In the contemporary financial landscape, the way we interact with money has undergone a radical transformation. Gone are the days of carrying bulky wallets filled with cash or waiting days for a check to clear. The rise of peer-to-peer (P2P) payment platforms has revolutionized personal finance, making transactions as simple as sending a text message. At the forefront of this digital revolution is Venmo. Originally a simple tool for splitting dinner bills, Venmo has evolved into a comprehensive financial ecosystem. Understanding how to create and manage a Venmo account is no longer just a technical convenience; it is a foundational skill for modern financial literacy.

The Evolution of Peer-to-Peer Payments in Modern Personal Finance

Before diving into the mechanics of account creation, it is essential to understand the role Venmo plays in the broader financial sector. Venmo, owned by PayPal, has bridged the gap between traditional banking and the social media age. It operates on a “social payment” model, which has significantly influenced how younger generations perceive and handle money.

Why Venmo is a Cornerstone of the Digital Wallet

Venmo has become synonymous with casual financial transactions. Its ubiquity is its greatest strength; because “everyone has it,” it serves as a friction-less medium for the exchange of value. For the individual, it functions as a digital wallet that holds a balance, connects to traditional bank accounts, and even offers a physical debit card. In the context of personal finance, Venmo acts as a liquid asset repository, allowing for immediate movement of funds without the bureaucratic hurdles of wire transfers or the physical limitations of ATMs.

Assessing the Financial Benefits of P2P Apps

The primary financial benefit of using Venmo is efficiency. Velocity of money—how quickly money moves through the economy or your own accounts—is a key concept in finance. Venmo increases this velocity by allowing for instant settlements. Furthermore, for those managing a strict budget, Venmo provides a transparent, digital paper trail of every “micro-transaction” that might otherwise go unrecorded when using cash. By integrating Venmo into your financial toolkit, you gain a clearer view of your discretionary spending habits.

Step-by-Step: Establishing Your Venmo Financial Profile

Creating a Venmo account is a straightforward process, but from a financial management perspective, it requires attention to detail to ensure your assets are protected and your account is fully functional for higher-volume transactions.

Downloading the App and Initial Registration

To begin, download the Venmo app from the official Google Play Store or Apple App Store. While there is a web interface, Venmo is designed primarily for mobile use.

- Open the App: Select your preferred sign-up method (Email or Facebook). For professional financial tracking, using a dedicated email address is often recommended.

- Create a Secure Password: As this is a financial tool, utilize a robust, unique password.

- Phone Verification: Venmo requires a valid U.S. mobile number that can receive SMS codes. This is a critical security measure to prevent unauthorized account creation and to facilitate two-factor authentication.

Verifying Your Identity for Enhanced Transaction Limits

One of the most overlooked steps in the setup process is identity verification. Under federal law (specifically the USA PATRIOT Act), financial institutions are required to obtain, verify, and record information that identifies each person who opens an account.

To increase your weekly spending limits and to be able to hold a “Venmo Balance,” you must verify your identity. Navigate to the “Settings” menu and select “Identity Verification.” You will be asked to provide:

- Your legal full name.

- Your Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN).

- Your date of birth.

- Your home address.

Completing this step transitions your account from a basic “user” to a verified financial entity, allowing for larger transfers and access to the Venmo Debit Card.

