Embarking on the journey of creating a small business is an endeavor that promises both immense rewards and significant challenges. While the allure of entrepreneurship often stems from a passion for an idea or a desire for independence, the bedrock upon which any successful venture is built is its financial viability and astute monetary management. In an increasingly dynamic global economy, understanding the financial intricacies of launching, operating, and growing a small business is not just an advantage; it is an absolute necessity. This comprehensive guide will navigate the essential financial considerations for aspiring entrepreneurs, ensuring you lay a solid economic foundation for your small business.

Laying the Financial Foundation: From Idea to Viability

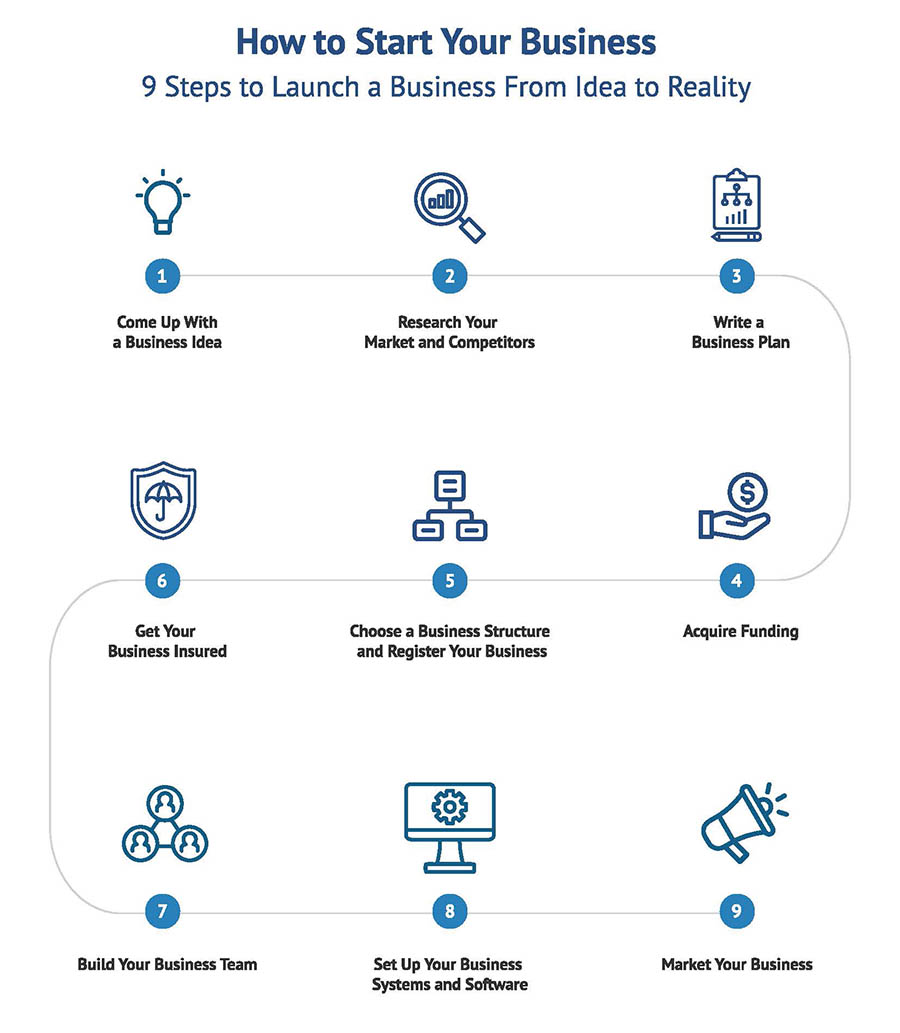

The genesis of any small business begins with an idea, but transforming that idea into a sustainable enterprise requires rigorous financial scrutiny from the outset. Before investing time, effort, and capital, it’s crucial to ascertain the economic potential of your concept.

Validating Your Business Idea with a Profitability Lens

Before passion takes over, put your idea through a profitability test. This involves more than just identifying a market need; it’s about determining if that need can be met profitably.

- Market Size and Demand Analysis: Quantify the potential customer base and their willingness to pay. Research existing competitors and analyze their pricing structures, revenue models, and market share. Is there enough demand to generate sufficient revenue to cover costs and yield a profit?

- Revenue Streams and Pricing Strategy: How will your business make money? Identify potential revenue streams (e.g., direct sales, subscriptions, advertising, consulting). Develop a preliminary pricing strategy that balances perceived value, production costs, and competitive positioning. Consider different pricing models (cost-plus, value-based, competitive pricing) and their implications for your bottom line.

