Missing a tax deadline is a common occurrence, but when one year turns into several, the psychological and financial weight can become overwhelming. Whether due to a personal crisis, missing documentation, or simple procrastination, failing to file your taxes creates a significant “financial leak” in your personal economy. Fortunately, the path to compliance is well-defined. Filing prior year taxes is not just about staying on the right side of the law; it is a critical move for your personal financial health, allowing you to claim owed refunds, protect your Social Security benefits, and secure your ability to obtain credit.

This guide explores the strategic approach to handling back taxes, the technical steps required to file, and the financial tools available to help you manage potential debt.

1. Understanding the Financial Implications of Unfiled Returns

Before diving into the paperwork, it is essential to understand why the IRS—and your own financial portfolio—requires these returns. Many taxpayers believe that if they don’t owe money, they don’t need to file. This is a misconception that can cost thousands of dollars.

The Three-Year Window for Refunds

One of the most significant financial risks of not filing is the permanent loss of your tax refund. The IRS generally provides a three-year window to claim a refund. If you do not file a return within three years of its original due date, the money becomes the property of the U.S. Treasury. For millions of Americans, this means leaving “found money” on the table that could have been used for debt repayment, emergency funds, or investments.

The Risk of a “Substitute for Return” (SFR)

If you fail to file, the IRS may eventually file a “Substitute for Return” on your behalf. While this might sound like they are doing the work for you, it is rarely in your favor. When the IRS prepares an SFR, they use the income reported by your employers (via W-2s and 1099s) but typically do not include any deductions, credits, or exemptions you might be entitled to. This often results in a tax bill much higher than what you would actually owe if you filed yourself.

Impact on Credit and Loan Approvals

From a personal finance perspective, unfiled taxes are a major hurdle for significant life milestones. If you apply for a mortgage, a small business loan, or even federal student aid (FAFSA), the lender will almost certainly require copies of your filed tax returns. Incomplete tax records signal financial instability to lenders, often leading to immediate rejection.

2. Gathering the Necessary Financial Documentation

Filing for a prior year is more complex than filing for the current year because the data is often buried or lost. To ensure accuracy and maximize your deductions, you must reconstruct your financial history for that specific period.

Retrieving Lost Income Statements

If you have lost your W-2s or 1099s from three or four years ago, you shouldn’t guess the numbers. You can request a “Wage and Income Transcript” from the IRS. This document summarizes the information that employers and financial institutions reported to the IRS under your Social Security number. This is the most reliable way to ensure your filing matches the IRS’s records, reducing the risk of an audit.

Locating Year-Specific Tax Forms

Tax laws and forms change every year. You cannot file a 2020 tax return on a 2023 form. You must download the specific revision of Form 1040 for the year you are filing. This also applies to schedules (like Schedule C for business income or Schedule SE for self-employment tax). Using the wrong year’s form will result in the IRS rejecting your submission, further delaying your compliance.

Accounting for Business Expenses and Deductions

For those with side hustles or small businesses, reconstructing expenses from years past requires a deep dive into bank statements and credit card records. Because the “burden of proof” lies with the taxpayer, you must ensure you have documentation for any deductions claimed. If you are missing receipts, look for digital footprints—email confirmations, bank line items, and calendar entries—to justify your business expenses.

