In the modern landscape of digital banking and global commerce, credit and debit cards have become the primary vehicles for our daily financial transactions. JPMorgan Chase, as one of the largest financial institutions in the world, processes billions of dollars in transactions every year. However, with this volume of commerce comes the inevitable risk of billing errors, unauthorized charges, or unsatisfactory merchant interactions.

Learning how to effectively dispute a charge with Chase is more than just a customer service task; it is a vital skill in personal financial management. Whether you are dealing with a double-charge at a local restaurant, a subscription that refused to cancel, or a sophisticated fraudulent transaction, understanding the mechanisms of the “chargeback” process ensures that your capital remains protected. This guide provides an in-depth exploration of the dispute process, the legal protections afforded to consumers, and the strategic steps required to ensure a favorable outcome.

Understanding Your Rights Under the Fair Credit Billing Act (FCBA)

Before diving into the technical steps of the Chase mobile app or website, it is crucial to understand the legal framework that empowers consumers. In the United States, the Fair Credit Billing Act (FCBA) provides the backbone for credit card disputes. This federal law protects consumers from “billing errors,” a broad term that includes unauthorized charges, charges for goods not delivered, or charges for the wrong amount.

Fraudulent Transactions vs. Merchant Disputes

It is essential to distinguish between a fraudulent transaction and a merchant dispute, as Chase handles these through slightly different internal workflows.

- Fraudulent Transactions: These occur when your card information is stolen and used without your permission. In these cases, the priority is not just reversing the charge but also securing your account by canceling the compromised card and issuing a new one.

- Merchant Disputes: These occur when you authorized a transaction, but something went wrong with the fulfillment. Examples include receiving a damaged product, being charged the wrong price, or being billed for a service that was never rendered. In these scenarios, your account is usually still secure, but the specific transaction needs correction.

The Legal Timeframes for Filing

Under the FCBA, consumers generally have 60 days from the date the first statement containing the error was mailed to them to dispute a charge in writing. While Chase allows you to initiate disputes via their digital platforms for convenience, staying within this 60-day window is critical for maintaining your federal legal protections. Filing after this window may still result in a successful dispute through Chase’s internal policies, but you lose the absolute legal leverage provided by federal law.

