Purchasing a car is a significant financial commitment for most individuals, often representing one of the largest debts outside of a mortgage. Understanding how to accurately figure car payments is not just about crunching numbers; it’s about empowering yourself with knowledge to make informed decisions, negotiate effectively, and ensure your vehicle acquisition aligns with your broader financial goals. Without this foundational understanding, buyers risk overextending their budgets, falling prey to unfavorable loan terms, or simply making choices that don’t serve their long-term financial health.

This guide will demystify the process of calculating car payments, breaking down the key variables, exploring the underlying financial formulas, and offering practical strategies to approach car financing with confidence. From the moment you consider buying a new or used vehicle to signing on the dotted line, knowing how your monthly payment is derived will be your most valuable tool.

Understanding the Core Components of a Car Loan

At its heart, a car loan is an agreement to borrow a sum of money, pay it back over time, and pay an additional amount—interest—for the privilege of borrowing. Several key components dictate the size of your monthly payment. Grasping these individual elements is the first step towards accurately figuring out your financial commitment.

The Principal Loan Amount: What You’re Actually Borrowing

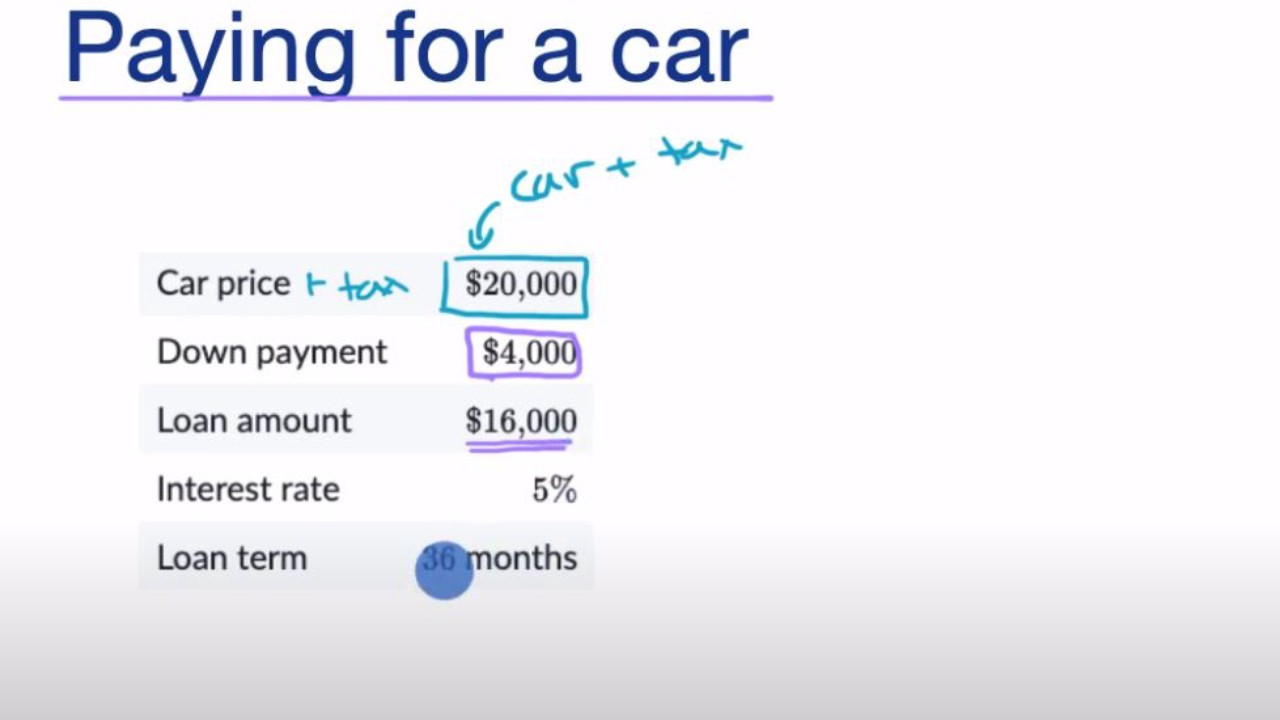

The principal is the total amount of money you are borrowing to purchase the vehicle. This isn’t necessarily the sticker price of the car. It’s the agreed-upon sale price minus any down payment, trade-in value, and potentially adjusted by the inclusion of taxes, fees, and extended warranties rolled into the loan. A lower principal amount directly translates to lower monthly payments and less interest paid over the life of the loan. This is why making a substantial down payment or securing a good trade-in value is so crucial.

Interest Rate (APR): The Cost of Borrowing

The interest rate, often expressed as an Annual Percentage Rate (APR), is perhaps the most impactful factor after the principal. It represents the cost of borrowing money from a lender, expressed as a percentage of the principal per year. A higher APR means you pay more for the loan each month and over its lifetime. Your credit score is the primary determinant of the interest rate you qualify for, with excellent credit scores unlocking the lowest rates. Even a small difference in APR can translate to thousands of dollars over a multi-year loan. For example, on a $30,000 loan over 60 months, a 5% APR yields a monthly payment of $566, while a 7% APR results in $594—a difference of $28 per month, or $1,680 over the loan term.

