In the intricate world of personal finance, business operations, and investment strategies, the ability to accurately calculate and deduct percentages is not merely a mathematical exercise—it’s a foundational skill. From deciphering sale prices and understanding loan interest to calculating net profit and navigating investment returns, percentages are omnipresent. Mastering this seemingly simple arithmetic operation empowers individuals and businesses to make informed decisions, optimize financial outcomes, and avoid costly miscalculations. This guide delves into the core mechanics, diverse applications, and practical tools for confidently deducting percentages, ensuring you’re always in control of your financial figures.

The Core Mechanics: Understanding Percentage Deduction

At its heart, deducting a percentage from a number is about finding a portion of a whole and then removing that portion. While the concept is straightforward, precision is paramount in financial contexts.

What is a Percentage and Why Deduct It?

A percentage literally means “per one hundred.” It’s a way of expressing a number as a fraction of 100. For instance, 25% means 25 out of 100, or 25/100, which simplifies to 0.25 in decimal form. The act of deducting a percentage arises from various financial scenarios where a portion of a value needs to be reduced. This could be a discount on a purchase, a tax applied to income, a fee subtracted from a service, or a reduction in an asset’s value. Without the ability to perform this calculation accurately, one would struggle to understand the true cost of items, the actual take-home pay, or the real value of an investment after various adjustments. It’s the gateway to understanding net figures across almost every financial domain.

The Fundamental Formula: Step-by-Step Breakdown

There are two primary methods to deduct a percentage from a number, both yielding the same result, but offering slightly different conceptual paths.

Method 1: Calculate the Percentage Amount First, Then Subtract

- Convert the percentage to a decimal: Divide the percentage by 100.

- Example: 20% becomes 20 / 100 = 0.20

- Multiply the decimal by the original number: This gives you the actual amount of the percentage.

- Example: If the original number is $150, then 0.20 * $150 = $30

- Subtract this amount from the original number: This is your final result.

- Example: $150 – $30 = $120

Method 2: Calculate the Remaining Percentage Directly

- Determine the remaining percentage: If you’re deducting 20%, you’re left with 100% – 20% = 80%.

- Convert the remaining percentage to a decimal: Divide the remaining percentage by 100.

- Example: 80% becomes 80 / 100 = 0.80

- Multiply this decimal by the original number: This directly gives you the final amount after the deduction.

- Example: If the original number is $150, then 0.80 * $150 = $120

Method 2 is often more efficient as it combines steps, particularly useful in spreadsheet applications or mental calculations.

Practical Examples: Simple Deductions

Let’s apply these methods to a couple of basic financial scenarios:

-

Scenario 1: A Discounted Item

- You want to buy a jacket priced at $200, and it’s on sale for 25% off.

- Using Method 1: 25% as decimal is 0.25. Discount amount = 0.25 * $200 = $50. Sale price = $200 – $50 = $150.

- Using Method 2: Remaining percentage = 100% – 25% = 75%. As decimal is 0.75. Sale price = 0.75 * $200 = $150.

-

Scenario 2: A Service Fee

- A consultant charges $500 for a service, but a 10% administrative fee is deducted upfront.

- Using Method 1: 10% as decimal is 0.10. Fee amount = 0.10 * $500 = $50. Net payment = $500 – $50 = $450.

- Using Method 2: Remaining percentage = 100% – 10% = 90%. As decimal is 0.90. Net payment = 0.90 * $500 = $450.

Everyday Applications in Personal Finance

The ability to deduct percentages accurately profoundly impacts personal financial management, from budgeting and shopping to understanding your income.

Navigating Sales and Discounts: Smart Shopping

One of the most common applications of percentage deduction is in retail. Sales, coupons, and loyalty programs frequently offer discounts expressed as percentages. Understanding how to calculate these deductions allows you to:

- Verify advertised prices: Ensure you’re being charged correctly at the checkout.

- Compare deals: Sometimes, a “30% off” might be better than “$50 off,” depending on the original price.

- Plan your spending: Accurately estimate the final cost of items before committing to a purchase.

- Avoid overspending: Stick to your budget by knowing the true cost after discounts.

For example, if a television is $800 with a 15% discount, knowing that 0.85 * $800 = $680 ensures you don’t budget for $700 thinking it’s “around” 15% off.

Calculating Taxes and Tips: Budgeting for Obligations

Taxes and tips are two crucial areas where percentage deduction is indispensable for budgeting and maintaining good financial health.

- Sales Tax: While often added on top of a price, understanding how to factor it in (or deduct it mentally for pre-tax cost) is vital. More importantly, income tax deductions, property tax reductions, or tax credits sometimes involve deducting a percentage from your total tax liability or income.

- Tips/Gratuity: When you want to tip a specific percentage (e.g., 18% or 20%) on a bill, you’re essentially performing this calculation. If your meal is $75 and you want to leave a 20% tip, you calculate 0.20 * $75 = $15, then add it to the bill. Or, if the bill already includes a service charge expressed as a percentage, you need to verify it and potentially deduct it from what you planned to tip additionally.

