In an increasingly digitized financial landscape, the humble money order might seem like a relic of a bygone era. Yet, for specific transactions, or when dealing with parties who prefer traditional methods or lack access to banking facilities, a money order remains an indispensable financial tool. Issued by trusted institutions like Chase Bank, money orders offer a secure, traceable, and reliable way to send guaranteed funds. This comprehensive guide will walk you through the process of obtaining and meticulously filling out a money order from Chase Bank, ensuring your financial transactions are executed with precision and peace of mind.

Understanding Money Orders and Their Purpose

Before diving into the specifics of filling one out, it’s crucial to understand what a money order is, its practical applications, and why it holds a distinct place among various payment methods.

What is a Money Order?

A money order is a prepaid financial instrument that functions similarly to a check, but with guaranteed funds. Unlike a personal check, which can bounce if the account lacks sufficient funds, a money order’s value is paid upfront to the issuer (in this case, Chase Bank). This makes it a highly secure form of payment, as the recipient is assured that the funds are legitimate and available. It’s essentially a certificate that states a specific amount of money is available to be paid to a named payee.

Chase Bank, as a major financial institution, provides money orders as a service to its customers. When you purchase a money order from Chase, you’re essentially buying a piece of paper that represents a specific sum, backed by the bank’s credibility.

When to Use a Money Order

Money orders are particularly useful in several scenarios where other payment methods might be less suitable or impractical:

- Sending money through the mail securely: If you need to mail payment and want to avoid sending cash or a personal check that could be lost or stolen, a money order offers a traceable and safer alternative.

- Paying bills to companies that don’t accept personal checks or digital payments: Some smaller businesses, landlords, or utility companies may have specific payment requirements.

- Making payments to individuals without bank accounts: Recipients who are unbanked or prefer not to use electronic transfers can easily cash a money order at various locations, including post offices, banks, or even some retail stores.

- Limiting personal information: Unlike personal checks, a money order doesn’t typically reveal your bank account number, adding an extra layer of privacy and security.

- Proof of payment: Money orders come with a receipt or stub, which serves as proof of purchase and can be used to track the payment if necessary.

Advantages Over Other Payment Methods

While digital payment apps and online banking have revolutionized how we transfer funds, money orders retain distinct advantages:

- Guaranteed Funds: The primary benefit. Since it’s prepaid, there’s no risk of a money order bouncing due to insufficient funds, unlike a personal check. This offers assurance to the payee.

- Accessibility: Widely accepted and cashable. Even if the recipient doesn’t have a bank account, they can often cash it at a post office, the issuing bank, or other approved locations.

- Traceability: Every money order has a unique serial number. Keeping your stub allows you to track its status and potentially cancel it if it’s lost or stolen, a feature not always available with cash.

- Cost-Effective for Small Transfers: While there is a small fee, it’s often more economical for smaller amounts than a wire transfer or certified check, particularly for international remittances where exchange rates and higher fees can apply.

- Security against Fraud: It’s generally safer than sending cash through the mail, and because the funds are verified upfront, it reduces the risk of fraud compared to accepting a personal check from an unknown party.

Acquiring and Preparing Your Chase Money Order

The journey to successfully completing a money order begins with knowing where to get one and what information you’ll need at your fingertips. Preparation is key to a smooth and error-free transaction.

Where to Purchase a Money Order from Chase

Chase Bank, like most major financial institutions, offers money orders primarily through its branch network.

- Chase Bank Branches: This is the most common and reliable place to purchase a money order. You’ll need to visit a Chase branch during business hours. A teller will assist you with the purchase. You might need to be a Chase account holder, or at least have a valid ID, to complete the transaction.

- Other Locations (Not Chase Specific): While Chase money orders must be purchased at Chase, it’s worth noting that money orders are also widely available at post offices (USPS money orders), Western Union, and certain grocery or convenience stores. However, if your specific instruction is to use a Chase money order, a Chase branch is your only option.

