In the landscape of personal finance, the difference between those who struggle and those who thrive is rarely just the size of their paycheck. Instead, it is the level of intentionality they apply to every dollar earned. A budget spreadsheet is not merely a document of past spending; it is a strategic roadmap for future wealth. By creating a customized spreadsheet, you transform abstract financial goals into a concrete, actionable plan. This guide provides an in-depth exploration of how to construct a professional-grade budget spreadsheet that serves as the foundation for your financial independence.

The Architectural Foundation: Defining Your Financial Categories

Before opening your software of choice, you must understand the categories that will drive your financial data. A spreadsheet is only as effective as the logic behind its structure. In the world of personal finance, we categorize transactions not just to see where the money went, but to understand the “why” behind our behavior.

Tracking Total Net Income

Your budget must begin with an accurate representation of your “bottom line” income. This is not your gross salary, but your net take-home pay after taxes, insurance premiums, and retirement contributions have been deducted. If you have multiple streams of income—such as a primary salary, a side hustle, or dividends—each should have its own row. This allows you to see the diversity of your income portfolio. Understanding the stability and timing of these inflows is the first step in ensuring your expenses never outpace your earnings.

Categorizing Fixed vs. Variable Expenses

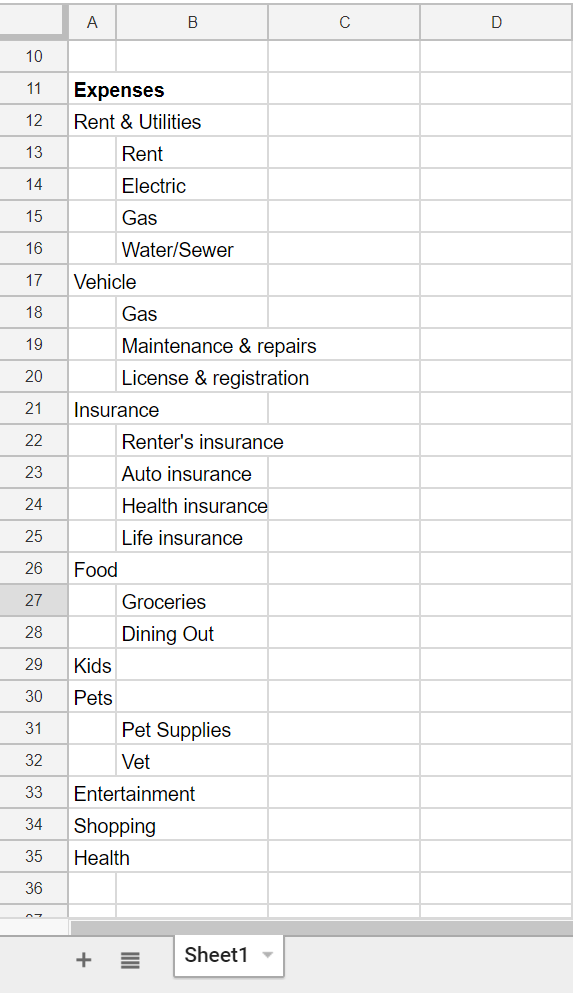

A professional budget distinguishes between fixed and variable costs. Fixed expenses are your non-negotiables: rent or mortgage payments, insurance, car payments, and subscription services. These are predictable and generally remain static month-to-month.

Variable expenses, however, are where the “battle” for your budget is won or lost. These include groceries, dining out, entertainment, and fuel. By separating these, you gain clarity on your “discretionary” spending. When you need to tighten your belt to reach a savings goal, the variable column is the first place you look for optimization.

Prioritizing Savings and Debt Obligations

In a sophisticated financial model, savings should not be treated as “whatever is left over.” Instead, savings and debt repayments should be treated as “invoices” you pay to your future self. Your spreadsheet should include specific rows for emergency funds, retirement accounts (like an IRA or 401k), and high-interest debt repayment. By placing these at the top of your expense list, you adopt the “pay yourself first” mentality, ensuring that your long-term financial health is never sacrificed for short-term consumption.

