For many individuals and business owners, taxes represent one of the single largest annual expenses. However, the American tax code is not merely a set of rules for collection; it is also a roadmap of incentives designed to encourage certain economic behaviors, such as saving for retirement, investing in healthcare, and supporting charitable causes. Decreasing your taxable income is not about evasion; it is about tax avoidance—the legal process of organizing your financial affairs to minimize tax liability.

By understanding the distinction between gross income and adjusted gross income (AGI), you can implement strategies that keep more of your hard-earned money in your pocket. This guide explores the most effective, professional-grade strategies to lower your taxable income through retirement planning, healthcare accounts, strategic deductions, and investment management.

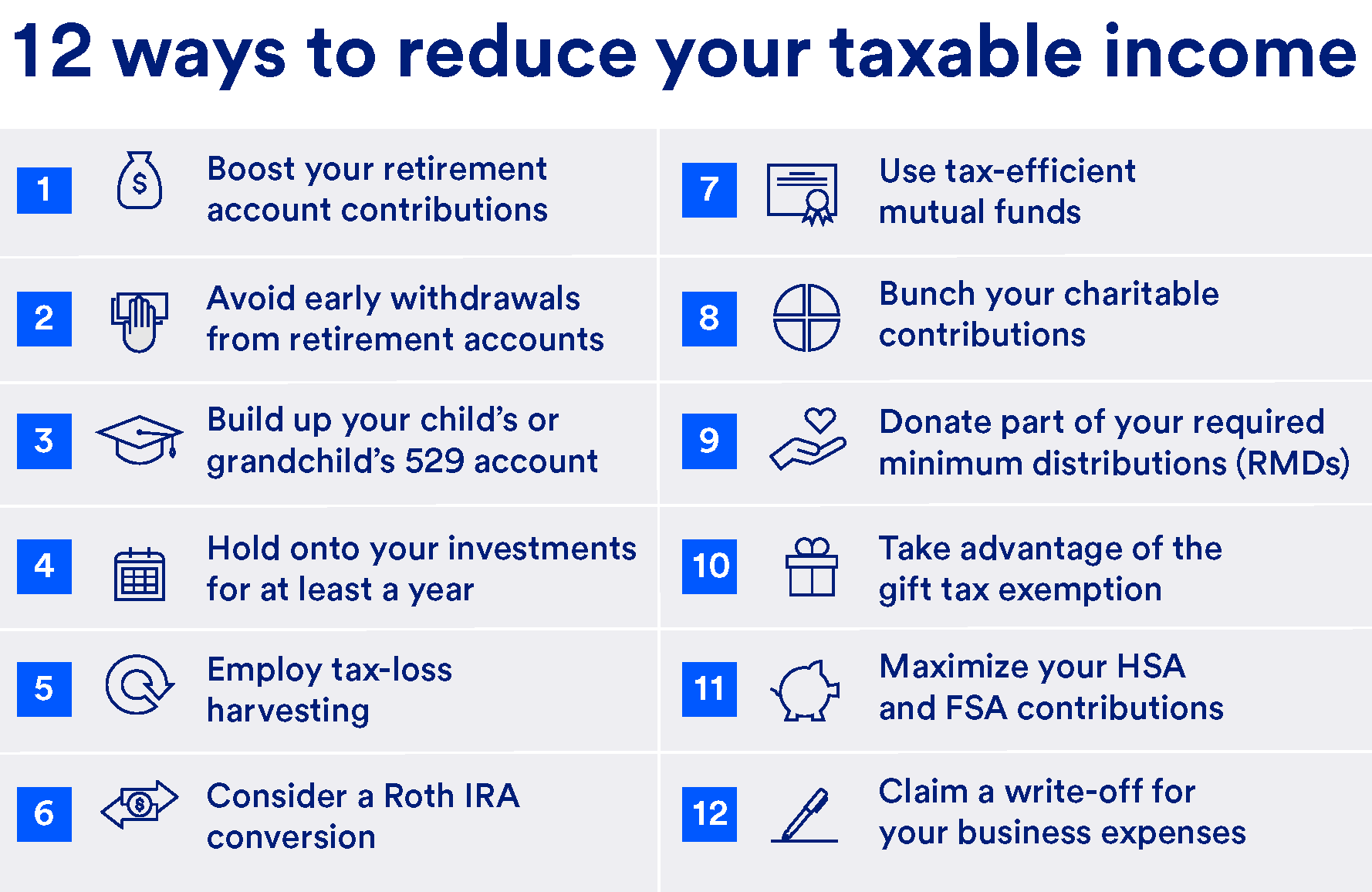

Maximizing Contributions to Retirement Accounts

One of the most effective ways to lower your taxable income is by “paying your future self.” The IRS provides significant incentives for individuals to save for retirement by allowing them to deduct contributions from their current year’s gross income.

Employer-Sponsored Plans: 401(k) and 403(b)

The 401(k) (for private sector employees) and the 403(b) (for non-profit and public sector employees) are the workhorses of tax reduction. Contributions to these plans are typically made on a “pre-tax” basis. This means that if you earn $100,000 and contribute $20,000 to your 401(k), the IRS only sees $80,000 of taxable income.

Beyond the immediate tax break, these accounts offer tax-deferred growth. You do not pay capital gains taxes or dividend taxes on the growth within the account annually; instead, you only pay taxes when you withdraw the funds during retirement, at which point you may be in a lower tax bracket.

Traditional IRAs and the Power of Pre-Tax Dollars

If you do not have access to an employer-sponsored plan, or if you want to save beyond what your employer offers, a Traditional Individual Retirement Account (IRA) is a powerful tool. Depending on your income level and whether you or your spouse are covered by a retirement plan at work, your contributions to a Traditional IRA may be fully or partially tax-deductible. Unlike a Roth IRA—which is funded with after-tax dollars and offers no immediate tax break—the Traditional IRA directly reduces your AGI for the year in which you contribute.