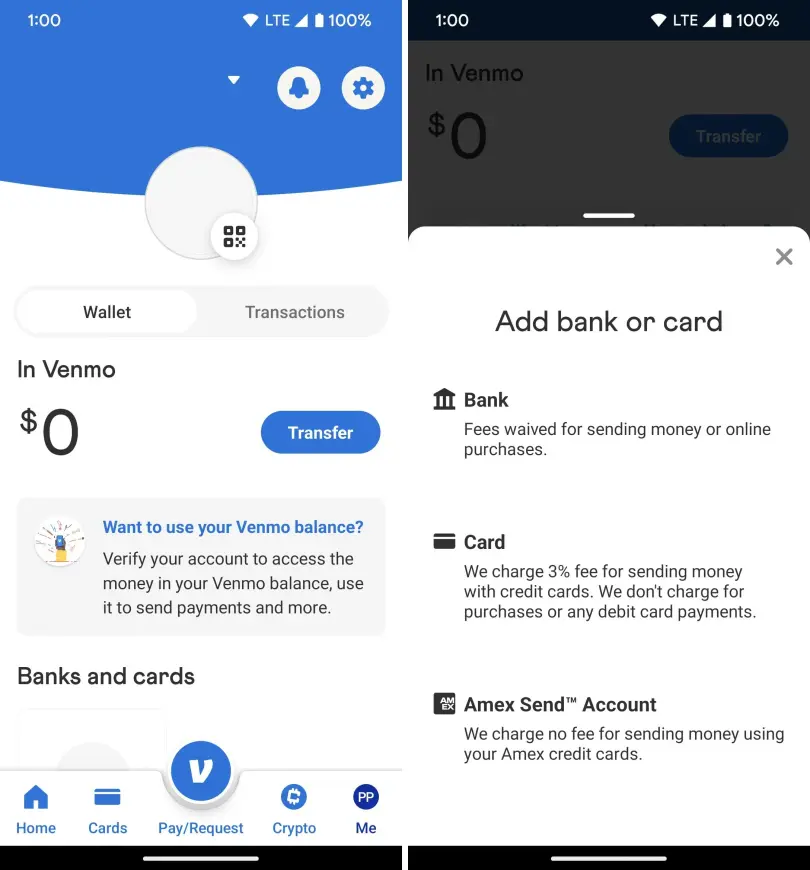

Linking Bank Accounts vs. Credit Cards: A Cost-Benefit Analysis

Once your profile is set, you must link a source of funds. This is where strategic financial decision-making comes into play.

- Bank Accounts (Checking/Savings): Linking a bank account via the Plaid interface or manual verification is the most cost-effective method. Transfers from your bank to Venmo (and vice versa) are typically free.

- Debit Cards: These offer the same fee-free benefits as bank accounts but allow for “Instant Transfers” (for a small percentage fee) if you need to move money from Venmo to your bank in minutes rather than days.

- Credit Cards: Venmo allows you to link credit cards, but this comes with a 3% transaction fee. From a wealth-management perspective, using a credit card on Venmo is generally discouraged unless necessary, as the fees quickly outweigh any potential rewards points or cash back.

Maximizing Security and Privacy in the Digital Financial Ecosystem

In the digital age, financial security is synonymous with digital security. Because Venmo is a “social” app, it defaults to settings that may not be appropriate for everyone’s financial privacy needs.

Configuring Multi-Factor Authentication (MFA)

The first line of defense is MFA. Venmo uses your phone number as a second factor, but you should also enable biometric locks. In the “Settings” menu under “FaceID & PIN,” ensure that you require a biometric scan or a passcode every time the app is opened. This prevents unauthorized access if your phone is lost or stolen.

Managing Privacy Settings for Financial Discretion

Venmo’s unique feature is its social feed, where transactions are visible to friends or the public. From a professional finance standpoint, sharing your transaction history is rarely beneficial.

To secure your data:

- Go to Settings > Privacy.

- Change the default transaction setting from “Public” or “Friends” to “Private.”

- This ensures that only you and the other participant in the transaction can see the details. Protecting your financial data is a key component of preventing social engineering attacks and identity theft.

Safeguarding Against Common Digital Payment Scams

As you begin using your account, be aware of the “accidental deposit” scam. A stranger may send you money “by mistake” and ask you to send it back. Often, they are using a stolen credit card to send the initial funds. When the bank eventually reverses the fraudulent charge, you will be out the money you “returned.” Always contact Venmo support rather than interacting directly with strangers regarding unexpected funds.

Leveraging Venmo for Advanced Financial Management

Once your account is established and secured, you can look beyond simple transfers and utilize Venmo as a legitimate tool for business and investment.

Utilizing Venmo for Business and Side Hustles

For freelancers and small business owners, Venmo offers dedicated Business Profiles. This is distinct from a personal account and allows you to accept payments for goods and services legally. Business profiles provide professional features like performance dashboards, QR code kits for in-person sales, and the ability to appear in the “business search” within the app. From an accounting perspective, keeping business transactions separate from personal ones is vital for clean bookkeeping.

Understanding Tax Implications and Reporting Requirements

The IRS has updated reporting requirements (Form 1099-K) for P2P payment processors. If you use a Venmo Business Profile or receive payments marked as “Goods and Services” that exceed certain thresholds, Venmo is required to report that income to the IRS. As a user, it is your responsibility to maintain accurate records. Using Venmo’s built-in “Export to CSV” feature can simplify your tax preparation by providing an organized list of your business-related inflows and outflows.

Exploring Crypto and Savings Features within the Platform

Venmo has expanded its financial reach by allowing users to buy, sell, and hold cryptocurrencies like Bitcoin and Ethereum directly within the app. For those looking to diversify their portfolio with small amounts of capital, this provides a low-barrier entry point. Additionally, the Venmo Credit Card offers “Cash Back to Crypto,” which automatically invests your monthly rewards into a cryptocurrency of your choice. While these are high-risk assets, having them integrated into your primary payment app allows for a more holistic (if aggressive) approach to digital asset management.

Conclusion: Integrating Venmo into Your Financial Strategy

Creating a Venmo account is the first step toward participating in a more agile and interconnected financial world. By following the proper setup procedures—verifying your identity, choosing the right funding sources, and locking down your privacy settings—you transform a simple app into a powerful financial instrument.

Whether you are using it to manage shared household expenses, scale a side hustle, or simply move money between accounts with ease, Venmo offers a level of flexibility that traditional banking struggles to match. However, with this convenience comes the responsibility of vigilance. Treat your Venmo account with the same gravity as a traditional bank account, and it will serve as a reliable, efficient, and essential component of your personal financial infrastructure.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.