In the intricate world of personal finance, investing, and business operations, the ability to accurately calculate and interpret percentages is not just a useful skill—it’s a fundamental necessity. While calculating a simple percentage might seem straightforward, many real-world financial scenarios involve a “percentage of a percentage.” This concept underpins everything from understanding multi-tiered discounts and compounded investment returns to calculating effective tax rates and complex commission structures. Mastering this seemingly advanced calculation is crucial for making informed financial decisions, optimizing your investments, and ensuring the profitability of your ventures. This article will demystify the process, providing a clear, practical guide to navigating these essential financial calculations within the “Money” domain.

The Foundation: Understanding Percentages in Finance

Before diving into the complexities of calculating a percentage of a percentage, it’s vital to solidify our understanding of what a percentage represents and its ubiquitous role in finance. A solid grasp of the basics forms the bedrock for tackling more advanced applications.

What is a Percentage and Why It Matters for Your Money

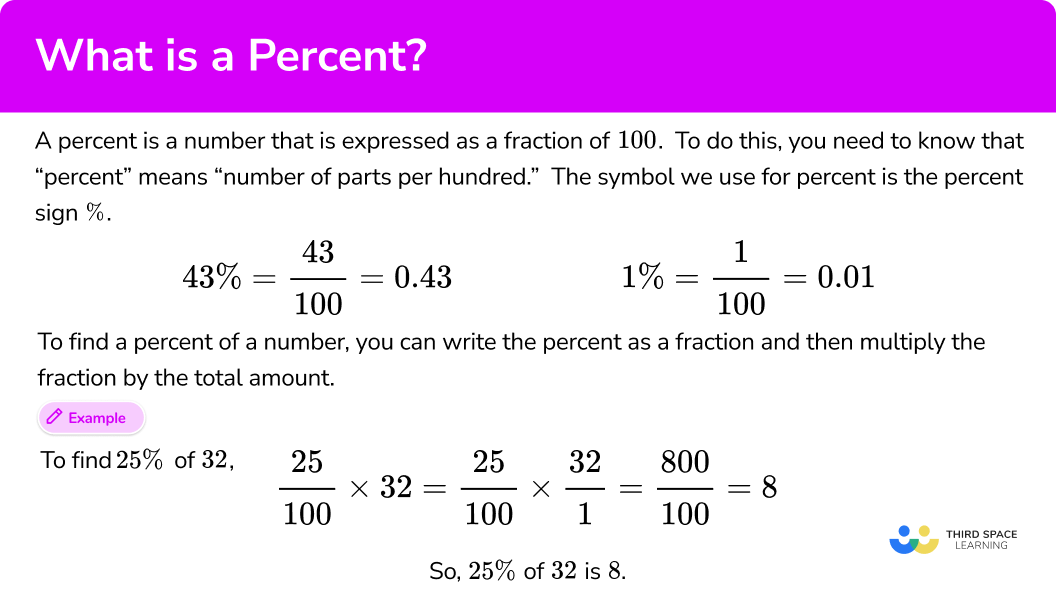

At its core, a percentage simply means “per hundred” or “out of one hundred.” It’s a way to express a proportion or a fraction of a whole, where the whole is considered to be 100. For instance, 25% represents 25 parts out of 100, or one-quarter of the total.

In the realm of money, percentages are the universal language for expressing rates, changes, proportions, and performance. Consider these common financial applications:

- Interest Rates: Whether it’s the interest you earn on savings, the rate on a loan, or the return on a bond, it’s always expressed as a percentage.

- Discounts and Sales Tax: Retailers advertise discounts as percentages off the original price, and governments levy sales tax as a percentage of the purchase amount.

- Investment Returns: The growth or decline of your investment portfolio, mutual funds, or individual stocks is typically communicated as a percentage gain or loss.

- Inflation: The rate at which the general level of prices for goods and services is rising, and subsequently, purchasing power is falling, is measured in percentages.