Loan Term: How Long You’ll Be Paying

The loan term refers to the duration over which you agree to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). A longer loan term generally results in lower monthly payments because the principal is spread out over more installments. However, this convenience comes at a significant cost: you will pay more in total interest over the life of the loan. Conversely, a shorter loan term means higher monthly payments but less total interest paid and quicker debt freedom. It’s a delicate balance between affordability and minimizing overall cost.

Down Payment: Reducing Your Principal

A down payment is an upfront sum of money you pay towards the purchase of the vehicle, reducing the amount you need to finance. This is arguably the most effective way to lower your monthly car payment and the total interest paid. A larger down payment immediately reduces your principal, meaning you borrow less. It also signals to lenders that you are a lower-risk borrower, potentially helping you qualify for a better interest rate. Financial experts often recommend aiming for a down payment of at least 10-20% for a new car and 20% or more for a used car to minimize negative equity and improve loan terms.

The Mechanics of Payment Calculation

While modern technology has made manual calculation less frequent, understanding the underlying formula for an amortizing loan provides invaluable insight into how your payments are structured and how changes to variables impact your bottom line.

The Standard Amortization Formula Explained

Most car loans use an amortization schedule, meaning each payment consists of both principal and interest. In the early stages of the loan, a larger portion of your payment goes towards interest, gradually shifting to more principal as the loan matures. The formula for calculating a fixed monthly loan payment (M) is:

M = P [ i(1 + i)^n ] / [ (1 + i)^n – 1]

Where:

- M = Monthly payment

- P = Principal loan amount

- i = Monthly interest rate (annual APR divided by 12)

- n = Total number of payments (loan term in months)

This formula effectively distributes the total principal and total interest owed over the entire loan term, ensuring each monthly payment is the same.

Practical Application: Manual Calculation Walkthrough

Let’s illustrate with an example:

- P (Principal): $25,000

- APR: 6% (or 0.06 as a decimal)

- n (Loan Term): 60 months

First, calculate the monthly interest rate (i): 0.06 / 12 = 0.005

Now, plug the values into the formula:

M = 25,000 [ 0.005(1 + 0.005)^60 ] / [ (1 + 0.005)^60 – 1]

M = 25,000 [ 0.005(1.005)^60 ] / [ (1.005)^60 – 1]

M = 25,000 [ 0.005(1.34885) ] / [ 1.34885 – 1]

M = 25,000 [ 0.00674425 ] / [ 0.34885 ]

M = 25,000 * 0.0193306

M ≈ $483.27

This manual walkthrough highlights the intricate relationship between each variable and the final payment. Understanding this process, even if you don’t calculate it manually every time, strengthens your grasp of the loan dynamics.

Leveraging Online Calculators and Financial Tools

While manual calculations are enlightening, online car loan calculators are indispensable tools for quickly and accurately figuring out payments. Websites of banks, credit unions, and financial publications offer free, user-friendly calculators. These tools allow you to input different principal amounts, interest rates, and loan terms, instantly showing you the corresponding monthly payment. Many also provide amortization schedules, detailing how much principal and interest you pay with each installment. Using these calculators extensively during your car shopping process allows for easy comparison of different financing scenarios and helps you set realistic budget expectations before even stepping foot in a dealership.

Influential Factors Beyond the Core

While principal, interest rate, and loan term are the direct determinants of your monthly payment, several external factors significantly influence these core components, and thus, your overall financing package.

Credit Score: Your Gateway to Better Rates

Your credit score is arguably the most critical factor influencing the interest rate you’ll be offered. Lenders use your score to assess your creditworthiness and the likelihood of you repaying the loan. A FICO score of 720 or higher is generally considered “excellent” and will qualify you for the most competitive interest rates. Scores below 670 are typically categorized as “subprime” and will likely result in significantly higher interest rates, sometimes even double-digit APRs, making your car payment substantially more expensive. Before applying for a car loan, it’s wise to check your credit report and score, allowing you time to address any inaccuracies or take steps to improve your score if needed.

Trade-In Value: A Strategic Principal Reduction

If you’re replacing an existing vehicle, its trade-in value can act as a direct down payment, reducing the principal amount you need to finance. Researching your current car’s market value using resources like Kelley Blue Book (KBB) or Edmunds before visiting a dealership empowers you to negotiate a fair trade-in price. A higher trade-in value means less money borrowed, leading to lower monthly payments and reduced total interest. Conversely, if your trade-in has negative equity (meaning you owe more on it than it’s worth), that negative amount may be rolled into your new car loan, increasing your principal and your payments.