When you go to a Chase branch, be prepared to provide cash or debit funds directly from your Chase checking or savings account for the amount of the money order plus any associated fees.

Essential Information to Gather Before Filling Out

To ensure a seamless process and avoid errors, have the following information ready before you even start writing on the money order itself:

- The exact amount of money: Double-check the precise amount you need to send. This should be confirmed before you even purchase the money order, as the teller will issue it for a specific value.

- The full name of the payee: This is the individual or organization who will receive the money. Accuracy is paramount. Use their legal name, just as it would appear on a check or official document.

- The payee’s address (optional but recommended): While not always strictly required on the money order itself, having the payee’s address is useful for your records and for mailing the money order.

- Your full name and address (purchaser/sender): You will need to provide this information on the money order for identification purposes.

- Any account numbers or reference numbers: If the payment is for a bill or an invoice, there might be an account number or reference code that needs to be included. This is crucial for the payee to properly credit your payment.

Understanding Fees and Limits

Chase Bank, like other issuers, charges a small fee for money orders. These fees are typically nominal, often a few dollars, and can vary. It’s always a good idea to confirm the current fee schedule with a Chase representative when you make your purchase.

There are also limits to the amount a single money order can be issued for. For instance, USPS money orders have a maximum limit of $1,000. While Chase’s limits might differ, it’s common for financial institutions to have similar ceilings per money order to mitigate risk. If you need to send a larger sum, you might need to purchase multiple money orders or consider alternative payment methods like a cashier’s check or wire transfer. Always inquire about these limits at the time of purchase.

A Step-by-Step Guide to Filling Out Your Chase Money Order

Once you have purchased your money order from Chase and have all the necessary information at hand, it’s time to carefully fill it out. Precision and legibility are key to preventing delays or issues for the recipient.

Always use a pen with blue or black ink. Avoid pencils, as they can be easily erased and tampered with.

Section 1: The Payee’s Name

This is arguably the most critical part. You will typically find a line labeled “Pay to the Order of,” “Payee,” or similar.

- Write the full, legal name of the person or organization who will receive the money. For example, “John D. Smith” or “ABC Corporation.”

- Be meticulous with spelling. Any discrepancies could cause issues for the recipient when attempting to cash or deposit the money order.

- Do not leave this blank. A blank payee line means anyone could potentially fill it in and cash it, making it as risky as cash if lost.

Section 2: Your Name and Address (Purchaser)

Look for a section labeled “Purchaser,” “Sender,” “Remitter,” or “From.”

- Fill in your full name and current address. This identifies you as the sender of the funds. This information is important for tracking purposes and for the recipient to know who sent the payment.

- While this section is often less critical for the immediate cashing of the money order, it’s vital for your records and for resolving any potential issues later.