- Profit Margins: Businesses use percentages to understand how much profit they make relative to their revenue or costs.

- Budget Allocation: You might allocate a certain percentage of your income to housing, savings, or entertainment.

Without percentages, comparing financial performance across different scales or over different periods would be incredibly cumbersome and often misleading. They provide a standardized, relatable metric for financial analysis.

Converting Percentages to Decimals: The First Step

The golden rule for performing any mathematical operation with percentages is to first convert them into their decimal equivalents. This is a straightforward process: simply divide the percentage by 100.

For example:

- 10% becomes 10 / 100 = 0.10

- 25% becomes 25 / 100 = 0.25

- 5% becomes 5 / 100 = 0.05

- 125% becomes 125 / 100 = 1.25 (useful for calculating increases beyond the original value)

This conversion is crucial because mathematical operations (multiplication, division) are performed with decimals, not directly with the percentage symbol. Attempting to multiply 100 by “10%” without conversion will lead to incorrect results.

Basic Percentage Calculations: Discounts, Increases, and Simple Interest

Once percentages are converted to decimals, basic calculations become intuitive:

- Finding a percentage of a number: Multiply the number by the decimal equivalent of the percentage.

- Example: What is 15% of $200?

- 15% = 0.15

- 0.15 * $200 = $30

- Example: What is 15% of $200?

- Calculating a discount: Subtract the percentage of the number from the original number.

- Example: A $50 item is 20% off.

- 20% of $50 = 0.20 * $50 = $10

- Discounted price = $50 – $10 = $40

- Alternatively (and more efficiently for compound calculations): If 20% is off, you are paying 80% of the original price. 0.80 * $50 = $40.

- Example: A $50 item is 20% off.

- Calculating an increase: Add the percentage of the number to the original number.

- Example: A $1,000 investment grows by 10%.

- 10% of $1,000 = 0.10 * $1,000 = $100

- New value = $1,000 + $100 = $1,100

- Alternatively: If it grows by 10%, it’s 110% of the original. 1.10 * $1,000 = $1,100.

- Example: A $1,000 investment grows by 10%.

These fundamental skills are the building blocks for the more complex “percentage of a percentage” calculations we will now explore.

Unpacking “Percentage of a Percentage”: Real-World Financial Scenarios

The concept of “percentage of a percentage” arises when a calculation based on a percentage then serves as the basis for another percentage calculation. This is exceedingly common in various financial contexts, making its understanding indispensable for sound financial literacy.

Multi-Stage Discounts and Promotions

One of the most common applications is in retail, where multiple discounts are applied sequentially. This is often misunderstood, leading consumers to overestimate their savings.

- Scenario: A store offers 20% off all items, and on top of that, you have a coupon for an “additional 10% off the discounted price.”

- Many people mistakenly think this is a total of 30% off. However, the second 10% is off the already reduced price, not the original price.

- Financial Impact: For consumers, correctly calculating this ensures you know the true final price. For businesses, accurately modeling these discounts is critical for pricing strategies and managing profit margins.

Compounding Returns and Investment Growth

Perhaps the most significant financial application of a percentage of a percentage is in compounding interest and investment returns. This is where your money earns returns, and those returns then start earning returns themselves.

- Scenario: You invest $1,000, and it earns a 7% return in the first year. In the second year, it earns another 7% return.

- The second year’s 7% return is calculated on the new total amount ($1,000 + first year’s earnings), not just the original $1,000.

- Financial Impact: This “return on return” is the engine of wealth creation over time. Understanding how percentages compound is key to long-term financial planning, retirement savings, and evaluating investment products.

Tiered Commissions and Multi-Layered Taxation

In business finance and personal income, percentages of percentages can determine how much you earn or how much you owe.

- Scenario (Commissions): A salesperson earns 10% commission on sales up to $50,000, and then 5% commission on sales above $50,000. Alternatively, a company might pay a reseller 15% of the net profit (which is itself a percentage of revenue after costs).

