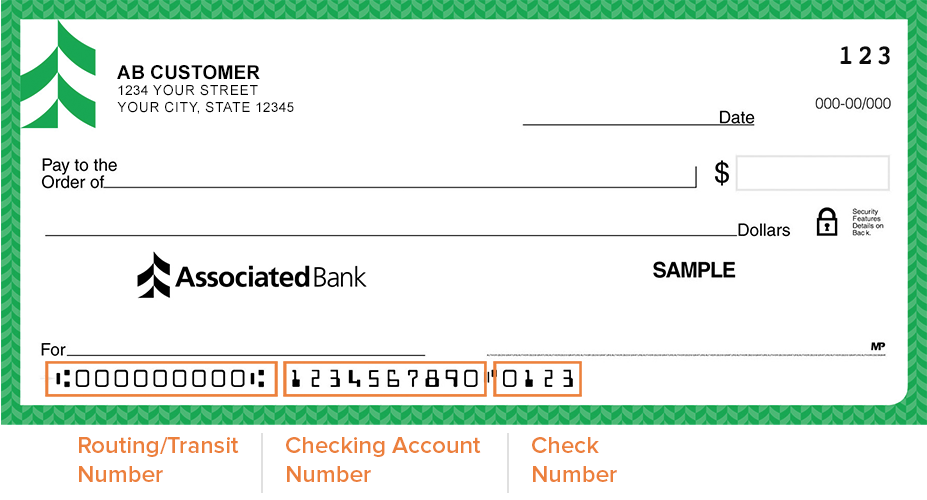

If you still use a physical checkbook, you are carrying your account information with you. At the bottom of every personal check, there is a series of numbers printed in a special font known as MICR (Magnetic Ink Character Recognition). This line typically contains three distinct sets of numbers:

- The Routing Number: Usually the first nine-digit sequence on the left, identifying the specific financial institution.

- The Account Number: Generally the middle sequence of numbers. It can vary in length depending on the bank but is unique to your specific account.

- The Check Number: The final, shorter sequence on the right, which matches the number in the top-right corner of the check.

Monthly Paper Statements

For those who still receive physical mail from their bank, the monthly statement is a goldmine of information. Your account number is typically located at the top of the first page, often labeled as “Account Summary” or “Statement Period.” For security purposes, some banks may partially mask the number (e.g., showing only the last four digits), but most full paper statements intended for your records will display the complete sequence.

The Initial Account Opening Package

When you first open a bank account, the institution provides a “Welcome Kit” or a set of “Account Opening Disclosures.” These documents contain your formal account agreement, fee schedules, and, most importantly, your full account number. If you have a dedicated filing system for your personal finance documents, this original paperwork is a definitive source of truth.

Utilizing Digital Banking Platforms for Instant Access

In today’s fast-paced digital economy, most people require their financial information on the go. Mobile and online banking have revolutionized the way we interact with our money, making it easier than ever to retrieve account details with a few taps or clicks.

Navigating Mobile Banking Apps

The majority of major financial institutions offer robust mobile applications. To find your account number here, you typically need to log in using biometric verification (like FaceID or a fingerprint). Once on the dashboard:

- Select the specific account (Checking, Savings, etc.).

- Look for a tab or icon labeled “Account Details,” “Info,” or “Manage.”

- In many apps, the account number is hidden behind an “eye” icon or asterisks for privacy. Tapping this icon will reveal the full string of digits.

Online Banking Portals via Web Browsers

If you are working from a desktop or laptop, logging into your bank’s official website provides a comprehensive view of your finances. Once authenticated, navigate to the “Accounts” overview. Similar to the mobile app, you will usually find a section dedicated to “Account Features” or “Account Services.” This section will list your full account number alongside your current balance and interest rate.

Accessing e-Statements and PDF Downloads

Even if you have opted out of paper mail, your bank generates a digital version of your statement every month. These “e-Statements” are legally binding documents and contain your full account number. Accessing the “Statements” or “Documents” tab in your online portal allows you to download a PDF version of your statement, which is often required when applying for a mortgage or verifying your income for a lease.

Direct Communication with Your Financial Institution

There are instances where technology might fail or physical documents might be lost. In these cases, interacting directly with bank personnel is the most secure way to recover your information.

Visiting a Local Branch

For individuals who prefer face-to-face interaction, visiting a local branch is a foolproof method. However, because of strict banking regulations and privacy laws, you cannot simply walk in and ask for a number. You must provide a valid government-issued photo ID (such as a driver’s license or passport). Once your identity is verified, a personal banker can provide you with your account details and even print out a “Direct Deposit Authorization” form, which includes both your account and routing numbers.

Contacting Customer Support via Phone

You can also find your account number by calling the customer service line located on the back of your debit card. Be prepared to go through a rigorous identity verification process. The representative may ask for your Social Security number, your mother’s maiden name, or details about your most recent transactions. Note that for security reasons, some banks have policies against reading the full account number over the phone; instead, they may offer to mail a physical letter to your address on file.

Understanding the Difference: Account Number vs. Routing Number

One of the most common pitfalls in personal finance is the confusion between the account number and the routing number. Using the wrong one can lead to failed payments, late fees, or funds being sent to the wrong destination.

What is a Routing Number?

A routing transit number (RTN) is a nine-digit code used by financial institutions to identify themselves within the United States. It acts like an address for the bank itself. Larger banks may have different routing numbers for different states or for different types of transactions (such as wire transfers vs. ACH transfers).

What is an Account Number?

While the routing number identifies the bank, the account number identifies you within that bank. It is your unique “internal” address. No two people at the same institution will have the same account number for the same type of account.

Why the Distinction Matters for Transactions

When setting up an “Automated Clearing House” (ACH) transfer—the standard for direct deposits and utility payments—you must provide both. The routing number tells the system which “building” to go to, and the account number tells it which “room” the money belongs in. If you provide your debit card number instead of your account number, the transaction will almost certainly be rejected, as debit card numbers are linked to a payment processor (like Visa or Mastercard) rather than the direct bank ledger.

Best Practices for Financial Security and Privacy

Your bank account number is a sensitive piece of data. If it falls into the wrong hands, it can be used for fraudulent ACH withdrawals. Therefore, finding your account number is only half the battle; the other half is keeping it secure.

Safeguarding Your Information

Treat your account number with the same level of caution as your Social Security number. Never share it over unencrypted email or text messages. If you must send financial details, use secure document-sharing portals provided by your bank or accountant. Additionally, if you use physical checks, ensure they are stored in a locked drawer or a safe, as they display your full financial “coordinates” to anyone who sees them.

Verifying Recipients for Transfers

When you are on the giving end of a transaction—sending money to a business or an individual—always verify the account number through a secondary medium. “Authorized Push Payment” fraud is on the rise, where scammers intercept emails and swap out legitimate bank details for their own. A quick phone call to the recipient to verify the last four digits of the account number can save you from significant financial loss.

Monitoring for Unauthorized Access

Regularly reviewing your bank statements is the best way to ensure your account number hasn’t been compromised. Look for small, unauthorized “micro-deposits” or withdrawals, which are often used by hackers to verify if an account is active before attempting a larger theft. Most modern banking apps allow you to set up “Real-Time Alerts,” notifying you via push notification every time a transaction occurs.

By mastering the various ways to locate and protect your bank account number, you take a proactive step in managing your personal finances. Whether through the tactile reliability of a checkbook or the high-tech convenience of a mobile app, staying informed ensures that your financial operations remain seamless, secure, and under your total control.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.