In the intricate world of finance, simple percentages are often just the tip of the iceberg. Whether you’re managing personal investments, deciphering multi-tiered business discounts, or calculating real returns amidst inflation, the ability to find “a percent of a percent” is not merely an academic exercise—it’s a critical skill for making informed financial decisions. This seemingly complex mathematical operation is, in essence, the sequential application of percentages, and mastering it reveals a profound depth to financial analysis, moving beyond surface-level numbers to expose the true impact of compounding, deductions, and growth.

Understanding how to accurately calculate a percent of a percent empowers individuals and businesses to navigate a financial landscape where sequential changes are the norm. It’s the difference between merely seeing a 10% discount and truly grasping the effective price after a further 5% off, or between observing a nominal investment return and understanding its real value after accounting for fees and inflation. This article will demystify the process, grounding it firmly in practical financial applications, and equip you with the insights needed to make smarter, more strategic financial choices.

The Foundational Concept: Understanding Percentages in Finance

Before diving into the complexities of sequential percentage calculations, it’s crucial to solidify our understanding of the basic building blocks. In finance, a percentage is more than just a number followed by a percent sign; it’s a dynamic tool for representing proportions, rates, and changes, forming the bedrock of almost every financial calculation.

What is a Percentage? A Financial Perspective

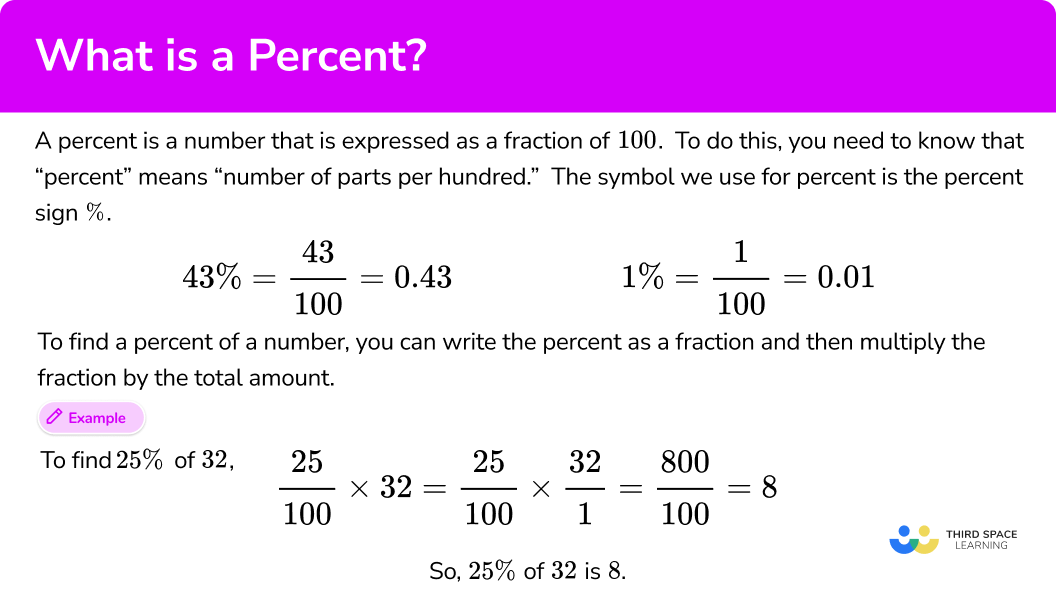

At its core, a percentage represents a fraction of 100. For instance, 5% literally means 5 out of 100, or 5/100. In finance, this simple concept translates into powerful metrics: interest rates, tax rates, growth rates, profit margins, discounts, and commissions are all expressed as percentages. Its ubiquity stems from its ability to standardize comparisons, allowing us to gauge performance, cost, or benefit relative to a whole, regardless of the absolute values involved. Understanding that a percentage is always relative to a base value—which can shift—is the first step towards mastering more complex financial arithmetic.