- Scenario (Taxation): Income tax systems often use tiered brackets, where different percentages apply to different portions of your income. While not always a direct percentage of a percentage in calculation, understanding how marginal rates apply to portions of income (rather than the whole) requires similar sequential thinking. More directly, consider VAT/GST on an item that has already had excise duty applied.

- Financial Impact: For individuals, it’s crucial for understanding take-home pay. For businesses, it’s vital for calculating sales incentives, partner payouts, and accurate tax liabilities.

Expense Ratios and Management Fees on Investments

Understanding the true cost of managing your investments often involves multiple layers of percentage-based fees.

- Scenario: A mutual fund has an expense ratio of 0.50% of your assets. If you’re invested through an advisor who also charges 1% of your assets under management.

- Financial Impact: While these might seem like small percentages, they can significantly erode long-term returns, especially when compounded over decades. Identifying the cumulative effect of these percentage-based fees on your percentage returns is paramount for net growth.

Step-by-Step Guide: Calculating a Percentage of a Percentage

Calculating a percentage of a percentage can be approached in a couple of ways, both yielding the same correct result. The chosen method often depends on personal preference and the specific context of the problem.

Method 1: Sequential Calculation (Applying one percentage after another)

This method involves performing the calculations one step at a time, applying each percentage change to the intermediate result rather than the original amount.

- Step 1: Convert all percentages to their decimal equivalents.

- If a discount, subtract the decimal from 1 (e.g., 20% off = 1 – 0.20 = 0.80).

- If an increase, add the decimal to 1 (e.g., 10% increase = 1 + 0.10 = 1.10).

- Step 2: Apply the first percentage change to the original amount.

- Step 3: Apply the second percentage change to the result from Step 2.

- Step 4: Continue this process for any subsequent percentage changes.

Method 2: The Multiplier Approach (Converting all percentages to decimals first)

This method is often more efficient, especially when dealing with multiple sequential percentage changes, as it involves multiplying all the decimal multipliers together first.

- Step 1: Convert all percentages to their decimal multipliers.

- As in Method 1, for a 20% discount, the multiplier is 0.80. For a 10% increase, the multiplier is 1.10.

- Step 2: Multiply all the decimal multipliers together. This gives you a single, cumulative multiplier.

- Step 3: Multiply this cumulative multiplier by the original amount.

Practical Examples: From Budgeting to Portfolio Analysis

Let’s apply these methods to concrete financial scenarios:

Example 1: Multi-Stage Discount (Method 1 & 2)

- An item costs $100. It’s 20% off, and then an additional 10% off the reduced price.

- Method 1 (Sequential):

- Original price: $100

- First discount (20% off): $100 * (1 – 0.20) = $100 * 0.80 = $80

- Second discount (10% off the $80): $80 * (1 – 0.10) = $80 * 0.90 = $72

- Final price: $72

- Method 2 (Multiplier):

- First discount multiplier: 0.80

- Second discount multiplier: 0.90

- Cumulative multiplier: 0.80 * 0.90 = 0.72

- Final price: $100 * 0.72 = $72

- Insight: Notice that 20% + 10% = 30% would yield $70, which is incorrect. The actual total discount is $100 – $72 = $28, or 28%.

- Method 1 (Sequential):

Example 2: Compounding Investment Returns (Method 2 is ideal here)

- You invest $5,000. It earns 8% in Year 1, 10% in Year 2, and 5% in Year 3.

- Method 2 (Multiplier):

- Year 1 multiplier: 1.08

- Year 2 multiplier: 1.10

- Year 3 multiplier: 1.05

- Cumulative multiplier: 1.08 * 1.10 * 1.05 = 1.2474

- Final value: $5,000 * 1.2474 = $6,237

- Insight: This demonstrates the power of compounding. The effective average annual return is not simply (8+10+5)/3, and the total growth isn’t 8%+10%+5% of the original. Each year’s percentage gain is on a larger base.

