Stepping into the world of tax filing for the first time can feel like navigating a complex maze blindfolded. For many young professionals, recent graduates, or individuals experiencing significant life changes, the annual obligation to file taxes is a rite of passage that often comes with a hefty dose of apprehension. However, far from being an insurmountable challenge, understanding and fulfilling your tax responsibilities is a fundamental aspect of personal financial management. It’s an opportunity to ensure you’re meeting legal requirements, maximizing your financial health through deductions and credits, and gaining a clearer picture of your income and expenditures.

This guide is designed to demystify the process, offering a clear, step-by-step approach to help you confidently complete your first tax return. We’ll delve into the financial tools and strategies that can simplify the task, ensuring you not only file correctly but also potentially save money along the way. Your first tax filing doesn’t have to be a source of stress; instead, it can be an empowering lesson in financial literacy and compliance.

Understanding the Financial Imperative of Tax Filing

Before diving into the mechanics, it’s crucial to grasp the fundamental financial principles and responsibilities underpinning tax season. Taxes are not merely an administrative burden; they are a direct contribution to public services and an integral part of your personal financial ecosystem. Understanding these basics sets a strong foundation for accurate and advantageous filing.

Who Needs to File and Why It Matters

The primary question for many first-timers is: “Do I even need to file?” The answer hinges on several factors, including your gross income, filing status, and age. For instance, if your income exceeds a certain threshold—which changes annually—you are generally required to file. However, even if you fall below the filing threshold, you might still want to file to receive a refund for taxes already withheld from your paychecks (e.g., through W-2 employment) or to claim certain refundable tax credits. Neglecting to file when required can lead to penalties, interest charges, and a build-up of financial liabilities, which can negatively impact your credit score and future financial dealings. Proactive filing ensures compliance and protects your financial standing.

Decoding Key Tax Concepts: Income, Deductions, and Credits

The language of taxation often seems opaque, but three concepts form its backbone:

- Gross Income: This is the total amount of money you earn from all sources before any deductions or taxes are taken out. It includes wages, salaries, tips, self-employment earnings, investment income, and even certain types of benefits. Accurate reporting of gross income is the starting point for your tax calculation.