Converting Percentages to Decimals for Calculation

The most common pitfall in percentage calculations is attempting to perform operations directly with the percent sign. For any calculation, the percentage must first be converted into its decimal equivalent. This is achieved by dividing the percentage by 100. For example:

- 5% becomes 0.05

- 10% becomes 0.10

- 12.5% becomes 0.125

- 100% becomes 1.00

This conversion is non-negotiable for accurate financial modeling. Multiplying a financial figure by its decimal equivalent allows you to calculate the portion represented by that percentage. For instance, to find 5% of $1,000, you multiply $1,000 by 0.05, yielding $50. This foundational step ensures precision, especially when dealing with multiple layers of percentage adjustments.

The Importance of Base Value in Financial Calculations

When working with percentages, especially “a percent of a percent,” recognizing the changing base value is paramount. Often, a subsequent percentage is applied not to the original starting amount, but to the new value after the first percentage has been applied. This sequential adjustment is precisely what gives rise to the need to calculate a percent of a percent. For example, if you get a 10% discount on an item, and then an additional 5% off “the discounted price,” the second 5% is applied to a smaller base value. Failing to account for this shifting base is a common error that can lead to significant miscalculations in financial planning and analysis.

Navigating Sequential Percentage Changes: The Core of “Percent of a Percent”

The essence of calculating a percent of a percent lies in understanding that financial scenarios rarely involve a single, isolated percentage adjustment. From investment returns that compound over time to multi-layered tax structures, sequential percentage changes are a financial reality that demands a specialized approach.

Applying Successive Discounts or Markups

One of the most relatable applications of finding a percent of a percent is in retail, dealing with successive discounts or markups. Imagine a product originally priced at $200. First, it receives a 20% discount.

- First Discount: $200 * 0.20 = $40. New price = $200 – $40 = $160.

- Now, assume an additional promotional discount of 10% off the already discounted price. This is where “a percent of a percent” comes in. The 10% is applied to the new base of $160, not the original $200.

- Second Discount: $160 * 0.10 = $16. Final price = $160 – $16 = $144.

A common mistake is to add the percentages (20% + 10% = 30%) and apply it to the original price ($200 * 0.30 = $60, leading to a final price of $140). This is incorrect because the second discount is on a smaller base. The true effective discount is not simply the sum of individual percentages; it’s a result of their sequential application. The correct calculation, $144, demonstrates the power of understanding the changing base. The same logic applies to successive markups or profit margins.

Calculating Compound Interest and Investment Growth

Perhaps the most impactful application of “percent of a percent” in personal finance is compound interest. This is often called the “eighth wonder of the world” for good reason. When an investment earns interest, and that interest is then reinvested to earn more interest, you are effectively earning a “percent of a percent.”

- If you invest $1,000 at an annual interest rate of 5%.

- Year 1: Interest = $1,000 * 0.05 = $50. Total = $1,050.

- Year 2: The 5% interest is now calculated on the new base of $1,050. Interest = $1,050 * 0.05 = $52.50. Total = $1,102.50.

Notice that in Year 2, the interest earned ($52.50) is higher than in Year 1 ($50), even though the rate is the same. This is because the interest is calculated on the previous year’s total (principal + accumulated interest), demonstrating “a percent of a percent” in action. Understanding this mechanism is vital for projecting long-term investment growth, planning for retirement, and comprehending the true cost of loans.

Understanding Financial Fees and Commissions Structure

Many financial products and services involve multi-tiered fee or commission structures that require this sequential calculation. For example, a financial advisor might charge a 1% annual management fee on the asset value, and then an additional 0.5% transaction fee on any trades made after the management fee has been accounted for (though this specific example is simplified for illustration, real-world fee structures can be more complex but still rely on the same principle). Or, a sales professional earns a commission based on sales, and then a portion of that commission is subject to a performance bonus percentage.

Consider a fund with $100,000 that has a 1% management fee and a 0.2% administrative fee calculated on the remaining balance after the management fee.

- Management Fee: $100,000 * 0.01 = $1,000. Remaining balance = $99,000.

- Administrative Fee: $99,000 * 0.002 = $198.

Total fees are $1,000 + $198 = $1,198.

