While Federal tax returns often dominate the conversation during tax season, filing state taxes is an equally critical component of your personal finance strategy. For many Americans, state taxes represent a significant portion of their annual financial obligations. Understanding the nuances of state-level taxation is not just about compliance; it is about optimizing your cash flow, maximizing potential refunds, and avoiding the stiff penalties that come with late or incorrect filings.

Unlike the Internal Revenue Service (IRS), which provides a unified system for the entire country, state tax laws are a patchwork of varying regulations, rates, and requirements. Navigating this landscape requires a structured approach to ensure you are meeting your obligations without overpaying.

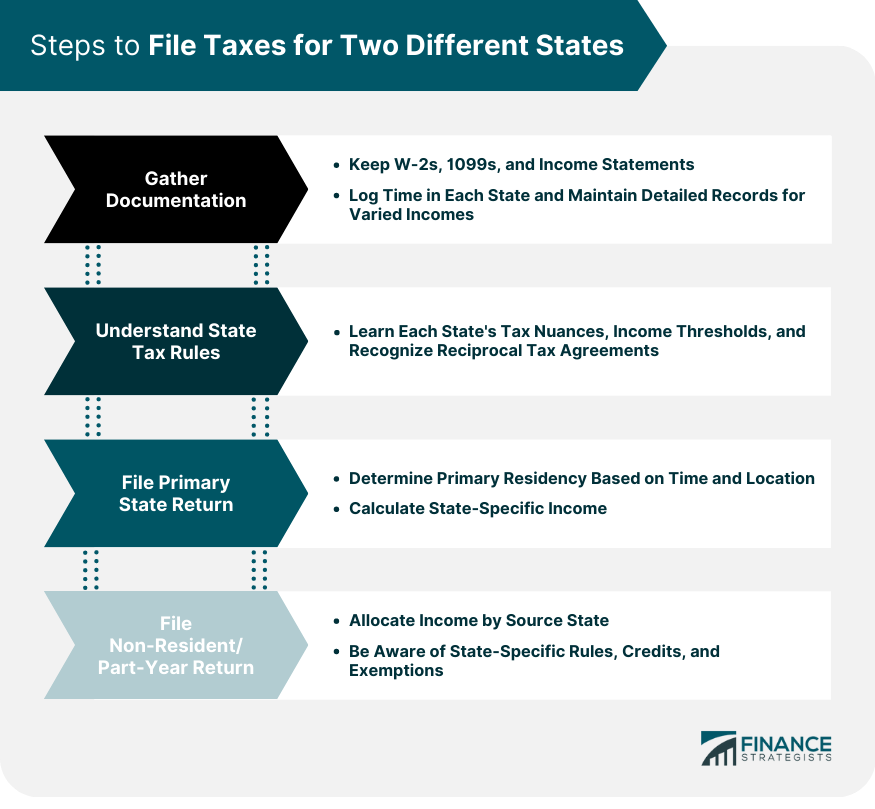

Determining Your State Filing Requirements and Residency Status

The first step in filing state taxes is identifying which states have a legal claim to your income. While the federal government taxes all U.S. citizens on their global income, states generally only tax income that has a “nexus” or connection to that specific state.

Identifying Your Tax Residency

Your residency status is the primary factor determining how you are taxed. States typically categorize filers into three groups:

- Full-Year Residents: If you lived and worked in one state for the entire calendar year, your filing process is straightforward. You will report all income earned to that state.

- Part-Year Residents: If you moved from one state to another during the year, you may be required to file “part-year” returns in both states. This involves prorating your income based on the dates you lived in each location.

- Non-Residents: You may need to file a non-resident return if you live in one state but earned income in another—for example, through freelancing, rental property, or a job that required physical presence in a different state.