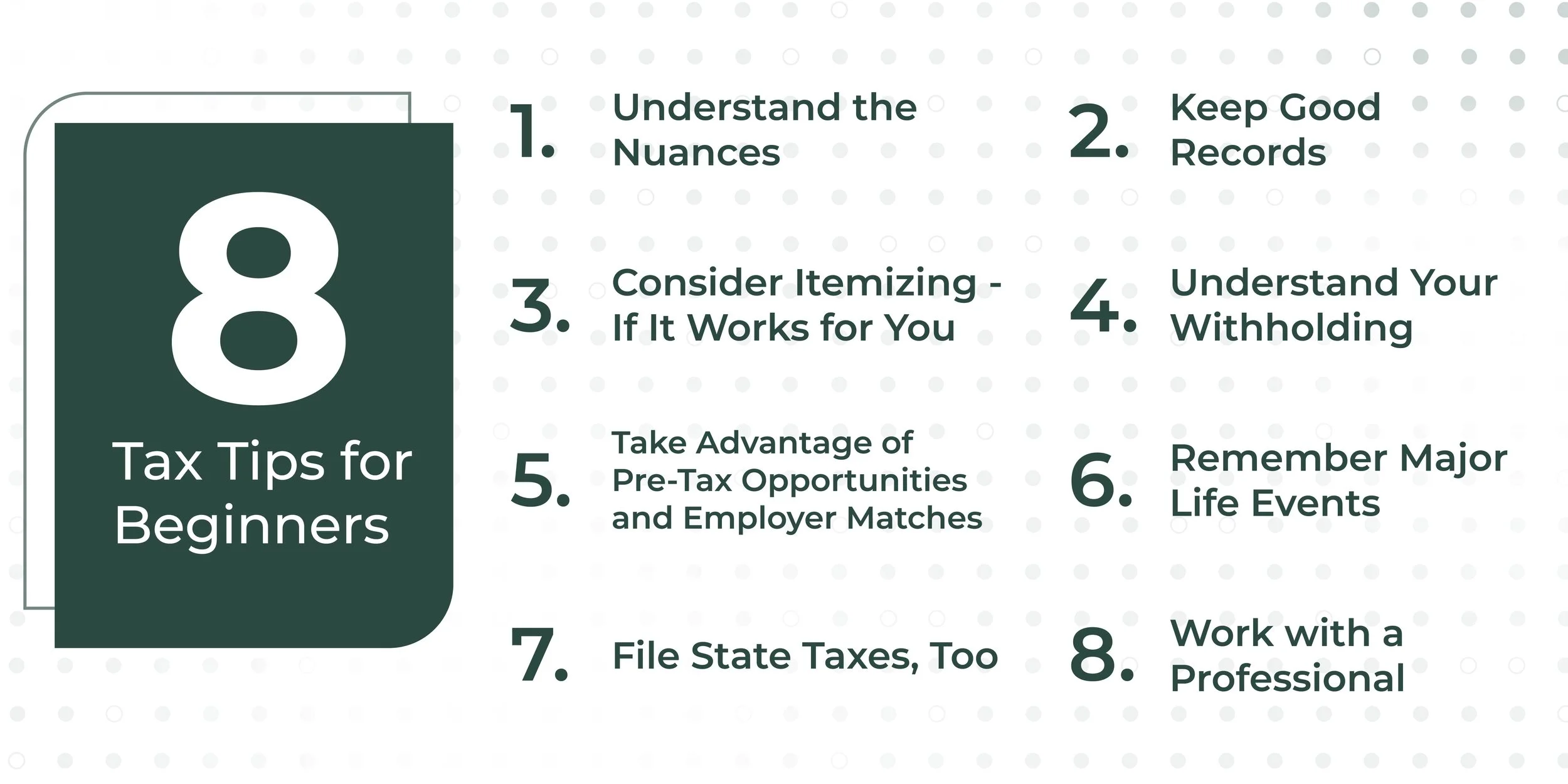

- Deductions: These are amounts that reduce your taxable income. The less taxable income you have, the less tax you owe. Common deductions include contributions to traditional IRAs, student loan interest, and certain itemized deductions like medical expenses or state and local taxes (if you don’t take the standard deduction). Choosing between the standard deduction and itemizing can be a significant financial decision, often determined by which option results in a lower taxable income.

- Credits: Unlike deductions, which reduce your taxable income, tax credits directly reduce the amount of tax you owe, dollar for dollar. Some credits, known as refundable credits, can even result in a refund exceeding the amount of tax you paid. Examples include the Earned Income Tax Credit (EITC), Child Tax Credit, and education credits. Identifying and claiming all eligible credits is paramount for maximizing your refund or minimizing your tax liability.

These concepts are the financial levers you can pull to optimize your tax outcome. A keen understanding of them can significantly impact your financial bottom line for the year.

The Importance of Deadlines: A Financial Non-Negotiable

Tax deadlines are non-negotiable financial milestones. In most countries, the primary filing deadline for individual income tax returns falls in April. Missing this deadline, especially if you owe money, can result in penalties for failure to file and failure to pay, plus interest on the unpaid amount. These financial penalties can accumulate quickly, turning a manageable tax bill into a considerable financial burden. If you anticipate needing more time, filing for an extension is a smart financial move; it gives you more time to file, though not more time to pay any taxes owed. Marking these dates on your calendar and planning accordingly is a basic but critical financial discipline.

Gathering Your Essential Financial Documents

The cornerstone of an accurate tax return is a complete collection of your financial documents. Think of these as the ingredients for your financial stew; without them, the final product will be incomplete or incorrect. Organizing these documents early in the tax season significantly reduces stress and potential errors.