- Method 2 (Multiplier):

Avoiding Common Pitfalls and Misinterpretations

While the mechanics of calculating a percentage of a percentage are straightforward, misinterpretations can lead to significant financial errors.

The “Additional Discount” Fallacy

As shown in our discount example, a “20% off then an additional 10% off” is not equivalent to “30% off.” This common misconception leads consumers to believe they are saving more than they actually are. Always remember that successive percentage discounts apply to the remaining balance, not the original total. This principle applies equally to successive increases.

Understanding Basis Points and Percentage Point Changes

In finance, particularly when discussing interest rates or investment fees, you’ll encounter “basis points” (bps) and “percentage point changes.”

- Percentage Point Change: If an interest rate goes from 4% to 5%, that’s a 1 percentage point increase.

- Percentage Change: However, the rate itself increased by (5-4)/4 = 0.25 = 25%. This is a percentage change in the rate, not a percentage point change.

- Basis Points: One basis point is 0.01% (one hundredth of a percentage point). So, 100 bps equals 1 percentage point. If an expense ratio increases by 25 bps, it means it increased by 0.25 percentage points (e.g., from 0.50% to 0.75%).

Understanding this distinction is critical for accurately interpreting financial news, comparing financial products, and tracking investment performance.

The Impact of Compounding Over Time: A Double-Edged Sword

Compounding is often hailed as the “eighth wonder of the world” when it comes to investment growth, but it’s a double-edged sword.

- Positive Compounding: For investments, the longer your money compounds, and the higher the percentage returns, the exponentially greater your wealth becomes. Small consistent percentage gains, when compounded, lead to significant sums.

- Negative Compounding (or Fees): The same principle applies to fees, interest on debt, and inflation. Small percentage-based fees, when compounded over decades, can significantly erode your investment returns. High-interest credit card debt, if not paid off, compounds rapidly, turning manageable balances into overwhelming ones. Recognizing these compounding effects is vital for managing debt and maximizing investment growth.

Leveraging Tools for Financial Percentage Calculations

While understanding the manual calculation is essential, for complex financial modeling and large datasets, leveraging technology becomes indispensable.

Spreadsheets (Excel, Google Sheets) for Complex Models

Spreadsheet software like Microsoft Excel or Google Sheets are the go-to tools for financial professionals and savvy individuals alike.

- Formulas: They allow you to input formulas that automate percentage calculations. You can set up columns for original amounts, discount percentages, and final prices, and have the sheet automatically calculate everything.

- Scenario Analysis: You can easily change percentage rates (e.g., different interest rates or inflation scenarios) and instantly see the impact on your budget, investment projections, or business forecasts.

- Data Organization: For tracking multiple investments, managing complex budgets, or analyzing sales data with tiered commissions, spreadsheets offer unparalleled organization and analytical power.

Financial Calculators and Online Tools

For quick, on-the-spot calculations, dedicated financial calculators (physical or online) are incredibly useful. Many online investment platforms and banking sites also offer built-in calculators for specific scenarios like loan payments, compound interest, or retirement savings projections. These tools simplify the process, often requiring only the input of a few key percentages and values.

Programming and Automation for Business Finance

In larger business contexts, especially in financial analysis, accounting, or data science departments, programming languages like Python or R are used to automate complex percentage-based calculations. This is particularly relevant for:

- Algorithmic Trading: Calculating percentage gains/losses on thousands of trades.

- Large-scale Data Analysis: Processing vast datasets to determine profit margins across numerous products or customer segments.

- Automated Reporting: Generating financial reports that include various percentage metrics and their cumulative effects.

Understanding how to find a percentage of a percentage is more than just a math problem; it’s a crucial component of financial literacy. From navigating consumer sales to strategically investing for retirement or managing a business’s bottom line, these calculations are ever-present. By mastering the methods and recognizing their real-world implications, you empower yourself to make smarter, more informed financial decisions, ultimately paving the way for greater financial success and stability.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.