- Cost Analysis and Break-Even Point: Detail all potential costs – both one-time startup expenses (equipment, legal fees, initial inventory) and ongoing operational costs (rent, utilities, salaries, marketing). Calculate your break-even point: the volume of sales needed to cover all costs. This critical metric helps determine if your projected sales figures are realistic enough to reach profitability.

- SWOT Analysis with a Financial Focus: Assess your Strengths, Weaknesses, Opportunities, and Threats, specifically from a financial perspective. What are your financial strengths (e.g., low overhead potential)? What are your financial weaknesses (e.g., high upfront costs)? What financial opportunities exist (e.g., grants, emerging markets)? What financial threats loom (e.g., economic downturns, rising material costs)?

Crafting a Robust Business Plan: The Financial Blueprint

A business plan is more than just a document; it’s your strategic financial roadmap. It compels you to think through every aspect of your venture, particularly its economic dimensions, before you commit substantial resources.

- Executive Summary (Financial Highlights): Briefly outline your business concept, market opportunity, key financial projections (e.g., projected revenue, profit margins, funding requirements), and the overall financial appeal of your venture.

- Market Analysis (Target Audience and Revenue Potential): Elaborate on your market research, identifying your target demographic, their purchasing power, and how your product/service will capture their expenditure.

- Management Team (Financial Acumen): Highlight the financial expertise within your team or advisors, demonstrating the capability to manage funds effectively.

- Service or Product Line (Cost and Pricing): Detail your offerings, emphasizing their cost of production, proposed pricing, and potential profit margins.

- Marketing and Sales Strategy (Budget and ROI): Outline how you plan to attract customers, including your marketing budget, expected customer acquisition costs (CAC), and projected return on investment (ROI) for marketing efforts.

- Financial Projections: This is the heart of the financial plan.

- Startup Costs: A detailed list of all expenses incurred before opening.

- Sales Forecasts: Realistic projections of revenue for the first 1-3 years, broken down monthly or quarterly.

- Profit and Loss (P&L) Statement: Projected income statement showing revenues, costs, and net profit or loss over time.

- Cash Flow Statement: Forecasts the movement of cash in and out of your business, critical for managing liquidity.

- Balance Sheet: A snapshot of your business’s assets, liabilities, and equity at a specific point in time.

- Break-Even Analysis (Revisited): A more refined calculation based on your detailed projections.

- Funding Request (If Applicable): Clearly state the amount of funding required, how it will be used, and the expected return for investors or the repayment plan for lenders.

Understanding Startup Costs and Initial Capital Needs

Accurately estimating your startup costs is paramount to avoiding undercapitalization, a common pitfall for new businesses.

- Fixed vs. Variable Costs: Differentiate between fixed costs (rent, insurance, loan payments) that remain constant regardless of production volume, and variable costs (raw materials, production labor) that fluctuate with output.

- One-Time vs. Ongoing Expenses: Categorize costs as either one-time outlays (e.g., legal fees for incorporation, initial equipment purchase, website development) or recurring operational expenses (e.g., salaries, utilities, marketing spend).

- Working Capital: Beyond the initial setup, you’ll need a reserve of cash to cover operating expenses during the initial period before your business becomes profitable. This is your working capital and is often underestimated. A good rule of thumb is to have 3-6 months of operating expenses saved.

- Contingency Fund: Always budget for the unexpected. A contingency fund, typically 10-20% of your total startup costs, acts as a financial buffer for unforeseen expenses or delays.

Securing Your Capital: Funding Strategies for Small Businesses

Once you’ve quantified your capital needs, the next step is to explore the various avenues for securing the necessary funds. The best option depends on your business type, risk tolerance, and access to resources.

Bootstrapping and Personal Investment: The Lean Startup Approach

Bootstrapping means funding your business primarily through personal savings, credit, or the initial revenues generated by the business itself. It’s often the leanest and most common starting point for small businesses.

- Personal Savings: Using your own money provides complete control and avoids debt. However, it exposes personal assets to business risk.

- Personal Credit Cards/Lines of Credit: Can provide quick access to funds but come with high interest rates and the risk of accumulating personal debt. Use with extreme caution and only for short-term needs.

- Friends and Family: Often a source of patient capital with flexible terms, but mixing personal relationships with business can be complex. Formalize any agreements with clear terms.