Income Statements: The Core of Your Financial Narrative

Your income statements are the most critical documents. For most employees, this will be Form W-2, provided by your employer, detailing your wages, tips, other compensation, and withheld federal and state taxes. If you’ve worked as a freelancer, independent contractor, or received non-employee compensation, you’ll likely receive Form 1099-NEC. Other 1099 forms cover various types of income, such as interest (1099-INT), dividends (1099-DIV), or distributions from retirement accounts (1099-R). For online income generated through platforms like PayPal or Stripe, you might receive a 1099-K if you meet certain transaction volume thresholds. Consolidating all these forms ensures every source of income is accurately reported, preventing discrepancies that could trigger an audit or penalties.

Proof of Deductions and Credits: Unlocking Financial Savings

To effectively reduce your taxable income or tax liability, you need documentation to back up your claims for deductions and credits. This might include:

- Mortgage Interest Statement (Form 1098): If you own a home, this shows the interest you paid, which is often deductible.

- Student Loan Interest Statement (Form 1098-E): Documents interest paid on student loans, a common deduction for many first-time filers.

- Tuition Statements (Form 1098-T): Essential for claiming education credits like the American Opportunity Tax Credit or Lifetime Learning Credit.

- Records of Charitable Contributions: Receipts or acknowledgment letters for donations to qualified organizations.

- Retirement Contributions: Statements from your IRA or 401(k) showing contributions, particularly relevant for traditional IRA deductions.

- Medical Expense Records: If you itemize deductions and have substantial out-of-pocket medical expenses.

Thorough record-keeping throughout the year directly translates into financial benefits during tax season. Don’t leave money on the table by overlooking these vital documents.

Previous Year’s Tax Returns: A Blueprint for Financial Continuity

While it’s your first time filing this year, if you’ve ever filed before (e.g., as a dependent), having previous returns can be helpful. They provide a blueprint for your financial journey, showing carryover amounts for certain deductions or credits, previous year’s adjusted gross income (AGI) which may be needed for verification, or simply a reference for how certain income or deductions were handled previously. Even if it’s your absolute first time filing independently, familiarizing yourself with generic tax forms can be beneficial.

Choosing Your Filing Method: A Strategic Financial Decision

The method you choose to prepare and file your taxes can impact both the ease of the process and your financial outcome. Each option offers different levels of support, cost, and control.

DIY with Tax Software: Leveraging Financial Tools for Empowerment

For many first-time filers, especially those with straightforward tax situations, using tax preparation software is an excellent, cost-effective option. Financial tools like TurboTax, H&R Block Tax Software, or TaxAct guide you through the process with interview-style questions, automatically populate forms, and perform calculations.

- Free vs. Paid Options: Many software providers offer free versions for basic returns (often federal-only) if your income falls below a certain threshold or if your tax situation is very simple. Paid versions offer more comprehensive features, covering complex deductions, investments, and state tax filings.

- Benefits of Guided Software: These platforms often include robust error checking, ensuring mathematical accuracy and prompting you for common deductions or credits you might overlook. They also securely handle e-filing, which is generally the fastest way to receive a refund. This financial tool empowers you to take control of your tax process.

Professional Tax Preparers: When Expert Financial Advice is Needed

If your financial situation is complex—perhaps you’re self-employed with significant business expenses, have diverse investment portfolios, own multiple properties, or have experienced a major life event—hiring a professional tax preparer can be a wise financial investment.

- When to Consider an Accountant or Enrolled Agent: These professionals (CPAs, Enrolled Agents, or tax attorneys) possess in-depth knowledge of tax law. They can identify less obvious deductions, advise on tax planning strategies for future financial health, and represent you if you face an audit. While it involves a fee, the peace of mind, potential tax savings, and expert guidance can far outweigh the cost for complex scenarios. They are invaluable financial advisors during tax season.

Free Tax Help Programs: Community-Driven Financial Support

For individuals meeting specific income or age requirements, free tax preparation services are available through programs like the Volunteer Income Tax Assistance (VITA) and Tax Counseling for the Elderly (TCE). These programs are staffed by IRS-certified volunteers who provide free basic income tax return preparation. They are excellent community resources for those needing financial assistance and guidance without incurring professional fees.