Understanding Salary Deductions and Net Pay

For most employees, gross pay is rarely the amount that hits their bank account. Various deductions, often percentage-based, reduce the gross figure to arrive at net pay. These can include:

- Income Tax: Calculated as a percentage of taxable income.

- Social Security & Medicare: Fixed percentage deductions in many countries.

- Retirement Contributions: Often a percentage of salary (e.g., 5% to a 401k).

- Health Insurance Premiums: Sometimes a percentage of salary or a flat fee that impacts your overall percentage take-home.

By understanding these deductions, you can accurately forecast your take-home pay, create realistic budgets, and assess the true impact of salary changes or new benefits. If your gross pay is $4,000 per month and combined deductions (taxes, benefits, retirement) amount to 28%, your net pay is $4,000 * (1 – 0.28) = $4,000 * 0.72 = $2,880.

Managing Loan Payments and Interest Reductions

Loans, mortgages, and credit card balances often involve interest calculations that can be seen as either adding or deducting percentages depending on the context. While interest is typically added to a principal, understanding how to calculate it (e.g., a 5% interest rate on a loan balance) is the precursor to understanding how much is being deducted from your potential savings or future wealth due to interest payments. Furthermore, when negotiating a loan, understanding a percentage-point reduction in interest rates directly translates to a percentage deduction in the total cost of borrowing over the loan’s lifetime.

Business and Investment Insights

Beyond personal finance, deducting percentages is a cornerstone of business operations and strategic investment decisions.

Profit Margins and Markdowns: Pricing Strategies

For businesses, calculating profit margins and implementing markdowns are daily activities that rely heavily on percentage deduction.

- Markdowns: When inventory isn’t moving, businesses apply markdowns (e.g., “20% off all winter coats”). Calculating the markdown price is essential for clearing stock while minimizing losses. If an item costs $100 and is marked down by 30%, the new price is $70.

- Profit Margins: While gross profit margin is typically calculated as (Revenue – Cost of Goods Sold) / Revenue, understanding how various expenses (expressed as percentages of revenue) deduct from gross profit to arrive at net profit is critical. For instance, if operating expenses are 20% of revenue, that’s a direct deduction from the gross profit pool.

Commissions and Fees: Understanding Business Costs

Many business models involve commissions, referral fees, or administrative charges, all expressed as percentages.

- Sales Commissions: Salespeople often earn a percentage of their sales. If a product sells for $1,000 and the salesperson gets a 10% commission, $100 is deducted from the revenue to pay the commission.

- Platform Fees: Online marketplaces (like Etsy, Amazon, eBay) or payment processors (like PayPal, Stripe) charge a percentage of each transaction. If you sell an item for $50 and the platform takes a 5% fee, you receive $50 * 0.95 = $47.50. Accurately accounting for these deductions is vital for setting prices and understanding profitability.

Investment Returns and Portfolio Adjustments

In the investment world, percentages are the language of performance, risk, and fees.

- Investment Losses: If a stock you own drops by 15%, you need to calculate the new value. A $1,000 investment losing 15% is now worth $1,000 * 0.85 = $850.

- Management Fees: Many investment funds (mutual funds, ETFs) charge an expense ratio, which is an annual percentage deducted from your total investment. An expense ratio of 0.5% means that for every $10,000 invested, $50 is deducted annually in fees, impacting your net returns.

- Portfolio Rebalancing: Deciding to reduce exposure to a particular asset class often involves selling a percentage of that holding. For example, if you want to reduce your tech stock allocation from 30% to 20% of your portfolio, and your portfolio is $100,000, you need to know how much to sell.

Budgeting and Expense Management: Optimizing Cash Flow

Businesses, like individuals, rely on accurate percentage calculations for budgeting. If the marketing department’s budget is 15% of projected revenue, and revenue forecasts decline by 10%, you need to deduct that percentage from the marketing budget’s base. Managing expenses by category (e.g., “rent is 10% of total overhead”) helps in strategic cost-cutting, where identifying areas to reduce a percentage of spending can significantly improve cash flow.

Tools and Techniques for Efficient Calculation

While mental math is useful for quick estimates, for accuracy and handling larger numbers, leveraging technology is key.

The Power of Calculators and Spreadsheets (Excel/Google Sheets)

- Basic Calculators: Most modern calculators have a “%” button. To deduct a percentage, you typically enter the original number, then “-“, then the percentage, then “%”, then “=”. For example,