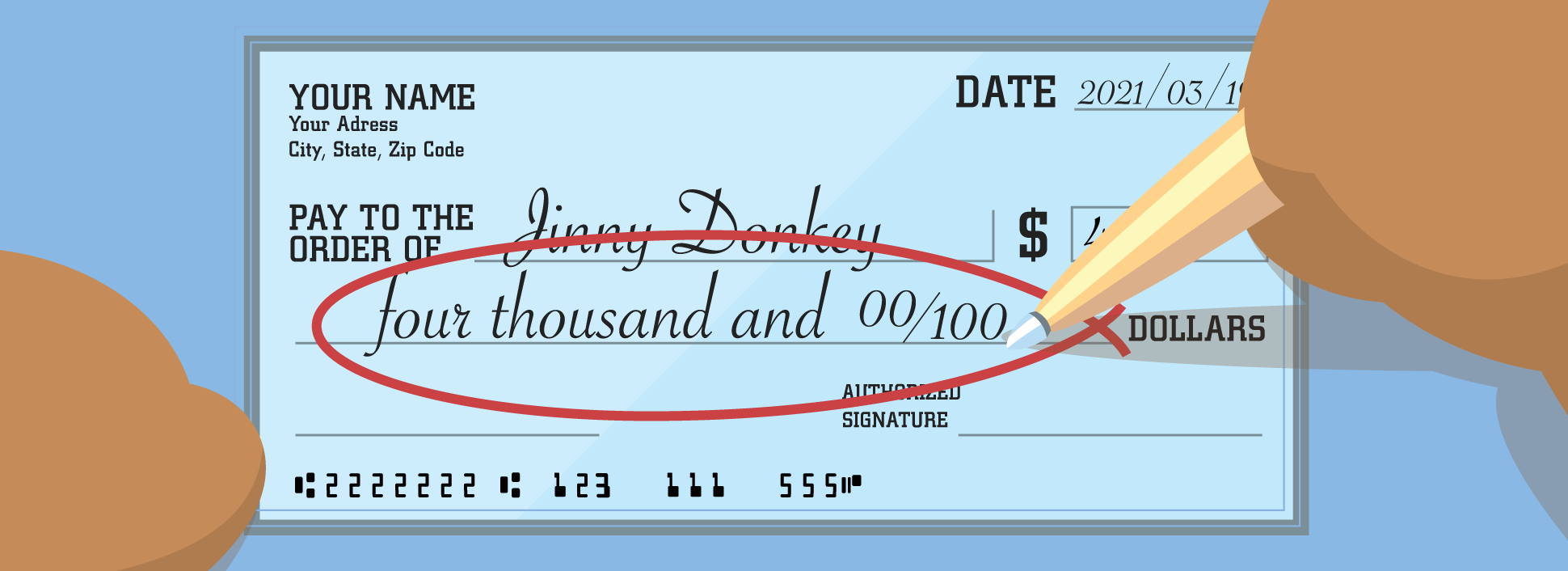

Section 3: The Amount (Numerically and Written)

The money order will have two places to write the amount: one numerical and one written out.

- Numerical Amount: There will be a box or a line often preceded by a dollar sign ($). Write the exact dollar amount clearly, using cents if applicable (e.g., “$150.75”). Ensure the decimal point is clear.

- Written Amount: Below or next to the numerical amount, there will be a line to write out the amount in words (e.g., “One Hundred Fifty and 75/100 Dollars”). This serves as a safeguard against alteration of the numerical amount.

- Start writing at the far left of the line to prevent anyone from adding words before your amount.

- Fill any remaining space with a line (e.g., “One Hundred Fifty and 75/100 Dollars —–“) to further prevent tampering.

- If there are no cents, you can write “and 00/100” or “and no/100.”

Section 4: Memo Line (Optional but Recommended)

Many money orders have a “Memo” or “For” line, similar to a personal check.

- Use this line to specify the purpose of the payment. This could be an account number, invoice number, rent payment for a specific month, or a brief description (e.g., “Invoice #12345,” “June Rent,” “Donation”).

- This is especially helpful for the payee to apply your payment correctly and for your own records.

Section 5: The Signature

There will be a line for the “Purchaser’s Signature” or “Sender’s Signature.”

- Sign your legal signature clearly. This validates you as the sender and confirms your authorization of the payment.

Crucial: Retain Your Money Order Stub

Every money order comes with a detachable stub or receipt.

- DO NOT lose this stub! It contains vital information: the money order number, the date of purchase, the amount, and potentially the payee’s name.

- This stub is your proof of purchase and is absolutely essential for tracking the money order, verifying its status, or initiating a refund or replacement if it gets lost or is never cashed. File it in a safe place until you confirm the transaction is complete.

Safeguarding Your Transaction: Best Practices and What to Do After

Filling out a money order is just one part of the process. Ensuring its safe delivery and knowing what to do in case of issues are equally important for a secure financial transaction.

Verifying Information Before Mailing

Before you seal that envelope, take a moment to review everything you’ve written on the money order:

- Recipient’s Name: Is it spelled correctly? Is it the full legal name?

- Amount: Do both the numerical and written amounts match? Are they correct?

- Your Information: Is your name and address accurate?

- Memo Line: Is any required reference information included?