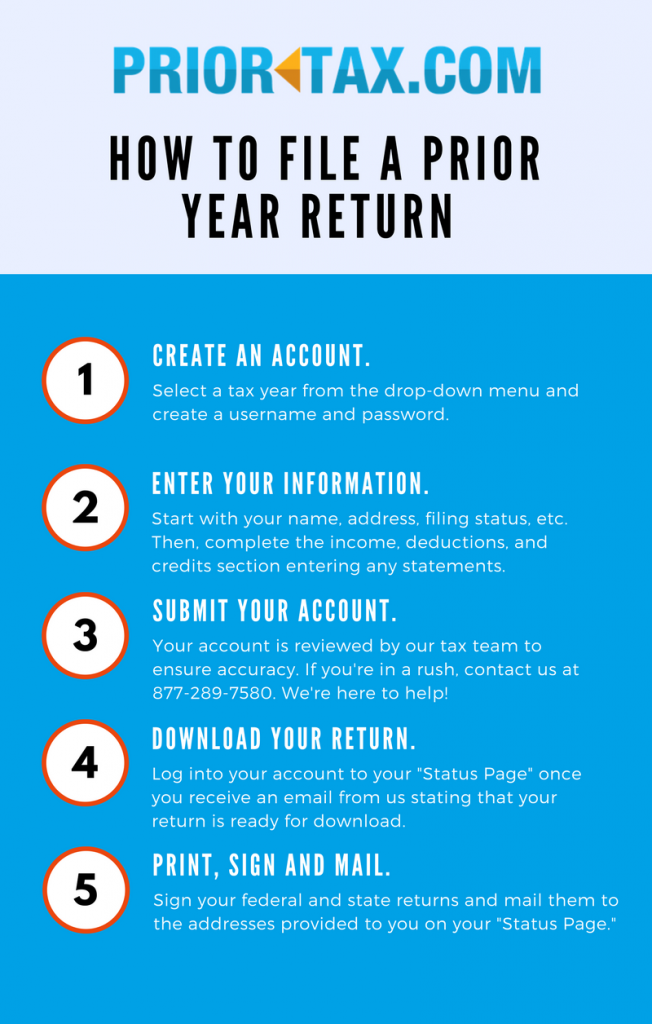

3. The Step-by-Step Process for Filing Back Taxes

Once your documentation is in order, the actual process of filing requires a methodical approach. Unlike current-year taxes, prior-year returns often require manual intervention and physical mailing.

Preparing the Return: Software vs. Manual Filing

Most popular tax software programs allow you to prepare prior-year returns, but they often charge a separate fee for each year. Additionally, you generally cannot e-file a prior-year return as an individual; e-filing is typically reserved for the current tax year. You will likely need to print the completed forms, sign them, and mail them to the specific IRS processing center designated for your region.

The Importance of Sequential Filing

If you are behind on multiple years, it is generally best to file them in chronological order. Your “Adjusted Gross Income” (AGI) from one year often carries over or affects calculations for the next. For example, capital losses that exceed the annual limit can be carried forward to future years. By filing in order, you ensure that these financial benefits flow correctly through your history.

Verifying the Mailing Process

When dealing with back taxes, “proof of filing” is your greatest defense. Always send your returns via Certified Mail with a Return Receipt Requested. This provides you with a paper trail proving that you submitted the documents on a specific date. If the IRS later claims they never received your return, that receipt is your “get out of debt” card regarding late-filing penalties.

4. Managing Penalties, Interest, and IRS Debt

If you discover that you owe money for prior years, the financial math changes. The IRS charges both a “failure to file” penalty and a “failure to pay” penalty, plus compounded interest.

Calculating the Cost of Delay

The failure to file penalty is generally 5% of the unpaid taxes for each month or part of a month that a tax return is late. This penalty caps at 25%. The failure to pay penalty is 0.5% per month. Because these costs compound, a small tax bill can quickly balloon into a significant financial burden. However, filing the return—even if you cannot pay immediately—stops the “failure to file” penalty from growing.

Exploring the IRS “Fresh Start” Program

For taxpayers facing significant debt, the IRS offers several relief options under the “Fresh Start” initiative.

- Installment Agreements: This allows you to pay your debt over a period of up to 72 months. It is an excellent tool for maintaining cash flow while satisfying your tax obligations.

- Offer in Compromise (OIC): In extreme cases of financial hardship, the IRS may allow you to settle your tax debt for less than the full amount you owe. This requires an extensive disclosure of your assets and income.

- Penalty Abatement: If you have a valid reason for not filing (e.g., serious illness or natural disaster) and have a clean history for the previous three years, you may qualify for “First-Time Abatement” to have your penalties removed.

Dealing with Interest

While the IRS has the authority to waive penalties, they rarely waive interest. Interest is set by law and is tied to the federal underpayment rate. The best strategy to minimize interest is to pay as much as possible as early as possible, even before the IRS officially processes your old returns.

5. Protecting Your Financial Future Through Compliance

Filing your prior year taxes is more than a corrective measure; it is a foundational step in building a sustainable financial future. Once you are caught up, the focus shifts to staying current and optimizing your tax position.

Adjusting Withholdings and Estimated Payments

The most common reason for falling behind on taxes is an incorrect withholding amount or a failure to pay estimated quarterly taxes for self-employed income. Use the “IRS Tax Withholding Estimator” tool to ensure your current employer is taking out the right amount. If you are an entrepreneur, set aside 25-30% of every check into a high-yield savings account specifically for tax season. This ensures that you are never surprised by a bill you cannot pay.

Building a Relationship with a Tax Professional

For those with complex financial lives—including investments, real estate, or business income—working with a Certified Public Accountant (CPA) or an Enrolled Agent (EA) is an investment rather than a cost. These professionals can identify deductions you might have missed and represent you before the IRS if any issues arise with your prior-year filings.

The Peace of Mind Dividend

Beyond the numbers, there is a significant psychological benefit to being “tax compliant.” The stress of an unfiled return often prevents individuals from making big financial moves, like buying a home or starting a business. By cleaning the slate, you regain the freedom to manage your money with confidence, knowing that your financial foundation is solid and transparent.

In conclusion, filing prior year taxes is a manageable process that requires organization, persistence, and a clear understanding of IRS protocols. By taking these steps, you stop the accumulation of penalties, protect your eligibility for refunds, and ensure that your financial record reflects your true economic standing. Whether you do it yourself or hire a professional, the best time to start is today.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.