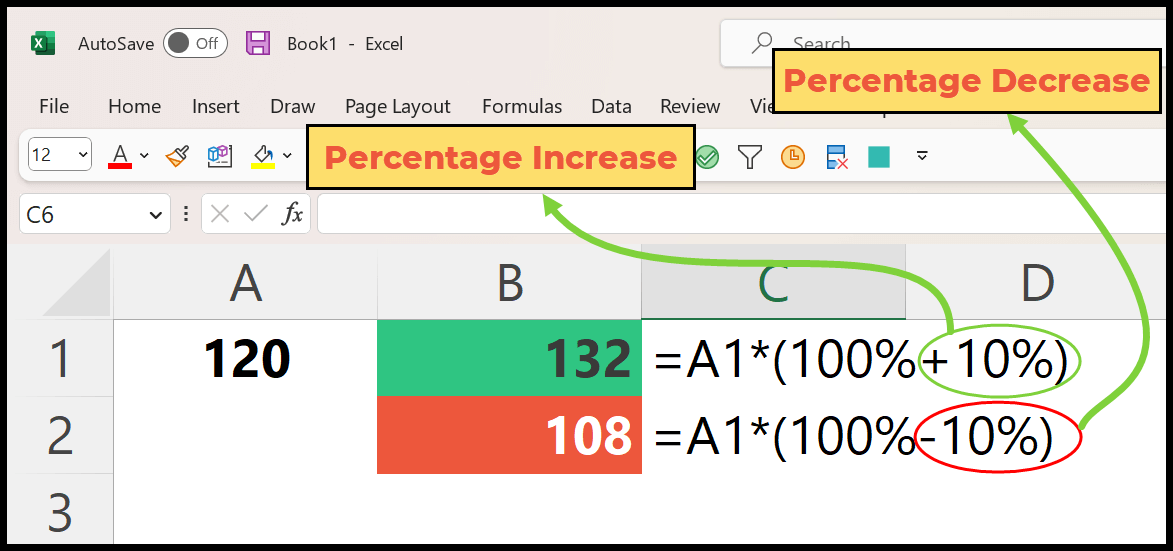

150 - 20 % =. This directly applies Method 2. - Spreadsheets (Excel/Google Sheets): These are invaluable for financial calculations, especially when dealing with multiple deductions or large datasets.

- To calculate a 20% deduction from a number in cell A1:

=A1 * (1 - 0.20)or=A1 * 0.8(Method 2)=A1 - (A1 * 0.20)(Method 1)

- Spreadsheets allow you to change the percentage easily in a separate cell and have all dependent calculations update automatically, making them perfect for “what-if” financial scenarios.

- To calculate a 20% deduction from a number in cell A1:

Online Financial Tools and Apps

Many online budgeting tools, financial calculators, and banking apps incorporate percentage deductions directly into their features. For example, investment platforms will show your portfolio value after fees, or budgeting apps will automatically categorize transactions and show you what percentage of your income goes to different expense categories. Dedicated percentage calculators are also widely available online for quick, accurate calculations without needing to remember the formula.

Mental Math Shortcuts for Quick Estimates

While not for precise financial reporting, quick mental math can help you make on-the-spot decisions.

- Finding 10%: Move the decimal one place to the left. (e.g., 10% of $150 is $15).

- Finding 5%: Half of 10%. (e.g., 5% of $150 is $7.50).

- Finding 1%: Move the decimal two places to the left. (e.g., 1% of $150 is $1.50).

- Approximating: For 20% off $150, think “2 x 10% off” ($15 x 2 = $30). For 25% off, think “1/4 off” ($150 / 4 = $37.50). These mental shortcuts allow for rapid evaluation of discounts or potential costs while shopping or making quick financial assessments.

Common Mistakes and How to Avoid Them

Even with simple operations, errors can creep in, especially in high-stakes financial scenarios. Awareness of these common pitfalls can save significant headaches and money.

Confusing Percentage Points with Percentages

This is a subtle but critical distinction. A “percentage point” refers to the absolute difference between two percentages, while a “percentage change” refers to the relative change.

- Example: If an interest rate drops from 10% to 8%, that’s a 2 percentage point decrease. It is not a 2% decrease. It’s a (2/10) = 20% decrease in the interest rate itself.

Misunderstanding this can lead to drastic miscalculations of financial impacts, particularly in investment returns or loan interest changes. When deducting a percentage from a number, ensure you’re applying the correct percentage value, not a percentage point difference.

Incorrect Base Values: What Are You Deducting From?

One of the most frequent errors is applying the percentage deduction to the wrong base number.

- Example: A common mistake is deducting two consecutive percentages from the original number rather than from the new, reduced number. If an item is $100 and has a 10% discount, then an additional 5% discount, you do not deduct 15% from $100.

- Correct: $100 – 10% = $90. Then $90 – 5% = $85.50.

- Incorrect: $100 – 15% = $85.

Always ensure the percentage is applied to the current or correct base value relevant to the specific step of the calculation.

Double-Checking Your Work: The Importance of Verification

In financial matters, complacency is costly. Always take an extra moment to verify your calculations, especially for significant transactions.

- Use two methods: If you calculate it one way, try a slightly different method or use a different tool (e.g., mental math, then a calculator) to confirm.

- Sense check: Does the answer make logical sense? If you deduct 20% from $100, the result should be less than $100, and significantly less if the percentage is large. An answer of $8,000 when deducting from $100 is an obvious error.

- Review source data: Ensure you’re using the correct original numbers and the correct percentages.

Mastering how to deduct a percentage from a number is more than just arithmetic; it’s a critical financial literacy skill. From making savvy purchasing decisions and accurately managing personal budgets to understanding complex business finance and investment scenarios, this seemingly simple calculation underpins a vast array of financial competence. By understanding the core mechanics, leveraging appropriate tools, and being mindful of common pitfalls, you can confidently navigate your financial journey, ensuring precision and control over every dollar.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.