Building the Framework: Technical Setup and Formula Integration

Once the categories are defined, the actual construction of the spreadsheet begins. The goal is to create a tool that is both robust enough to handle complex data and simple enough to maintain consistently. Whether you use Excel, Google Sheets, or another financial tool, the logic remains the same.

Structural Layout and Data Architecture

A functional budget spreadsheet usually follows a monthly grid format. Your vertical columns should represent the months of the year, while your horizontal rows represent your categories (Income, Fixed Expenses, Variable Expenses, Savings).

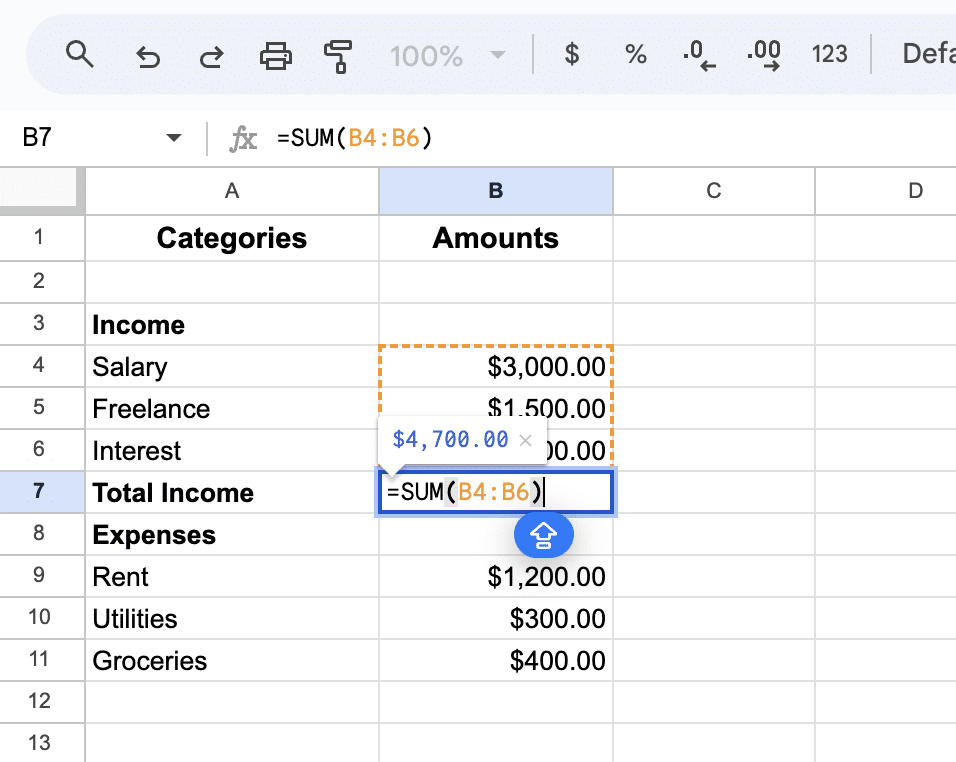

At the end of your rows, create a “Total” column that uses a SUM formula to aggregate your yearly spending. This macro-view is essential for spotting seasonal trends. For instance, you might notice that your utility bills spike in the summer or your “gift” category expands significantly in December. Anticipating these fluctuations allows for smoother cash flow management throughout the fiscal year.

Essential Formulas for Financial Accuracy

Automating your spreadsheet reduces the risk of human error and saves time. The most critical formula is the basic subtraction of total expenses from total income, often placed at the bottom of each month’s column. This is your “Net Cash Flow.”

