Understanding exactly how much money flows into your bank account each month is the cornerstone of financial literacy. While it may seem as simple as looking at a pay stub, the reality of modern personal finance is often far more complex. With the rise of the gig economy, side hustles, investment dividends, and varying tax structures, “calculating monthly income” has become a strategic exercise rather than a simple math problem.

Whether you are looking to create a bulletproof budget, apply for a mortgage, or plan for early retirement, having a precise grasp of your monthly earnings is essential. This guide provides a professional deep dive into the methodologies of income calculation, ensuring you account for every dollar while maintaining a realistic view of your purchasing power.

1. Distinguishing Between Gross and Net Income

The most frequent error in financial planning is confusing gross income with net income. To manage your finances like a professional, you must understand that the “big number” on your contract is rarely the amount available for your expenses.

Understanding Gross Monthly Income

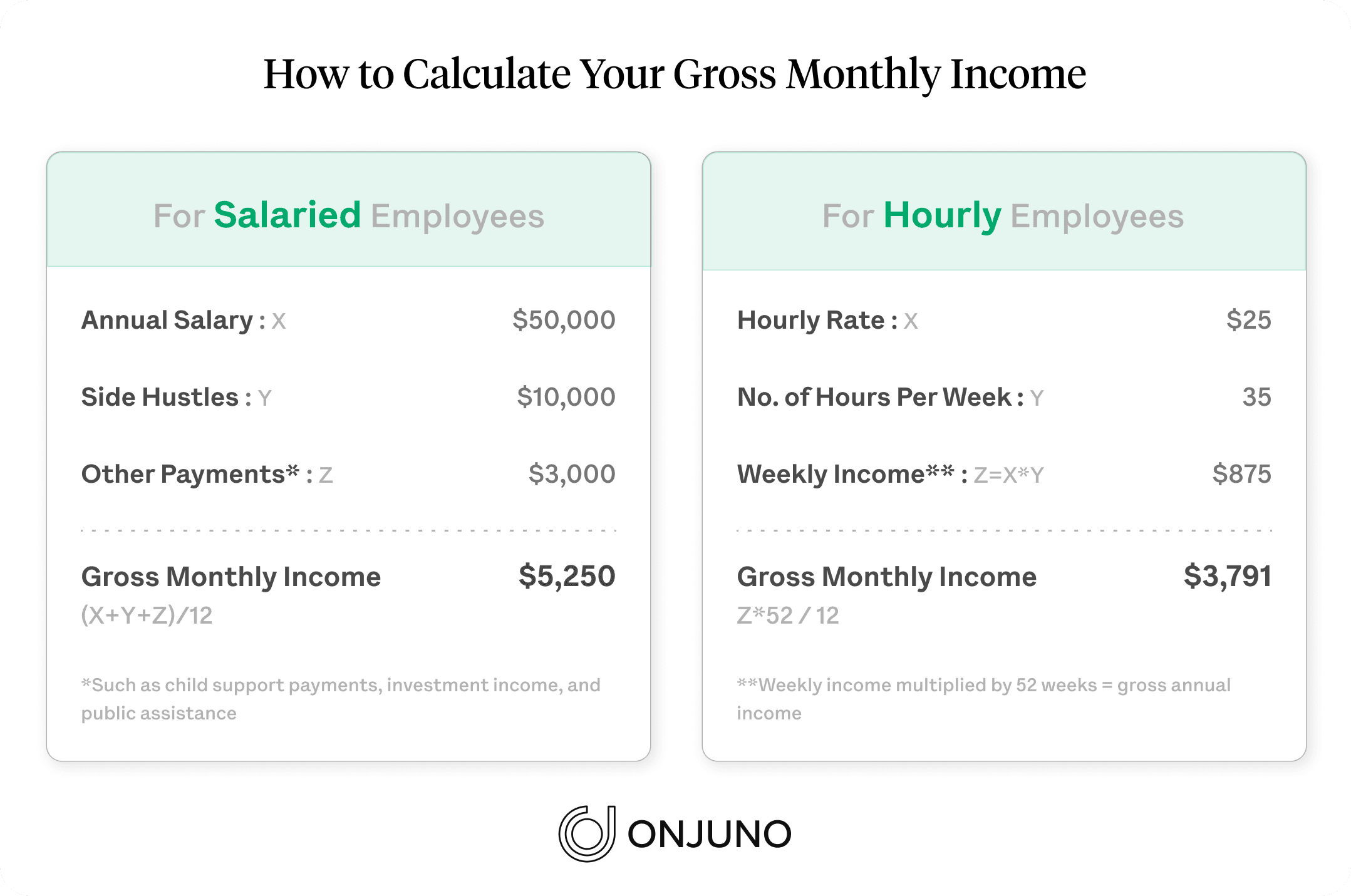

Gross monthly income is the total amount you earn before any taxes or deductions are removed. For salaried employees, this is typically your annual salary divided by twelve. If you are an hourly worker, it is your hourly rate multiplied by the average number of hours worked per month.

Gross income is a critical metric because it is what lenders and credit card companies use to determine your creditworthiness. However, for daily life, relying on your gross income can lead to a dangerous overestimation of your spending capacity.

The Reality of Net Income (Take-Home Pay)

Net income is the “bottom line”—the actual amount deposited into your account. To calculate this accurately, you must subtract several key components from your gross pay:

- Federal and State Taxes: Depending on your jurisdiction and bracket, this can consume 10% to 35% of your earnings.

- FICA Contributions: This includes Social Security and Medicare taxes.

- Health and Insurance Premiums: If you have employer-sponsored healthcare, these premiums are usually deducted directly from your check.

