Tax season is an annual milestone that often evokes a mixture of anxiety and confusion for millions of taxpayers. However, viewing tax filing not as a burdensome chore, but as a critical component of personal financial management, can fundamentally change your perspective. Filing a tax return is the process by which you report your income, expenses, and other pertinent financial information to the government, ensuring that you have paid the correct amount of tax and, ideally, claiming any refunds you are owed.

In the contemporary financial landscape, staying compliant while maximizing your financial position requires a strategic approach. Whether you are a traditional W-2 employee, a burgeoning freelancer, or a small business owner, understanding the mechanics of tax filing is essential for long-term wealth preservation. This guide provides a deep dive into the nuances of filing your tax return, focusing on preparation, methodology, and long-term planning.

Preparation: The Foundation of a Stress-Free Tax Filing

The difference between a seamless tax season and a frantic one usually lies in the quality of preparation. Tax filing is essentially a data-entry exercise; if the data is organized, the process becomes mechanical. If the data is missing, the process becomes an investigative headache.

Gathering Essential Documentation

Before you open any software or meet with a professional, you must assemble your financial paper trail. For most individuals, this begins with income statements. If you are an employee, your employer will provide a Form W-2. If you are a contractor or freelancer, you will likely receive various 1099 forms (such as the 1099-NEC for non-employee compensation or 1099-K for third-party payments).

Beyond income, you must collect documentation for potential deductions. This includes 1098 forms for mortgage interest, records of charitable contributions, and receipts for medical expenses if they exceed a certain percentage of your adjusted gross income (AGI). Organized digital folders or physical binders divided by category can save hours of time when the filing deadline approaches.

Understanding Your Filing Status

Your filing status is a pivotal factor that determines your standard deduction and the tax brackets applied to your income. The five main statuses are Single, Married Filing Jointly, Married Filing Separately, Head of Household, and Qualifying Surviving Spouse.

Choosing the correct status is vital because it directly impacts your tax liability. For example, the “Head of Household” status offers more favorable tax rates and a higher standard deduction than “Single,” but it requires specific criteria, such as paying more than half the cost of keeping up a home for a qualifying person. Misclassifying your status can lead to overpaying or, conversely, triggering an IRS inquiry.

Deductions vs. Credits: Maximizing Your Wealth

One of the most misunderstood aspects of the tax return is the difference between deductions and credits. A tax deduction reduces the amount of your income that is subject to tax. For instance, if you earn $70,000 and have a $10,000 deduction, you are only taxed on $60,000.

A tax credit, however, is a dollar-for-dollar reduction of your actual tax bill. If you owe $5,000 in taxes but have a $2,000 credit, your bill drops to $3,000. Credits are generally more valuable than deductions. Understanding available credits, such as the Earned Income Tax Credit (EITC) or the Child Tax Credit, can result in thousands of dollars staying in your pocket rather than going to the treasury.