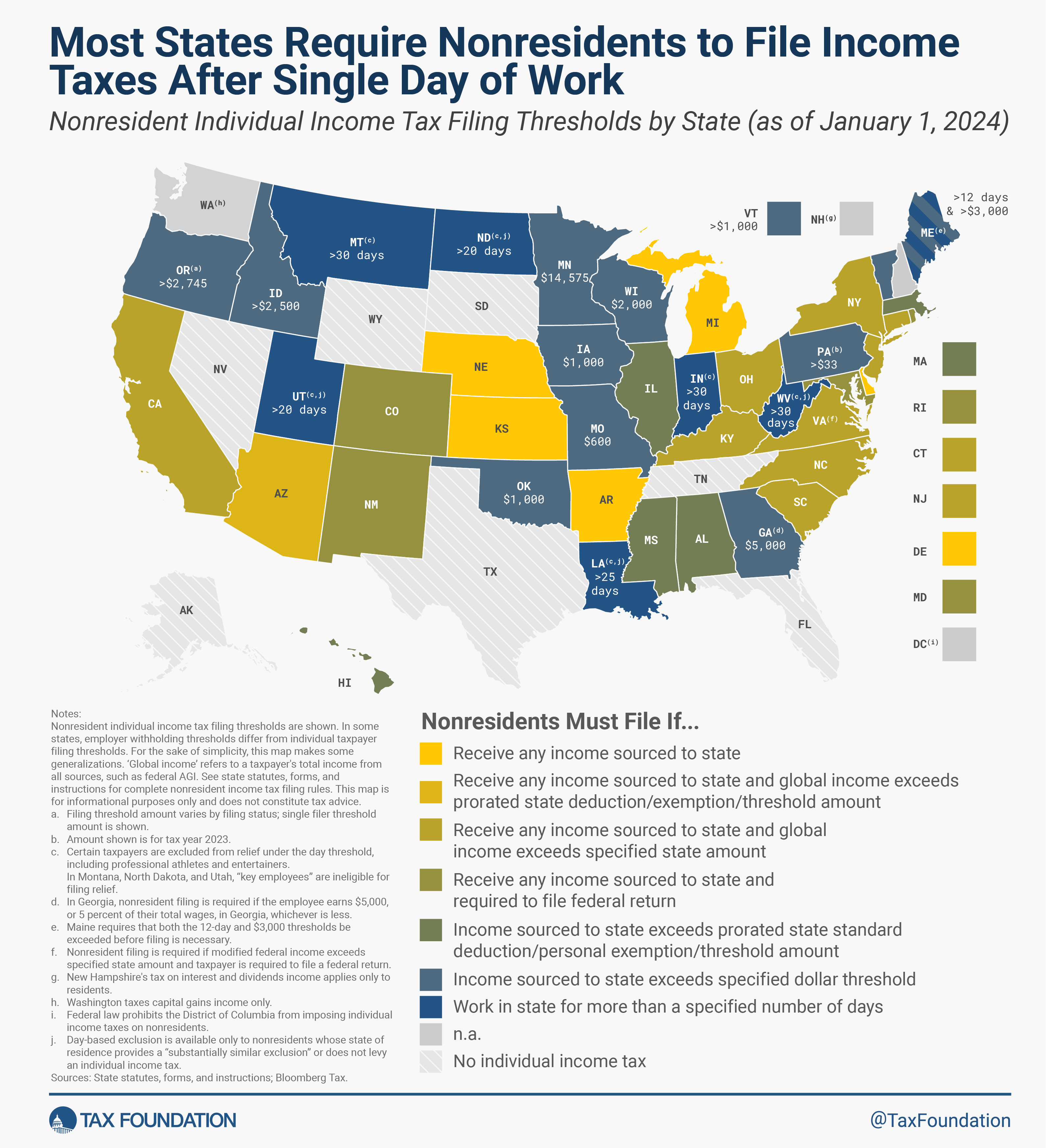

States Without Income Tax

It is important to note that not all residents face a state income tax burden. As of the current tax year, several states—including Alaska, Florida, Nevada, South Dakota, Tennessee, Texas, Washington, and Wyoming—do not levy a traditional state income tax. However, residents of these states may still have other filing obligations, such as taxes on dividends and interest or business-related filings. If you live in a tax-free state but work in a state that does tax income, you will likely still need to file a non-resident return in the state where the income was generated.

Income Thresholds and Filing Triggers

Every state sets its own minimum income threshold for filing. In some states, if your gross income falls below a certain level (often tied to the standard deduction), you may not be required to file a return at all. However, it is often beneficial to file even if you are below the threshold if state taxes were withheld from your paycheck, as this is the only way to claim a refund of those overpaid funds.

Selecting the Most Efficient Filing Method

Once you have determined where you need to file, the next hurdle is choosing how to file. The landscape of tax preparation has shifted significantly toward digital solutions, offering various pathways depending on your financial complexity and budget.

Leveraging State-Sponsored Electronic Filing

Most state revenue departments have invested heavily in their own online portals. Many states now offer “Direct File” programs that allow residents to submit their state returns for free directly through the state’s website. These systems are often the most cost-effective method for taxpayers with simple financial situations, such as those with only W-2 income and standard deductions. Unlike commercial software, these portals are designed specifically for that state’s unique forms and schedules, reducing the likelihood of transcription errors.

Commercial Software and Integrated Filing

For individuals with more complex financial lives—such as small business owners, active investors, or those with multi-state income—commercial tax software (like TurboTax, H&R Block, or FreeTaxUSA) is often the preferred choice. These tools offer the advantage of “data pulling,” where the software automatically imports information from your federal return into your state return. This integration is crucial for maintaining consistency across filings, as many state returns begin with your Federal Adjusted Gross Income (AGI) as the baseline.