Navigating the Filing Process Step-by-Step

Once you’ve chosen your method and gathered your documents, the actual filing process becomes a series of structured steps, each critical for financial accuracy.

Inputting Your Information Accurately: Precision is Key

Whether you’re using software or working with a preparer, the core task is accurately inputting all your financial data. This involves transferring information from your W-2s, 1099s, and deduction receipts into the appropriate fields. Double-check account numbers, income figures, and Social Security numbers. A simple typo can lead to significant delays in processing your return or even trigger an IRS inquiry. This meticulousness is a critical financial habit.

Double-Checking for Errors and Missed Opportunities: Optimizing Your Financial Outcome

Before hitting “submit,” thoroughly review your entire return. Most tax software includes a review step that highlights potential issues. Manually check for:

- Unreported Income: Did you forget any small freelance gigs or investment earnings?

- Overlooked Deductions/Credits: Did you claim everything you’re entitled to? Did you contribute to an IRA? Did you pay student loan interest? Are you eligible for any education credits? This is where your financial literacy truly pays off.

- Correct Filing Status: Is “Single,” “Married Filing Jointly,” or “Head of Household” correctly chosen? This impacts your standard deduction and tax brackets.

- Bank Account Information for Direct Deposit: If you’re expecting a refund, ensure your bank routing and account numbers are correct for direct deposit; errors here can cause significant delays in receiving your funds.

This review phase is your last chance to optimize your financial outcome and prevent future headaches.

Submitting Your Return: The Final Financial Act

- E-file vs. Mail: Electronic filing (e-file) is strongly recommended. It’s faster, more secure, and provides immediate confirmation that your return has been received by the tax authority. If you must mail your return, ensure it’s sent via certified mail with a return receipt requested to have proof of mailing and delivery.

- What to Do If You Owe or Are Owed a Refund: If you owe taxes, you typically have options to pay electronically (direct debit, credit card) or via mail with a check. Pay by the deadline to avoid penalties. If you’re due a refund, e-filing with direct deposit is the quickest way to receive your money, often within a few weeks. Managing your cash flow around tax payments or refunds is an important part of personal finance.

Beyond Your First Filing: Planning for Future Financial Health

Your first tax filing is more than just a one-time event; it’s an initiation into ongoing financial responsibility. Developing good habits now will serve your financial health for years to come.

Record-Keeping Best Practices: A Foundation for Financial Accuracy

Establish a system for keeping your financial records organized throughout the year. Whether it’s a dedicated physical folder, a cloud storage service, or a digital app, ensure you have a secure, accessible place for all income statements, receipts for deductions, and records of significant financial transactions. This proactive approach eliminates frantic searches during tax season and ensures you never miss a deduction. This is a fundamental aspect of robust personal financial management.

Adjusting Withholding or Estimated Payments: Proactive Financial Planning

After your first tax season, review your tax outcome. If you received a large refund, it means you overpaid taxes throughout the year. While a refund can feel nice, it essentially means you gave the government an interest-free loan. Consider adjusting your W-4 form with your employer to have less tax withheld, allowing you to keep more of your money throughout the year for investing or saving. Conversely, if you owed a significant amount, you might need to adjust your withholding or make estimated tax payments (especially if you have self-employment income) to avoid penalties next year. This is strategic financial planning in action.

Seeking Professional Advice for Complex Situations: Investing in Expertise

As your financial life evolves—you might start a business, buy a home, invest in the stock market, or experience other major life changes—your tax situation will likely become more complex. Don’t hesitate to seek professional financial advice. A tax advisor can help with long-term tax planning, investment strategies with tax implications, and navigate intricate tax laws. Viewing this as an investment in your financial future, rather than an expense, can yield significant returns.

Your first time doing taxes marks a significant milestone in your financial journey. While it may initially seem daunting, approaching it with a structured plan, understanding key financial concepts, and leveraging available tools will not only ensure compliance but also empower you to make informed financial decisions. This foundational experience is invaluable, setting the stage for a lifetime of confident and competent financial management.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.