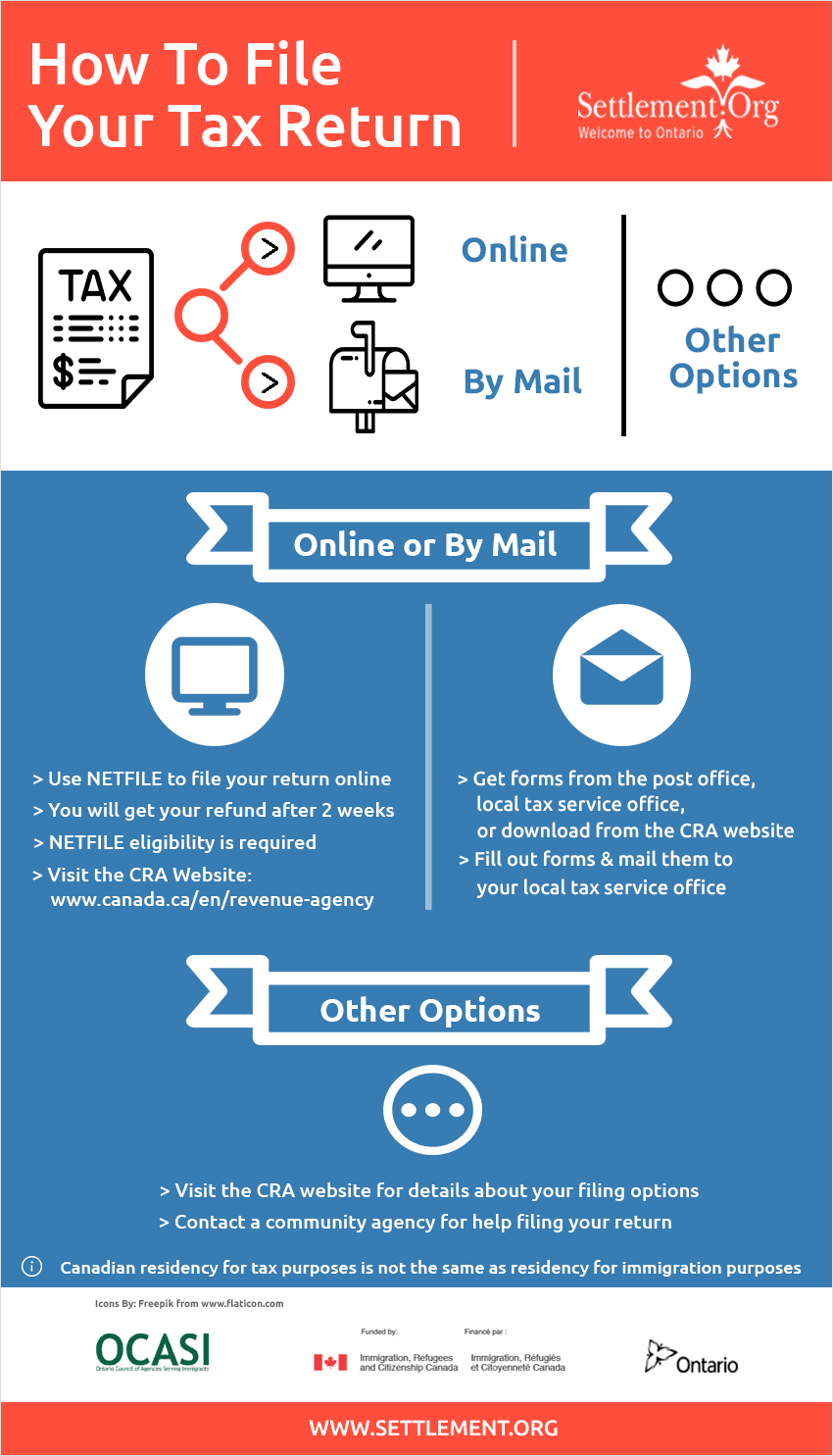

Navigating Filing Methods: Choosing the Right Path

Once your documents are in order, the next decision is how to actually submit the return. In the modern era, the “Money” niche has been revolutionized by financial tools that cater to every level of complexity.

The Rise of E-filing and IRS Free File

The Internal Revenue Service (IRS) strongly encourages electronic filing (e-filing). It is faster, more accurate, and results in quicker refunds compared to paper returns. For those whose income falls below a specific threshold (generally around $79,000), the IRS Free File program provides access to brand-name tax software at no cost. This is an underutilized financial tool that allows middle-to-low-income earners to navigate complex forms with guided help, ensuring they don’t miss out on standard credits.

The Professional Route: Working with CPAs and Enrolled Agents

While software is sufficient for many, high-net-worth individuals or those with complex investment portfolios often benefit from the expertise of a Certified Public Accountant (CPA) or an Enrolled Agent. Tax laws are dynamic and frequently subject to legislative changes. A professional does more than just fill out forms; they provide strategic tax advice.