- Signature: Have you signed it?

This quick double-check can prevent significant headaches and delays down the line.

Tracking and Cancelling a Lost or Unused Money Order

This is where your retained stub becomes invaluable.

- Tracking: If the payee confirms they haven’t received the money order, or if you simply want to verify it’s been cashed, you can use the money order number on your stub to initiate a trace. You would typically contact Chase Bank directly with this information. They can usually tell you if and when it was cashed, and by whom.

- Cancelling/Refund: If a money order is lost, stolen, or you simply no longer need it, you might be able to get a refund.

- Uncashed Money Order: If the money order has not been cashed, you can typically apply for a refund. This process usually involves filling out a form, providing your purchase stub, and potentially paying a stop payment fee. Be prepared for this process to take several weeks, as Chase will need to verify that the money order has not been cashed before issuing a refund.

- Lost or Stolen: Report it to Chase Bank immediately. They will guide you through the process of requesting a stop payment and a refund, but again, the stub is crucial evidence of your purchase.

Common Pitfalls to Avoid

- Never leave the payee line blank: This is critical security advice.

- Don’t sign the back (endorse) until you are the payee: Endorsing a money order makes it payable to someone else or to cash, which should only be done by the intended recipient.

- Keep your stub separate from the money order: If you mail them together and the envelope is lost or stolen, you lose your only proof of purchase and tracking number.

- Be wary of overpayment scams: If someone sends you a money order for more than the agreed-upon amount and asks you to send back the difference, it’s likely a scam. The money order might be fraudulent, and you’ll be out the money you sent.

Beyond Money Orders: Exploring Alternative Payment Solutions

While money orders are excellent for specific situations, it’s also wise to be aware of other financial tools that might serve your needs, particularly in an age dominated by digital transactions. Understanding your options allows you to choose the most efficient, secure, and cost-effective method for each unique payment scenario.

Digital Alternatives for Secure Payments

For many routine transactions, particularly person-to-person or online payments, digital platforms offer speed and convenience.

- Online Banking Transfers (Chase QuickPay with Zelle): If both you and the recipient bank with Chase or other participating banks, services like Zelle allow for instant, direct bank-to-bank transfers using just an email address or phone number. This is often free and highly secure.

- Payment Apps (Venmo, PayPal, Cash App): These popular apps facilitate quick transfers between individuals, often for free for standard transactions. They are convenient for splitting bills, paying friends, or making purchases from small businesses. However, they may involve fees for instant transfers or business transactions, and consumer protections can vary.

- Bill Pay Services: Most banks, including Chase, offer robust online bill pay services where you can set up recurring payments or one-time transfers to businesses. This eliminates the need for money orders for many common bills.

- Wire Transfers: For larger sums or international payments where speed and certainty are paramount, a wire transfer is a direct electronic transfer of funds from one bank to another. While more expensive than money orders, they are highly secure and guaranteed.

Certified Checks and Cashier’s Checks

For substantial payments where the recipient requires guaranteed funds but a money order’s limit is too low, certified checks and cashier’s checks issued by Chase Bank are excellent alternatives.

- Cashier’s Check: This is a check drawn on the bank’s own funds, not your personal account. When you purchase a cashier’s check from Chase, the bank debits your account for the amount plus a fee, then issues a check guaranteed by the bank itself. This makes it an extremely secure form of payment, widely accepted for large purchases like real estate down payments or car purchases.

- Certified Check: With a certified check, Chase verifies that you have sufficient funds in your account to cover the check, and then “certifies” the check, essentially guaranteeing the funds. The money is usually put on hold in your account. While still secure, a cashier’s check might be preferred for higher-value transactions as it is drawn directly on the bank’s funds.

Each of these financial tools has its place in a well-managed personal finance strategy. By understanding the nuances of money orders, especially how to meticulously fill one out from an institution like Chase Bank, alongside exploring its modern and traditional alternatives, you empower yourself to navigate your financial transactions with confidence, security, and efficiency.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.