- Pre-sales/Customer Deposits: If possible, secure pre-orders or deposits from customers before fully launching. This validates demand and provides upfront capital.

- Bartering/Sweat Equity: Exchange services or labor for goods/services, or invest your own unpaid labor to reduce initial cash outlay.

Exploring Debt Financing: Loans, Lines of Credit, and Microloans

Debt financing involves borrowing money that must be repaid, typically with interest, within a specified timeframe.

- Traditional Bank Loans: Commercial banks offer various loan products for small businesses, often requiring a solid business plan, collateral, and a good personal credit score. Examples include term loans (fixed repayments over time) and revolving lines of credit (flexible access to funds up to a certain limit).

- SBA-Backed Loans: The U.S. Small Business Administration (SBA) doesn’t lend directly but guarantees a percentage of loans made by participating lenders. This reduces risk for lenders, making it easier for small businesses to qualify. SBA loans often have favorable terms and lower down payments.

- Microloans: Offered by non-profit organizations, microloans are small loans (typically under $50,000) for startups and small businesses, often with less stringent requirements than traditional banks. They are valuable for businesses with limited collateral or credit history.

- Equipment Financing: Loans specifically for purchasing business equipment, where the equipment itself serves as collateral.

- Invoice Factoring: Selling your outstanding invoices to a third party at a discount to get immediate cash. Useful for businesses with long payment terms.

Navigating Equity Funding and Grant Opportunities

Equity financing involves selling a portion of your company ownership in exchange for capital. Grants, on the other hand, are funds that don’t need to be repaid.

- Angel Investors: Wealthy individuals who invest their own money in early-stage companies, often in exchange for equity. They typically provide not just capital but also mentorship and industry connections.

- Venture Capital (VC) Firms: Professional investment firms that fund high-growth potential startups in exchange for significant equity. VC funding is less common for typical small businesses and is usually sought by companies with disruptive technology or rapid scalability potential.

- Crowdfunding: Raising small amounts of capital from a large number of people, often through online platforms.

- Reward-based crowdfunding: Supporters receive a product or service in return for their contribution (e.g., Kickstarter).

- Equity crowdfunding: Supporters receive a small stake in the company (requires compliance with specific regulations).

- Grants: Non-repayable funds awarded by government agencies, foundations, or corporations for specific purposes. Eligibility criteria can be very strict, often tied to specific industries (e.g., tech, scientific research, social impact) or demographics (e.g., women-owned, veteran-owned businesses). Research available grants diligently, as they are highly competitive.

Establishing Financial & Legal Structure for Growth

The financial implications of your business’s legal structure are profound, impacting liability, taxation, and administrative burden. Choosing wisely from the outset can save significant time and money down the line.

Choosing the Right Business Entity for Tax Efficiency and Liability

Your business structure dictates how you file taxes, your personal liability for business debts, and the administrative complexity.

- Sole Proprietorship: Easiest to set up, minimal legal formalities. Income and expenses are reported on your personal tax return (Schedule C). However, there’s no legal distinction between you and your business, meaning personal assets are at risk.

- Partnership: Similar to a sole proprietorship but with two or more owners. Profits and losses are passed through to the partners’ personal tax returns. Still carries unlimited personal liability for partners, although limited partnerships (LPs) or limited liability partnerships (LLPs) offer some liability protection.

- Limited Liability Company (LLC): Offers the liability protection of a corporation while allowing profits and losses to be passed through to owners’ personal tax returns, avoiding “double taxation.” Provides flexibility in management and is popular for small businesses.

- Corporation (C-Corp or S-Corp):

- C-Corporation: A separate legal entity from its owners, offering the strongest liability protection. Subject to “double taxation” – the corporation pays taxes on its profits, and shareholders pay taxes again on dividends received.

- S-Corporation: Avoids double taxation by passing profits and losses directly to the owners’ personal income without being subject to corporate tax rates. Has stricter requirements than an LLC, such as limits on the number and type of shareholders.

Consulting with an accountant and a business attorney is highly recommended to select the most financially and legally advantageous structure for your specific situation.

Essential Financial Registrations, Licenses, and Insurance

Compliance with various regulations is crucial for avoiding penalties and ensuring smooth financial operations.

- Federal Tax ID (EIN): A federal employer identification number (EIN) is required for most businesses, especially if you plan to hire employees, operate as a corporation or partnership, or file certain tax returns.