Step-by-Step Guide to Disputing a Charge with Chase

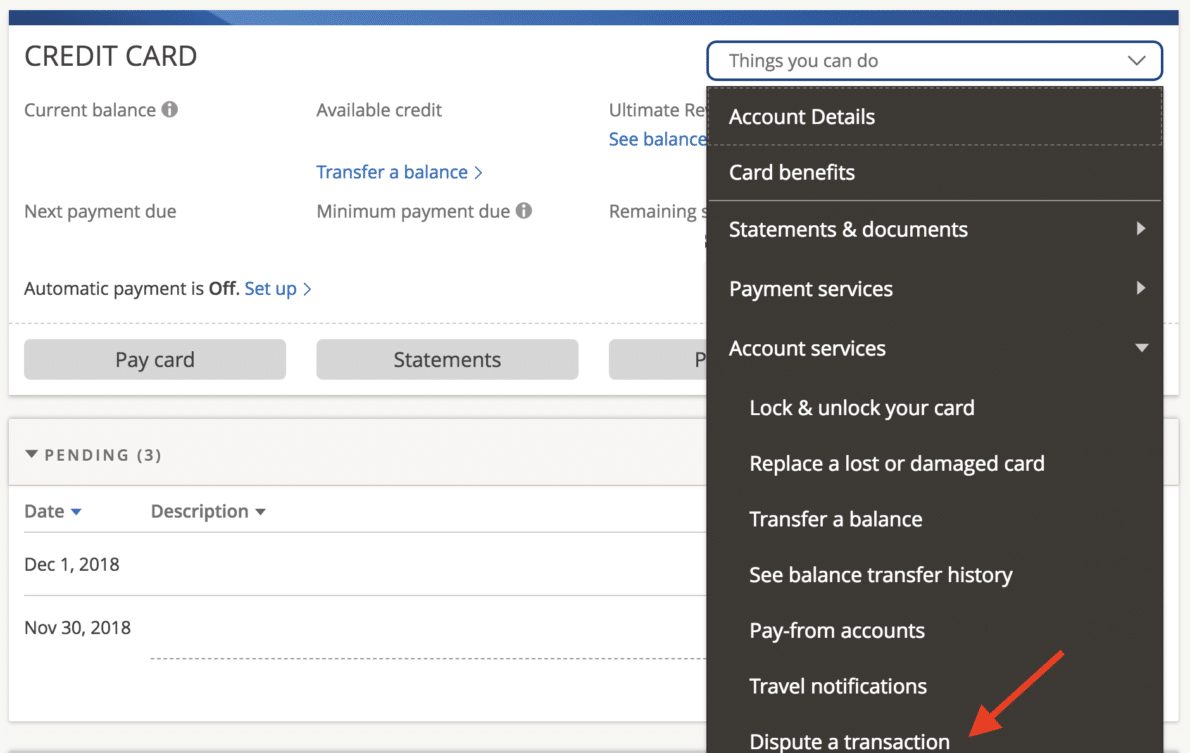

Chase has invested heavily in its digital infrastructure, making it relatively seamless for customers to flag suspicious or incorrect transactions. There are three primary ways to initiate this process: the mobile app, the online portal, and direct communication.

Using the Chase Mobile App

For most users, the mobile app is the fastest route.

- Log In: Securely access your account using biometrics or your password.

- Select the Account: Tap on the specific credit or debit card account where the charge appeared.

- Find the Transaction: Scroll through your transaction history. Once you find the disputed item, tap it to view the transaction details.

- Initiate Dispute: Look for the link or button labeled “Report a Problem” or “Dispute this Transaction.”

- Provide Details: The app will prompt you with a series of questions. Is it fraud? Did you not receive the item? Was the amount incorrect? Answer these accurately to ensure the case is routed to the correct department.

Navigating the Chase Online Portal

If you prefer a desktop view—which is often better for uploading documentation—the Chase website offers a robust dispute interface.

- Sign In: Go to Chase.com and log into your dashboard.

- Transaction Search: Navigate to your “Activity” or “Statements” tab.

- Dropdown Menu: Next to each transaction, there is typically an icon (often a chevron or three dots). Clicking this will reveal the “Dispute Transaction” option.

- Documentation Upload: The desktop version makes it easier to attach PDFs or JPEG images of receipts, cancellation emails, or photos of damaged goods.

Calling Customer Service or Sending Written Notice

While digital methods are efficient, some complex cases benefit from human intervention. You can call the number on the back of your card to speak with the Chase Claims Department. If you wish to invoke your full rights under the FCBA, it is often recommended to follow up a digital or phone dispute with a written letter sent via certified mail to the address listed on your billing statement for “billing inquiries.” This creates a definitive paper trail that is legally recognized.

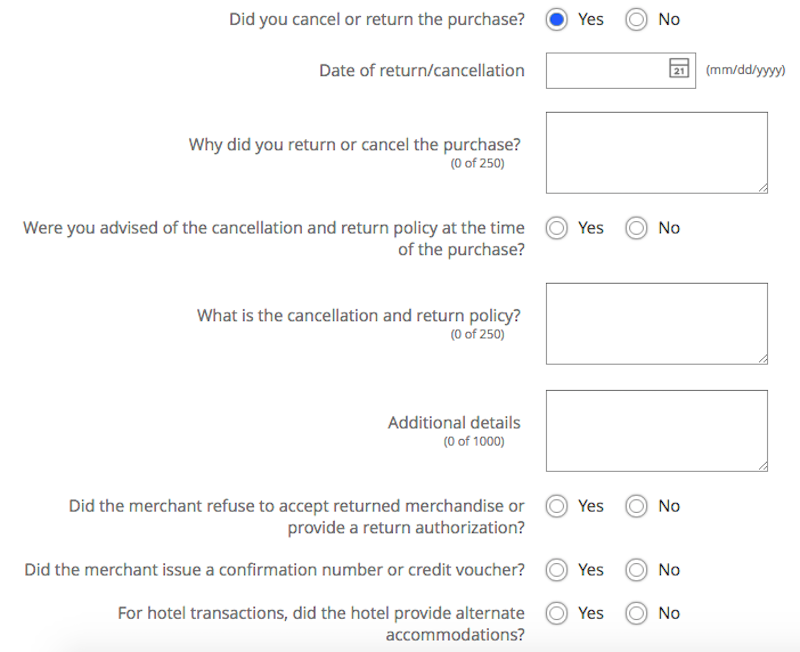

Gathering Evidence for a Successful Outcome

Initiating a dispute is only the first half of the battle. Once Chase receives your claim, they act as a mediator between you and the merchant’s bank. To win the dispute, you must provide a compelling case that proves the charge was illegitimate or erroneous.