The Role of Professional Tax Preparers

If your financial situation involves high-net-worth investments, complex corporate structures, or significant side-hustle income across multiple jurisdictions, hiring a Certified Public Accountant (CPA) or Enrolled Agent (EA) may be a wise investment. A professional can provide personalized advice on state-specific tax planning strategies that automated software might overlook. From a financial perspective, the cost of a professional preparer is often offset by the tax savings they identify and the peace of mind they provide during a potential audit.

Maximizing Deductions and State-Specific Tax Credits

The “Money” aspect of filing state taxes truly comes alive when you begin exploring deductions and credits. State governments often use tax incentives to encourage certain behaviors, such as saving for education, investing in green energy, or supporting local businesses.

Common State-Level Deductions

Many states allow you to choose between a standard deduction and itemizing your deductions, similar to the federal process. However, the rules for what can be deducted often diverge. Some states allow deductions for:

- 529 College Savings Plans: Many states offer a full or partial deduction for contributions made to a state-sponsored 529 plan, providing a powerful incentive for families to save for education.

- Medical Expenses: Some states have lower thresholds for deducting medical expenses than the federal government, making it easier to reduce your taxable income.

- State and Local Taxes (SALT): While federal law caps the SALT deduction, the way states handle the interplay of property taxes and income taxes varies wildly.

Strategic Tax Credits

Tax credits are more valuable than deductions because they reduce your tax liability dollar-for-dollar.

- Earned Income Tax Credit (EITC): Many states offer a “piggyback” EITC, which provides additional relief to low-to-moderate-income working individuals and families.

- Child and Dependent Care Credits: To help offset the cost of childcare, several states offer credits that can significantly lower your end-of-year tax bill.

- Property Tax Credits: Some states provide “circuit breaker” credits for homeowners or renters whose property taxes represent a high percentage of their total income.

Navigating Multi-State Filing and Remote Work Challenges

The rise of the digital economy and remote work has complicated state tax filing for millions. If your income originates in one state while you reside in another, you face a unique set of financial rules.

Understanding Reciprocity Agreements

To simplify life for commuters, many neighboring states have “reciprocity agreements.” These agreements allow residents who work in a neighboring state to pay income tax only to their state of residence. For example, a resident of Virginia who works in Washington D.C. can generally file just one return in Virginia. Understanding these agreements is essential to avoid “double-taxation” and the headache of filing multiple returns.

The “Convenience of the Employer” Rule

Some states, most notably New York, employ a “convenience of the employer” rule. Under this regulation, if your employer is based in that state, they may tax your income even if you are working remotely from a different state, unless your remote status is a requirement of the employer rather than a personal choice. This can create a significant financial burden, as you may find yourself paying taxes to a state you rarely visit. In these cases, your home state usually offers a credit for taxes paid to another state, but the math can be incredibly complex.

Handling “Nexus” for Side Hustles

If you run an online business or a side hustle, you must be aware of “economic nexus” laws. If your business generates a certain amount of revenue or a specific number of transactions in a state where you don’t live, you may be required to collect sales tax and file business income taxes in that state. This is a critical area of business finance that requires careful tracking of where your customers are located.

Long-Term Financial Planning and Record Management

Effective tax filing is not a once-a-year event; it is a year-round discipline. Managing your records and planning your payments can prevent financial shocks and ensure a smooth filing process.

Digital Record Keeping for Audit Protection

The statute of limitations for state tax audits varies, but it is generally recommended to keep all tax-related documents for at least seven years. This includes W-2s, 1099s, receipts for deductible expenses, and proof of residency. Maintaining a digital archive of these documents ensures that if a state revenue department questions your return three years from now, you have the evidence ready to defend your filing.

Managing Estimated Tax Payments

For those with significant non-wage income—such as freelancers, investors, or business owners—waiting until April to pay your state taxes can lead to underpayment penalties. Most states require quarterly estimated tax payments. Integrating these payments into your monthly budget ensures that you are not hit with a massive, unexpected bill during tax season. It also helps in maintaining a more accurate picture of your “true” net income throughout the year.

Preparing for Deadlines and Extensions

While the federal tax deadline is typically April 15th, state deadlines do not always align. Some states set their deadlines later in April or even in May. Furthermore, an extension to file your federal return does not always automatically grant an extension for your state return. You must verify the specific requirements for your state to avoid late-filing fees, which can accumulate interest quickly, eating into your hard-earned savings.

By taking a proactive, informed approach to state taxes, you transform a mundane legal obligation into a strategic financial tool. Whether you are maximizing credits, navigating the complexities of remote work, or simply choosing the most cost-effective filing method, mastering your state taxes is an essential step toward long-term financial stability.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.