- State and Local Licenses/Permits: Research state and local requirements, which vary widely by industry and location. These can include general business licenses, professional licenses, sales tax permits, health permits, and zoning permits.

- Business Bank Account: Separate your personal and business finances immediately. A dedicated business bank account simplifies accounting, helps track expenses, and provides a professional image.

- Business Insurance: Protect your assets from unforeseen events. Essential types include:

- General Liability Insurance: Covers claims of bodily injury or property damage caused by your business.

- Professional Liability Insurance (E&O): For service-based businesses, covers claims of negligence or errors in professional services.

- Property Insurance: Covers damage to your business property (e.g., office, equipment, inventory).

- Workers’ Compensation Insurance: (If you have employees) Covers medical treatment and lost wages for employees injured on the job.

- Business Interruption Insurance: Replaces lost income if your business has to temporarily close due to covered perils.

Setting Up Your Business Banking and Accounting Systems

Efficient financial management hinges on well-organized banking and robust accounting practices.

- Choose the Right Bank: Select a bank that offers business-friendly services, competitive fees, and convenient access. Consider merchant services if you plan to accept credit card payments.

- Accounting Software: Implement reliable accounting software (e.g., QuickBooks, Xero, FreshBooks) from day one. This will help you track income and expenses, manage invoicing, reconcile bank accounts, and generate financial reports. Automating these processes saves time and reduces errors.

- Chart of Accounts: Set up a clear chart of accounts to categorize all your financial transactions consistently. This is essential for accurate financial reporting and tax preparation.

- Payroll System: If you have employees, establish a payroll system that handles withholding taxes, benefits, and direct deposits accurately and in compliance with labor laws.

- Invoice and Payment Tracking: Develop a system for sending professional invoices, tracking payments received, and following up on overdue accounts.

Mastering Business Finance: Day-to-Day Operations and Profitability

Effective financial management is an ongoing process that directly impacts your business’s ability to survive and thrive. It involves vigilant monitoring, strategic decision-making, and proactive planning.

Developing Effective Pricing Strategies and Revenue Models

Your pricing directly impacts your revenue and profitability. It’s not a one-time decision but an evolving strategy.

- Cost-Plus Pricing: Adding a markup percentage to the cost of your product or service. Simple but may not reflect market value.

- Value-Based Pricing: Pricing based on the perceived value to the customer, often allowing for higher margins. Requires deep understanding of customer needs and competitive landscape.

- Competitive Pricing: Setting prices based on what competitors charge. Useful in highly competitive markets.

- Dynamic Pricing: Adjusting prices in real-time based on demand, supply, and other market factors.

- Subscription Models: Recurring revenue streams common in SaaS (Software as a Service) or content businesses.

- Freemium Models: Offering a basic service for free and charging for premium features.

- Bundling: Offering multiple products or services together at a lower combined price.

Regularly review and adjust your pricing based on market feedback, cost changes, and competitive actions.

Budgeting, Cash Flow Management, and Expense Control

These are the pillars of financial stability for any small business.

- Annual Operating Budget: Create a detailed budget outlining projected revenues and expenses for the year. Monitor actual performance against the budget monthly or quarterly and identify variances.

- Cash Flow Projections: Develop a 12-month rolling cash flow forecast to predict when cash will be coming in and going out. This helps identify potential cash shortages or surpluses, allowing for proactive planning (e.g., securing a line of credit, scheduling investments).

- Expense Tracking and Control: Implement strict expense tracking. Categorize every expense and look for opportunities to reduce costs without compromising quality or essential operations. Regularly review vendor contracts and negotiate better terms.

- Accounts Receivable Management: Efficiently manage the money owed to you by customers. Establish clear payment terms, send invoices promptly, and follow up on late payments professionally.

- Accounts Payable Management: Manage your obligations to suppliers and vendors. Take advantage of early payment discounts if cash flow allows, but always pay bills on time to maintain good vendor relationships and credit.

Understanding Financial Statements and Key Performance Indicators (KPIs)

Financial statements are your business’s health reports, and KPIs offer critical insights into specific aspects of performance.

- Profit and Loss (P&L) Statement: Shows your revenue, costs, and profit over a period. Helps assess profitability.

- Cash Flow Statement: Tracks cash inflows and outflows. Essential for managing liquidity.

- Balance Sheet: A snapshot of your assets, liabilities, and equity at a specific point in time. Shows your company’s financial health.