If you simply added the percentages (1% + 0.2% = 1.2%) and applied it to the original $100,000, you’d get $1,200. While the difference here is small ($2), across large sums and numerous transactions, such discrepancies can accumulate into significant miscalculations, impacting net returns or actual costs.

Inflation and Real Returns: Adjusting for Economic Shifts

Inflation represents the rate at which the general level of prices for goods and services is rising, and subsequently, the purchasing power of currency is falling. When evaluating investment returns, it’s crucial to understand not just the nominal return (the stated percentage gain) but also the “real return” after accounting for inflation.

- If your investment yielded a 7% nominal return, but inflation for the same period was 3%, your real return is not simply 7% – 3% = 4%.

- Instead, you need to consider the impact of inflation on the original purchasing power. If an initial $100 effectively became worth $107 due to the investment, but the cost of goods increased by 3%, the $107 can now buy less than $107 worth of goods from the previous year.

- The exact calculation for real return involves division: (1 + Nominal Return) / (1 + Inflation Rate) – 1. So, (1 + 0.07) / (1 + 0.03) – 1 = 1.07 / 1.03 – 1 ≈ 1.0388 – 1 ≈ 0.0388 or 3.88%. This effectively shows what percentage of your investment’s growth truly represents an increase in purchasing power. While slightly different in mechanics from a simple “percent of a percent” multiplication, it embodies the spirit of adjusting a value (or a return) based on another percentage factor.

Practical Applications in Personal and Business Finance

Mastering the calculation of a percent of a percent is not merely theoretical; it has profound practical implications across various aspects of personal and business finance, enabling more accurate forecasting, budgeting, and strategic planning.

Evaluating Investment Performance with Compounding Returns

For investors, understanding compound growth is paramount. It allows for a realistic projection of long-term wealth accumulation. Comparing two investment options, one offering a consistent 6% annual return and another offering 5% in year one and 7% in year two, requires sequential calculation. It’s never as simple as averaging or adding the percentages; each year’s return is applied to the growing principal, highlighting the true power of compounding over time. This insight drives critical decisions about diversification, rebalancing, and long-term financial goals.

Decoding Multi-Tiered Taxation and Deductions

Tax systems globally often involve progressive tax brackets, deductions, and credits that interact in complex ways. A taxable income might first be reduced by certain deductions, then the resulting net income is subject to various tax rates based on tiers, and finally, tax credits might further reduce the final tax liability. Each step involves applying a percentage (or a fixed amount) to a newly calculated base. For instance, understanding how a tax deduction of X% of eligible expenses impacts your overall tax bill requires calculating the deduction, subtracting it from your gross income to get your new taxable income, and then applying the relevant tax bracket percentages. This multi-layered approach prevents taxpayers from overpaying or underpaying.

Analyzing Profit Margins and Discounts in Retail

Businesses constantly juggle costs, pricing, and promotional discounts. A product’s cost might be $50. A business wants a 40% gross profit margin on the selling price. This is not simply adding 40% to the cost ($50 * 1.40 = $70). A 40% profit margin means that the cost ($50) represents 60% of the selling price. So, $50 / 0.60 = $83.33 (selling price). If a 15% promotional discount is then offered, it’s applied to $83.33, not the original $50. Accurate calculation of these sequential percentages ensures profitability and competitive pricing strategies, preventing losses due to miscalculated markdowns.

Budgeting and Debt Management: Impact of Variable Rates

In personal finance, managing debt, especially credit cards or variable-rate loans, often involves “a percent of a percent.” Credit card interest is typically calculated on your average daily balance, and if you carry a balance, the interest for the next cycle is calculated on the principal plus the accrued interest from the previous cycle. This compounding effect, much like with investments, can significantly escalate debt if not managed effectively. Understanding how interest rates (percentages) are applied sequentially to your outstanding balance is crucial for budgeting, prioritizing debt repayment, and minimizing interest costs.

Strategies for Accurate Financial Calculations

With the complexities of sequential percentages, having a robust methodology and leveraging the right tools is essential for maintaining accuracy in financial calculations.

Step-by-Step Calculation Methodology

The most reliable approach to finding a percent of a percent is a methodical, step-by-step process:

- Convert Percentages to Decimals: Always start by transforming all relevant percentages into their decimal equivalents.