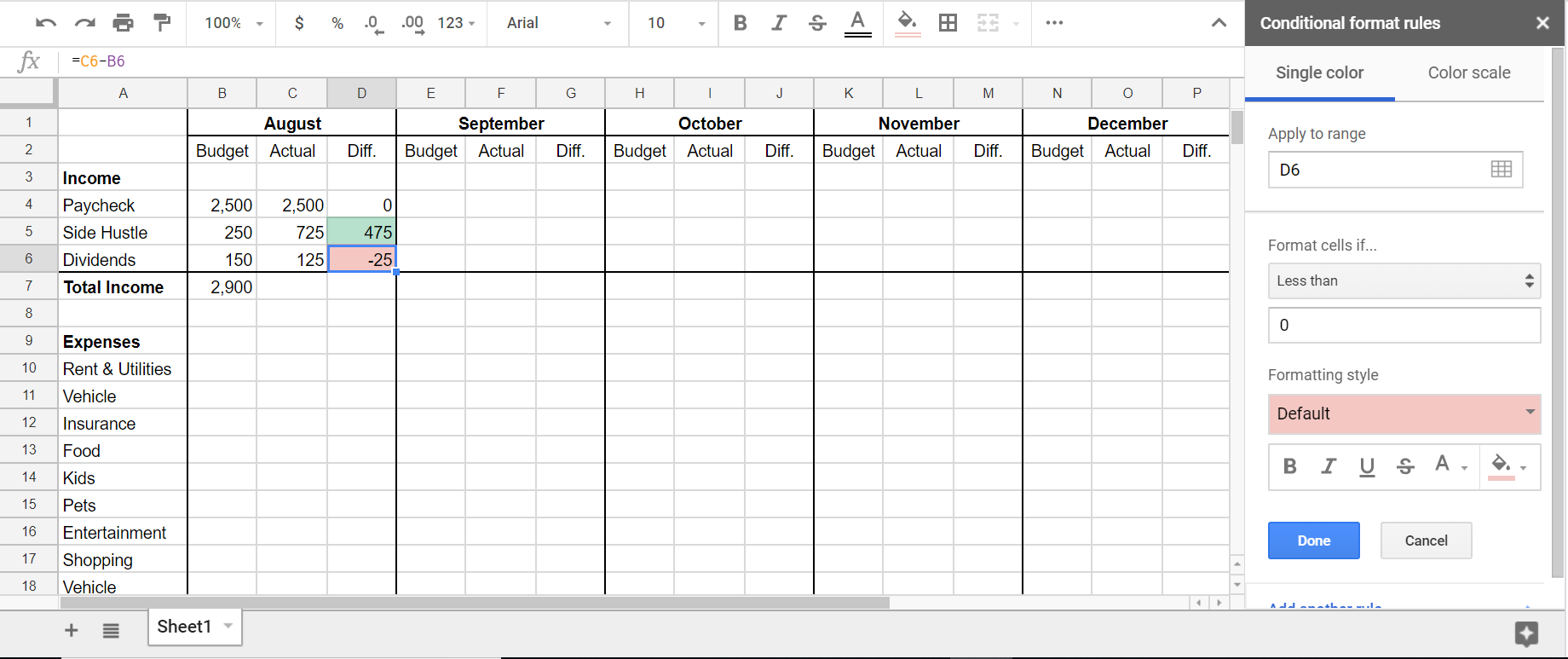

Beyond simple addition and subtraction, consider using “Variance Analysis.” Create a column for your “Planned” budget and a column for your “Actual” spending. By using a formula to calculate the difference (Actual – Planned), you can see exactly where you overspent. If your “Dining Out” cell turns red when you exceed your limit (using conditional formatting), it provides an immediate psychological cue to adjust your behavior for the remainder of the month.

Automating Data Entry and Maintenance

To ensure the longevity of your budgeting habit, the process must be frictionless. Many modern financial tools allow you to export CSV files from your bank account. You can set up a “Data Dump” tab in your spreadsheet where you paste these transactions. Using a lookup formula (like VLOOKUP or XLOOKUP), your main budget tab can automatically pull these numbers into the correct categories. This shifts your role from a manual data entry clerk to a high-level financial analyst.