- Key Performance Indicators (KPIs):

- Gross Profit Margin: (Revenue – Cost of Goods Sold) / Revenue. Indicates the profitability of your core products/services.

- Net Profit Margin: Net Profit / Revenue. Shows overall profitability after all expenses.

- Operating Cash Flow: Cash generated from regular business operations.

- Customer Acquisition Cost (CAC): Total sales and marketing cost / Number of new customers.

- Customer Lifetime Value (CLTV): The total revenue a customer is expected to generate over their relationship with your business.

- Break-Even Point: Revisited periodically, especially with changes in costs or pricing.

- Debt-to-Equity Ratio: Total Liabilities / Shareholder Equity. Indicates financial leverage.

Regularly review these statements and KPIs to make informed decisions about pricing, cost reduction, investment, and growth strategies.

Strategic Tax Planning and Compliance

Tax obligations can be a significant burden if not managed effectively. Proactive tax planning is crucial.

- Understand Your Obligations: Be aware of federal, state, and local tax requirements, including income tax, self-employment tax, sales tax, payroll tax, and property tax.

- Record Keeping: Maintain meticulous records of all income and expenses. This is indispensable for accurate tax filing and for audit purposes.

- Deductions and Credits: Understand eligible business deductions (e.g., home office, business travel, professional development, depreciation) and tax credits to minimize your tax liability legally.

- Estimated Taxes: Pay estimated quarterly taxes if you expect to owe a certain amount, to avoid penalties.

- Professional Advice: Engage a qualified accountant or tax professional. They can provide invaluable advice on tax strategy, ensure compliance, and often identify deductions you might overlook.

Sustaining and Scaling Your Small Business Financially

Once your business is established and profitable, the focus shifts to sustainable growth and long-term financial health. This involves strategic reinvestment, disciplined debt management, and a forward-looking perspective.

Reinvesting Profits for Sustainable Growth

Profitable small businesses often face the decision of how to utilize their earnings. Reinvesting profits back into the business is a powerful way to fuel sustainable growth without incurring additional debt or diluting equity.

- Product/Service Development: Invest in R&D to enhance existing offerings or create new ones, staying competitive and expanding market reach.

- Marketing and Sales Expansion: Allocate funds to scale marketing campaigns, expand sales teams, or explore new distribution channels to acquire more customers.

- Operational Efficiency: Upgrade equipment, improve technology, or streamline processes to reduce costs and increase productivity.

- Talent Acquisition and Development: Hire key personnel, invest in employee training, or offer competitive benefits to attract and retain top talent.

- Working Capital Buffer: Strengthen your cash reserves to provide greater financial resilience against economic downturns or unexpected events.

Managing Debt and Optimizing Capital Structure

As your business grows, you may take on additional debt to finance expansion. Managing this debt wisely is critical.

- Debt-to-Equity Balance: Strive for an optimal balance between debt and equity financing. While debt can leverage returns, excessive debt can increase financial risk.

- Interest Rate Management: Monitor interest rates on your loans and explore opportunities to refinance at lower rates if possible.

- Debt Repayment Strategy: Develop a clear plan for paying down debt, prioritizing high-interest loans first.

- Credit Score Management: Maintain a strong business credit score by paying bills on time, managing credit utilization, and regularly reviewing your credit report. This is vital for securing favorable terms on future financing.

Exit Strategies and Valuation Considerations

Even if an exit is years away, understanding potential exit strategies and how your business will be valued can inform your financial decisions today.

- Selling the Business: This involves preparing your financials for potential buyers, highlighting profitability, strong cash flow, and growth potential. A clear valuation method (e.g., asset-based, earnings multiple, discounted cash flow) will be applied.

- Succession Planning: If you plan to pass the business to family or employees, financial planning will involve valuing the business for internal transfer, potentially setting up trusts, or employee stock ownership plans (ESOPs).

- Liquidation: In some cases, selling off assets and closing the business might be the most financially prudent option. Understanding the liquidation value of your assets is important.

- Building Value: Every financial decision, from managing expenses to generating revenue, contributes to the overall value of your business. Focus on building a financially robust and attractive enterprise from the start.

Creating a small business is a marathon, not a sprint, and its success is inextricably linked to sound financial principles. By diligently planning, securing appropriate funding, establishing robust financial structures, mastering day-to-day financial operations, and strategically managing growth, entrepreneurs can build not just a business, but a financially resilient and prosperous enterprise. The path is challenging, but with a deep understanding of its monetary dimensions, your small business can achieve enduring success.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.