- Identify the Initial Base Value: Determine the starting amount to which the first percentage will be applied.

- Apply the First Percentage: Perform the calculation (multiplication for finding the percentage amount, then addition/subtraction to find the new base value).

- Identify the New Base Value: The result of the first application becomes the new base for the next percentage.

- Apply the Second Percentage: Perform the calculation using the new base.

- Continue Sequentially: Repeat steps 3-5 for any subsequent percentages.

This disciplined approach minimizes errors and clarifies the impact of each percentage adjustment.

Leveraging Financial Calculators and Software

While manual calculation is fundamental for understanding, for complex or repetitive tasks, leveraging technology is smart.

- Spreadsheets (e.g., Excel, Google Sheets): Invaluable for setting up dynamic models. You can easily link cells, allowing changes to one percentage or base value to instantly update all subsequent calculations. Formulas like

=(1+rate1)*(1+rate2)-1for combined growth rates, or=(Original_Value*(1-Discount1)*(1-Discount2))for successive discounts, streamline complex operations. - Dedicated Financial Calculators: Handheld financial calculators often have specific functions for compound interest, effective rates, and amortization, which inherently handle sequential percentage calculations.

- Online Financial Tools: Numerous websites offer calculators for compound interest, loan repayments, and investment growth, simplifying these calculations for personal finance needs.

Common Pitfalls and How to Avoid Them

Even seasoned professionals can make mistakes. Being aware of common pitfalls is key to avoiding them:

- Adding Percentages Instead of Multiplying/Applying Sequentially: As discussed with discounts, simply adding percentages (e.g., 20% + 10% = 30%) is incorrect for sequential changes. Always apply them one after another to the changing base.

- Forgetting to Convert to Decimals: Performing calculations directly with “5%” instead of “0.05” will lead to wildly inaccurate results.

- Applying to the Wrong Base: Accidentally applying a subsequent percentage to the original base instead of the new, adjusted base is a frequent error. Carefully track which value serves as the current base for each step.

- Misinterpreting “of” vs. “to” / “from”: Understand whether a percentage is being applied to increase a value, from to decrease it, or simply of a value to find a component.

Mastering “Percent of a Percent” for Financial Empowerment

The ability to accurately find a percent of a percent transcends basic arithmetic; it’s a powerful tool for financial empowerment, offering clarity and precision in an increasingly complex economic landscape.

Enhancing Decision-Making in Investments

For investors, this skill is non-negotiable. It allows for realistic projections of portfolio growth, helps in comparing the true returns of different investment vehicles (factoring in fees and compounding), and provides a clearer picture of future wealth accumulation. Understanding how even small, sequentially applied percentages accumulate can profoundly impact retirement planning, education savings, and major purchase decisions.

Optimizing Personal Spending and Savings

On a personal level, this knowledge helps consumers make savvier purchasing decisions, truly understanding the effective price after multiple discounts or the actual cost of financing a purchase with compounded interest. It also aids in setting realistic savings goals by accurately projecting how savings grow over time with compounding interest, or how debt can spiral without effective management.

Driving Business Profitability and Pricing Strategies

For businesses, mastering sequential percentage calculations is fundamental to financial health. It informs robust pricing strategies, ensuring that products are profitable even after accounting for manufacturing costs, overhead, markups, and potential promotional discounts. It helps in accurately forecasting revenue, managing expenses with multi-tiered structures, and analyzing the real impact of sales incentives and commissions on the bottom line. This precision leads to healthier margins and more sustainable growth.

In conclusion, “how to find a percent of a percent” is far more than a mathematical puzzle; it’s a cornerstone of financial literacy. From the everyday discounts you encounter to the long-term growth of your investments, the sequential application of percentages dictates the true financial outcome. By embracing a methodical approach, leveraging appropriate tools, and staying vigilant against common errors, you can transform this seemingly intricate concept into a clear pathway for deeper financial understanding and more empowered decision-making. The journey from simply seeing numbers to truly understanding their interwoven impact is where real financial acumen begins.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.