- Retirement Contributions: 401(k) or 403(b) contributions are often pre-tax, reducing your current take-home pay while building future wealth.

Calculating the Monthly Average for Bi-Weekly Pay

Many professionals are paid bi-weekly (every two weeks) rather than twice a month. This results in 26 paychecks per year. To find your true monthly average, do not simply multiply one paycheck by two. Instead, multiply one paycheck by 26 and divide the total by 12. This accounts for the “bonus” months where you receive three paychecks, providing a more accurate monthly baseline.

2. Navigating Variable and Irregular Income Streams

In the modern economy, a single stable paycheck is no longer the universal norm. Freelancers, contractors, and those with performance-based bonuses face the challenge of “income volatility.” Figuring out monthly income in these scenarios requires a more conservative and analytical approach.

The Trailing Average Method

For those with fluctuating earnings—such as real estate agents or freelance consultants—the most effective way to determine monthly income is the six-month or twelve-month trailing average. By totaling your earnings over the last year and dividing by twelve, you smooth out the peaks and valleys. Professional financial planners often recommend using the lowest-earning month of the past year as your “baseline” for budgeting, while treating anything above that as a surplus for savings.

Factoring in Bonuses and Commissions

If a significant portion of your income is derived from quarterly bonuses or sales commissions, these should be categorized separately from your “core” monthly income. Because these funds are not guaranteed, they should not be used to cover fixed costs like rent or car payments. Instead, treat them as “accelerants” for your financial goals, such as debt repayment or investment.

Accounting for Self-Employment Taxes

If you are a 1099 contractor or business owner, your “gross” income is misleading because no taxes are withheld at the source. A professional rule of thumb is to set aside 25% to 30% of every dollar earned into a separate high-yield savings account for quarterly estimated tax payments. Only after this “tax tax” is removed can you begin to calculate your actual monthly income.

3. Identifying and Incorporating Passive Income

True financial health is often measured by the diversity of income streams. When figuring out your monthly income, it is vital to include the “invisible” money generated by your assets.

Investment Dividends and Interest

If you hold dividend-paying stocks or high-yield savings accounts, these generate monthly or quarterly cash flow. While many choose to reinvest these dividends automatically, they still constitute part of your total monthly income. For a comprehensive financial view, aggregate the annual yield of your portfolio and divide it by twelve to see how much your capital is contributing to your lifestyle.

Rental Income and Real Estate

For those with investment properties, calculating monthly income requires a “Net Operating Income” (NOI) mindset. Your monthly income is not the rent check you receive; it is the rent minus the mortgage, property taxes, insurance, and a “sinking fund” for maintenance. If the rent is $2,000 but expenses are $1,600, your actual monthly income from that asset is $400.

Royalties and Digital Assets

In the digital age, many individuals earn monthly income from book royalties, online courses, or affiliate marketing. Because these streams can be “lumpy,” they should be tracked over a longer duration to establish a reliable monthly median.

4. Tools and Methodologies for Tracking

Accuracy in calculating income is rarely achieved through memory alone. It requires a systematic approach and the right financial tools to ensure that no revenue stream is overlooked and no expense is undercounted.

Financial Aggregation Software

Tools like Mint, YNAB (You Need A Budget), or specialized banking apps can automatically aggregate your various income streams. By linking your bank accounts, brokerage accounts, and payment processors (like PayPal or Stripe), these tools provide a real-time dashboard of your total monthly inflows. This technology is particularly useful for identifying small, recurring income sources that might otherwise be forgotten.

The Manual Audit (The Spreadsheet Method)

Despite the convenience of apps, many high-net-worth individuals prefer the manual spreadsheet method for its forced intentionality. By manually entering every deposit into a ledger once a month, you become intimately aware of your financial trajectory. A professional-grade spreadsheet should have columns for:

- Source of Income

- Gross Amount

- Tax/Deduction Amount

- Net Amount

- Frequency (Weekly, Bi-weekly, Monthly)

Bank Statement Reconciliation

At the end of each month, perform a “reconciliation.” Compare your calculated income against your actual bank deposits. If there is a discrepancy, it often points to an overlooked subscription, a bank fee, or an error in tax withholding. This level of scrutiny ensures that your “figured” income matches your “actual” reality.

5. Strategic Application: Why the Number Matters

Knowing your monthly income is not just an academic exercise; it is a diagnostic tool used to measure your financial progress and stability.

The Debt-to-Income (DTI) Ratio

Lenders use your gross monthly income to calculate your DTI ratio. To maintain a healthy financial profile, your total monthly debt payments (including housing) should ideally not exceed 36% of your gross income. If your calculated monthly income reveals a DTI higher than 43%, it is a professional signal that you are over-leveraged and need to either increase income or aggressively pay down debt.

Establishing the Emergency Fund

Financial experts recommend maintaining an emergency fund of three to six months of expenses. However, a more robust way to calculate this is based on your net monthly income. By knowing exactly what you bring home, you can set a target for your “peace of mind” fund that truly reflects your lifestyle and provides a safety net that is proportional to your earning power.

Future Planning and Scalability

Finally, figuring out your monthly income allows you to set a “savings rate”—the percentage of your net income that goes toward investments. Whether your goal is 10%, 20%, or 50%, this percentage is the single greatest predictor of long-term wealth. Without a solid monthly income figure, your savings rate is merely a guess.

In conclusion, figuring out your monthly income requires a blend of basic arithmetic and strategic foresight. By distinguishing between gross and net, accounting for the volatility of side hustles, and leveraging modern tracking tools, you move from financial ambiguity to total command over your economic future. Clarity in what you earn is the first, and most important, step in determining what you can become.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.