From a financial management perspective, the fee paid to a CPA is often offset by the tax savings they identify through sophisticated strategies, such as loss harvesting in brokerage accounts or optimizing depreciation for rental properties.

Comparing Tax Software Solutions

For the “do-it-yourself” crowd, the market is saturated with financial software designed to simplify the tax code. These platforms use interview-style interfaces to extract the necessary information. When choosing a software tool, consider the complexity of your situation. Some platforms are better suited for simple W-2 filings, while others offer robust modules for cryptocurrency traders or rental property owners. The key is to find a tool that balances cost-effectiveness with the comprehensive coverage of your specific financial activities.

Specialized Scenarios: Small Business Owners and Freelancers

The shift toward the “gig economy” and entrepreneurship means that an increasing number of taxpayers cannot simply rely on a single W-2. If you are self-employed, your tax return is essentially a financial report of your business health.

Managing Self-Employment Tax Obligations

Unlike traditional employees, whose employers pay half of their Social Security and Medicare taxes, self-employed individuals are responsible for the full 15.3% self-employment tax. This can be a significant “sticker shock” for new entrepreneurs. Effective tax filing in this category requires filing Schedule SE to calculate these obligations. Understanding this cost is essential for pricing your services correctly and maintaining a healthy cash flow throughout the fiscal year.

Business Expenses and the Home Office Deduction

The “Money” aspect of self-employment revolves around maximizing legitimate business expenses to lower taxable income. The IRS allows you to deduct “ordinary and necessary” expenses. This includes everything from marketing costs and professional software to a portion of your home expenses if you maintain a dedicated home office.

The home office deduction is often avoided by taxpayers for fear of audits, but when applied correctly and supported by documentation (like the square footage of the office relative to the home), it is a powerful tool for reducing a small business owner’s tax burden.

The Necessity of Quarterly Estimated Taxes

One of the biggest mistakes in business finance is waiting until April to pay a year’s worth of taxes. The U.S. tax system is a “pay-as-you-go” system. If you expect to owe more than $1,000, you are generally required to make quarterly estimated payments. Filing your annual return becomes much easier when you have already paid into the system throughout the year, preventing heavy penalties and the stress of a massive lump-sum payment in the spring.

Post-Filing Best Practices and Long-Term Wealth Management

The process doesn’t end the moment you hit “submit.” A sophisticated approach to money management involves analyzing the return to prepare for the future.

Record Keeping and Audit Prevention

Once your return is filed, you must maintain your records. The general rule of thumb is to keep tax records for at least three years, though some financial experts recommend seven years to cover all potential statute of limitations. In the event of an audit, having a well-organized digital archive of your receipts, bank statements, and filed returns is your best defense. This level of organization is a hallmark of disciplined financial planning.

Analyzing the Refund: The “Interest-Free Loan” Concept

While receiving a large tax refund feels like a windfall, from a strictly financial perspective, it means you gave the government an interest-free loan for a year. If you receive a massive refund, it may be wise to adjust your W-4 withholdings. By having less tax withheld each paycheck, you increase your monthly cash flow, which can be redirected into high-yield savings accounts or retirement investments, allowing your money to grow for you rather than sitting in the government’s coffers.

Tax Planning as an Investment Strategy

Finally, use your filed return as a roadmap for the coming year. Tax filing is a retrospective look at your finances, but tax planning is prospective. Look at your effective tax rate and identify ways to lower it. This might include increasing contributions to a 401(k) or a traditional IRA, which reduces your taxable income, or utilizing a Health Savings Account (HSA) for its triple-tax advantage.

In conclusion, filing a tax return is more than a legal obligation; it is a critical exercise in financial literacy. By meticulously preparing your documentation, choosing the right filing method, understanding the nuances of self-employment, and using the results to inform future planning, you can transform tax season from a period of stress into a strategic advantage for your personal wealth. Control your taxes, and you take a significant step toward controlling your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.