Documenting Communication with the Merchant

Chase (and the law) generally requires that you make a “good faith effort” to resolve the issue with the merchant directly before filing a dispute. Save every email, chat log, and record of phone calls. If you attempted to return an item or cancel a subscription, the timestamped confirmation of that attempt is your most powerful piece of evidence. If a merchant promised a refund but failed to issue it within the promised timeframe, a screenshot of that promise is “the smoking gun” for your claim.

Providing Proof of Delivery or Cancellation

In disputes involving physical goods, evidence is often binary.

- Non-Delivery: If a package never arrived, provide tracking numbers that show the item was never delivered or was sent to the wrong address.

- Not as Described: If you received a product that was significantly different from the advertisement, take clear photos. Comparison photos (the website’s image vs. the actual product) are highly effective.

- Cancellations: For recurring subscriptions, the “Cancellation Confirmation” email is essential. If the merchant does not provide one, a screenshot of the “Account Settings” page showing the subscription status as “Canceled” will suffice.

What Happens After You File: The Investigation Process

Once a dispute is filed, the “chargeback” process begins. This is a structured sequence governed by card network rules (Visa or Mastercard).

Temporary Credits and Interest Suspensions

In many cases, Chase will issue a “temporary credit” to your account for the amount of the disputed charge. This ensures that you do not have to pay for the disputed item while the investigation is ongoing. Additionally, under the FCBA, you have the right to withhold payment for the disputed amount, and the bank cannot report that amount as delinquent to credit bureaus while the investigation is active. However, it is important to remember that this credit is provisional. If the merchant provides evidence that the charge was valid, Chase will “re-bill” the amount to your account.

Potential Outcomes and Rebuttals

The merchant has a set period (usually 30 to 45 days) to respond to the dispute.

- Merchant Accepts: They may choose not to fight the dispute, in which case your temporary credit becomes permanent.

- Merchant Challenges: They may provide evidence, such as a signed delivery receipt or a signed contract.

If the merchant challenges, Chase will notify you. You often have a second opportunity to provide a rebuttal. Read the merchant’s evidence carefully; they often use automated systems that might miss the specific nuance of your complaint (e.g., they provide proof of delivery, but your complaint was that the item inside was broken).

Proactive Financial Management: Avoiding Future Disputes

While knowing how to dispute a charge is a necessary defensive skill, proactive financial management can reduce the frequency and stress of these incidents.

Monitoring Accounts with Real-Time Alerts

The best way to catch a billing error or fraud is immediately after it happens. Through the Chase mobile app, you can set up “Push Notifications” for every transaction. If you receive a notification for a $200 charge while you are sitting on your couch, you can freeze your card instantly and initiate a dispute within minutes. This speed often makes the recovery process much smoother.

Understanding Merchant Names on Statements

One common source of “false positive” disputes is confusing merchant names. Many companies use a “Doing Business As” (DBA) name or a parent company name on credit card statements that differs from the brand name. For example, a charge from a local coffee shop might appear as “SRG Group LLC.” Before filing a dispute, a quick web search of the name on your statement can save you the time and effort of a mistaken dispute, which can sometimes lead to your account being flagged or your relationship with a merchant being terminated.

![]()

The Role of Virtual Cards and Digital Wallets

Using tools like Apple Pay, Google Pay, or Chase’s own digital wallet features can add a layer of security. These services use “tokenization,” meaning the merchant never receives your actual card number. This significantly reduces the risk of fraud, leaving you only to worry about legitimate merchant disputes rather than malicious identity theft.

In conclusion, disputing a charge with Chase is a fundamental right that protects your hard-earned money. By understanding the legal protections of the FCBA, utilizing Chase’s digital tools efficiently, and maintaining rigorous documentation, you can navigate financial discrepancies with confidence. In the ecosystem of personal finance, being an informed and assertive consumer is the ultimate safeguard for your economic well-being.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.