Sales Tax, Fees, and Other Charges: The Hidden Costs

The sticker price is rarely the final price. Car purchases involve various additional costs that can significantly inflate the total amount financed if not paid upfront. These include:

- Sales Tax: Varies by state, often a percentage of the vehicle’s purchase price.

- Registration and Licensing Fees: Required to legally operate the vehicle, also vary by state.

- Dealer Fees: Such as documentation fees, advertising fees, or preparation fees. These can sometimes be negotiable.

- Extended Warranties/Service Contracts: Optional, but often pushed by dealerships. While they offer peace of mind, they also add to the loan principal if financed.

- GAP Insurance: Covers the difference between what you owe on your loan and the car’s actual cash value if it’s totaled or stolen. Often recommended, but can also be financed.

It’s crucial to get a detailed breakdown of all these costs and understand which ones can be paid out-of-pocket versus which will be added to your loan, impacting your monthly payment.

Strategies for Smart Car Financing

Navigating the car financing landscape can be complex, but with strategic planning, you can significantly optimize your car payments and overall financial burden.

The Power of a Larger Down Payment

As discussed, a larger down payment is your best defense against high monthly payments and excessive interest. Aiming for at least 10-20% of the car’s value reduces the principal, lowers your monthly outlay, and reduces the total interest paid over the loan’s life. Furthermore, a substantial down payment can help you avoid negative equity (where your car is worth less than you owe) and might even help you qualify for a better interest rate. If you can save up for a larger down payment, the long-term savings are substantial.

Negotiating for a Lower Interest Rate

Your interest rate isn’t always fixed. Beyond improving your credit score, you can actively shop around for the best rate. Get pre-approved for a loan from several lenders (banks, credit unions, online lenders) before visiting a dealership. This pre-approval gives you a benchmark interest rate and allows you to walk into the dealership with leverage. The dealership’s finance department may try to beat your pre-approved rate, or at the very least, you’ll know if their offer is competitive. Don’t be afraid to negotiate the APR, especially if you have an excellent credit history.

Choosing an Appropriate Loan Term

While a longer loan term offers lower monthly payments, it costs you more in total interest. Conversely, a shorter term saves interest but demands higher monthly payments. The key is to find a balance that fits your budget without incurring unnecessary interest. For new cars, 60-month loans are common, but extending to 72 or 84 months can inflate total interest considerably. Consider the “total cost of ownership” rather than just the monthly payment. If a shorter term means a tight monthly budget, perhaps a slightly less expensive car with a shorter term is a more financially prudent choice.

Refinancing Your Existing Car Loan

If you’ve already purchased a car and your financial situation has improved (e.g., your credit score has increased, or interest rates have dropped), refinancing your car loan can be an excellent strategy to lower your monthly payments or reduce the total interest you’ll pay. Refinancing involves taking out a new loan to pay off your existing one, ideally with a lower interest rate or a more favorable term. This can free up cash flow each month or significantly reduce your total repayment amount. Research different lenders and compare their refinancing offers to find the best deal.

Holistic Financial Planning for Car Ownership

Figuring out car payments goes beyond mere calculation; it’s about integrating this significant expense into your broader financial picture and planning for long-term ownership.

Integrating Car Payments into Your Overall Budget

A car payment should never be considered in isolation. It needs to fit comfortably within your overall monthly budget alongside housing, food, utilities, savings, and other debt obligations. A common rule of thumb suggests that your total car expenses (payment, insurance, fuel, maintenance) should not exceed 10-15% of your net monthly income. Exceeding this percentage can put a strain on your finances, limit your ability to save, and potentially lead to financial stress. Use budgeting apps or spreadsheets to visualize how a potential car payment impacts your cash flow before committing.

Beyond the Monthly Payment: Total Cost of Ownership

The monthly car payment is just one piece of the puzzle. The “total cost of ownership” includes:

- Depreciation: The decline in the car’s value over time.

- Insurance: A mandatory and significant ongoing expense.

- Fuel: An ever-present and variable cost.

- Maintenance and Repairs: Regular servicing, unexpected repairs, tires, etc.

- Registration and Fees: Annual renewals.

Factoring in all these costs provides a realistic view of how much a car truly costs you each month and year. A car with a lower monthly payment might have higher insurance costs or be known for expensive repairs, potentially making it more costly in the long run than a slightly pricier alternative.

The Importance of Emergency Funds

No matter how meticulously you plan, unexpected car-related expenses can arise—a sudden repair, a minor accident, or a temporary job loss. Having a robust emergency fund in place is crucial to cover these unforeseen costs without derailing your budget or forcing you to take on additional debt. Ideally, this fund should cover 3-6 months of essential living expenses, including your car payment and associated costs. A strong emergency fund provides a financial safety net, allowing you to handle car ownership challenges with confidence rather than anxiety.

By diligently applying these principles—understanding the core components, leveraging calculation tools, recognizing influential factors, employing smart financing strategies, and planning holistically—you can approach car acquisition not as a daunting task, but as a manageable financial decision that supports your overall financial well-being.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.