The Self-Employed Advantage: SEP IRAs and Solo 401(k)s

For entrepreneurs, freelancers, and small business owners, the opportunities for tax reduction are even greater. A Simplified Employee Pension (SEP) IRA allows you to contribute a significant percentage of your net self-employment income, often much higher than standard IRA limits. Similarly, a Solo 401(k) allows you to contribute both as an employee and as an employer, effectively doubling your ability to shield income from taxation. These vehicles are essential for high-earning professionals looking to mitigate a heavy tax burden.

Utilizing Health and Flexible Spending Accounts

Healthcare costs are a significant burden for many, but the tax code offers several ways to pay for these expenses using untaxed dollars, thereby reducing your overall taxable income.

The Triple Tax Advantage of Health Savings Accounts (HSAs)

The HSA is widely considered the most tax-advantaged account in existence. To qualify, you must be enrolled in a High Deductible Health Plan (HDHP). The HSA offers a “triple” tax benefit:

- Contributions are 100% tax-deductible (or made pre-tax through payroll), lowering your taxable income.

- The money grows tax-free within the account.

- Withdrawals for qualified medical expenses are tax-free.

If you do not use the funds, they roll over indefinitely, unlike other healthcare accounts. For savvy investors, the HSA can function as a secondary retirement account; after age 65, you can withdraw funds for any reason (though non-medical withdrawals are taxed as ordinary income, similar to a Traditional IRA).

Flexible Spending Accounts (FSAs) for Healthcare and Childcare

If you do not have an HDHP, you may still have access to a Flexible Spending Account (FSA) through your employer. FSAs allow you to set aside pre-tax dollars for medical, dental, and vision expenses.

Furthermore, many employers offer a Dependent Care FSA. This allows parents to set aside pre-tax income to pay for childcare services, such as daycare, preschool, or summer camps. Since these contributions are taken out before taxes are calculated, they directly lower your reported taxable income. The caveat is the “use it or lose it” rule, which generally requires you to spend the funds within the plan year.

Strategic Deductions and Tax Credits

Lowering taxable income often requires choosing the right path during the tax filing process: taking the standard deduction or itemizing your deductions.