Strategic Budgeting Methodologies for Wealth Accumulation

A spreadsheet is a tool, but the methodology you apply to it determines your financial trajectory. Depending on your goals—whether you are aggressively paying down debt or building a multi-million dollar portfolio—different budgeting styles may apply.

The 50/30/20 Rule for Balanced Allocation

For those seeking a balanced approach to personal finance, the 50/30/20 rule is a gold standard. Under this framework, 50% of your net income goes toward “Needs” (housing, utilities, basic groceries), 30% toward “Wants” (lifestyle choices, hobbies), and 20% toward “Financial Goals” (debt repayment and savings).

Your spreadsheet should include a “Summary” section that calculates these percentages automatically. If you find that your “Needs” are consuming 70% of your income, it is a clear indicator that you are “house poor” or over-leveraged, signaling a need for structural changes in your lifestyle.

Zero-Based Budgeting for Maximum Efficiency

Zero-based budgeting is the practice of assigning every single dollar a job until your total income minus your total expenses equals zero. This does not mean you have zero dollars in your bank account; it means every dollar is accounted for—whether it is going toward a coffee, a mortgage payment, or a brokerage account. This method is highly effective for those who feel their money “disappears” without knowing where it went. By tracking to a zero balance in your spreadsheet, you regain total command over your capital.

The Digital Envelope System

Historically, the envelope system involved putting physical cash into envelopes for different categories. In a digital spreadsheet, you can replicate this by creating “Sinking Funds.” These are rows dedicated to future, non-monthly expenses, such as a car repair fund or a vacation fund. By “billing” yourself a small amount each month for these categories, you ensure that when the expense eventually arrives, the money is already sitting in your account, preventing the need to rely on high-interest credit cards.

Advanced Analytics: Visualizing Your Path to Financial Independence

The true power of a budget spreadsheet lies in its ability to project the future. Once you have several months of data, you can move from reactive tracking to proactive wealth building.

Utilizing Charts and Graphs for Trend Analysis

Humans are visual creatures. A wall of numbers can be overwhelming, but a pie chart showing your expense distribution or a line graph showing your net worth growth over time is highly motivating.

In your spreadsheet, create a “Dashboard” tab. Use a bar chart to compare monthly income vs. expenses. If the “Income” bar is consistently much higher than the “Expense” bar, you are building a “Margin.” This margin is the engine of wealth. Seeing that gap widen over months and years provides the psychological reinforcement needed to stay disciplined.

The Monthly Review and Variance Audit

At the end of every month, conduct a “Financial Audit.” This is a professional review of your spreadsheet where you ask critical questions: Where did I exceed my budget? Was it a one-time emergency or a recurring lifestyle creep? Did I meet my savings goals?

Use this time to adjust your projections for the following month. If you consistently under-budget for groceries, stop trying to force a lower number and adjust the spreadsheet to reflect reality. A budget that is too restrictive will eventually be abandoned; a budget that is accurate is a tool you will use for a lifetime.

Tracking Net Worth and Long-Term Projections

While a budget tracks cash flow, your net worth tracks your overall financial health. Create a separate section in your spreadsheet to list your assets (cash, home equity, retirement accounts) and your liabilities (student loans, credit card debt, mortgages).

By linking your monthly budget “surplus” to your net worth tracker, you can see how every dollar you save today contributes to your long-term goal. You can even add a simple compound interest formula to project where your net worth will be in 10, 20, or 30 years based on your current savings rate. This transforms your spreadsheet from a boring chore into an inspiring vision of your financial freedom.

Conclusion: The Spreadsheet as a Catalyst for Growth

Creating a budget spreadsheet is one of the most significant steps an individual can take toward mastering their money. It is more than just a list of numbers; it is a manifestation of your values and your vision for the future. By carefully categorizing your finances, automating the technical framework, applying strategic methodologies, and visualizing your progress, you move from a state of financial uncertainty to a state of total control.

Wealth is not built by chance; it is built by design. Your spreadsheet is the blueprint for that design. As you consistently update and refine your financial model, you will find that you are no longer working for your money—instead, your money is working for you.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.