Choosing Between Standard and Itemized Deductions

The Tax Cuts and Jobs Act significantly increased the standard deduction, making it the most beneficial choice for the majority of taxpayers. However, if your specific expenses—such as mortgage interest, state and local taxes (SALT), and medical expenses—exceed the standard deduction threshold, itemizing can further reduce your taxable income.

Professional tax planning involves “bunching” deductions. For example, if you are close to the threshold, you might choose to make two years’ worth of charitable contributions in a single tax year to surpass the standard deduction limit and maximize your tax savings for that period.

Charitable Giving and Donor-Advised Funds

Charitable donations to qualified 501(c)(3) organizations are a primary way to reduce taxable income for those who itemize. For high-net-worth individuals, a Donor-Advised Fund (DAF) is an excellent tool. You can contribute a large sum to the fund—receiving an immediate tax deduction for the full amount—and then distribute that money to various charities over several years. This is particularly effective in a high-income year where you need a large deduction to move into a lower tax bracket.

Education Credits and Student Loan Interest

While credits (which reduce your tax bill dollar-for-dollar) are different from deductions (which reduce taxable income), they are both vital for financial efficiency. The Student Loan Interest Deduction allows you to subtract up to $2,500 of interest paid on qualified student loans from your income, even if you do not itemize. Additionally, the American Opportunity Tax Credit (AOTC) and the Lifetime Learning Credit (LLC) help offset the costs of higher education, effectively lowering the “net” cost of your taxes.

Investment-Based Tax Reduction Strategies

Your investment portfolio offers several sophisticated avenues for managing and reducing taxable income. Proper “tax-loss harvesting” and understanding “holding periods” can significantly impact your year-end tax liability.

Tax-Loss Harvesting: Turning Losses into Wins

Tax-loss harvesting is the practice of selling investments that are currently at a loss to offset capital gains realized elsewhere in your portfolio. If your total capital losses exceed your capital gains, you can use the remaining loss to offset up to $3,000 of your ordinary taxable income. Any losses beyond that $3,000 can be carried forward to future tax years. This strategy allows investors to maintain their market exposure (by purchasing a similar, but not identical, asset) while lowering their current tax bill.

Holding for the Long Term: Capital Gains Tax Optimization

The duration for which you hold an asset changes how it is taxed. Assets held for less than a year are subject to short-term capital gains tax, which is the same as your ordinary income tax rate. However, assets held for longer than a year are taxed at long-term capital gains rates (0%, 15%, or 20%), which are significantly lower than ordinary income tiers. By strategically timing the sale of assets, you can ensure that your investment income is taxed at the most favorable rate possible.

Deductions for Business Owners and Side Hustlers

With the rise of the gig economy and remote work, more people than ever are eligible for business-related tax deductions. These deductions are subtracted from your gross business income, lowering the “net” profit that is actually subject to tax.

The Qualified Business Income (QBI) Deduction

Under Section 199A, many sole proprietors, partners, and S-corporation owners can deduct up to 20% of their qualified business income from their taxes. This is a massive “above-the-line” deduction that was created to provide tax parity between small businesses and large corporations. While there are income limits and phase-outs based on the type of profession, the QBI deduction remains one of the most powerful tools for reducing taxable income for the self-employed.

Documenting Business Expenses and the Home Office Deduction

Every dollar spent on your business is a dollar that isn’t taxed. This includes marketing, software subscriptions, professional services, and travel. If you use a portion of your home exclusively for business, you may also qualify for the Home Office Deduction. This allows you to deduct a portion of your rent or mortgage interest, utilities, and insurance. The key to these deductions is meticulous record-keeping; by using dedicated financial tools to track every expense, you ensure that you aren’t paying taxes on money that was actually a business cost.

In conclusion, decreasing your taxable income is a proactive, year-round endeavor. It requires a combination of disciplined retirement saving, smart healthcare choices, and strategic investment management. By leveraging these professional financial strategies, you can minimize your tax liability, maximize your wealth-building potential, and ensure that your financial plan is as efficient as possible.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.